Introduction

Cryptocurrency has gained significant popularity in recent years, with individuals and businesses increasingly utilizing it for various transactions and investments. However, along with the growth of cryptocurrency comes the need to understand and fulfill tax obligations related to it. Failing to comply with tax regulations can result in penalties and legal consequences.

Fortunately, there are strategies you can employ to legally minimize your tax liability on cryptocurrency. By making informed decisions and taking advantage of applicable tax rules, you can optimize your financial situation while staying within the bounds of the law. This article outlines several effective approaches to help you avoid paying excessive taxes on your crypto investments.

It is important to note that tax laws can vary depending on your jurisdiction, so it’s crucial to consult with a tax professional who is well-versed in cryptocurrency taxation. These general strategies are meant to provide you with a starting point for exploring tax-efficient options but should not be considered as personal tax advice.

Now let’s delve into these strategies that can help you avoid paying excessive taxes on cryptocurrency.

Understand the Tax Obligations for Cryptocurrency

Before diving into strategies to minimize your tax liability, it’s crucial to have a solid understanding of the tax obligations associated with cryptocurrency. The tax treatment of cryptocurrencies can vary from country to country, and even within different regions.

In most jurisdictions, cryptocurrency is treated as property for tax purposes. This means that when you sell or exchange your crypto holdings, you may realize capital gains or losses, which need to be reported on your tax return. Additionally, if you receive cryptocurrencies as income or compensation, such as through mining or airdrops, you may also need to pay taxes on this income.

It’s important to keep detailed records of all your cryptocurrency transactions, including dates of acquisition, purchase prices, sale prices, and any relevant fees or expenses incurred. These records will be crucial when calculating your gains or losses and determining your tax liability.

Furthermore, staying up to date with any developments or changes in cryptocurrency tax regulations is essential. Tax authorities are increasingly focusing on cryptocurrency transactions, and new guidelines may be introduced to address the evolving nature of this digital asset class. Consulting with a tax professional who specializes in cryptocurrency taxation can help ensure compliance with current regulations and maximize your tax efficiency.

By understanding and fulfilling your tax obligations, you can avoid costly penalties and stay on the right side of the law. With this knowledge in hand, let’s explore specific strategies to minimize your tax burden on cryptocurrency.

Hold onto Your Cryptocurrency for at Least a Year

One effective strategy to minimize your tax liability on cryptocurrency is to hold onto your investments for at least a year. In many jurisdictions, including the United States, holding assets for more than a year qualifies them for long-term capital gains treatment.

Long-term capital gains are generally taxed at a lower rate compared to short-term gains, which are derived from assets held for less than a year. By holding onto your cryptocurrency investments for at least a year, you may be eligible for these preferential tax rates, ultimately reducing the amount of tax you owe on any gains realized upon the sale or exchange of your crypto.

It’s important to note that tax laws can change, and long-term capital gains rates can vary depending on your jurisdiction. Consulting with a tax professional will help you understand the specific tax rates and regulations applicable to your situation.

Additionally, by holding onto your cryptocurrency investments for an extended period, you have the potential to benefit from further price appreciation. Cryptocurrency markets are known for their volatility, and by giving your investments time to grow, you increase the likelihood of significant gains. This approach not only reduces your tax liability but also allows you to potentially enjoy more substantial profits.

While holding onto your cryptocurrency for at least a year can be a beneficial tax strategy, it’s important to carefully consider your investment goals and risk tolerance. Cryptocurrency markets can be unpredictable, and price fluctuations can occur over long periods. Make sure to assess your financial situation and consult with a financial advisor before implementing this strategy.

By strategically timing the sale or exchange of your cryptocurrency investments to meet the long-term capital gains threshold, you can take advantage of lower tax rates and potentially increase your overall investment return.

Take Advantage of Tax-Free Crypto Exchanges

Another strategy to consider when trying to minimize your tax liability on cryptocurrency is utilizing tax-free crypto exchanges. Some jurisdictions offer tax exemptions or favorable regulations for specific types of crypto-to-crypto exchanges.

In these tax-friendly jurisdictions, you can potentially swap one cryptocurrency for another without incurring immediate tax consequences. This means that you can rebalance your crypto portfolio, diversify your holdings, or take advantage of market opportunities without triggering taxable events.

It’s important to note that these tax-free exchanges typically have specific requirements and limitations. For example, they might only apply to certain types of cryptocurrencies or have a maximum threshold for tax-free transactions. Additionally, the tax treatment of these exchanges can vary depending on your jurisdiction.

Before engaging in tax-free crypto exchanges, it is crucial to thoroughly research and understand the regulations and requirements set forth by your local tax authorities. Consulting with a tax professional who specializes in cryptocurrency taxation can provide you with the necessary guidance to ensure compliance.

By utilizing tax-free crypto exchanges, you can strategically manage your cryptocurrency portfolio while deferring tax liabilities. This allows you to make necessary adjustments to your holdings without incurring immediate tax obligations, potentially reducing your overall tax burden over time.

However, it’s essential to stay informed about any changes in tax regulations that may affect the tax treatment of cryptocurrency exchanges. Local tax authorities may impose new guidelines or tighten existing regulations, so staying up to date is crucial for maintaining compliance and maximizing tax efficiency.

Utilize Tax-Loss Harvesting

Tax-loss harvesting is a strategy commonly used in traditional financial markets, but it can also be applied to cryptocurrency investments. The idea behind tax-loss harvesting is to strategically sell losing investments to offset capital gains and reduce your overall tax liability.

If you have cryptocurrency holdings that have depreciated in value since you acquired them, you can sell them at a loss. By realizing these losses, you can offset any capital gains you have realized from other investments or from the sale of appreciated cryptocurrencies.

When implementing tax-loss harvesting, it’s important to be mindful of the “wash-sale” rule, which prohibits repurchasing the same or substantially identical investment within a short period. If you repurchase the same cryptocurrency within 30 days of selling it at a loss, the IRS (or tax authority in your jurisdiction) may disallow the loss for tax purposes.

Instead, you can reinvest the funds from the sale into a different cryptocurrency or wait for the 30-day period to pass before repurchasing the initial investment. By doing so, you can realize the tax benefit of the loss while still maintaining exposure to the cryptocurrency market.

Remember to keep accurate records of your cryptocurrency transactions, including the details of the sold assets and any corresponding gains or losses. These records will be necessary for accurately calculating your capital gains and losses and properly reporting them on your tax return.

Utilizing tax-loss harvesting can help you lower your overall tax liability on cryptocurrency investments by leveraging losses to offset gains. However, it’s crucial to consult with a tax professional who understands the intricacies of cryptocurrency taxation to ensure compliance with relevant regulations and maximize your tax savings.

Convert Your Cryptocurrency to Stablecoins

Another strategy to consider when aiming to minimize tax liability on cryptocurrency is converting your volatile cryptocurrencies into stablecoins. Stablecoins are cryptocurrencies that are typically pegged to the value of a stable asset, such as a fiat currency like the US dollar.

By converting your cryptocurrency holdings into stablecoins, you can reduce the tax implications associated with price fluctuations. Since stablecoins aim to maintain a stable value, there is less potential for significant gains or losses when compared to highly volatile cryptocurrencies.

When you convert your cryptocurrency into stablecoins, the transaction is treated as a tax-deferred event, meaning you would not owe taxes on the unrealized gains or losses at that time. This can help you defer tax obligations and potentially create a more tax-efficient strategy for managing your cryptocurrency investments.

Moreover, stablecoins offer the advantage of liquidity and stability. They can be used for various purposes, such as making purchases or transferring funds, without the risk of significant value fluctuations that can occur with other cryptocurrencies.

It’s important to note that tax laws and regulations may differ depending on your jurisdiction. Consult with a tax professional who specializes in cryptocurrency taxation to understand the specific tax implications of converting your cryptocurrency into stablecoins in your area.

By converting your cryptocurrency holdings into stablecoins, you can minimize the tax impact of price volatility while still maintaining exposure to the cryptocurrency market. This strategy provides stability, flexibility, and potential tax advantages compared to holding highly volatile cryptocurrencies.

However, it’s crucial to keep accurate records of your transactions involving stablecoins, as they may still be subject to taxation when you eventually exchange them back into fiat currency or another cryptocurrency. Proper record-keeping is essential to accurately report your gains or losses and ensure compliance with tax regulations.

Donate Your Cryptocurrency to Charity

Donating your cryptocurrency holdings to eligible charitable organizations is not only a generous act but can also provide you with potential tax benefits. Many jurisdictions allow for tax deductions or credits for charitable donations, and cryptocurrency donations are no exception.

When you donate your cryptocurrency to a registered charity, you may be eligible to claim a tax deduction for the fair market value of the donated assets. The tax deduction can help offset your taxable income, reducing your overall tax liability.

One advantage of donating cryptocurrency is that you can potentially avoid capital gains tax on the appreciation of your holdings. If you have cryptocurrency that has significantly increased in value since you acquired it, selling it would trigger capital gains tax. However, by donating the cryptocurrency directly to a charity, you can bypass the capital gains tax and still benefit from the tax deduction for the fair market value of the donation.

It’s essential to ensure that the charitable organization is eligible to receive cryptocurrency donations and that you receive proper documentation for your contribution. Consult with the charity and a tax professional to understand the specific requirements and procedures for donating cryptocurrency in your jurisdiction.

By donating your cryptocurrency to charity, you can make a positive impact while potentially reducing your tax liability. It’s a win-win situation: the charity receives valuable funds, and you benefit from tax advantages.

However, it’s important to note that tax laws can be complex, and the specific tax benefits and regulations related to cryptocurrency donations may vary depending on your jurisdiction. Consulting with a tax professional who specializes in cryptocurrency taxation will ensure that you adhere to the necessary requirements and maximize your tax benefits while supporting charitable causes.

Utilize a Self-Directed IRA or 401(k) for Crypto Investments

If you have retirement accounts such as an Individual Retirement Account (IRA) or a 401(k), you may be able to utilize a self-directed version of these accounts to invest in cryptocurrencies. A self-directed IRA or 401(k) gives you more control over your investments, including the ability to allocate funds towards cryptocurrencies.

By utilizing a self-directed retirement account for crypto investments, you can enjoy potential tax advantages. Contributions to traditional IRAs or 401(k)s are typically tax-deductible, meaning you can reduce your taxable income in the year of contribution. Additionally, any growth or gains on your investments within the account can be tax-deferred until you withdraw the funds during retirement.

When investing in cryptocurrencies within a self-directed retirement account, you can potentially benefit from tax-free growth. This means that you won’t owe taxes on any realized gains or income generated by your crypto investments as long as the funds remain within the account.

It’s important to note that there are specific rules and regulations governing self-directed retirement accounts, and not all custodians support cryptocurrency investments. Therefore, it’s crucial to research and select a reputable custodian that allows for crypto investments within a self-directed retirement account.

Furthermore, compliance with all applicable tax and reporting requirements is paramount when utilizing a self-directed IRA or 401(k) for crypto investments. Mistakes or failure to meet the guidelines can result in penalties, taxes, or even disqualification of the retirement account.

Consulting with a financial advisor or tax professional experienced in self-directed retirement accounts and cryptocurrency taxation is highly recommended. They can guide you through the process, ensure compliance, and help you maximize the potential tax advantages of using a self-directed IRA or 401(k) for crypto investments.

By taking advantage of a self-directed retirement account, you can invest in cryptocurrencies while enjoying potential tax benefits and securing your financial future.

Consider Offshore Cryptocurrency Holdings

For individuals looking to minimize their tax liability on cryptocurrency investments, considering offshore cryptocurrency holdings can be a viable strategy. Offshore jurisdictions often offer favorable tax regulations for international investors, including lenient or even zero tax rates on capital gains from cryptocurrency investments.

By holding your cryptocurrency investments in an offshore account or entity, you may be able to reduce your tax obligations. This arrangement can be particularly beneficial for individuals residing in jurisdictions with high tax rates on cryptocurrency gains or strict reporting requirements.

However, it’s important to note that engaging in offshore cryptocurrency holdings can have legal and regulatory implications. Some jurisdictions have specific requirements for reporting foreign income and assets, and failure to comply with these requirements can result in penalties and legal consequences.

Before considering offshore cryptocurrency holdings, it’s crucial to consult with a tax professional who specializes in international taxation and understands the legal and regulatory landscape. They can provide guidance on the most appropriate jurisdiction and help you navigate the complexities of offshore investing.

Additionally, it’s essential to carefully assess the risks associated with offshore holdings, such as increased exposure to fraud, hacking, or other security vulnerabilities. Researching and selecting reputable and secure offshore exchanges or custodial services is paramount to safeguarding your investments.

It’s worth noting that regulations surrounding offshore cryptocurrency holdings can evolve and change over time. Staying updated on international tax laws and relevant regulatory changes is crucial to ensure ongoing compliance and to take advantage of any strategic opportunities.

Consider offshore cryptocurrency holdings as a potential strategy if you are seeking to minimize your tax liability on cryptocurrency investments. However, ensure that you fully understand the legal and regulatory environment, consult with a tax professional, and prioritize the security of your investments.

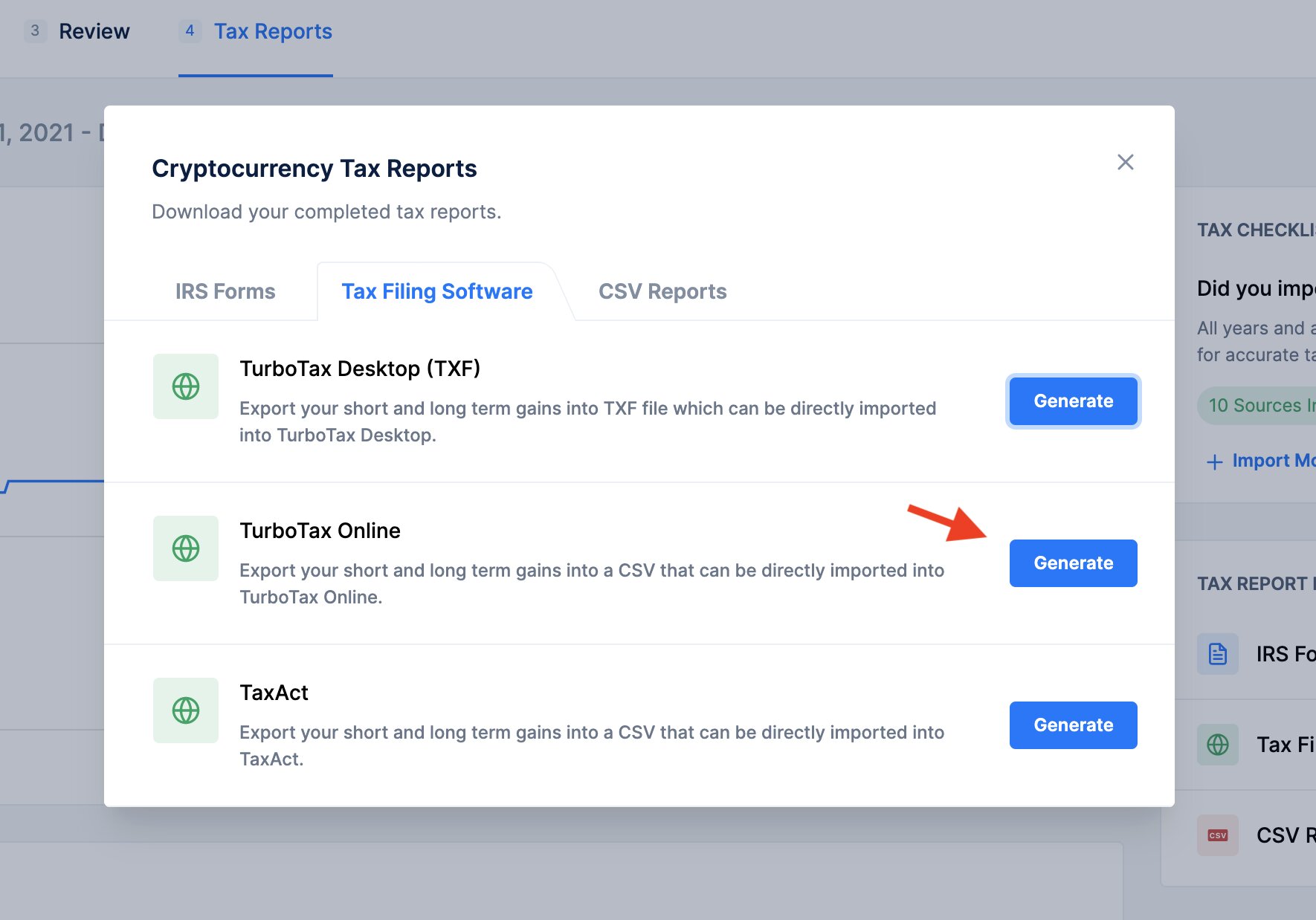

Keep Accurate Records and Seek Professional Help

When it comes to navigating the complex world of cryptocurrency taxation, one of the most critical strategies is to keep accurate records and seek professional help. Keeping meticulous records of your cryptocurrency transactions is essential for accurately reporting your gains, losses, and other relevant information on your tax returns.

Every time you buy, sell, or exchange cryptocurrencies, make sure to record the date, amount, purchase price, and sale price. Additionally, keep track of any fees or expenses associated with your transactions. These records will be invaluable when it comes time to calculate your taxable gains or losses and provide documentation for tax authorities.

Given the ever-evolving nature of cryptocurrency taxation, seeking professional help from a tax advisor who specializes in cryptocurrency taxation is highly recommended. A knowledgeable professional can provide personalized guidance based on your specific jurisdiction and situation.

A tax professional can help you understand the tax implications of your cryptocurrency investments, ensure compliance with relevant regulations, and help you identify tax-efficient strategies. Their expertise can save you time, money, and potential legal trouble.

Furthermore, as tax laws and regulations surrounding cryptocurrency continue to evolve, seeking professional help is essential to stay informed and up to date. Tax professionals are well-equipped to interpret complex tax codes and keep abreast of any changes that may impact your cryptocurrency investments.

Remember that cryptocurrency taxation can be complex, and making mistakes or failing to comply with tax regulations can have severe consequences. Avoid unnecessary penalties and legal troubles by relying on the expertise of professionals who understand the intricacies of cryptocurrency taxation.

In summary, keeping accurate records and seeking professional help are imperative when it comes to managing your cryptocurrency tax obligations. By doing so, you can ensure compliance with tax laws, maximize tax efficiency, and minimize the risk of any adverse consequences.

Conclusion

Managing tax obligations related to cryptocurrency investments requires careful consideration and strategic decision-making. By implementing the strategies outlined in this article, you can work towards minimizing your tax liability while staying within the bounds of the law.

First and foremost, understanding the tax obligations for cryptocurrencies is crucial. Familiarize yourself with the tax treatment of cryptocurrencies in your jurisdiction and stay updated on any changes or developments in tax regulations.

Holding onto your cryptocurrency investments for at least a year can potentially qualify them for the more favorable long-term capital gains tax treatment. Additionally, taking advantage of tax-free crypto exchanges, utilizing tax-loss harvesting, and converting your cryptocurrency to stablecoins are all strategies worth exploring.

Donating your cryptocurrency to charity not only contributes to a good cause but can also provide you with tax benefits. Furthermore, considering offshore cryptocurrency holdings and utilizing self-directed retirement accounts can offer additional avenues to potentially reduce your tax liability.

Throughout your cryptocurrency journey, keeping accurate records of your transactions and seeking professional help from tax advisors experienced in cryptocurrency taxation is essential. They can provide personalized guidance, ensure compliance, and help you navigate the complexities of tax regulations.

Remember, tax laws can be intricate and subject to change. Staying informed, seeking professional advice, and maintaining accurate records are key to maximizing your tax efficiency and minimizing any potential legal consequences.

By implementing these strategies and staying proactive, you can effectively manage your tax obligations and optimize your financial outcomes in the ever-evolving world of cryptocurrency.