Introduction

Cryptocurrency has gained significant popularity in recent years as a decentralized form of digital currency. With its rising acceptance and use, it is important for individuals who own and trade cryptocurrencies to understand how they are taxed. The world of cryptocurrency taxation can be complex and confusing, but with the right knowledge and guidance, you can ensure compliance with tax regulations while minimizing your liabilities.

When it comes to cryptocurrency, the tax authorities treat it as property rather than traditional currency. This means that every time you sell, trade, or earn cryptocurrency, you may be subject to capital gains tax. The tax code surrounding cryptocurrency is evolving, and it’s crucial to stay up-to-date with the regulations specific to your country or jurisdiction. Failing to report cryptocurrency transactions accurately can result in penalties, audits, or legal consequences.

As the popularity and value of cryptocurrencies continue to rise, tax authorities worldwide are increasingly focusing on ensuring individuals and businesses properly report their cryptocurrency transactions. By understanding how cryptocurrency is taxed and taking the necessary steps to comply with tax laws, you can avoid potential problems and enjoy the benefits of this digital asset class.

In this article, we will explore the various aspects of cryptocurrency taxation, including how cryptocurrencies are taxed, factors to consider when calculating cryptocurrency taxes, and the steps involved in paying taxes on cryptocurrency. We will also discuss the importance of choosing the right tax professional, common mistakes to avoid, and the international tax implications of cryptocurrency. Additionally, we will provide some useful tax tools and resources to help you navigate the complexities of cryptocurrency taxation.

Understanding Cryptocurrency Taxes

When it comes to cryptocurrency, taxes can be a bit more complex than traditional forms of income. Cryptocurrencies like Bitcoin, Ethereum, and Litecoin are classified as property by tax authorities, which means they are subject to capital gains tax when bought, sold, or traded. However, the specifics of cryptocurrency taxation can vary from country to country, so it’s important to consult local tax regulations.

The tax implications of cryptocurrencies can be challenging to understand, especially for individuals who are new to the world of digital assets. Here are some key concepts to help you understand cryptocurrency taxes:

- Cryptocurrency as Property: The classification of cryptocurrencies as property means that any gain or loss from their sale, exchange, or use must be reported on your tax return.

- Capital Gains: When you sell or exchange your cryptocurrency at a higher price than what you initially paid for it, you realize a capital gain. Conversely, if you sell at a lower price, you incur a capital loss. These gains or losses are subject to tax.

- Short-term vs. Long-term Capital Gains: The duration for which you hold your cryptocurrency determines whether the capital gain is considered short-term or long-term. Short-term gains are typically taxed at a higher rate than long-term gains.

- Fair Market Value: The fair market value of a cryptocurrency is the value it would sell for on an open market. This value is used to determine your taxable gain or loss when you sell or exchange your cryptocurrency.

- Crypto-to-Crypto Transactions: Swapping one cryptocurrency for another is considered a taxable event. The fair market value of both cryptocurrencies at the time of the exchange is used to calculate your gain or loss.

Understanding these fundamental principles will help you navigate the intricacies of cryptocurrency taxation. It’s crucial to keep accurate records of your cryptocurrency transactions, including the date of acquisition, purchase price, fair market value, and date of sale or exchange. These records will be invaluable when it comes time to calculate your tax liabilities.

How Do Cryptocurrencies Get Taxed?

As mentioned earlier, cryptocurrencies are generally treated as property for tax purposes. This means that the tax implications for owning, buying, selling, and trading cryptocurrencies are similar to those for owning other types of property, such as stocks or real estate. Here are some ways in which cryptocurrencies get taxed:

- Capital Gains Tax: When you sell or exchange your cryptocurrency for a profit, you may be liable to pay capital gains tax on the realized gain. The tax rate can vary depending on the duration for which you held the cryptocurrency and your overall income tax bracket.

- Income Tax: If you receive cryptocurrencies as payment for goods or services, they are subject to income tax. The fair market value of the received cryptocurrency at the time of receipt will be considered as taxable income.

- Miner Taxes: If you are involved in cryptocurrency mining, the rewards or earnings you receive from mining activities may be subject to taxation. These earnings would be treated as self-employment income and subject to income tax and self-employment tax.

- Gifts and Donations: If you gift or donate cryptocurrency, there may be tax implications for both the donor and the recipient. In some countries, gifts may be subject to gift tax, and deductible donations may require proper documentation and valuation.

- Foreign Account Reporting: If you have cryptocurrency holdings in foreign exchanges or foreign accounts, there may be additional reporting requirements such as Foreign Bank Account Reports (FBAR) or Foreign Account Tax Compliance Act (FATCA) filings.

- State and Local Taxes: Apart from federal taxes, you may also have to consider state and local tax regulations when it comes to cryptocurrency taxation. Each jurisdiction may have its unique rules and requirements.

It’s important to note that tax regulations surrounding cryptocurrencies are continuously evolving, and it’s crucial to stay updated with the latest guidance from tax authorities in your country or jurisdiction. Hiring a qualified tax professional who specializes in cryptocurrency taxation can provide you with the necessary expertise and guidance to ensure compliance with tax laws while minimizing your tax liabilities.

Factors to Consider When Calculating Cryptocurrency Taxes

Calculating your cryptocurrency taxes can be a complex process, as numerous factors need to be taken into account. Properly accounting for these factors ensures accurate reporting and helps you minimize your tax liabilities. Here are some important factors to consider:

- Cost Basis Method: The cost basis is the original value of your cryptocurrency when it was acquired. There are several methods for calculating the cost basis, such as First-In-First-Out (FIFO), Last-In-First-Out (LIFO), Specific Identification, and Average Cost. Choosing the right cost basis method is crucial for determining your taxable gain or loss.

- Crypto-to-Crypto Transactions: When you exchange one cryptocurrency for another, it is essential to calculate the fair market value of both cryptocurrencies at the time of the transaction. This value will determine the taxable gain or loss for the transaction.

- Gifts and Donations: If you gift or donate cryptocurrency, you need to properly document and value the gift or donation. This ensures accurate reporting and potential tax benefits.

- Income from Mining and Staking: If you are involved in cryptocurrency mining or staking, you must accurately calculate the fair market value of the income generated. This income should be reported as self-employment income and subject to self-employment tax.

- Foreign Transactions: If you have engaged in cryptocurrency transactions with foreign exchanges or held cryptocurrency in foreign accounts, you may have additional reporting requirements. Familiarize yourself with the tax laws and reporting obligations of the countries involved.

- Reporting Deadlines: It is essential to stay aware of the reporting deadlines for cryptocurrency taxes. Failure to report on time may result in penalties or legal consequences.

- Record Keeping: Accurate and comprehensive record-keeping is crucial for calculating and reporting cryptocurrency taxes. Keep track of your transactions, acquisition dates, purchase prices, fair market values, and any other relevant details. This documentation will be helpful in case of audits or future tax calculations.

Calculating cryptocurrency taxes requires careful consideration of these factors and compliance with tax regulations in your country or jurisdiction. Seeking the guidance of a qualified tax professional who specializes in cryptocurrency taxation can help ensure accurate reporting and minimize your tax liabilities.

Steps to Pay Taxes on Cryptocurrency

Paying taxes on cryptocurrency can seem daunting, but following a systematic approach can simplify the process. Here are the steps you can take to pay taxes on your cryptocurrency:

- Educate Yourself: Start by educating yourself about the tax regulations and requirements specific to cryptocurrencies in your country or jurisdiction. Understand how cryptocurrencies are treated for tax purposes and familiarize yourself with the reporting obligations.

- Organize Your Records: Gather all the necessary records, including transaction history, acquisition dates, purchase prices, fair market values, and any other relevant information. Having organized records makes it easier to calculate your taxable gain or loss accurately.

- Calculate Your Taxable Gain or Loss: Use the information from your records and apply the appropriate cost basis method to calculate your taxable gain or loss for each cryptocurrency transaction.

- Complete the Required Tax Forms: Fill out the necessary tax forms as per the regulations in your country or jurisdiction. This may include reporting capital gains and losses on specific forms or schedules.

- Include Cryptocurrency Income: If you received cryptocurrency as income from mining, staking, or as payment for goods or services, report it as taxable income. Make sure to accurately calculate the fair market value at the time of receipt.

- Pay the Applicable Taxes: Determine the amount of tax you owe based on the calculated gain or income. Make the payment by the due date specified by your local tax authority.

- Keep Copies of Your Tax Returns and Payments: Maintain copies of your tax returns and proof of tax payments for future reference. These records are important in case of audits or inquiries by tax authorities.

- Consider Seeking Professional Help: If you find the process complex or want to ensure accuracy, consider consulting a qualified tax professional specializing in cryptocurrency taxation. They can provide guidance, help with calculations, and ensure compliance with tax regulations.

Following these steps will help you navigate the process of paying taxes on your cryptocurrency. Remember, it’s crucial to stay informed about any changes in tax regulations and seek professional advice if needed to ensure compliance and minimize your tax liabilities.

Choosing the Right Tax Professional for Cryptocurrency Taxes

Dealing with cryptocurrency taxes can be complex and challenging, and it’s often beneficial to seek the assistance of a qualified tax professional. Here are some factors to consider when choosing the right tax professional for your cryptocurrency tax needs:

- Specialization in Cryptocurrency Taxes: Look for a tax professional who has specific expertise and experience in handling cryptocurrency taxation. They should be up-to-date with the latest tax laws and regulations related to cryptocurrencies in your country or jurisdiction.

- Knowledge of Cost Basis Methods: Since calculating the cost basis of your cryptocurrency transactions is crucial, ensure that the tax professional is well-versed in different cost basis methods. They should be able to help you select the most advantageous method for your situation.

- Understanding of Crypto-to-Crypto Transactions: Cryptocurrency tax professionals should understand the tax implications of exchanging one cryptocurrency for another. They can help you accurately calculate the fair market value of both cryptocurrencies at the time of the transaction.

- Experience with International Tax Matters: If you have international cryptocurrency transactions or holdings, it’s essential to choose a tax professional experienced in dealing with international tax matters. They can guide you through the complexities of reporting and compliance obligations across borders.

- Reputation and Client Reviews: Research the tax professional’s reputation and read client reviews to ensure they have a track record of providing excellent service and expertise in cryptocurrency taxation.

- Accessibility and Availability: Consider the accessibility and availability of the tax professional. It’s crucial to choose someone who is responsive and available to address your questions and concerns during the tax-filing process.

- Transparent Fee Structure: Discuss the tax professional’s fee structure upfront and ensure that it aligns with the complexity of your situation. Transparency in fees will help you avoid any surprises later on.

- Commitment to Continuous Learning: Cryptocurrency taxation is a rapidly evolving field. Look for a tax professional who demonstrates a commitment to staying updated with the latest developments in cryptocurrency tax regulations.

Choosing the right tax professional is crucial to ensuring accurate reporting and minimizing your tax liabilities. By selecting an expert in cryptocurrency taxation, you can navigate the complexities of cryptocurrency taxes with confidence and ease.

Common Mistakes to Avoid When Paying Taxes on Cryptocurrency

When it comes to paying taxes on cryptocurrency, there are several common mistakes that individuals should be aware of in order to avoid potential issues with tax authorities. By understanding these mistakes and taking proactive measures, you can ensure compliance with tax regulations and minimize the risk of penalties or audits. Here are some common mistakes to avoid:

- Failure to Report All Transactions: One of the most common mistakes is not reporting all cryptocurrency transactions. Every sale, trade, or use of cryptocurrency should be accurately reported on your tax return. Even small transactions need to be accounted for.

- Ignoring Crypto-to-Crypto Transactions: Many individuals overlook or misunderstand the tax implications of exchanging one cryptocurrency for another. Remember that these transactions are taxable events, and you should calculate the gain or loss based on the fair market value of both cryptocurrencies at the time of the exchange.

- Inaccurate Reporting of Income: If you receive cryptocurrency as payment for goods or services, it is considered taxable income. Inaccurate reporting or failure to report this income can lead to penalties or audits. Accurately calculate the fair market value of the received cryptocurrency at the time of receipt.

- Incorrect Cost Basis Calculation: Choosing the wrong cost basis method or miscalculating the cost basis can result in inaccurate reporting of gains or losses. Take the time to understand the different cost basis methods and select the most appropriate one for your situation.

- Lack of Documentation and Recordkeeping: Failing to maintain accurate records of your cryptocurrency transactions can lead to difficulties in calculating your tax liability and supporting your reported figures. Keep comprehensive records of all transactions, including dates, purchase prices, fair market values, and any relevant supporting documentation.

- Overlooking International Tax Obligations: If you have cryptocurrency transactions or holdings in foreign exchanges or accounts, you may have additional reporting requirements. Be aware of international tax laws and fulfill all necessary reporting obligations to avoid legal consequences.

- Not Seeking Professional Guidance: Attempting to navigate cryptocurrency taxes without professional guidance can increase the likelihood of errors or misunderstandings. Consult with a qualified tax professional who specializes in cryptocurrency taxation to ensure accurate reporting and compliance with tax regulations.

Avoiding these common mistakes can help ensure that you accurately report your cryptocurrency transactions and pay the correct amount of taxes. Taking the time to understand the tax regulations, maintaining accurate records, and seeking professional assistance when needed can go a long way in minimizing the potential risks and challenges associated with cryptocurrency taxation.

Dealing with International Tax Implications of Cryptocurrency

The global nature of cryptocurrency presents challenges when it comes to international tax obligations. If you have cryptocurrency transactions or holdings in foreign exchanges or accounts, it is crucial to understand and address the international tax implications. Here are key considerations for dealing with international tax implications of cryptocurrency:

- Residency and Tax Treaties: Your residency status determines your tax obligations in a particular country. Understanding the tax rules and regulations of your resident country and any applicable tax treaties with the countries involved in your cryptocurrency transactions is essential.

- Reporting Foreign Accounts: If you hold cryptocurrency in foreign exchanges or foreign accounts, you may have additional reporting obligations. Familiarize yourself with the Foreign Bank Account Reports (FBAR) and Foreign Account Tax Compliance Act (FATCA) requirements and ensure compliance with the reporting deadlines.

- Exchange Rate Considerations: When dealing with international transactions in cryptocurrency, exchange rates play a significant role. Keep track of the exchange rates at the time of each transaction for accurate reporting and conversion to your resident country’s currency, if necessary.

- Tax Credits and Double Taxation: In cases where you pay taxes on the same cryptocurrency income in both your resident country and the foreign country, you may be eligible for tax credits to avoid double taxation. Consult a tax professional to determine the availability and utilization of tax credits.

- Permanent Establishment Risk: If you engage in cryptocurrency-related activities in a foreign country, there may be a risk of creating a permanent establishment. This could have tax implications, including the potential obligation to file tax returns and pay taxes in that country.

- Advice from International Tax Experts: Given the complexities of international tax obligations, seeking advice from tax professionals with expertise in cross-border taxation is highly recommended. They can provide assistance in understanding the specific tax implications and requirements of different jurisdictions.

- Complying with Local Regulations: Research and comply with the tax regulations and reporting requirements of the foreign country involved in your cryptocurrency transactions. Failure to comply with local tax laws can result in penalties, audits, or legal consequences.

Dealing with the international tax implications of cryptocurrency transactions requires careful attention to detail and adherence to the tax regulations of multiple jurisdictions. Engaging with international tax experts and maintaining accurate records of your cryptocurrency activities can help ensure compliance and mitigate potential risks associated with cross-border cryptocurrency taxation.

Cryptocurrency Tax Tools and Resources

Navigating the world of cryptocurrency taxation can be daunting, but there are several helpful tools and resources available to simplify the process and ensure compliance with tax regulations. Here are some cryptocurrency tax tools and resources you can leverage:

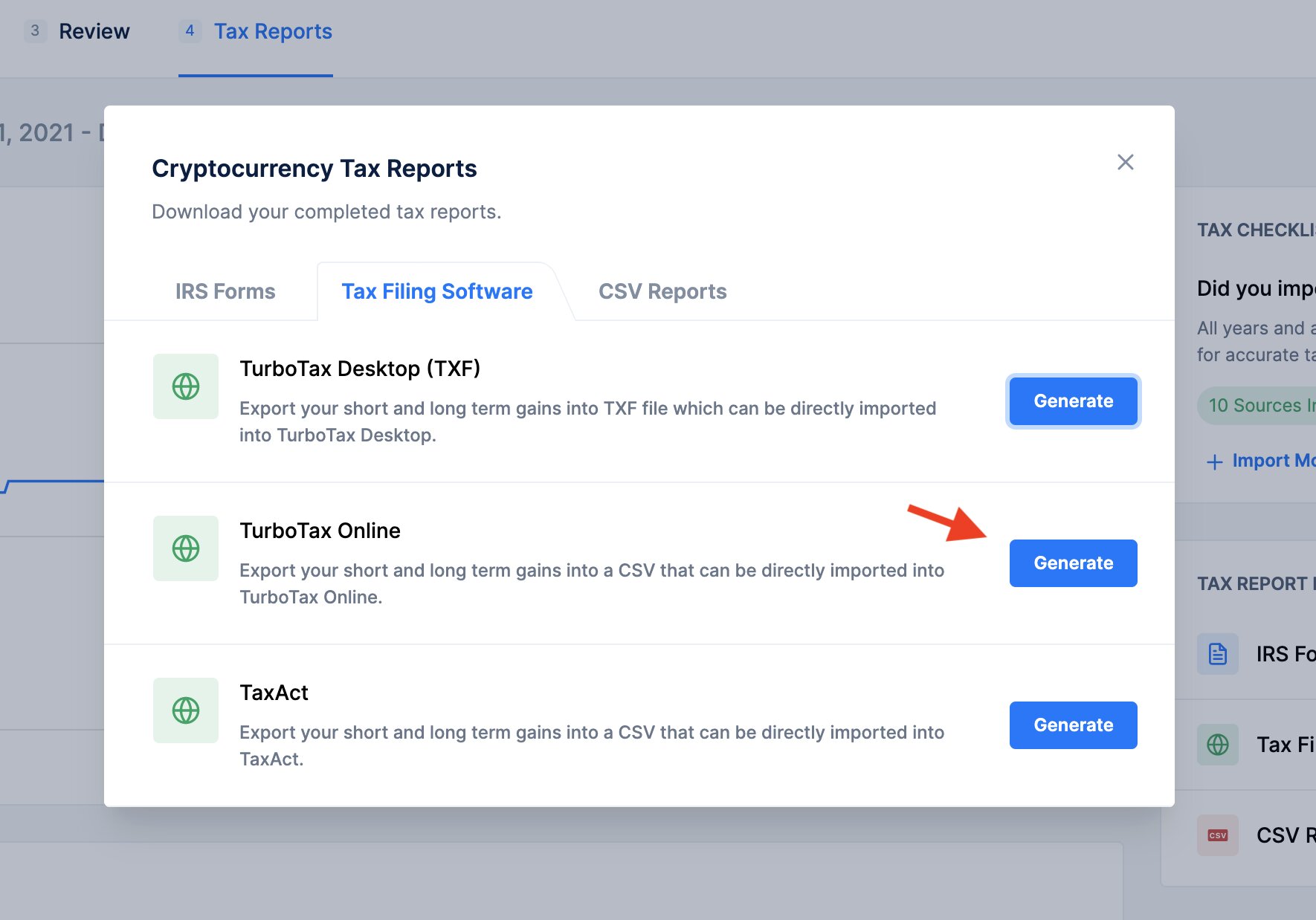

- Tax Software: Various tax software solutions are specifically designed to help crypto traders and investors calculate their tax liabilities. These platforms can integrate with popular cryptocurrency exchanges, centralize transaction data, and generate accurate tax reports.

- Cryptocurrency Tax Calculators: Online tax calculators provide a convenient way to estimate your cryptocurrency tax obligations. By inputting relevant transaction information, these calculators can assist in determining your taxable gains or losses.

- Blockchain Analysis Tools: Blockchain analysis tools can help track and analyze cryptocurrency transactions. These tools provide insights into your transaction history, aiding in the identification and organization of cryptocurrency transactions for tax reporting purposes.

- Tax Guides and Publications: Governments, tax authorities, and reputable accounting firms often publish guides and resources specific to cryptocurrency taxation. These resources provide insights into tax obligations, reporting requirements, and other helpful information.

- Online Cryptocurrency Tax Communities: Participating in online cryptocurrency tax communities and forums can be beneficial for gaining insights from others who have navigated the complexities of cryptocurrency taxation. Engaging with these communities allows you to share experiences, exchange tips, and learn from experts.

- Consulting a Tax Professional: Seeking the assistance of a tax professional who specializes in cryptocurrency taxation is always a wise choice. They can provide personalized guidance, answer your specific questions, and ensure accurate compliance with tax regulations.

- Stay Updated with Tax Laws: Cryptocurrency tax laws are continuously evolving. Stay informed about any changes or updates in the tax regulations of your country or jurisdiction. Subscribe to tax authority newsletters, follow reputable news sources, and consult professional advisors to ensure you remain up-to-date.

Utilizing these cryptocurrency tax tools and resources can significantly simplify the process of calculating and reporting your cryptocurrency tax obligations. Remember, each tool has its limitations and may not cover all aspects of your individual situation. Consulting with a tax professional is recommended to ensure accuracy and compliance with tax regulations specific to your circumstances.

Conclusion

Navigating the world of cryptocurrency taxation can be challenging, but with proper understanding and the right tools, you can ensure compliance and minimize your tax liabilities. Cryptocurrencies are treated as property for tax purposes, and it’s essential to report all cryptocurrency transactions accurately, including sales, trades, and income received.

When calculating cryptocurrency taxes, consider factors such as the cost basis method, crypto-to-crypto transactions, and accurate documentation of transactions. It’s important to be aware of common mistakes, such as failing to report all transactions or overlooking international tax implications.

To simplify the process, utilize cryptocurrency tax tools such as tax software, calculators, and blockchain analysis tools. Stay informed by consulting tax guides, subscribing to tax authority publications, and engaging with online cryptocurrency tax communities. Ultimately, consulting a tax professional who specializes in cryptocurrency taxation is highly recommended, as they can provide personalized guidance and ensure accurate compliance with tax regulations.

By taking proactive steps to understand and fulfill your cryptocurrency tax obligations, you can navigate the complexities of cryptocurrency taxation with confidence. Stay informed, maintain accurate records, and seek professional guidance when needed to ensure compliance and minimize your tax liabilities in this evolving landscape.