Introduction

Welcome to the world of cryptocurrencies, where digital assets have revolutionized the way we transact and store value. As the popularity of cryptocurrencies such as Bitcoin, Ethereum, and Litecoin continues to soar, it’s important for crypto users to understand the tax implications of their transactions. Tracking crypto transactions for tax purposes is crucial to ensure compliance with tax regulations and avoid potential penalties or audits.

Crypto transactions are subject to taxation in many countries, including the United States, Canada, and the United Kingdom. The tax treatment of cryptocurrencies can vary depending on factors such as whether the transaction involves buying, selling, or exchanging tokens, and the holding period of the digital assets.

While the decentralized and pseudonymous nature of cryptocurrencies may attract users seeking privacy, it’s important to note that tax authorities are increasingly scrutinizing crypto-related activities. Failure to accurately report crypto transactions can result in serious consequences, including fines and legal repercussions.

This article serves as a comprehensive guide on how to track crypto transactions for tax purposes. By understanding the steps involved and following best practices, you can ensure that you stay on the right side of the law and accurately report your crypto activities.

Why tracking crypto transactions for taxes is important

Tracking crypto transactions for tax purposes is essential for several reasons. First and foremost, it ensures compliance with tax regulations. Cryptocurrencies are treated as property for tax purposes in many jurisdictions, which means that every transaction needs to be reported and the corresponding tax liability calculated.

By accurately tracking your crypto transactions, you can avoid potential penalties, audits, and legal trouble. Tax authorities are becoming increasingly vigilant about crypto tax compliance, and failing to report your transactions can have serious consequences. By staying organized and documenting every transaction, you can demonstrate transparency and compliance in the event of an audit.

Additionally, tracking crypto transactions can help you accurately calculate your gains and losses. It’s important to determine the cost basis of your digital assets and calculate the capital gains or losses when you sell or exchange them. Properly tracking your transactions allows you to accurately report this information on your tax returns, avoiding any discrepancies and ensuring you pay the correct amount of tax.

Furthermore, tracking crypto transactions enables you to take advantage of any available tax deductions and benefits. For example, if you incur transaction fees while buying or selling cryptocurrencies, these fees may be deductible. Additionally, if you operate a cryptocurrency mining or staking business, you may be eligible for certain tax breaks or incentives.

Lastly, tracking your crypto transactions can provide valuable information for financial planning and investment purposes. By keeping track of your buying and selling activities, you can analyze your investment performance and make more informed decisions about your crypto portfolio. It can also help you accurately calculate your overall net worth, considering the value of your digital assets.

Understanding the tax implications of crypto transactions

Before diving into the process of tracking crypto transactions for taxes, it’s crucial to have a solid understanding of the tax implications associated with these transactions. Cryptocurrencies are considered taxable assets in many jurisdictions, and the tax treatment can vary depending on the specific transaction and jurisdiction.

In general, the following tax implications are important to consider:

1. Capital gains tax: When you sell or exchange cryptocurrencies, any gains or profits made are typically subject to capital gains tax. This tax is calculated based on the difference between the purchase price (cost basis) and the selling price of the digital asset.

2. Holding period: The length of time you hold a cryptocurrency can impact the tax rate applied to your capital gains. Short-term capital gains, which result from selling assets held for less than a year, are usually taxed at higher rates compared to long-term capital gains, which result from selling assets held for over a year.

3. Cryptocurrency mining: If you are involved in cryptocurrency mining, the rewards or earnings from mining activities may be subject to income tax. The value of the mined coins or tokens is typically considered taxable income.

4. Trading and exchanging: If you frequently trade or exchange cryptocurrencies, each transaction is subject to taxation. Any gains or losses resulting from these transactions need to be reported on your tax return.

5. Crypto payments: Some jurisdictions treat using cryptocurrencies to make purchases or payments as a taxable event. The value of the digital asset at the time of the transaction is typically used to calculate the taxable amount.

It’s important to consult with a tax professional or accountant who is knowledgeable about cryptocurrency taxation in your specific jurisdiction. They can provide guidance on the specific tax laws and regulations that apply to your crypto transactions, ensuring that you comply with the law and maximize any available tax benefits.

Step-by-step guide to tracking crypto transactions for taxes

Tracking crypto transactions for tax purposes can feel overwhelming, but breaking it down into manageable steps can simplify the process. Here is a step-by-step guide to help you navigate the process:

1. Gathering all transaction records: Start by collecting all the records of your crypto transactions. This includes records from cryptocurrency exchanges, wallet providers, and any other platforms or services you have used. Make sure to gather information about each transaction, including the date, type of transaction, amount, and any associated fees.

2. Organizing and categorizing transactions: Once you have gathered all your transaction records, organize them in a systematic manner. Create a spreadsheet or use accounting software to categorize each transaction based on its type (e.g., buying, selling, trading) and the digital asset involved. This will help streamline the process of calculating gains and losses.

3. Calculating gains and losses: Determine the cost basis of each digital asset involved in your transactions. The cost basis is typically the purchase price plus any associated fees. Calculate the gains or losses for each transaction by subtracting the cost basis from the selling price or fair market value at the time of the transaction. Keep a record of these calculations for accurate reporting.

4. Reporting the information on tax forms: Use the information gathered and calculated in the previous steps to accurately report your crypto transactions on your tax return. In the United States, for example, you may need to complete Form 8949 and Schedule D to report your capital gains and losses. Ensure that you provide all necessary details and double-check for accuracy before submitting your tax forms.

It’s important to note that these steps may vary depending on your jurisdiction and the specific tax regulations in place. Consulting with a tax professional or accountant familiar with cryptocurrency taxation can provide valuable guidance and ensure that you comply with the specific requirements in your jurisdiction.

By following this step-by-step guide, you can stay organized and accurately track your crypto transactions for tax purposes, giving you peace of mind and minimizing the risk of errors or compliance issues.

Gathering all transaction records

When it comes to tracking crypto transactions for taxes, the first step is to gather all transaction records. This includes collecting information about every crypto-related transaction you’ve made, whether it’s buying, selling, trading, or receiving digital assets.

Start by compiling records from the cryptocurrency exchanges you have used. Most exchanges provide transaction history or trade history reports that contain crucial details such as the date, time, type of transaction, amount, and associated fees. Download or request these reports from each exchange you’ve used during the tax year.

In addition to exchange records, collect information from wallet providers, decentralized finance (DeFi) platforms, and any other platforms or services where crypto transactions were conducted. These platforms usually offer transaction histories or statements that can help you track your activities accurately.

It’s important to ensure that you have records for both inbound and outbound transactions. Inbound transactions include any digital assets you have received or earned, such as mining rewards, airdrops, or staking rewards. Outbound transactions consist of any digital assets you have sent, sold, or traded with others.

When gathering your transaction records, be mindful of the tax year you are preparing for. Ensure that you gather records specific to that tax year and avoid mixing transactions from different years.

Keep in mind that the level of detail provided in transaction records may vary between platforms. Some may provide downloadable spreadsheets that include comprehensive information, while others may require you to manually gather and compile the necessary details.

To maintain organization and transparency, it’s advisable to create a dedicated folder or digital storage location to keep all transaction records securely. This will ensure that you have easy access to the records when needed and that they are all in one place.

By diligently gathering all your transaction records from various platforms and organizing them in one central location, you will have a solid foundation for accurately tracking your crypto transactions for tax purposes.

Organizing and categorizing transactions

Once you have gathered all your transaction records, the next step in tracking crypto transactions for taxes is to organize and categorize them. This will help you streamline the process of calculating gains and losses and ensure accurate reporting on your tax forms.

One effective way to organize your transactions is by creating a spreadsheet or using accounting software specifically designed for tracking crypto activities. This will enable you to create a structured system to manage your transactions.

Start by creating columns in your spreadsheet or software to record important details such as the date of the transaction, type of transaction (buying, selling, trading), digital asset involved, amount of the transaction, and any associated fees. You can also include additional columns to note specific details or categorize transactions further, such as whether the transaction was a personal purchase or a business-related transaction.

Categorizing the transactions based on their type and purpose can be helpful for tax reporting. For example, separate buying and selling transactions, as well as transactions related to mining, staking, or receiving income from cryptocurrencies. This will make it easier to determine the appropriate tax treatment for each category.

Moreover, consider grouping and labeling transactions based on the digital asset being transacted. This can be particularly useful if you have a diverse crypto portfolio. Creating separate sections or tabs in your spreadsheet for different digital assets can provide a clearer overview of your holdings and simplify the tracking process.

As you organize and categorize your transactions, ensure that you maintain accuracy and consistency throughout the process. Double-check the information you enter to avoid any mistakes or discrepancies that may lead to inaccurate tax reporting or calculations.

Remember to save and back up your organized transaction records regularly. This will ensure that you have a secure and readily accessible record of your crypto transactions for future reference or in case of an audit.

By organizing and categorizing your crypto transactions, you will have a clear and structured system to track your activities, making it easier to calculate gains and losses accurately and report them on your tax forms.

Calculating gains and losses

Calculating gains and losses is a crucial step in tracking crypto transactions for tax purposes. It involves determining the cost basis of your digital assets and calculating the capital gains or losses when you sell, exchange, or dispose of them.

To calculate gains and losses accurately, follow these steps:

1. Determine the cost basis: The cost basis is the original purchase price of the digital asset. It includes the amount you paid for it and any associated fees, such as transaction fees or exchange fees. If you received the digital asset through mining, airdrops, or as part of a staking reward, the fair market value of the asset at the time you received it is typically considered the cost basis.

2. Calculate gains and losses: When you sell or dispose of a digital asset, subtract the cost basis from the selling price or the fair market value at the time of the transaction. If the result is a positive number, it represents a capital gain. Conversely, if the result is negative, it represents a capital loss.

3. Consider the holding period: Your capital gains or losses may be subject to different tax rates depending on the length of time you held the digital asset. In many jurisdictions, short-term capital gains (assets held for less than a year) are taxed at higher rates compared to long-term capital gains (assets held for over a year). Consult your local tax regulations to determine the applicable tax rates for your situation.

4. Keep track of each transaction: Maintain accurate records of each transaction, including the calculated gains or losses and the corresponding dates. This will help in accurate reporting on your tax forms and provide a clear audit trail if required.

It is important to note that tax regulations related to crypto transactions can be complex, and there may be additional factors to consider, such as wash sale rules or specific regulations for certain types of transactions. Consulting with a tax professional or accountant who is knowledgeable about cryptocurrency taxation in your jurisdiction can provide valuable guidance and ensure accurate calculations.

By diligently calculating your gains and losses for each crypto transaction, you can accurately report the taxable income on your tax forms and comply with the applicable tax regulations.

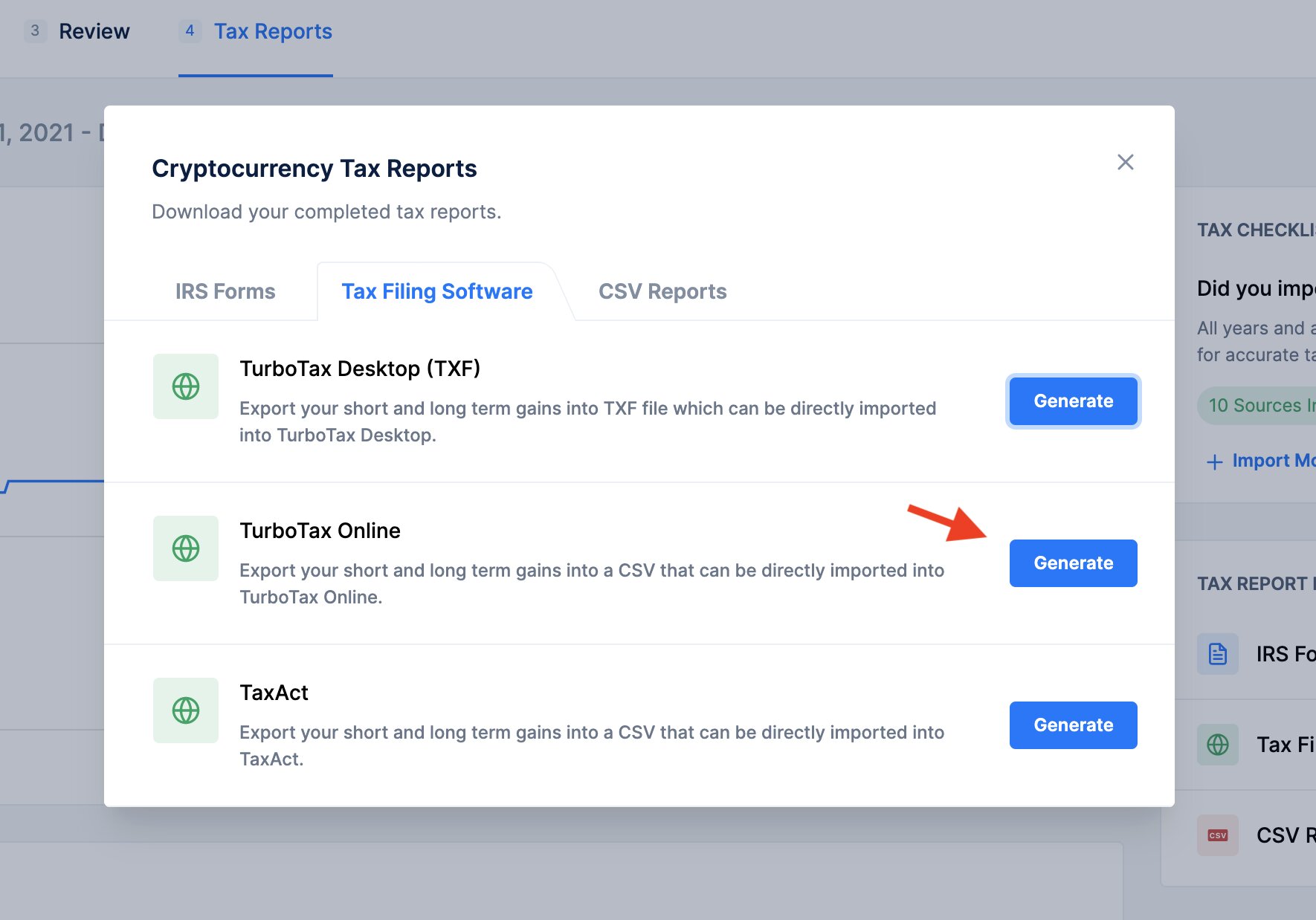

Reporting the information on tax forms

Once you have gathered and organized all your crypto transaction records, and calculated the gains and losses, the next step is to report this information on your tax forms. Reporting the relevant details accurately is essential to ensure compliance with tax regulations.

The specific tax forms and requirements can vary depending on your jurisdiction. Here are some general steps to consider when reporting your crypto transactions:

1. Form selection: Determine the tax forms required for reporting crypto transactions in your country. In the United States, for example, Form 8949 and Schedule D are commonly used to report capital gains and losses. Consult with a tax professional or visit your local tax authority’s website for guidance on the appropriate forms.

2. Enter transaction details: Transfer the information from your transaction records to the appropriate sections of the tax forms. Provide the necessary details for each transaction, including the date, type of transaction, digital asset involved, cost basis, selling price, and any applicable gains or losses.

3. Separate reporting categories: Differentiate between short-term and long-term capital gains or losses based on the holding period of each asset. In many jurisdictions, these categories have different tax rates, and accurate reporting is crucial to ensure tax compliance.

4. Additional forms and disclosures: In some cases, you may need to include additional forms or disclosures to report specific types of crypto transactions. For example, if you received income from mining or staking activities, additional forms may be required to report this income. Ensure that you understand the requirements specific to your jurisdiction.

5. Review and accuracy: Before submitting your tax forms, carefully review all the information you have entered. Double-check that all the details are accurate and match the supporting documentation. This will minimize the risk of errors and potential issues with tax authorities.

It is crucial to keep copies of all the tax forms and supporting documentation for your crypto transactions. This will serve as a record of your tax reporting and provide a clear audit trail if needed in the future.

Remember that tax regulations related to cryptocurrencies can be complex and subject to changes. It is advisable to consult with a tax professional or accountant who specializes in cryptocurrency taxation to ensure accurate reporting and compliance with the specific requirements in your jurisdiction.

Tips for accurate crypto transaction tracking

Tracking crypto transactions for tax purposes requires attention to detail and accurate record-keeping. Here are some tips to help you maintain accuracy and streamline your tracking process:

1. Maintain organized records: Keep all transaction records, including receipts, invoices, and statements, organized in a central location. This will make it easier to access and reference the information when needed.

2. Consistent data entry: Enter transaction details in a consistent and standardized format. Use the same units of measurement, currencies, and naming conventions to ensure uniformity across your records.

3. Document all buying and selling activities: Include both inbound and outbound transactions in your records. Document each purchase, sale, trade, or transfer of digital assets to ensure a complete record of your crypto activities.

4. Keep track of transaction fees: Record any fees associated with your transactions, such as exchange fees or transaction fees. These fees will be important for calculating accurate gains and losses.

5. Record the fair market value: If you received digital assets as income or through other means, record the fair market value of the asset at the time of receipt. This will help establish the cost basis for future transactions.

6. Regularly reconcile your records: Reconcile your records with the statements provided by exchanges or wallet providers to ensure accuracy. Resolve any discrepancies promptly and update your records accordingly.

7. Backup your data: Regularly back up your transaction records to prevent the loss of valuable data. Consider using encrypted cloud storage or offline storage methods for added security.

8. Seek professional advice: Consult with a tax professional or accountant who specializes in cryptocurrency taxation. They can provide guidance on accurate tracking, compliance with tax regulations, and any specific requirements based on your jurisdiction.

9. Stay informed about tax regulations: Stay updated with the latest tax regulations and guidelines related to cryptocurrencies in your jurisdiction. Changes in regulations can impact how you track and report your crypto transactions for taxes.

10. Use dedicated accounting software: Consider using specialized cryptocurrency accounting software or tools to streamline the tracking process. These tools can automatically import transaction data, calculate gains and losses, and generate reports.

By following these tips, you can ensure accurate and organized tracking of your crypto transactions for tax purposes. Remember that accurate record-keeping is not only essential for tax compliance but also provides valuable information for financial planning and investment purposes.

Common mistakes to avoid when tracking crypto transactions for taxes

Tracking crypto transactions for taxes can be complex, and there are several common mistakes that individuals can make. To ensure accurate reporting and avoid potential issues with tax authorities, it’s important to be aware of these common mistakes and take steps to avoid them:

1. Failing to track all transactions: One common mistake is not keeping track of every crypto transaction. It’s important to record all buying, selling, trading, and even receiving transactions, including airdrops, mining rewards, and staking income. Failing to track these transactions can lead to inaccurate tax reporting.

2. Ignoring transaction fees: Transaction fees associated with buying, selling, or transferring cryptocurrencies can impact your gains or losses. Many individuals mistakenly overlook these fees when calculating gains and losses. Be sure to include them in your records and calculations for accurate reporting.

3. Disregarding record-keeping: Proper record-keeping is crucial for accurate tax reporting. Failing to keep organized and detailed records of your crypto transactions can make it difficult to track and calculate gains and losses. Keep records of all transaction details, including dates, amounts, fees, and counterparties.

4. Incorrectly calculating gains and losses: Calculating gains and losses accurately is vital for tax compliance. Mistakes in determining the cost basis or incorrectly subtracting it from the selling price can result in inaccurate reporting. Take the time to carefully calculate gains and losses for each transaction, considering the cost basis and applicable holding periods.

5. Overlooking the tax implications of crypto payments: Using cryptocurrencies to make purchases or payments can trigger taxable events in some jurisdictions. The value of the digital asset at the time of the transaction needs to be reported. It’s important not to overlook the tax implications of crypto payments and include them in your records and tax reporting.

6. Neglecting wash sale rules: Wash sale rules, which disallow claiming losses on the sale of a security or digital asset if you repurchase it within a certain time frame, can also apply to cryptocurrencies. Be aware of these rules and ensure you handle any sales and repurchases properly to avoid incorrect reporting.

7. Failing to seek professional advice: Cryptocurrency taxation can be complex, and the rules vary from one jurisdiction to another. Failing to consult with a tax professional or accountant who specializes in crypto taxation can lead to misunderstandings and errors in your tax reporting. Seek professional advice to ensure compliance with the specific regulations in your jurisdiction.

8. Relying solely on tax software: While tax software can be helpful in automating calculations and generating reports, relying solely on it without understanding the underlying tax concepts can lead to errors. Make sure to review and validate the outputs of tax software to ensure accuracy.

By avoiding these common mistakes, you can maintain accurate and compliant tracking of your crypto transactions for tax purposes. Remember, it’s always better to be proactive and take the necessary steps to ensure accurate reporting rather than dealing with potential penalties or audits down the line.

Tools and software for simplifying the tracking process

Tracking crypto transactions for taxes can be a complex and time-consuming task. Fortunately, there are several tools and software options available that can help simplify the process and ensure accurate tracking. Here are some popular tools and software solutions:

1. Cryptocurrency tax software: Dedicated cryptocurrency tax software can automate many aspects of tracking and reporting crypto transactions. These tools can automatically import transaction data from exchanges and wallets, calculate gains and losses, and generate tax reports. Examples of popular cryptocurrency tax software include CoinTracking, CryptoTrader.Tax, and TokenTax.

2. Portfolio trackers: Portfolio tracking applications such as Blockfolio, Delta, and CoinStats can help you monitor your crypto holdings in real-time. These tools provide insightful data about your portfolio’s value, performance, and allocation, making it easier to track and manage your investments.

3. Accounting software: Utilizing general accounting software like QuickBooks or Xero can provide a more comprehensive approach to tracking your crypto transactions. These platforms enable you to create customized expense and income categories, record transfers, and generate financial statements that incorporate your cryptocurrency activities.

4. Blockchain explorers: Blockchain explorers such as Etherscan for Ethereum or Blockchain.com for Bitcoin allow you to view and analyze transaction history directly on the blockchain. These tools are useful for verifying transaction details and confirming wallet balances.

5. Crypto tax calculators: Online crypto tax calculators can help you estimate potential tax liabilities based on your crypto transactions. These tools usually require you to manually input transaction data and provide an estimate of your tax obligations. While not comprehensive solutions, they can still be helpful for planning purposes.

6. Spreadsheet templates: If you prefer a more hands-on approach, you can utilize spreadsheet templates specifically designed for tracking crypto transactions. These templates often include predefined formulas and categories to facilitate data entry and calculation. Excel, Google Sheets, and other spreadsheet software provide a simple and customizable option.

7. Accountants and tax professionals: When in doubt or dealing with complex crypto transactions, consulting with a tax professional or accountant who specializes in cryptocurrency taxation is highly recommended. They can guide you through the process, ensure accurate reporting, and offer personalized advice based on your specific situation.

Remember, while these tools and software solutions can greatly simplify the tracking process, it’s important to understand the underlying tax concepts and verify the accuracy of the outputs. Be sure to review the results, validate the calculations, and consult with a professional if needed to ensure compliance with tax regulations.

Conclusion

Tracking crypto transactions for taxes is a crucial responsibility for cryptocurrency users. By accurately recording and reporting your transactions, you can ensure compliance with tax regulations, minimize the risk of penalties, and maintain a clear audit trail.

Throughout this guide, we’ve explored the importance of tracking crypto transactions, understanding the tax implications, and provided a step-by-step process to help you stay organized. Remember, maintaining accurate records, categorizing transactions, and calculating gains and losses correctly are key elements of accurate tax reporting.

Additionally, we highlighted common mistakes to avoid and discussed tools and software options that can simplify the tracking process. Leveraging these tools can significantly streamline the task of tracking your crypto transactions and ensure accuracy in your tax reporting.

While this guide provides a comprehensive overview, it’s essential to consult with a tax professional or accountant who specializes in cryptocurrency taxation in your jurisdiction. They can offer personalized advice, address any specific tax requirements, and provide guidance to ensure compliance with the law.

By being diligent, organized, and seeking professional guidance when needed, you can effectively track your crypto transactions for taxes. Stay informed about tax regulations, keep accurate records, and utilize helpful tools to make the process smoother. With these practices in place, you can achieve accurate tax reporting and peace of mind in your cryptocurrency tax obligations.