Introduction

Cryptocurrencies have gained immense popularity in recent years, offering individuals a decentralized and secure means of conducting financial transactions. However, with the rise in cryptocurrency investments and trading, it becomes crucial to understand the tax implications associated with these digital assets. Whether you are an avid crypto trader or a casual investor, it is essential to comprehend how much tax you may be liable to pay on your crypto gains.

Cryptocurrency taxation can be a complex subject, as tax laws and regulations vary between different countries. Governments are increasingly recognizing the need to tax crypto gains to ensure compliance and generate revenue. This means that, in most jurisdictions, crypto gains are subject to taxation, similar to other forms of investment income.

The tax treatment of cryptocurrency primarily depends on how it is classified, whether as a digital currency or a property. Understanding the classification and tax rates can help you accurately determine your tax liability and ensure that you meet your legal obligations.

To accurately calculate your tax liability, it is important to differentiate between short-term capital gains and long-term capital gains. The distinction is based on the period of time that you hold the cryptocurrency before selling or converting it back into fiat currency. Different tax rates may apply to each category, with long-term gains generally having a more favorable tax treatment.

In this article, we will explore the tax implications of cryptocurrency gains and guide you through the various factors to consider when determining your tax liability. We will also provide insights into reporting your crypto gains on your tax return and offer strategies to help you minimize your tax obligations. By understanding the tax rules surrounding cryptocurrency gains, you can ensure compliance and make informed decisions to maximize your profitability in the world of cryptocurrencies.

How is cryptocurrency taxed?

Cryptocurrencies are often treated as assets for tax purposes, similar to stocks or real estate. As a result, the tax treatment of cryptocurrencies varies depending on the jurisdiction and how they are used. Here are some common ways in which cryptocurrencies are taxed:

- Capital Gains Tax: In many countries, when you sell or dispose of your cryptocurrencies, you may be liable to pay capital gains tax on the profits. The capital gain is typically calculated by subtracting the cost basis (the amount you paid to acquire the cryptocurrency) from the selling price. The tax rate applied to capital gains depends on the holding period of the cryptocurrency, with short-term gains usually taxed at a higher rate than long-term gains.

- Income Tax: In some cases, cryptocurrencies may be subject to income tax if they are received as payment for goods or services, or as a form of income from mining activities. The value of the cryptocurrency at the time of receipt is usually considered taxable income. The tax rate applied to cryptocurrency income may vary depending on the individual’s overall income and tax bracket.

- Transaction Tax: Certain jurisdictions impose transaction taxes on cryptocurrency transactions. These taxes are typically a percentage of the transaction value and are levied on both the buyer and the seller. Transaction taxes are designed to generate revenue for the government and regulate the use of cryptocurrencies.

- Wealth Tax: In a few countries, individuals may be subject to wealth taxes based on the value of their cryptocurrency holdings. This means that you may need to report the value of your cryptocurrencies as part of your overall wealth and pay taxes accordingly.

It is important to note that tax regulations and laws regarding cryptocurrencies are evolving rapidly. Governments are continuously updating their tax guidelines to keep up with the changing landscape of digital currencies. It is advisable to consult with a tax professional or seek expert advice to ensure compliance with the latest tax requirements specific to your jurisdiction.

Short-term vs. long-term capital gains

When it comes to the taxation of cryptocurrency gains, understanding the distinction between short-term and long-term capital gains is essential. The holding period of a cryptocurrency determines which category it falls into and can have significant implications on the tax rate you are subject to.

Short-term capital gains apply to cryptocurrencies that have been held for less than a certain period, typically one year, before being sold or converted back into fiat currency. These gains are typically taxed at the individual’s ordinary income tax rate. In countries with progressive tax systems, the tax rate increases as the individual’s income level rises. Therefore, short-term gains on cryptocurrencies are generally subject to higher tax rates.

On the other hand, long-term capital gains are applied to cryptocurrencies that have been held for longer than the specified period, usually one year. Long-term gains often receive more favorable tax treatment, with tax rates that are lower than the ordinary income tax rates. This preferential treatment is designed to incentivize long-term investing and provide tax benefits to those who hold their investments for an extended period.

The exact tax rates for long-term capital gains on cryptocurrencies will depend on the specific tax laws and regulations of your jurisdiction. It is important to consult with a tax advisor or review the tax guidelines provided by the relevant tax authorities to determine the applicable tax rates for your crypto gains.

To illustrate the difference in tax treatment, let’s consider an example. Imagine you purchased one Bitcoin six months ago at a cost of $10,000, and it is now valued at $15,000. If you sell your Bitcoin today, the $5,000 profit would be considered a short-term capital gain and would be taxed according to your ordinary income tax rate. However, if you hold the Bitcoin for more than a year and then sell it, the $5,000 profit would be classified as a long-term capital gain and might be subject to a lower tax rate.

It is essential to keep track of the holding period of your cryptocurrencies to accurately determine whether the gains are short-term or long-term. Maintaining detailed records of your transactions, including purchase dates and sale dates, will help ensure accurate reporting and enable you to optimize your tax planning.

Determining your taxable crypto gains

To accurately determine your taxable crypto gains, you need to track and calculate the cost basis of your cryptocurrencies and consider any relevant deductions or adjustments. Here are some key factors to consider when determining your taxable crypto gains:

- Cost Basis: The cost basis of a cryptocurrency is the original purchase price plus any associated fees or expenses. It represents the amount of money you invested in acquiring the cryptocurrency. When you sell or dispose of your crypto assets, you need to subtract the cost basis from the selling price to calculate your capital gains.

- Specific Identification: In the case of selling or disposing of only a portion of your cryptocurrency holdings, you have the option to use a specific identification method for determining your cost basis. This method allows you to identify the specific units or coins you are selling, along with their associated cost basis. By doing so, you can potentially optimize your tax liability by selecting coins with the highest cost basis to minimize your gains.

- FIFO Method: The First-In, First-Out (FIFO) method is the default method used by many countries to calculate the cost basis of your cryptocurrencies. Under this method, when you sell or dispose of a portion of your holdings, the cost basis is determined based on the earliest acquired coins. This means that you are assumed to be selling the oldest units of your cryptocurrency first.

- Holding Period: As mentioned earlier, the holding period of your cryptocurrencies determines whether the gains are considered short-term or long-term capital gains. It is important to track the date of acquisition and sale of each cryptocurrency to accurately determine the applicable tax rates.

- Deductions and Adjustments: Depending on your jurisdiction, there may be certain deductions or adjustments that can be applied to your taxable crypto gains. For example, you may be able to deduct certain investment-related expenses or offset capital losses against capital gains. It is important to review the tax laws and regulations of your country to understand any deductions or adjustments that you may be eligible for.

To simplify the process of determining your taxable crypto gains, it is highly recommended to keep detailed records of all your cryptocurrency transactions. This includes information such as the date of acquisition, the cost basis of each unit, any associated fees or expenses, and the date of sale or disposal. By maintaining organized records, you can ensure accurate reporting, minimize errors, and facilitate the tax filing process.

Tax rates for crypto gains

The tax rates for cryptocurrency gains vary between different jurisdictions and can depend on various factors such as your income level, holding period, and the specific tax laws of your country. Here are some general considerations regarding the tax rates for crypto gains:

1. Ordinary Income Tax Rates: In some countries, cryptocurrencies are treated as ordinary income, subjecting them to the individual’s applicable income tax rate. This means that your crypto gains are taxed based on your income level, similar to how your regular salary or wages are taxed. The tax rate progressively increases as your income rises, with higher income individuals typically facing higher tax rates.

2. Capital Gains Tax Rates: In many jurisdictions, cryptocurrencies are subject to capital gains tax rather than ordinary income tax rates. The tax rates for capital gains can be more favorable, especially for long-term investments. Countries often differentiate between short-term capital gains (held for less than a year) and long-term capital gains (held for more than a year), with long-term gains generally being subject to lower tax rates. It is important to consult the tax laws of your specific jurisdiction to determine the applicable capital gains tax rates for crypto gains.

3. Progressive Tax Scales: Some countries have progressive tax rates that apply to both ordinary income and capital gains. This means that the tax rate increases as your income or gain amount increases. The tax scales may have different brackets or thresholds that determine the tax rate for each level of income or gain. Understanding the tax brackets and thresholds in your country will allow you to accurately calculate your tax liability on crypto gains.

4. Tax Exemptions or Discounts: Certain jurisdictions may provide tax exemptions or discounts for crypto gains up to a certain threshold. For example, there may be a specific amount of gains that are tax-free or subject to a reduced tax rate. These exemptions or discounts are often aimed at encouraging individuals to invest in cryptocurrencies and stimulate economic growth.

5. International Tax Considerations: If you engage in cross-border transactions involving cryptocurrencies, it is crucial to consider the tax implications of both your resident country and the country where the transaction occurs. Tax treaties and international tax regulations may impact the tax rates and reporting requirements for crypto gains in such cases.

It is important to note that tax laws and rates regarding cryptocurrencies can change, and the information provided here is for general guidance purposes. To accurately determine the tax rates applicable to your cryptocurrency gains, it is recommended to consult a tax professional or review the specific tax guidelines provided by the authorities in your jurisdiction.

Reporting your crypto gains on your tax return

Properly reporting your crypto gains on your tax return is crucial to ensure compliance with tax laws and avoid any potential penalties or legal issues. While the specific reporting requirements may vary based on your jurisdiction, here are some general guidelines to help you navigate the process:

1. Keep Detailed Records: It is essential to maintain organized and detailed records of all your cryptocurrency transactions. This includes information such as the date of acquisition or receipt, the cost basis, the date of sale or disposal, and the proceeds received. Having accurate records will help you calculate your gains accurately and provide supporting documentation if required.

2. Determine the Cost Basis: Calculate the cost basis of your cryptocurrencies, taking into account the original purchase price, any associated fees or expenses, and any relevant adjustments or deductions allowed by the tax regulations in your jurisdiction. This cost basis will be used to determine your capital gains or losses upon the sale or disposal of your crypto assets.

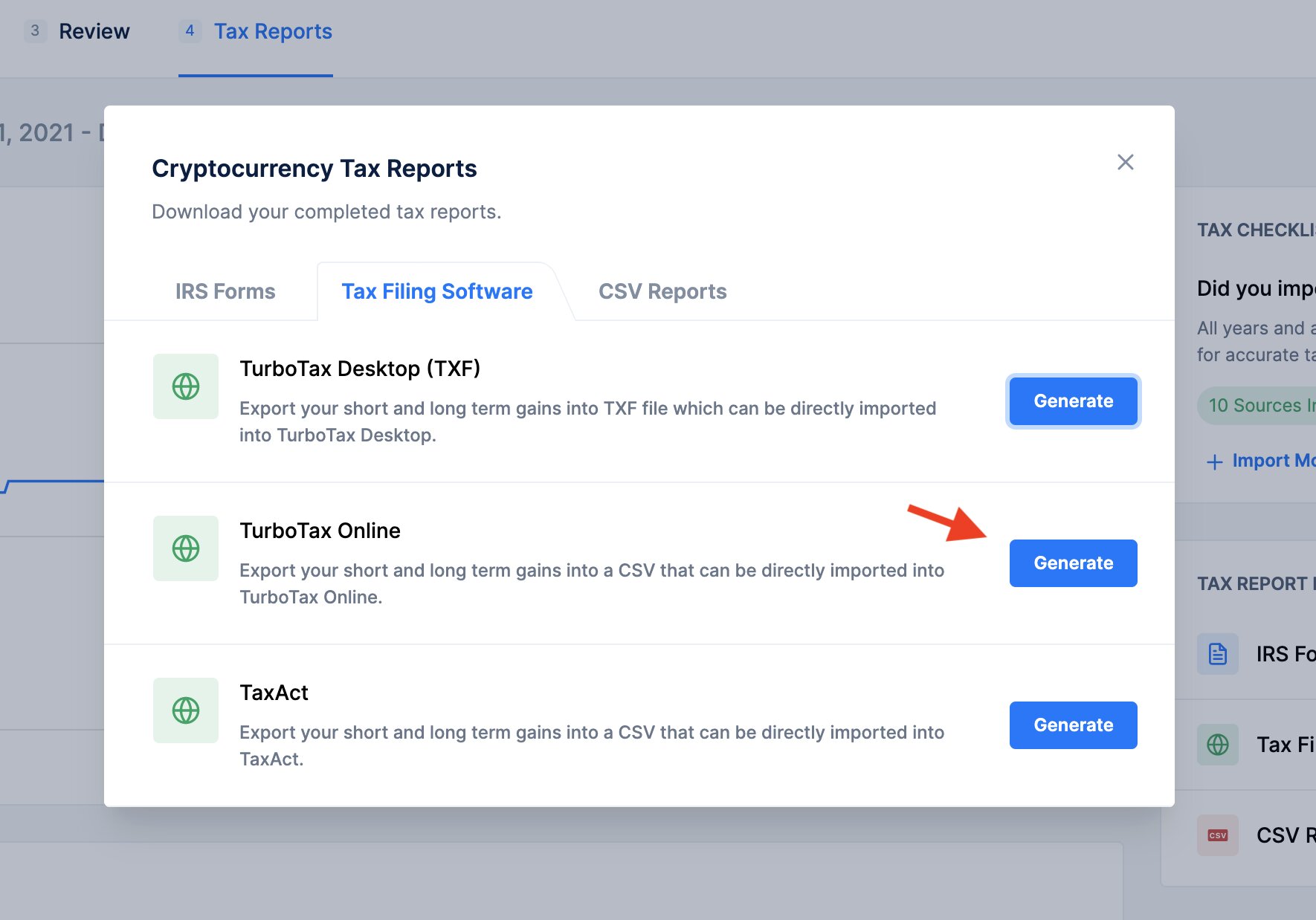

3. Fill out the Appropriate Tax Forms: Consult the tax forms or schedules specific to your country to accurately report your crypto gains. In some countries, there may be dedicated forms or schedules for reporting cryptocurrency transactions, while in others, you may need to report them on general income or capital gains tax forms. Be sure to include all necessary information and provide accurate calculations.

4. Declare All Income: Ensure that you declare all cryptocurrency-related income, including mining income or income from exchanging cryptocurrencies for goods or services. Failure to report all income can lead to penalties or legal consequences.

5. Follow Reporting Deadlines: Be aware of the tax reporting deadlines in your jurisdiction and submit your tax return within the specified timeframe. Late filing or non-compliance may result in penalties or interest charges.

6. Seek Professional Advice if Needed: If you are unsure about how to report your crypto gains or have complex tax situations, it is advisable to consult with a tax professional familiar with cryptocurrency taxation. They can provide guidance tailored to your specific circumstances and ensure that you meet all reporting requirements accurately.

Remember, accurate and transparent reporting of your crypto gains is not only essential for legal compliance but also demonstrates good financial responsibility. By fulfilling your tax obligations, you contribute to the integrity of the cryptocurrency market and help build trust and acceptance of digital assets in the broader financial ecosystem.

Tax strategies to minimize your crypto gains tax

While it is important to fulfill your tax obligations, there are several legitimate strategies that can help you minimize your crypto gains tax liability. By utilizing these strategies, you can optimize your tax planning and potentially keep more of your crypto profits. Here are some tax strategies to consider:

1. Holding Period: Holding your cryptocurrencies for more than a year can qualify your gains as long-term capital gains, which are often subject to lower tax rates compared to short-term gains. By strategically planning your transactions and holding periods, you can take advantage of the favorable tax treatment for long-term gains.

2. Tax-Loss Harvesting: If you have crypto investments that have experienced losses, you may consider selling them to offset your capital gains. By realizing capital losses, you can reduce your overall tax liability. However, it’s important to ensure compliance with the “wash sale” rule, which prohibits repurchasing the same or substantially identical assets within a specified period.

3. Tax-Advantaged Accounts: Depending on your jurisdiction, investing in your cryptocurrencies through tax-advantaged accounts such as Individual Retirement Accounts (IRAs) or Self-Invested Personal Pensions (SIPPs) may offer tax advantages. These accounts allow you to invest in cryptocurrencies while deferring or potentially eliminating tax on the gains until withdrawal or retirement.

4. Charitable Donations: Donating your cryptocurrencies to charitable organizations can have dual benefits: supporting a cause you care about and potentially reducing your tax liability. Depending on the tax laws in your jurisdiction, donating appreciated cryptocurrencies to qualified charities may allow you to claim a deduction for the current market value of the donated assets, while also avoiding capital gains tax on the appreciation.

5. Gift or Inheritance: Depending on the tax laws in your jurisdiction, gifting or inheriting cryptocurrencies may provide opportunities for reducing your tax liability. Consult with a tax professional to understand the specific rules and allowances related to gifting or inheriting cryptocurrencies, as they can vary widely.

6. Proper Expense Deductions: If you actively trade cryptocurrencies, you may be eligible to deduct certain expenses related to your trading activities, such as trading fees, exchange fees, and other transaction costs. Keeping receipts and records of these expenses can help you accurately claim deductions and reduce your taxable crypto gains.

Remember, tax laws and regulations are complex and can vary between jurisdictions. It is essential to consult with a tax advisor or professional who specializes in cryptocurrency taxation to ensure that you are effectively implementing these strategies in compliance with the tax laws of your specific jurisdiction.

Potential penalties for non-compliance

Failure to comply with tax regulations regarding cryptocurrency gains can result in various penalties and legal consequences. While the specific penalties can vary depending on your jurisdiction, it is important to understand the potential ramifications to avoid unnecessary risks. Here are some potential penalties for non-compliance with cryptocurrency taxation:

1. Fines and Penalties: Governments impose monetary fines and penalties for failing to accurately report crypto gains or underreporting income. These penalties can be based on a percentage of the tax owed and can quickly accumulate, resulting in a significant financial burden. The amount of the fines can vary depending on the severity of the non-compliance and may increase for repeated offenses.

2. Interest Charges: In addition to fines and penalties, tax authorities may also charge interest on the outstanding tax amounts. Interest accrues from the date of the tax filing deadline until the tax liability is paid in full. These interest charges can further add to the overall amount owed and create additional financial strain.

3. Audits and Investigations: Non-compliance with cryptocurrency taxation increases the risk of being audited or investigated by tax authorities. Tax audits involve a thorough review of your financial records and transactions to ensure compliance with tax laws. The process can be time-consuming, intrusive, and may require you to provide substantial documentation and evidence to support your tax positions.

4. Legal Consequences: In cases of deliberate tax evasion or fraud, individuals may face criminal charges and legal consequences. Tax evasion is a serious offense that can result in substantial fines and imprisonment. Engaging in fraudulent activities, such as intentionally providing false information or creating fictitious transactions, can lead to criminal prosecution and severe penalties.

5. Damage to Reputation: Non-compliance with cryptocurrency taxation can also have non-monetary consequences, such as damage to your personal or professional reputation. Negative publicity or being associated with tax evasion can harm your credibility and trustworthiness, which may have long-lasting impacts on your personal and professional relationships.

It is essential to prioritize compliance with tax regulations and fulfill your tax obligations regarding cryptocurrency gains. Staying informed about the tax laws in your jurisdiction, keeping accurate records, and seeking professional advice when necessary can help mitigate the risk of non-compliance and the associated penalties and consequences.

Tax considerations for different types of cryptocurrencies

When it comes to taxation, different types of cryptocurrencies may have unique considerations and implications. Whether you are dealing with Bitcoin, Ethereum, or any other digital asset, understanding the tax implications specific to each cryptocurrency is crucial. Here are some tax considerations to keep in mind for different types of cryptocurrencies:

1. Bitcoin (BTC): Being the first and most widely recognized cryptocurrency, Bitcoin has attracted significant attention from tax authorities worldwide. In most jurisdictions, Bitcoin is considered as property or an asset and is subject to capital gains tax when sold or exchanged for fiat currency. It is important to track the cost basis of your Bitcoin transactions and determine the applicable tax rates based on the holding period.

2. Ethereum (ETH): Similar to Bitcoin, Ethereum is generally treated as an asset for tax purposes. The tax treatment of Ethereum transactions, such as mining income or staking rewards, can vary depending on the jurisdiction. It is important to report any income earned from Ethereum activities and accurately determine the cost basis for capital gains calculations when selling or disposing of Ethereum.

3. Stablecoins: Stablecoins, such as Tether (USDT) or USD Coin (USDC), are designed to have a stable value tied to a fiat currency like the US dollar. The tax treatment of stablecoins can depend on how they are classified by tax authorities. If considered the same as the underlying fiat currency, transactions involving stablecoins may have tax implications similar to traditional currency transactions. However, if considered a digital asset, tax rules applicable to other cryptocurrencies, such as capital gains tax, may apply.

4. Privacy Coins: Privacy-focused cryptocurrencies like Monero (XMR) and Zcash (ZEC) offer enhanced privacy features to protect transaction details and user identities. The tax treatment of privacy coins can be challenging as it may be difficult to accurately track transactions and determine the cost basis. Tax authorities are increasingly focusing on privacy coins, and it is important to ensure compliance with reporting requirements and accurately calculate taxable gains or losses.

5. Tokenized Assets: Tokenized assets represent real-world assets, such as real estate or artwork, on a blockchain. The tax treatment of tokenized assets can vary based on how they are classified. In some cases, the tax implications may align with those of the underlying asset, while in others, they may be treated as separate assets subject to capital gains tax.

It is crucial to stay updated on the evolving tax regulations surrounding different cryptocurrencies. Tax laws and guidance may change, especially as governments and tax authorities continue to adapt to the growing use of digital assets. Consulting with a tax professional familiar with cryptocurrency taxation can help ensure accurate reporting and compliance with the tax laws specific to each type of cryptocurrency.

Conclusion

Navigating the world of cryptocurrency taxation is essential for any crypto investor or trader. Understanding how cryptocurrencies are taxed, the distinction between short-term and long-term gains, and the various factors that determine your taxable gains is crucial in accurately reporting and minimizing your tax liability.

By staying informed about the tax laws and regulations in your jurisdiction, you can ensure compliance, mitigate the risk of penalties, and optimize your tax planning. Keeping detailed records of your cryptocurrency transactions and seeking professional guidance when needed can help streamline the reporting process and ensure accurate calculations.

Furthermore, exploring tax strategies such as holding periods, tax-loss harvesting, utilizing tax-advantaged accounts, and considering charitable donations can help minimize your crypto gains tax liability, allowing you to maximize your profitability in the cryptocurrency space.

It is important to remember that tax laws and regulations surrounding cryptocurrencies are evolving, and each jurisdiction may have its own specific rules. Therefore, it is always advisable to consult with a tax professional who specializes in cryptocurrency taxation to ensure compliance with the latest tax requirements and optimize your tax strategy.

Taking a proactive approach to understand and comply with cryptocurrency taxation not only helps you fulfill your legal obligations but also fosters trust, transparency, and wider adoption of cryptocurrencies in the global financial ecosystem. By staying informed and making informed financial decisions, you can navigate the tax landscape and make the most of your cryptocurrency investments.