Introduction

Welcome to the world of cryptocurrency, where digital assets are making waves and revolutionizing the way we think about money. As more and more individuals and businesses are getting involved in the crypto market, a common question arises: Do I need to pay taxes on cryptocurrency?

The short answer is yes. Just like any other form of income or investment, cryptocurrency is subject to taxation. The Internal Revenue Service (IRS) in the United States has categorized cryptocurrency as property, which means that any profits earned from buying, selling, and trading crypto are subject to taxes.

While the concept of paying taxes on cryptocurrency might seem daunting, it is an important aspect to consider to ensure compliance with tax laws and avoid potential penalties. Understanding the tax implications of your crypto activities is crucial for staying on the right side of the law and maximizing your financial gains.

In this article, we will delve into the world of cryptocurrency taxes, exploring the different types of taxation, reporting requirements, tax deductions, and strategies for minimizing your tax burden. Whether you are a seasoned crypto investor or just starting to explore the possibilities, this guide will provide you with valuable insights to navigate the complex world of cryptocurrency taxation.

Note that this article is intended for informational purposes only and does not constitute professional tax advice. It is recommended to consult with a tax professional or accountant for personalized guidance based on your specific circumstances.

What is cryptocurrency?

Cryptocurrency is a form of digital or virtual currency that uses cryptography for security. Unlike traditional fiat currencies such as the US dollar or the euro, cryptocurrency operates on a decentralized network called blockchain, which is a distributed ledger that records all transactions made with the currency.

The most well-known cryptocurrency is Bitcoin, which was introduced in 2009 by an anonymous person or group of people known as Satoshi Nakamoto. Since then, thousands of other cryptocurrencies, often referred to as altcoins, have emerged, each with its own unique features and purposes.

One of the key characteristics of cryptocurrency is its decentralization. Unlike traditional currencies that are controlled by central banks and governments, cryptocurrencies are not governed by any central authority. Instead, they rely on cryptographic algorithms and peer-to-peer networks to validate and secure transactions.

Another defining feature of cryptocurrency is its limited supply. Most cryptocurrencies have a predetermined maximum supply, which is typically set through a process called mining. Mining involves using powerful computers to solve complex mathematical problems in order to validate and record new transactions on the blockchain. Miners are rewarded with newly created cryptocurrency as an incentive for their computational work.

Cryptocurrency has gained popularity due to its potential for financial freedom, security, and fast, low-cost transactions. It has also opened up new possibilities for decentralized applications, smart contracts, and innovative fundraising mechanisms such as Initial Coin Offerings (ICOs).

While the concept of cryptocurrency may seem complex, owning and transacting with it can be as simple as using a mobile app or a digital wallet. Cryptocurrency transactions can be conducted globally, allowing for quick and efficient cross-border payments without the need for intermediaries.

However, with the rise of cryptocurrency comes the need to navigate the complex landscape of taxes and regulations. As governments around the world strive to adapt to the growing popularity of cryptocurrency, it is important for individuals and businesses to understand the tax implications and ensure compliance with the law.

Do I need to pay taxes on cryptocurrency?

Yes, you need to pay taxes on cryptocurrency. The IRS considers cryptocurrency to be property, not currency, which means that any gains or losses from your cryptocurrency activities are subject to taxation. Whether you are buying, selling, trading, or mining cryptocurrency, it is important to understand the tax obligations associated with these activities.

One of the reasons why cryptocurrency is subject to taxation is to ensure that individuals and businesses are accurately reporting their income and capital gains. Cryptocurrency transactions can be anonymous and difficult to trace, making it important for tax authorities to track these activities and ensure compliance with tax laws.

The tax treatment of cryptocurrency depends on various factors, including how long you hold the cryptocurrency, the purpose of your cryptocurrency activities, and the nature of the gains or losses. Different countries have different tax laws, so it is important to consult with a tax professional or accountant familiar with cryptocurrency taxation in your jurisdiction.

It is worth noting that tax authorities are increasingly focusing on cryptocurrency transactions and cracking down on individuals and businesses that fail to report their cryptocurrency income. In the United States, the IRS has issued guidance stating that virtual currency transactions are subject to federal income tax rules, and failure to report cryptocurrency income can result in civil penalties and even criminal charges.

Even if you are not actively buying or selling cryptocurrency, you may still have tax obligations if you receive cryptocurrency as payment for goods or services. For example, if you are a freelancer or business owner and your clients pay you in cryptocurrency, the value of the cryptocurrency at the time of receipt needs to be reported as income.

It is important to keep accurate records of your cryptocurrency transactions, including the date, value, and purpose of each transaction. This will help ensure that you accurately report your cryptocurrency income and capital gains when filing your taxes.

In the next sections, we will explore the different types of taxation that may apply to your cryptocurrency activities, including capital gains tax, reporting requirements, deductions, and strategies for minimizing your tax burden.

Differentiating between capital gains and ordinary income

When it comes to taxing cryptocurrency, it is important to understand the distinction between capital gains and ordinary income. Depending on the nature of your crypto activities, your earnings may be classified as one or the other, and the tax implications can vary.

Capital gains typically refer to the profits earned from buying and selling cryptocurrency as an investment. If you hold a cryptocurrency for a certain period of time and then sell it at a higher price, the resulting profit is considered a capital gain. On the other hand, if you buy a cryptocurrency and use it to purchase goods or services, any increase or decrease in its value at the time of the transaction may be treated as ordinary income.

The classification of your cryptocurrency earnings as either capital gains or ordinary income depends on several factors, including your intention when acquiring the cryptocurrency, the holding period, and the frequency and nature of your trading activities.

If you are actively trading cryptocurrencies with a high frequency and for short periods of time, your profits may be considered ordinary income. This is similar to how profits from day trading stocks or other securities are treated. On the other hand, if you hold a cryptocurrency for a longer period of time with the intention of investing, any gains from selling it would likely be treated as capital gains.

The tax rates for capital gains and ordinary income can also differ. In many jurisdictions, including the United States, capital gains are subject to different tax rates based on the length of time the asset was held. If you hold a cryptocurrency for less than a year before selling it, the gains may be considered short-term capital gains and taxed at your regular income tax rate. If you hold the cryptocurrency for more than a year, the gains may be considered long-term capital gains and taxed at a lower rate.

It is important to keep detailed records of your cryptocurrency transactions, including the purchase price, sale price, and holding period. Accurately classifying your earnings as capital gains or ordinary income and properly reporting them on your tax return will help ensure compliance with tax laws and minimize the risk of audits or penalties.

Consulting with a tax professional or accountant familiar with cryptocurrency taxation in your jurisdiction is highly recommended to ensure you understand the specific rules and regulations that apply to your situation.

How are capital gains taxed?

When it comes to taxable cryptocurrency transactions, understanding how capital gains are taxed is crucial. The tax treatment of capital gains from cryptocurrency can vary depending on your jurisdiction, holding period, and other factors.

In general, capital gains from the sale or exchange of cryptocurrency are subject to taxation. However, the tax rates and rules for capital gains can differ between short-term and long-term holdings.

In the United States, for example, short-term capital gains are taxed at the individual’s ordinary income tax rate. This means that if you hold a cryptocurrency for less than a year before selling it, the gains will be treated as short-term capital gains and taxed at your regular income tax rate. The specific tax rate depends on your income level and tax bracket.

On the other hand, long-term capital gains are subject to lower tax rates. In the United States, if you hold a cryptocurrency for more than a year before selling it, the gains will be treated as long-term capital gains. For most individuals, the long-term capital gains tax rate is lower than their ordinary income tax rate. The specific long-term capital gains tax rates depend on your income level and filing status.

It is important to note that tax laws and rates can vary between countries and jurisdictions. Some countries may have different tax rates for short-term and long-term capital gains, while others may have a flat tax rate for all capital gains. Additionally, there may be specific rules or exemptions for cryptocurrency transactions, so it is recommended to consult with a tax professional or accountant familiar with your local tax laws.

Calculating your capital gains for cryptocurrency can be complex, especially if you have multiple transactions or have acquired cryptocurrency through different means (such as mining or airdrops). Proper record-keeping is essential to accurately calculate your gains and losses. Keep track of the purchase price, sale price, transaction fees, and any other relevant information for each cryptocurrency transaction.

It is important to report your capital gains from cryptocurrency on your tax return and pay any applicable taxes. Failure to report your cryptocurrency transactions and pay taxes can result in penalties, fines, or even legal consequences.

Properly understanding and fulfilling your tax obligations related to capital gains from cryptocurrency will help you stay compliant with tax laws and avoid potential issues with tax authorities.

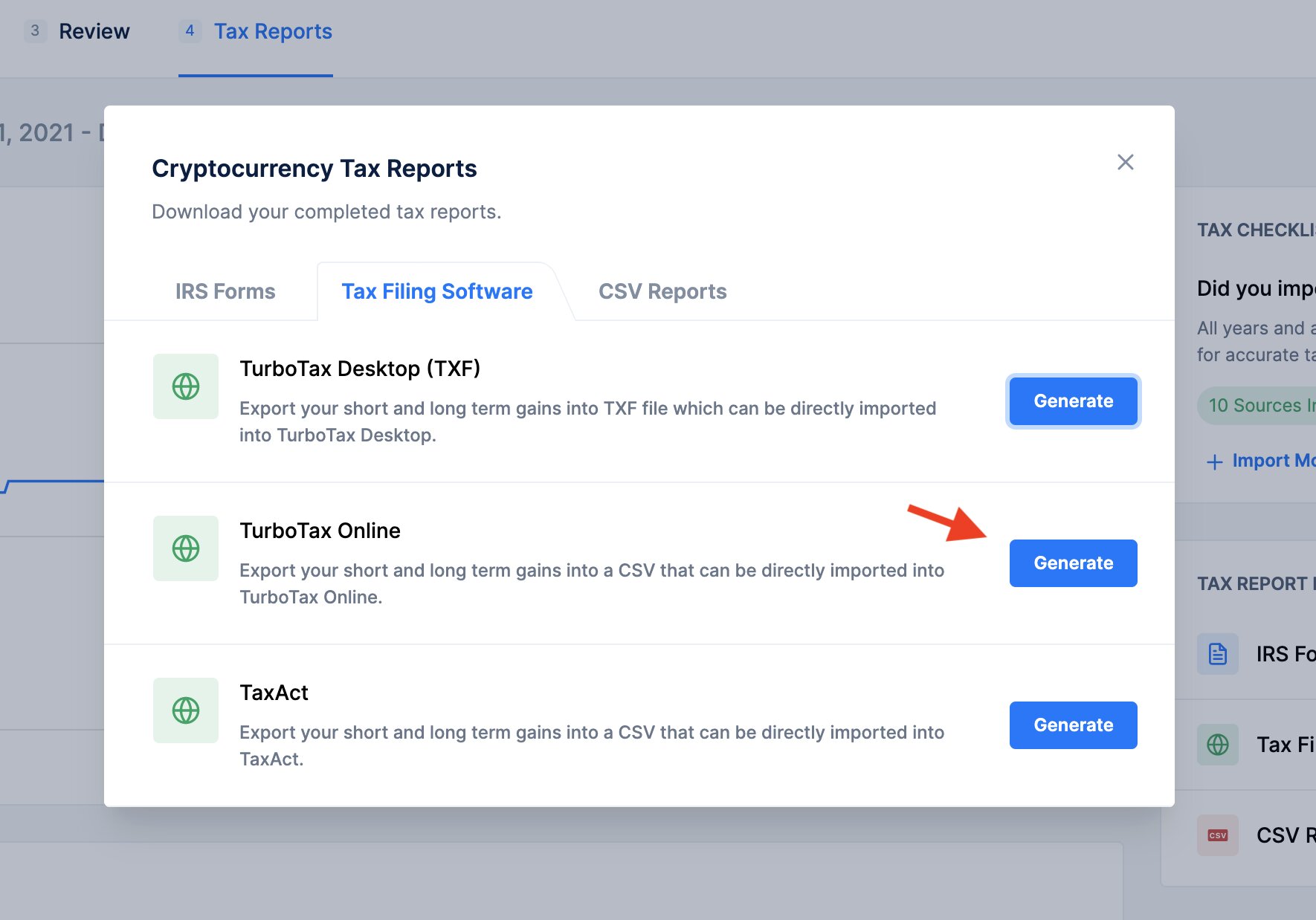

Reporting cryptocurrency transactions

When it comes to taxes and cryptocurrency, proper reporting of your transactions is essential to ensure compliance with tax laws. Reporting your cryptocurrency transactions accurately and in a timely manner will help you avoid penalties, audits, and other potential issues with tax authorities.

The specific reporting requirements for cryptocurrency transactions can vary between countries and jurisdictions. However, here are some general guidelines that can help you navigate the process:

1. Keep detailed records: It is crucial to maintain thorough records of all your cryptocurrency transactions. This includes information such as the date of the transaction, the value in your local currency at the time of the transaction, the type of transaction (buying, selling, trading, mining, etc.), and any associated fees. Proper record-keeping will make it easier for you to calculate your gains and losses and report them accurately.

2. Calculate your gains and losses: Using the information from your records, calculate the gains and losses from your cryptocurrency transactions. This involves determining the difference between the purchase price and the sale price or the fair market value at the time of the transaction.

3. Use the correct tax forms: Most tax authorities require you to report your cryptocurrency transactions on your tax return. This may involve using specific forms or schedules dedicated to reporting capital gains and losses. Be sure to use the appropriate forms and follow the instructions provided by your tax authority.

4. Report all taxable transactions: It is important to report all taxable cryptocurrency transactions, including buying, selling, trading, and receiving cryptocurrency as payment. Even if you are unsure about the tax implications of a particular transaction, it is better to err on the side of caution and report it.

5. Understand reporting thresholds: Some jurisdictions may have reporting thresholds for cryptocurrency transactions. For example, in the United States, if your cryptocurrency transactions result in gains or losses below a certain threshold, you may not be required to report them. However, it is still advisable to keep accurate records of all transactions for future reference and to be prepared in case the threshold is lowered or eliminated in the future.

6. Consider seeking professional assistance: Cryptocurrency taxation can be complex, and tax laws are constantly changing. It is wise to consult with a tax professional or accountant who is familiar with cryptocurrency taxation in your jurisdiction. They can provide guidance and ensure that you are fulfilling your reporting requirements accurately.

Remember, reporting your cryptocurrency transactions is crucial for remaining compliant with tax laws and avoiding any potential penalties or legal issues. By staying organized and keeping accurate records, you can navigate the reporting process with confidence.

Keeping track of your cryptocurrency investments

Keeping track of your cryptocurrency investments is essential for several reasons. It allows you to accurately calculate your gains and losses, monitor the performance of your investments, and fulfill your tax reporting requirements. Here are some tips to help you effectively manage and track your cryptocurrency investments:

1. Use a dedicated portfolio tracking tool: There are numerous portfolio tracking tools available that are specifically designed for managing cryptocurrency investments. These tools allow you to input your transactions, monitor the value of your holdings in real-time, and generate reports for tax purposes. Some popular portfolio tracking tools include CoinTracker, CoinTracking, and Delta.

2. Keep a detailed transaction history: Maintain a comprehensive record of all your cryptocurrency transactions. This includes information such as the date, time, and value of each transaction, as well as any fees incurred. You can use spreadsheets or journals to log your transactions, or you can rely on portfolio tracking tools mentioned earlier that automatically store this data for you.

3. Track your cost basis: Knowing the cost basis of your cryptocurrency investments is crucial for calculating your gains and losses. The cost basis is the original purchase price of the cryptocurrency, including any fees incurred during the purchase. By tracking the cost basis of each cryptocurrency holding, you can accurately determine your gains or losses when you sell or trade them.

4. Consider using labels or tags: As your cryptocurrency portfolio grows, it may become challenging to track each specific investment. Consider using labels or tags to categorize your investments based on factors such as the purpose (e.g., long-term investment, trading), the type of cryptocurrency, or the exchange used. This will help you analyze the performance of different segments of your portfolio more effectively.

5. Regularly update and reconcile your records: It is important to keep your records up to date by entering new transactions and reconciling them with your bank statements or exchange histories. This ensures the accuracy of your portfolio and makes it easier to identify any discrepancies or errors.

6. Factor in external factors: Cryptocurrency values can fluctuate based on external factors such as news events, regulatory developments, or market trends. Consider keeping track of relevant news articles or market analysis to better understand the factors influencing the value of your investments.

7. Backup your data: Back up your cryptocurrency investment records regularly to avoid any potential loss of data. Consider using secure cloud storage or external hard drives to protect your valuable information.

By implementing these practices, you can effectively keep track of your cryptocurrency investments, monitor their performance, and ensure accurate reporting for tax purposes. Regularly reviewing and analyzing your portfolio will also enable you to make informed decisions about buying, selling, or holding your cryptocurrencies.

Tax implications of mining and staking

Participating in cryptocurrency mining and staking can have specific tax implications that you need to be aware of. The tax treatment of mining and staking activities varies depending on your jurisdiction and the specific circumstances of your involvement. Here are some key points to consider:

Mining: Cryptocurrency mining involves using powerful computers to solve complex mathematical problems in order to validate and record new transactions on the blockchain. Miners, in return, are often rewarded with newly created cryptocurrency. From a tax perspective, mining activities are considered as ordinary income. The value of the cryptocurrency received as a mining reward is typically included in your taxable income at the fair market value at the time of receipt.

Staking: Staking involves actively participating in a proof-of-stake (PoS) blockchain network by holding and “staking” a certain amount of cryptocurrency. By doing so, you are validating and securing transactions on the network and, as a reward, you may receive additional cryptocurrency. Similar to mining, staking rewards are generally considered as ordinary income and should be reported accordingly.

Expenses and deductions: When mining or staking cryptocurrencies, you may incur expenses related to equipment, electricity, maintenance, or staking fees. In some jurisdictions, these expenses may be deductible against your mining or staking income, reducing your overall tax liability. It is important to keep detailed records of these expenses for proper documentation and potential deductions.

Reporting requirements: It is crucial to keep accurate records of your mining or staking activities, including the dates of each transaction, the value of the cryptocurrency received, any associated fees, and relevant expenses. These records will help you accurately report your income and expenses when filing your taxes. Depending on your jurisdiction, you may need to report your mining or staking income on specific tax forms or schedules dedicated to self-employment income or miscellaneous income. Consult with a tax professional to understand the specific reporting requirements in your jurisdiction.

Timeframe and valuation: Determining the fair market value of the cryptocurrency received from mining or staking can be challenging, especially as cryptocurrency prices can be volatile. The value of the cryptocurrency is generally determined at the time of receipt, and you must report it accordingly. There are various methods you can use to determine the fair market value, including using reputable cryptocurrency exchanges or platforms that provide historical price data.

Additional considerations: It is important to note that tax laws and regulations surrounding mining and staking activities are evolving and can vary widely between jurisdictions. It is essential to stay informed about any changes or updates to the tax regulations in your specific area and seek guidance from a tax professional who is experienced in cryptocurrency taxation.

Understanding the tax implications of mining and staking activities will help ensure that you fulfill your reporting and payment obligations accurately. Keeping detailed records, seeking professional advice, and staying informed about relevant tax regulations will help you navigate the tax complexities associated with these activities.

Tax treatment of cryptocurrency received as payment

As cryptocurrency gains wider acceptance in the business world, it’s important to understand the tax implications of receiving cryptocurrency as payment for goods or services. The tax treatment of cryptocurrency received as payment can vary depending on your jurisdiction and the specific circumstances of the transaction. Here are some key considerations:

Recognition of income: When you receive cryptocurrency as payment, the fair market value of the cryptocurrency at the time of receipt is considered taxable income. This means that you will need to report the value of the cryptocurrency received as income on your tax return, just as you would with traditional forms of payment such as cash or check.

Determining fair market value: Determining the fair market value of the cryptocurrency can be a challenge, especially considering the volatility of cryptocurrency prices. It is generally recommended to use reputable cryptocurrency exchanges or platforms to determine the fair market value at the time of receipt. Some jurisdictions may have specific guidance on how to determine the fair market value for tax purposes. Consult with a tax professional or accountant familiar with cryptocurrency taxation in your jurisdiction for guidance.

Timing of recognition: The timing of recognizing income from cryptocurrency received as payment may depend on whether you are operating as an individual or a business. For individuals, the income is typically recognized at the time of receipt. However, for businesses, the income may be recognized at the time of sale or conversion of the cryptocurrency into fiat currency. Different countries may have different rules regarding the timing of recognition, so it is important to consult with a tax professional or accountant to ensure compliance with local regulations.

Reporting requirements: Just like any other income, you will need to report the cryptocurrency received as payment on your tax return. In some jurisdictions, specific forms or schedules may need to be used to report this income. Keep accurate records of the date, value, and purpose of each cryptocurrency transaction to facilitate accurate reporting.

Cost basis for future transactions: The fair market value at the time of receipt will also serve as the cost basis for future tax calculations. If you later sell or exchange the cryptocurrency you received as payment, you will need to calculate the capital gains or losses based on the difference between the fair market value at the time of receipt and the subsequent sale price.

Additional considerations: It is important to note that tax laws surrounding cryptocurrency can be complex and vary between jurisdictions. It is recommended to consult with a tax professional or accountant familiar with cryptocurrency taxation to ensure compliance with the specific regulations in your area.

Understanding the tax treatment of cryptocurrency received as payment is essential to ensure accurate reporting and compliance with tax laws. Keeping detailed records and seeking professional advice can help you navigate the complexities of cryptocurrency taxation and minimize your tax obligations.

Tax deductions and credits for cryptocurrency activities

When it comes to cryptocurrency activities, there may be opportunities to take advantage of tax deductions and credits to help lower your overall tax liability. While the specific deductions and credits available can vary depending on your jurisdiction, here are some common considerations:

Business expenses: If you are involved in cryptocurrency activities as a business or self-employed individual, you may be able to deduct certain expenses related to your operations. This can include costs such as equipment, software, office space, professional services, and marketing expenses. Keeping detailed records of your business expenses is crucial to support your deductions and ensure accurate reporting.

Mining and staking expenses: If you are engaged in cryptocurrency mining or staking, the expenses incurred in these activities can often be deducted. This can include costs related to mining equipment, electricity, maintenance, and staking fees. As with other business expenses, it is important to keep records of these expenses for proper documentation and potential deductions.

Home office deduction: If you use a dedicated space in your home for cryptocurrency-related activities, you may be eligible for a home office deduction. The deduction allows you to deduct a portion of your home-related expenses, such as rent, mortgage interest, utilities, and home insurance, based on the percentage of your home used for business purposes. However, there are specific criteria and rules that need to be met to qualify for this deduction, so it’s important to consult with a tax professional for guidance.

Education and training: Expenses related to education and training in cryptocurrency and blockchain technology may also be eligible for tax deductions. This can include the cost of books, courses, conferences, and seminars that are directly related to improving your skills and knowledge in the cryptocurrency field. Be sure to keep receipts and records of your education-related expenses for potential deductions.

R&D tax credits: In some jurisdictions, there may be research and development (R&D) tax credits available for activities related to cryptocurrency development or innovation. These credits can help offset some of the costs incurred in developing new technologies or improving existing ones. If you are involved in cryptocurrency-related R&D activities, it’s worth exploring whether you qualify for these tax credits.

Consult with a tax professional: Due to the complexity of tax laws and the evolving nature of cryptocurrency regulations, it is highly recommended to consult with a tax professional or accountant who specializes in cryptocurrency taxation. They can help you identify eligible deductions and credits based on your specific circumstances and ensure that you take full advantage of any tax-saving opportunities.

Remember to keep thorough and accurate records of your expenses, income, and any supporting documentation to substantiate your deductions and credits. By understanding the available tax breaks and seeking professional guidance, you can optimize your tax situation and reduce your overall tax liability related to cryptocurrency activities.

Tax strategies for minimizing cryptocurrency taxes

Minimizing your tax liability related to cryptocurrency activities requires careful planning and consideration of various strategies. While the specific strategies available may depend on your jurisdiction and individual circumstances, here are some common tactics that can help reduce your cryptocurrency taxes:

Holding cryptocurrencies for the long term: By holding your cryptocurrencies for more than a year, you may benefit from long-term capital gains tax rates, which are typically lower than short-term rates. This strategy allows you to take advantage of potential tax savings by reducing the tax rate applied to your capital gains when you eventually sell or exchange the cryptocurrencies.

Utilizing tax-efficient investment accounts: Some jurisdictions offer tax-advantaged investment accounts, such as Individual Retirement Accounts (IRAs) or Self-Invested Personal Pensions (SIPPs), that allow you to invest in cryptocurrencies with certain tax benefits. These accounts can provide advantages, such as tax-free growth or tax-deferred gains, which can help minimize your tax liability on cryptocurrency investments. It’s important to consult with a tax professional or financial advisor to understand the specific rules and eligibility criteria for such accounts in your jurisdiction.

Strategically harvesting losses: If you have cryptocurrency investments that have experienced losses, you may consider strategically selling these investments to realize the losses. These capital losses can be used to offset capital gains, reducing your overall tax liability. This strategy is known as tax loss harvesting. However, be mindful of any wash sale rules, which restrict the ability to claim a loss if you repurchase the same or a substantially identical asset within a specific timeframe.

Balancing gains and losses: Managing your cryptocurrency portfolio to balance gains and losses can be a tax-efficient strategy. By strategically selling investments with gains and losses, you can offset the gains with losses, potentially reducing your taxable income. This approach allows you to maximize your tax benefits by minimizing the amount of capital gains subject to taxation.

Contributing to retirement accounts: Contributing a portion of your cryptocurrency gains to a retirement account, such as a Traditional IRA or a self-employed retirement plan, can offer tax advantages. These contributions may help reduce your current taxable income, allowing you to defer taxes on the contributions and potential gains until you withdraw the funds during retirement.

Consulting with a tax professional: Cryptocurrency taxation is complex and constantly evolving. Working with a tax professional or accountant who specializes in cryptocurrency taxation is highly recommended. They can provide personalized advice based on your specific situation and help you navigate the intricacies of cryptocurrency taxes. They can also help you stay updated with any changes in tax laws or regulations that may affect your cryptocurrency tax planning.

Remember, tax strategies should be approached with careful consideration and in compliance with the tax laws of your jurisdiction. It is essential to maintain accurate records, stay informed about relevant regulations, and seek professional guidance to optimize your tax position and minimize your cryptocurrency tax liability.

Common mistakes to avoid when filing cryptocurrency taxes

Filing your cryptocurrency taxes accurately is crucial for ensuring compliance with tax laws and avoiding potential penalties or audits. To help navigate the complexities of cryptocurrency taxation, it’s important to avoid these common mistakes:

1. Failure to report cryptocurrency transactions: One of the most critical mistakes is simply not reporting your cryptocurrency transactions on your tax return. Whether it’s buying, selling, trading, or receiving cryptocurrency as payment, all taxable transactions should be reported. Failure to do so can result in penalties and legal consequences.

2. Disregarding the value of cryptocurrency received as payment: When you receive cryptocurrency as payment for goods or services, it’s essential to determine the fair market value of the cryptocurrency at the time of receipt and report it as income. Neglecting to include this value can lead to underreporting of your taxable income.

3. Overlooking cryptocurrency-to-cryptocurrency transactions: If you exchange one cryptocurrency for another, it is important to understand that this transaction may trigger capital gains or losses. Each cryptocurrency-to-cryptocurrency exchange should be considered a taxable event, and the gains or losses should be reported accordingly.

4. Ignoring the tax implications of airdrops and hard forks: Airdrops, which involve receiving free cryptocurrency tokens, and hard forks, which result in the creation of new cryptocurrencies, can have tax implications. It is important to stay informed about the tax treatment of airdrops and hard forks in your jurisdiction and report them correctly.

5. Inadequate record-keeping: Keeping detailed and accurate records of your cryptocurrency transactions is crucial. Failing to maintain proper records can make it challenging to calculate gains and losses, provide documentation for deductions and credits, and substantiate your reporting in the event of an audit. Utilize portfolio tracking tools or maintain meticulous spreadsheets to record all relevant information.

6. Misunderstanding the tax classification of cryptocurrency: Cryptocurrency is often classified as property by tax authorities, which means that different tax rules apply compared to traditional currencies. Familiarize yourself with the tax laws and regulations specific to your jurisdiction to ensure proper reporting and compliance.

7. Neglecting to consult a tax professional: Cryptocurrency taxation is a complex and rapidly evolving field. Seeking guidance from a tax professional or accountant with expertise in cryptocurrency taxation is highly recommended. They can help you navigate the intricacies of cryptocurrency taxes, ensure accurate reporting, and identify potential deductions or credits that may minimize your tax liability.

8. Failing to stay updated on tax regulations: The taxation of cryptocurrency is constantly changing as governments worldwide adapt to this emerging technology. Make a commitment to stay informed about any updates or changes to the tax laws and regulations in your jurisdiction. This will help you stay compliant and avoid any potential tax pitfalls.

By avoiding these common mistakes and taking proactive steps to educate yourself on cryptocurrency taxation, you can ensure accurate reporting, minimize your tax liability, and maintain compliance with tax laws.

What to do if you haven’t been paying cryptocurrency taxes

If you have been involved in cryptocurrency activities and haven’t been paying taxes on your earnings, it’s important to take steps to rectify the situation. Failing to report and pay taxes on your cryptocurrency income can result in penalties, fines, and even legal consequences. Here are some steps to consider if you find yourself in this situation:

1. Assess your tax obligations: Start by evaluating your cryptocurrency activities and determining your tax obligations. Review your transaction history, including buying, selling, trading, and receiving cryptocurrency as payment, and calculate the income, gains, or losses derived from these activities.

2. Organize your records: Gather and organize any documentation and records related to your cryptocurrency transactions. This includes transaction histories, receipts, trade confirmations, and any other relevant information that can help substantiate your tax reporting.

3. Seek professional guidance: Consult with a tax professional or accountant who specializes in cryptocurrency taxation. They can provide guidance based on your specific situation and help you understand the steps you need to take to become compliant with tax laws. A professional can assist in accurately reporting your past cryptocurrency activities and determining any back taxes owed.

4. Participate in voluntary disclosure programs: Many jurisdictions offer voluntary disclosure programs that provide an opportunity to come forward and report past cryptocurrency income voluntarily. These programs may offer reduced penalties or other incentives to encourage individuals to correct their tax reporting. Check with your local tax authority to see if such programs exist in your jurisdiction.

5. Amend past tax returns: If you failed to report cryptocurrency income on your previous tax returns, you will likely need to file amended tax returns to correct the oversight. Work with your tax professional to prepare and file the necessary amended returns accurately.

6. Pay any back taxes owed: It’s important to address any tax liabilities from past years as soon as possible. Determine the amount of back taxes owed based on your corrected tax returns and make arrangements to pay the outstanding amount. Depending on your circumstances, you may be able to set up a payment plan or negotiate with tax authorities to resolve the owed taxes.

7. Stay compliant in the future: Moving forward, ensure that you stay compliant with tax laws and regulations regarding your cryptocurrency activities. Keep detailed records of all your transactions, report your income accurately, and pay any applicable taxes in a timely manner.

Remember, it’s always better to address any tax issues proactively. Failing to address past tax obligations can lead to increased penalties, fines, and additional stress. By taking the necessary steps to rectify the situation and becoming compliant, you can avoid further complications and ensure your tax responsibilities are properly fulfilled.

Conclusion

Understanding and fulfilling your tax obligations related to cryptocurrency is essential for staying compliant with tax laws and avoiding potential penalties. Whether you are buying, selling, trading, mining, or receiving cryptocurrency as payment, it is important to be aware of the tax implications and properly report your activities. Here are some key takeaways to remember:

– Cryptocurrency is considered property by tax authorities, and profits from cryptocurrency activities are subject to taxation.

– Capital gains and ordinary income are taxed differently, so it’s important to understand the distinction and how they apply to your cryptocurrency activities.

– Accurate record-keeping is crucial for calculating gains and losses, reporting transactions, and substantiating your tax reporting.

– Seek guidance from a tax professional or accountant who specializes in cryptocurrency taxation to ensure compliance and take advantage of available deductions or credits.

– Stay informed about tax laws and regulations specific to cryptocurrency in your jurisdiction, as they may change over time.

– If you have been non-compliant with cryptocurrency taxes, take proactive steps to rectify the situation by assessing your tax obligations, organizing your records, seeking professional guidance, and addressing any back taxes owed.

Remember, this article is intended for informational purposes only and should not be considered as professional tax advice. Tax laws and regulations vary between jurisdictions, so it’s important to consult with a qualified tax professional or accountant who can provide personalized advice based on your specific circumstances.

By adhering to tax laws, understanding the tax implications of your cryptocurrency activities, and seeking professional guidance when needed, you can navigate the complexities of cryptocurrency taxation and ensure that you fulfill your tax obligations while optimizing your tax position. Stay informed, stay organized, and stay compliant to enjoy the benefits of cryptocurrency while avoiding any potential tax-related issues.