Overview of Bitcoin and Taxes

Bitcoin, the first decentralized cryptocurrency, has gained significant popularity and value over the years. As it continues to grow in prominence, it’s crucial for individuals who own, transact, or invest in Bitcoin to understand the tax implications associated with it.

For tax purposes, the Internal Revenue Service (IRS) treats Bitcoin as property rather than currency. This means that any transactions involving Bitcoin are subject to taxation, similar to buying or selling stocks or other assets.

Whether you earn Bitcoin through mining, receive it as payment for goods or services, or purchase it on an exchange, you are required to report the income and comply with tax regulations. Failure to comply can lead to penalties, interest, and even legal consequences.

When it comes to reporting Bitcoin on your taxes, there are several key considerations you need to be aware of:

- Bitcoin as Property: The IRS considers Bitcoin as a form of property, which means that it is subject to capital gains tax. This means that when you sell or exchange Bitcoin, the difference between the purchase price and the selling price will be subject to tax.

- Bitcoin Income: If you receive Bitcoin as payment for goods or services, the fair market value of the Bitcoin at the time of receipt needs to be included as income on your tax return. This applies to freelancers, contractors, and businesses that accept Bitcoin as a form of payment.

- Bitcoin Sales or Exchanges: When you sell or exchange Bitcoin for cash, other cryptocurrencies, or goods and services, it is considered a taxable event. The gain or loss from the transaction needs to be reported on your tax return.

- Bitcoin Cost Basis: Calculating the cost basis of your Bitcoin is crucial for determining gains or losses when you sell or exchange it. The cost basis is the purchase price of the Bitcoin plus any expenses incurred, such as transaction fees or mining costs.

- Bitcoin Mining Expenses: If you mine Bitcoin, the expenses incurred in the mining process, such as electricity costs and mining equipment, may be deductible as business expenses. However, it’s important to consult a tax professional to determine the specific deductions you qualify for.

It’s important to note that tax regulations surrounding Bitcoin can be complex and may vary based on your jurisdiction. Therefore, seeking the guidance of a knowledgeable tax professional is highly recommended to ensure compliance with all applicable tax laws and avoid any potential issues with the IRS.

By understanding the basic concepts of Bitcoin taxation and staying informed about any updates or changes to tax regulations, you can navigate the world of cryptocurrency taxation with confidence and peace of mind.

Understanding Bitcoin as Property for Tax Purposes

When it comes to taxation, the Internal Revenue Service (IRS) classifies Bitcoin as property rather than currency. This distinction is crucial in determining how Bitcoin transactions are taxed.

As property, Bitcoin is subject to capital gains tax. This means that any gains or losses resulting from the sale or exchange of Bitcoin are treated similarly to those from buying or selling stocks or real estate.

One implication of Bitcoin being classified as property is the need to determine the fair market value of Bitcoin at the time of a transaction. Unlike traditional currency, Bitcoin’s value is known to be extremely volatile. Therefore, it’s essential to accurately track the value of Bitcoin when you receive it, sell it, or exchange it for goods or services.

For individuals who receive Bitcoin as payment for goods or services, the fair market value of the Bitcoin at the time of receipt must be reported as income on their tax return. This means that even if you don’t convert the Bitcoin into traditional currency, you are still responsible for reporting its value as income.

Similarly, when you sell or exchange Bitcoin for cash, other cryptocurrencies, or goods and services, the difference between the purchase price and the selling price is considered a capital gain or loss. If you held the Bitcoin for one year or less before selling or exchanging it, it is classified as a short-term capital gain or loss. If you held it for more than one year, it is classified as a long-term capital gain or loss.

Calculating the capital gain or loss requires determining the cost basis of the Bitcoin. The cost basis is the purchase price of the Bitcoin plus any expenses incurred during the acquisition, such as transaction fees. The difference between the fair market value at the time of purchase and the selling price is then used to calculate the gain or loss.

It’s important to maintain accurate records of all Bitcoin transactions, including the dates of acquisition and sale, the fair market value at the time of each transaction, and any associated expenses. This documentation will be essential for accurately reporting your Bitcoin-related income and capital gains or losses.

By understanding and adhering to the IRS classification of Bitcoin as property, you can ensure that you accurately report and comply with the tax regulations surrounding Bitcoin transactions. Consulting a tax professional familiar with cryptocurrency taxation can provide further guidance in navigating this complex area of taxation.

Reporting Bitcoin Income

Bitcoin income refers to any form of payment received in the form of Bitcoin for goods, services, or as part of a mining operation. It is important to understand the tax implications of Bitcoin income and properly report it on your tax return.

If you receive Bitcoin as payment for goods or services, the fair market value of the Bitcoin at the time of receipt needs to be included as income on your tax return. This applies to freelancers, contractors, and businesses that accept Bitcoin as a form of payment.

When reporting Bitcoin income, it is crucial to keep accurate records of the fair market value of the Bitcoin at the time of receipt. This can be done by referencing reputable Bitcoin exchanges or financial websites that provide historical price data.

It’s important to note that even if you do not convert the Bitcoin into traditional currency at the time of receipt, you are still required to report it as income. Failure to report Bitcoin income accurately may result in penalties and interest.

For taxpayers who receive a significant amount of Bitcoin income, it is recommended to consult a tax professional for guidance. They can assist in properly reporting the income and identifying any potential deductions or credits that may be applicable.

In addition to reporting Bitcoin income, it is also necessary to keep track of any associated expenses. For example, if you incurred expenses related to Bitcoin mining, such as electricity costs or equipment purchases, these expenses may be deductible as business expenses.

When reporting Bitcoin income and deducting expenses, it is vital to maintain detailed records and documentation. This includes records of transactions, invoices, receipts, and any other supporting documents relevant to the income and expenses.

By accurately reporting Bitcoin income and maintaining thorough documentation, you can ensure compliance with tax regulations and minimize the risk of audits or penalties. When in doubt, seeking the guidance of a tax professional experienced in cryptocurrency taxation is recommended to navigate the complexities of reporting Bitcoin income effectively.

Reporting Bitcoin Sales or Exchanges

When you sell or exchange Bitcoin for cash, other cryptocurrencies, or goods and services, it is considered a taxable event. This means that any gains or losses resulting from the transaction need to be reported on your tax return.

Calculating and reporting the gains or losses from Bitcoin sales or exchanges requires determining the cost basis and the fair market value of the Bitcoin at the time of the transaction.

The cost basis is the purchase price of the Bitcoin plus any expenses incurred during the acquisition, such as transaction fees. The fair market value is the price of the Bitcoin at the time of the sale or exchange.

If the fair market value at the time of the transaction is higher than the cost basis, you have a capital gain. Conversely, if the fair market value is lower than the cost basis, you have a capital loss.

If you held the Bitcoin for one year or less before selling or exchanging it, the capital gain or loss is classified as short-term. If you held it for more than one year, it is classified as long-term.

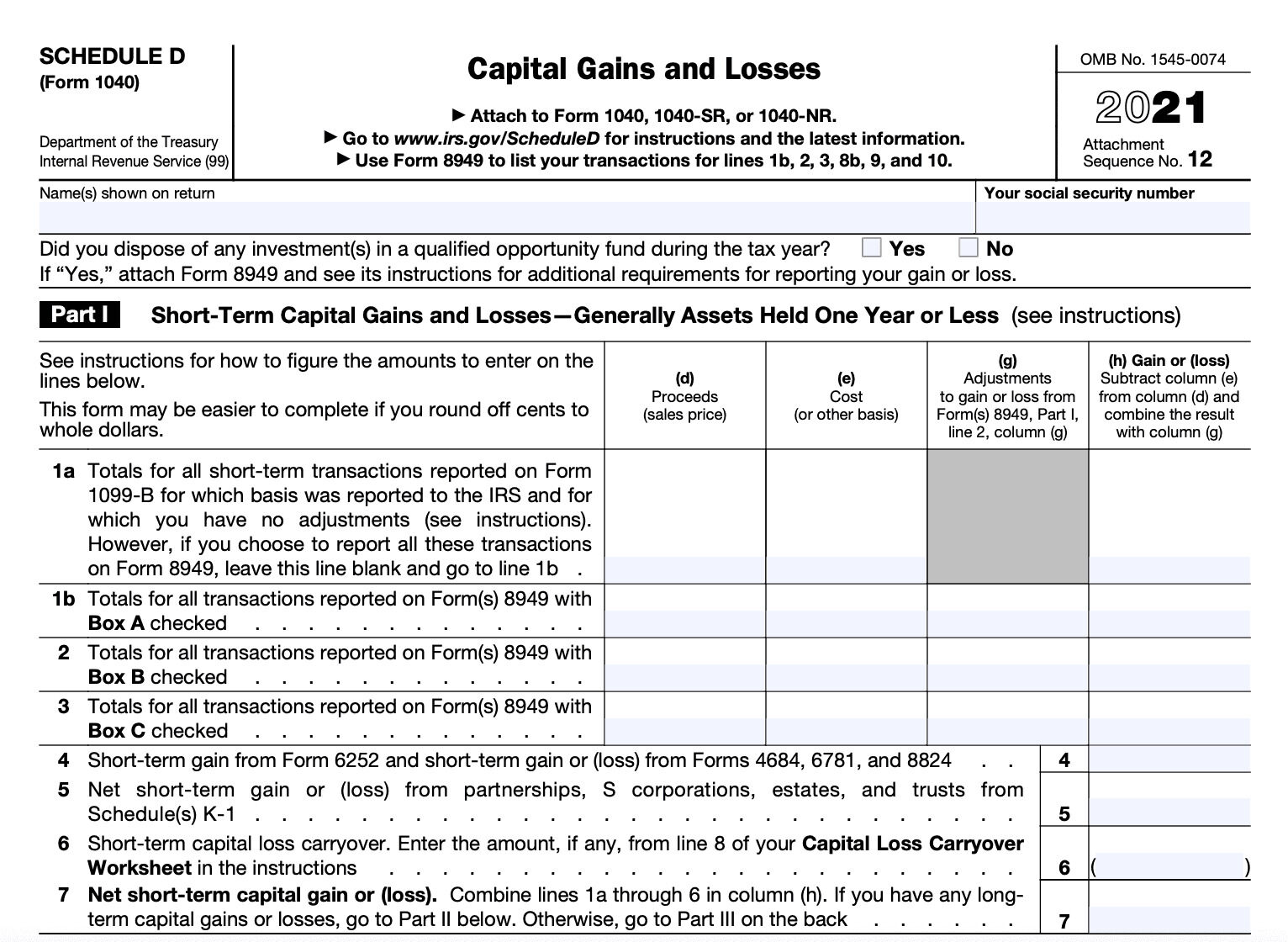

When reporting Bitcoin sales or exchanges, it is important to accurately calculate the gains or losses and report them on the appropriate tax forms. In the United States, this is usually done using Form 8949 and Schedule D.

It’s essential to keep detailed records of all Bitcoin sales or exchanges, including the dates of acquisition and sale, the cost basis, the fair market value, and any associated expenses. This documentation will help ensure accurate reporting and compliance with tax regulations.

If you conducted numerous Bitcoin transactions throughout the year, it may be beneficial to use cryptocurrency tax software or consult a tax professional experienced in cryptocurrency taxation. These resources can help streamline the process and ensure accurate reporting.

It’s important to note that tax regulations surrounding Bitcoin sales or exchanges can be complex and may vary based on your jurisdiction. Therefore, consulting a tax professional is highly recommended to ensure compliance with all applicable tax laws and avoid any potential issues with the tax authorities.

By properly reporting Bitcoin sales or exchanges and keeping detailed records, you can fulfill your tax obligations and minimize the risk of audits or penalties. Staying informed about any updates or changes to tax regulations concerning cryptocurrencies is also crucial for accurate reporting.

Calculating Bitcoin Cost Basis

Calculating the cost basis of your Bitcoin is a vital step in determining the gains or losses when you sell or exchange it. The cost basis is the purchase price of the Bitcoin plus any expenses incurred during the acquisition.

When calculating the cost basis of Bitcoin, it’s important to consider the following factors:

- Purchase Price: The initial purchase price of the Bitcoin is the starting point for calculating the cost basis. This is the amount you paid to acquire the Bitcoin, whether it was obtained through a cryptocurrency exchange or through other means.

- Exchange Fees: Transaction fees incurred during the acquisition of Bitcoin should be included in the cost basis. These fees are typically charged by cryptocurrency exchanges for facilitating the purchase or sale of Bitcoin.

- Transfer Fees: If you transferred Bitcoin from one wallet or exchange to another, any associated transfer fees should be added to the cost basis. These fees, charged by the network for validating and confirming transactions, can vary depending on the network congestion at the time of transfer.

- Mining Costs: If you obtained Bitcoin through mining, the cost basis would include the expenses incurred during the mining process. This may include the cost of mining equipment, electricity, cooling, and maintenance costs.

- Fiat Conversion Costs: If you converted fiat currency, such as USD, to Bitcoin, any fees or costs associated with the fiat-to-Bitcoin conversion should be factored into the cost basis. These costs can include banking fees or fees charged by payment processors.

When calculating the cost basis, it’s essential to keep accurate records of all the factors mentioned above. This documentation will help support the cost basis calculations and ensure accurate reporting of gains or losses.

For individuals who acquired Bitcoin at different times and different prices, the cost basis can become more complex. In such cases, it may be beneficial to use a tax software specifically designed for cryptocurrency or seek the guidance of a tax professional familiar with cryptocurrency taxation.

It’s important to note that tax regulations surrounding Bitcoin and cost basis calculations can differ based on your jurisdiction. Therefore, staying informed about the specific tax laws in your country or seeking professional assistance is crucial to ensure compliance and accurate reporting.

By accurately calculating the cost basis of your Bitcoin and maintaining detailed records, you can determine the gains or losses when you sell or exchange it and fulfill your tax obligations.

Deducting Bitcoin Mining Expenses

If you are involved in Bitcoin mining, it is important to understand that the expenses incurred in the mining process may be deductible as business expenses.

Bitcoin mining involves using powerful computer systems to solve complex algorithms and validate transactions on the Bitcoin network. However, it also requires significant amounts of electricity, specialized mining equipment, cooling systems, and ongoing maintenance costs.

When it comes to tax deductions, consult with a tax professional familiar with cryptocurrency taxation to ensure compliance with relevant tax laws in your jurisdiction. They can help identify which expenses related to Bitcoin mining may be deductible and guide you through the documentation and reporting requirements.

Here are some common expenses associated with Bitcoin mining that may be eligible for deductions:

- Electricity Costs: Mining Bitcoin requires a substantial amount of electricity, which can result in high energy bills. Typically, a portion of these costs can be deducted as a business expense.

- Mining Equipment: The cost of purchasing or leasing mining equipment, including ASIC (Application-Specific Integrated Circuit) miners, can be deductible. However, depending on the tax laws in your jurisdiction, the depreciation of the equipment may need to be spread over several tax years.

- Cooling and Maintenance: As mining equipment generates heat, cooling systems are necessary to maintain optimal operating conditions. The costs associated with cooling and maintenance, including repairs and replacements, may be eligible for deduction.

- Internet and Hosting Fees: If you incur expenses for high-speed internet connectivity and hosting services to operate your mining operation, these costs may be deductible. However, it’s important to track and document these expenses appropriately.

- Mining Pool Fees: If you participate in a mining pool, which is a group of miners that combine their resources to increase their chances of earning rewards, the fees associated with joining the pool may be deductible. However, only the portion of the fees directly related to your mining activities can be deducted.

It’s important to note that the deductibility of Bitcoin mining expenses may vary based on your jurisdiction and the specific tax laws in place. Meeting the criteria for deductibility, such as operating as a business and generating a profit motive, may also be necessary.

Keeping accurate records of all Bitcoin mining expenses is crucial to support your deductions and ensure compliance with tax regulations. Documentation should include invoices, receipts, bank statements, and any other relevant financial records pertaining to your mining operation.

Consult a tax professional to navigate the complex world of deducting Bitcoin mining expenses and to optimize your tax return based on the specific regulations in your jurisdiction.

Reporting Bitcoin Gifts and Donations

Bitcoin has become an increasingly popular asset to give as gifts or donate to charitable causes. However, it’s essential to understand the tax implications and reporting requirements when dealing with Bitcoin gifts and donations.

If you receive Bitcoin as a gift, the fair market value of the Bitcoin at the time of the gift needs to be included in your income for tax purposes. This means that you may be liable for income tax on the fair market value of the Bitcoin received as a gift.

When it comes to donating Bitcoin to charitable organizations, the tax treatment is similar to that of donating other types of property. If you donate Bitcoin to a qualified charitable organization, you may be able to claim a tax deduction for the fair market value of the Bitcoin at the time of the donation.

It’s important to note that the tax deduction for charitable donations of Bitcoin can vary depending on the tax laws in your jurisdiction. You should consult with a tax professional or refer to the tax regulations specific to your country to determine the specific deductibility rules and any limitations that may apply.

When reporting Bitcoin gifts or donations, it’s crucial to keep accurate records. For gifts, you should have documentation showing the fair market value of the Bitcoin at the time of the gift. This can be obtained from reputable Bitcoin exchanges or financial websites that provide historical price data.

For charitable donations, you should obtain a written acknowledgment from the charitable organization that specifies the date of the donation, the fair market value of the Bitcoin at the time of the donation, and any restrictions placed on the donation.

If you are making significant Bitcoin gifts or donations, it is advisable to consult with a tax professional experienced in cryptocurrency taxation. They can guide you through the reporting process and help maximize your potential tax benefits.

It’s important to accurately report Bitcoin gifts and donations to comply with tax regulations and avoid any potential issues with the tax authorities. Failing to report or misreporting Bitcoin gifts and donations can lead to penalties and interest.

By understanding the tax implications and reporting requirements for Bitcoin gifts and donations, you can ensure compliance with tax laws and potentially take advantage of tax benefits related to charitable giving.

International Tax Considerations for Bitcoin

As Bitcoin is a digital currency that operates on a decentralized network, it presents unique international tax considerations for individuals who engage in Bitcoin transactions across borders. It is crucial to understand these considerations to ensure compliance with tax regulations and avoid any potential issues.

The tax treatment of Bitcoin can vary significantly from one country to another. Some countries may view Bitcoin as a currency, while others classify it as property or a commodity. These different classifications can impact how Bitcoin transactions are taxed across borders.

One important consideration for international Bitcoin transactions is the determination of the jurisdiction in which taxes are owed. This can depend on factors such as residency, citizenship, and the source of income. It’s important to consult with a tax professional or refer to the tax regulations specific to your country to understand your tax obligations.

Another consideration is the reporting of foreign Bitcoin accounts or holdings. Some countries require individuals to report their holdings in foreign financial accounts, including Bitcoin wallets or exchanges, if the total value of these accounts exceeds a certain threshold. Failure to report foreign accounts can result in penalties or legal consequences.

Transferring Bitcoin across borders can also have tax implications. In some jurisdictions, transferring Bitcoin may trigger capital gains or other taxable events. It’s important to understand the tax regulations of both the country you are sending Bitcoin from and the country you are sending it to.

Additionally, if you are a business or self-employed individual accepting Bitcoin as payment from international customers, you may need to consider international tax regulations related to foreign income, withholding taxes, and reporting requirements. Consulting with a tax professional experienced in international taxation can help navigate these complexities.

Double taxation is another concern when it comes to international Bitcoin transactions. Double taxation occurs when the same income is subject to taxation in both the country where it was earned and the country of residence. Many countries have tax treaties in place to prevent or mitigate double taxation. Understanding these treaties and seeking guidance from a tax professional can help ensure that you do not pay more than your fair share of taxes.

Given the evolving nature of Bitcoin and the rapid developments in international tax regulations related to cryptocurrency, it’s crucial to stay informed about any updates or changes in tax laws. Engaging the services of a tax professional who specializes in international cryptocurrency taxation can help ensure compliance and optimize your tax situation.

By understanding and addressing the international tax considerations for Bitcoin, you can navigate the complexities of cross-border transactions and ensure compliance with tax regulations in your home country and abroad.

Common Mistakes to Avoid when Reporting Bitcoin on Taxes

Reporting Bitcoin on taxes can be complex and challenging, particularly due to the evolving nature of cryptocurrency taxation. To ensure accurate reporting and compliance with tax regulations, it’s essential to avoid these common mistakes:

- Failing to Report Bitcoin Income: Some individuals may overlook or intentionally not report Bitcoin income, whether it is received as payment for goods or services or earned through mining. Failing to report Bitcoin income can result in penalties, interest, and potential legal consequences.

- Incorrectly Reporting Bitcoin Sales or Exchanges: When selling or exchanging Bitcoin for cash, other cryptocurrencies, or goods and services, it’s important to accurately calculate the gains or losses and report them on the appropriate tax forms. Incorrectly reporting Bitcoin sales or exchanges can lead to erroneous tax liabilities.

- Underestimating or Overestimating Bitcoin Cost Basis: The cost basis of Bitcoin is critical for determining gains or losses when selling or exchanging it. Underestimating or overestimating the cost basis can result in incorrect calculations and potential inaccuracies on your tax return.

- Ignoring Tax Reporting for Bitcoin Mining: Individuals who mine Bitcoin may overlook the tax reporting obligations associated with mining activities. Expenses incurred in the mining process, such as electricity costs and mining equipment, may be deductible as business expenses, and failing to report them can result in missed deductions and potential audit triggers.

- Not Keeping Accurate Records: Detailed and accurate record-keeping is essential when dealing with Bitcoin. Failing to keep records of Bitcoin transactions, including dates, fair market values, cost basis, and associated expenses, can lead to difficulties in reporting and substantiating your tax positions.

- Failure to Understand International Tax Considerations: For individuals engaging in cross-border Bitcoin transactions, failing to understand the international tax considerations can result in non-compliance and potential double taxation. It’s crucial to be aware of the tax regulations in both your home country and the country of the transaction.

- Not Seeking Professional Guidance: Due to the complexities of Bitcoin taxation, it’s advisable to seek the guidance of a tax professional who is knowledgeable in cryptocurrency taxation. They can help navigate the intricacies, provide accurate advice, and ensure compliance with tax regulations.

By avoiding these common mistakes and taking a proactive approach to Bitcoin tax reporting, you can minimize the risk of errors, penalties, and potential legal issues. Staying informed about new developments in cryptocurrency taxation and seeking professional assistance when needed will help ensure accurate reporting and peace of mind.

Resources for Bitcoin Tax Reporting

When it comes to reporting Bitcoin on taxes, there are various resources available to help individuals navigate the complexities of cryptocurrency taxation. These resources can provide valuable information, tools, and guidance to ensure accurate reporting and compliance with tax regulations. Here are some key resources to consider:

- Tax Professionals: Consulting with a tax professional who specializes in cryptocurrency taxation can provide personalized guidance tailored to your specific tax situation. They can help you understand the reporting requirements, identify eligible deductions, and ensure compliance with tax laws.

- Cryptocurrency Tax Software: There are several cryptocurrency tax software solutions available that can streamline the reporting process. These software options can help calculate gains and losses, track transactions, generate tax forms, and ensure accurate reporting. Research and select a reputable tax software that suits your needs and supports the tax regulations in your jurisdiction.

- Tax Authorities Websites: The tax authorities in many countries provide comprehensive information on cryptocurrency taxation on their websites. These resources can include official guidelines, tax forms, publications, and frequently asked questions related to reporting Bitcoin on taxes. Checking the websites of your country’s tax authority can provide the most up-to-date and accurate information.

- Online Communities and Forums: Engaging in online communities and forums dedicated to cryptocurrency taxation can provide valuable insights and discussions. These communities often have experienced individuals who can share their knowledge and experiences related to reporting Bitcoin on taxes. It’s important to engage in reputable platforms and consider multiple perspectives.

- Industry Organizations and Associations: Some industry organizations and associations focus on cryptocurrency taxation and provide resources to their members. These organizations may offer educational materials, webinars, conferences, and networking opportunities that can enhance your understanding of Bitcoin tax reporting. Consider joining relevant organizations to access their resources and stay updated on industry developments.

- Official Documentation and Publications: Many tax authorities and financial regulatory bodies release official documentation and publications related to cryptocurrency taxation. These resources can provide in-depth guidance on reporting Bitcoin on taxes, including specific scenarios and examples. Accessing and studying these official documents can ensure accurate reporting and compliance.

It’s important to note that tax regulations and reporting requirements for Bitcoin can vary by jurisdiction. Therefore, it’s crucial to consult resources specific to your country or seek professional advice to ensure compliance with the applicable tax laws.

By utilizing these resources and staying informed about cryptocurrency taxation, you can enhance your understanding of reporting Bitcoin on taxes and navigate this complex area with confidence and accuracy.

Conclusion

Reporting Bitcoin on taxes is a crucial responsibility for individuals who own, transact, or invest in this popular cryptocurrency. Understanding the tax implications and accurately reporting Bitcoin-related income, sales, exchanges, and expenses is essential to ensure compliance with tax regulations and avoid penalties or legal issues.

Throughout this guide, we have explored various aspects of reporting Bitcoin on taxes, including understanding Bitcoin as property, reporting Bitcoin income, sales, exchanges, calculating cost basis, deducting mining expenses, reporting gifts and donations, international tax considerations, as well as common mistakes to avoid.

To navigate the complexities of Bitcoin tax reporting effectively, it is highly recommended to seek the guidance of a tax professional specializing in cryptocurrency taxation. They can provide personalized advice, ensure compliance with tax laws, and help optimize your tax situation.

In addition to professional assistance, utilizing resources such as cryptocurrency tax software, tax authority websites, online communities, industry organizations, and official documentation can enhance your understanding and streamline the reporting process.

Accurate record-keeping is crucial when it comes to Bitcoin tax reporting. Maintaining detailed records of transactions, fair market values, cost basis, and associated expenses will support your reporting and help substantiate your tax positions.

Furthermore, staying informed about updates in tax regulations and international tax considerations is essential, as the cryptocurrency taxation landscape continues to evolve rapidly.

By following the guidelines outlined in this guide and utilizing the available resources, you can navigate the world of Bitcoin tax reporting with confidence and ensure compliance with tax regulations while optimizing your tax situation.