Introduction

Bitcoin, the revolutionary digital currency, has gained immense popularity and interest in recent years. It offers a decentralized and peer-to-peer system that allows individuals to make secure transactions without the need for intermediaries like banks. Understanding how Bitcoin transactions work is crucial for anyone looking to dive into the world of cryptocurrencies.

Bitcoin is not a physical currency but rather a digital asset that exists solely in the virtual realm. It operates on a technology called blockchain, which is a public ledger that records all transactions made with Bitcoin. These transactions are transparent, secure, and cannot be altered, making Bitcoin a reliable and trustworthy form of digital currency.

In this article, we will explore the process of how Bitcoin transactions work, from generating a Bitcoin wallet to verifying transactions and adding them to the blockchain. We will also discuss the role of miners in confirming the transactions and the concept of transaction fees.

By gaining a better understanding of how Bitcoin transactions work, you will be equipped with the knowledge to navigate the world of cryptocurrencies and make informed decisions regarding your digital assets.

So, let’s dive into the intricacies of Bitcoin transactions and uncover the fascinating inner workings of this groundbreaking technology.

What is Bitcoin?

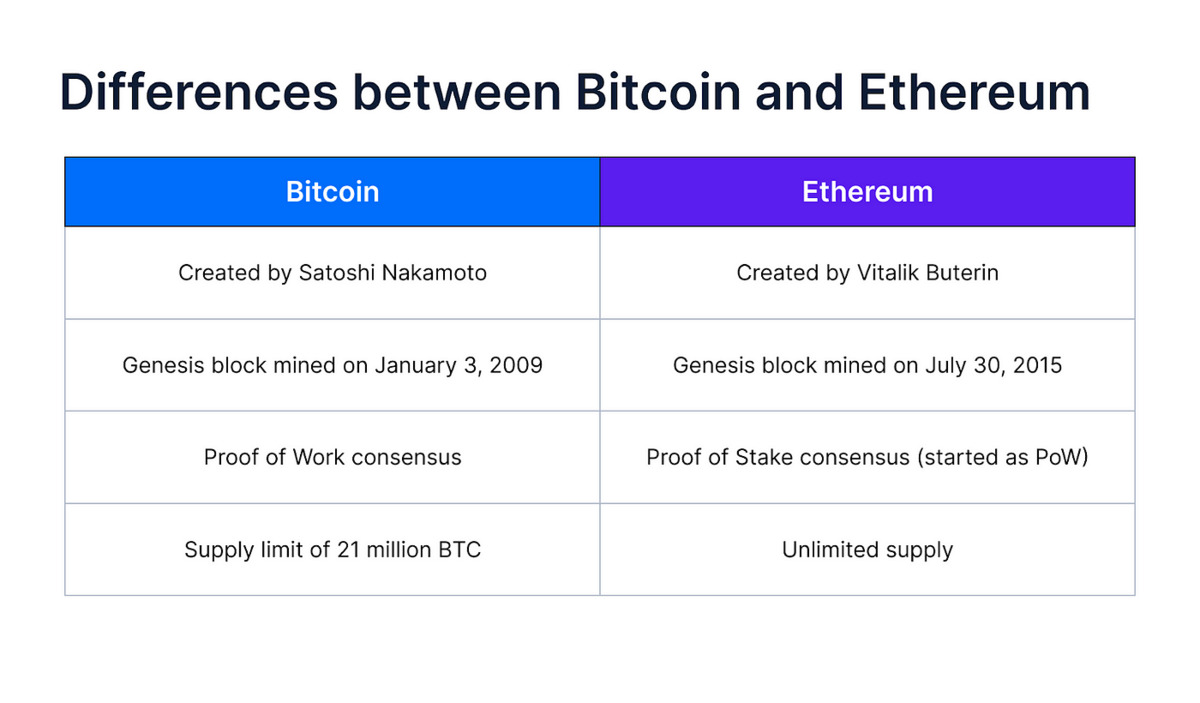

Bitcoin is a digital currency that was created in 2009 by an unknown individual or group of individuals using the pseudonym Satoshi Nakamoto. Unlike traditional currencies such as the US dollar or the euro, Bitcoin is not backed by any government or central authority. Instead, it operates on a decentralized network called blockchain.

At its core, Bitcoin is a revolutionary concept that enables individuals to make direct transactions with each other without the need for intermediaries. It provides a secure and anonymous way to transfer value across the internet, making it an attractive alternative to traditional banking systems.

Bitcoins are created through a process called mining. Mining involves using powerful computers to solve complex mathematical problems, which in turn validates and verifies transactions on the Bitcoin network. This process also generates new Bitcoins as a reward for the miners’ efforts.

One of the key features of Bitcoin is its limited supply. There will only ever be 21 million Bitcoins in existence, which creates scarcity and contributes to its value. Unlike traditional fiat currencies, which can be subject to inflation, the finite supply of Bitcoin helps maintain its purchasing power.

Bitcoin transactions are recorded on the blockchain, a decentralized ledger that is maintained by a network of computers, known as nodes. This transparent and incorruptible system ensures that transactions cannot be altered or tampered with, providing a high level of security.

Bitcoin has gained widespread adoption and acceptance in various industries, including online retail, travel, and even real estate. It offers benefits such as lower transaction fees, faster international transfers, and greater control over one’s financial assets.

As a digital currency, Bitcoin is stored in virtual wallets. These wallets can be accessed through a unique address and private key, which ensures the security and ownership of the Bitcoins. It is important to safeguard these keys to prevent unauthorized access and potential loss of funds.

In summary, Bitcoin is a decentralized digital currency that operates on the blockchain, providing a secure and efficient way to transfer value between parties. Its limited supply, transparency, and independence from central authorities make it an appealing option for those seeking financial freedom and control.

How do Bitcoin transactions work?

Bitcoin transactions are the backbone of the entire Bitcoin network. They enable individuals to send and receive Bitcoins securely and anonymously. Understanding how Bitcoin transactions work is essential for anyone looking to participate in the cryptocurrency ecosystem.

Here is a step-by-step explanation of how Bitcoin transactions work:

- Generating a Bitcoin Wallet: To send or receive Bitcoins, users need a Bitcoin wallet. This wallet consists of two cryptographic keys: a public key, which is shared with others for receiving funds, and a private key, which is kept secret and used to access and transfer the Bitcoins. Wallets can be software-based or hardware devices.

- Creating a Transaction: When a user wants to send Bitcoins to another user, they create a transaction by specifying the recipient’s address and the amount of Bitcoin to be sent. The transaction is then signed with the sender’s private key to authenticate and authorize the transfer.

- Verifying the Transaction: Once the transaction is created, it is broadcasted to the Bitcoin network, where it is verified by the network’s nodes. These nodes validate the transaction by confirming that the sender has sufficient funds and that the transaction meets the protocol rules.

- Adding the Transaction to the Blockchain: Once the transaction is verified, it is included in a block. A block is a collection of transactions that are added to the blockchain in a sequential and immutable manner. Each block contains a unique identifier called a hash, which links it to the previous block, forming a chain of blocks.

- Miners Confirm the Transaction: Miners play a vital role in the Bitcoin network. They compete to solve complex mathematical problems, which allows them to add new blocks to the blockchain. Once a miner solves a problem, they broadcast the solved block to the network, and other miners verify its validity. This process ensures that all transactions in the block are legitimate.

- Updates to Wallet Balances: Once a transaction is confirmed and added to the blockchain, the recipient’s wallet balance is updated to reflect the newly received Bitcoins. On the other hand, the sender’s wallet balance is reduced by the amount sent, ensuring that double spending is prevented.

- Transaction Fees: Bitcoin transactions often include a transaction fee, which is a small amount paid by the sender to incentivize miners to include their transaction in the next block. The transaction fee helps prioritize transactions, and higher fees usually result in faster confirmations.

By following these steps, Bitcoin transactions are executed securely, efficiently, and transparently. The decentralized nature of the blockchain ensures that transactions cannot be altered or reversed once they are confirmed, making Bitcoin a viable alternative to traditional financial systems.

Generating a Bitcoin Wallet

Before engaging in Bitcoin transactions, users need to generate a Bitcoin wallet. A wallet is a software or hardware device that allows individuals to securely store, send, and receive Bitcoins.

Here are the key steps involved in generating a Bitcoin wallet:

- Choose a Wallet Type: There are several types of Bitcoin wallets to choose from based on personal preferences and security needs. Software wallets, such as desktop or mobile wallets, are convenient and easy to use. Hardware wallets, on the other hand, are physical devices that offer increased security by storing the private keys offline.

- Download and Install a Wallet: If opting for a software wallet, users need to download and install the wallet software onto their chosen device. Wallets are typically available for various operating systems, such as Windows, macOS, Linux, iOS, and Android.

- Create a Wallet: Once the software wallet is installed, users can create a new wallet by generating a unique seed phrase, also known as a recovery phrase or backup phrase. This seed phrase consists of a series of randomly generated words that act as a master key for the wallet. It is crucial to back up and securely store this phrase as it is the only way to restore access to the wallet if the device is lost or damaged.

- Set a Strong Password or PIN: To enhance the security of the wallet, users should set a strong password or personal identification number (PIN). It is recommended to use a combination of uppercase and lowercase letters, numbers, and special characters.

- Receive and Share the Public Key: After the wallet is created, it generates a unique public key, also known as a Bitcoin address. This address is used to receive Bitcoins from other users. Users can share their public key with others, either by providing the address or by generating a QR code for easy scanning.

- Backup the Wallet: Regular backups are essential to prevent the loss of Bitcoins. Many wallets offer the option to create encrypted backups, which should be stored securely offline or on a separate device. It is important to regularly update and test the backup to ensure its validity.

Generating a Bitcoin wallet is the first step towards participating in the Bitcoin network. By following these steps and maintaining proper security measures, users can have a secure and reliable wallet to send, receive, and store their Bitcoins.

Creating a Transaction

Once a Bitcoin wallet is generated and set up, users can start creating transactions to send Bitcoins to other individuals or entities. Creating a transaction involves specifying the recipient’s address and the amount of Bitcoin to be sent, and then signing the transaction with the sender’s private key for authentication.

Let’s explore the process of creating a Bitcoin transaction:

- Access the Wallet: To create a transaction, users need to access their Bitcoin wallet through the wallet software or device. This requires entering the wallet’s password or PIN to unlock it securely.

- Specify the Recipient: Users need to provide the recipient’s Bitcoin address or scan the recipient’s QR code. This address is a unique string of characters that identifies the recipient’s wallet.

- Enter the Amount: Users need to specify the amount of Bitcoin they want to send to the recipient. The wallet software typically provides options to enter the amount in various units, such as BTC (Bitcoin) or satoshis (the smallest unit of Bitcoin).

- Optional Transaction Fee: Depending on the wallet software and current network conditions, users may have the option to include a transaction fee. Including a fee incentivizes miners to include the transaction in their blocks, leading to faster confirmations. The higher the fee, the more priority the transaction receives.

- Review and Confirm: Before finalizing the transaction, users should review all the details, including the recipient’s address, the amount, and the transaction fee. It is essential to double-check the information to ensure accuracy and avoid any potential mistakes.

- Sign the Transaction: Once satisfied with the transaction details, the user must sign the transaction with their private key. This cryptographic signature ensures that only the owner of the private key can authorize the transaction.

- Broadcast the Transaction: After signing the transaction, users can broadcast it to the Bitcoin network. This involves sending the transaction details to the network’s nodes, which will validate and verify the transaction’s authenticity.

Once the transaction is created and broadcasted, it starts its journey through the Bitcoin network for verification and confirmation. It is important to note that Bitcoin transactions are irreversible, meaning once confirmed and added to the blockchain, they cannot be reversed or modified.

By following these steps, users can successfully create a Bitcoin transaction and initiate the process of sending Bitcoins to recipients securely and efficiently.

Verifying the Transaction

After a Bitcoin transaction is created, it needs to be verified by the network nodes to ensure its validity. Verifying a transaction is crucial for maintaining the integrity and security of the Bitcoin network. Let’s explore the process of verifying a Bitcoin transaction:

- Transaction Propagation: Once a transaction is created, it is broadcasted to various nodes within the Bitcoin network. These nodes act as validators and propagate the transaction to other connected nodes in the network.

- Validation Rules: Each node receiving the transaction applies a set of validation rules to determine its legitimacy. These rules include verifying that the transaction is properly formatted, has valid inputs and outputs, and adheres to the consensus rules of the Bitcoin network.

- UTXO Verification: Nodes check if the inputs of the transaction are referred to as Unspent Transaction Outputs (UTXOs) and confirm that these UTXOs have not been spent in previous transactions. This process ensures that the sender has sufficient funds to cover the transaction amount.

- Double Spending Prevention: Nodes also verify that the transaction being propagated is not a double spend, meaning the same Bitcoin inputs are not used in multiple transactions simultaneously. This prevents fraudulent manipulation of the Bitcoin network.

- Consensus Verification: Nodes reach a consensus by communicating with each other to agree on the validity of the transaction. If a majority of nodes agree that the transaction is valid, it is considered confirmed and ready to be added to a block in the blockchain.

- Confirmation Time: The time taken for a transaction to be confirmed varies depending on network congestion and the transaction fee offered by the sender. Miners prioritize transactions with higher fees, so including an appropriate fee can help speed up the confirmation process.

- Confirmation Status: Once a transaction receives the required number of confirmations, typically six confirmations for high-value transactions, it is considered fully verified and permanently recorded on the blockchain. Each confirmation adds another block to the chain, making the transaction increasingly secure.

Verifying a transaction ensures that only valid and legitimate transactions are added to the blockchain. This process is crucial for maintaining the integrity and security of the Bitcoin network and preventing fraudulent or malicious activities.

By understanding the steps involved in verifying a Bitcoin transaction, users can have confidence in the safety and reliability of their transactions within the decentralized network.

Adding the Transaction to the Blockchain

Once a Bitcoin transaction is verified and confirmed by the network nodes, it is added to the blockchain – the public ledger that records all transactions in a chronological order. Adding the transaction to the blockchain ensures transparency, immutability, and the overall integrity of the Bitcoin network.

Let’s explore the process of adding a transaction to the blockchain:

- Block Formation: Transactions on the Bitcoin network are grouped together into blocks. Generally, multiple transactions are selected to be included in a block, depending on their size and the capacity of the block. The maximum block size is currently set at 1 megabyte (MB).

- Block Header: Each block contains a unique identifier called a block header. The block header includes information such as the block’s version, timestamp, previous block hash, and a nonce. The nonce is a number that miners change repeatedly while mining to find a valid hash for the block.

- Proof of Work: Miners engage in a process called mining to find a nonce that, when combined with the other block header data, produces a hash that meets certain difficulty criteria. This computationally intensive process requires significant computational power and electricity.

- Validating the Block: Once a miner finds a valid nonce and generates a hash that meets the difficulty criteria, they broadcast the completed block to the network. Other nodes on the network validate the block by verifying the proof of work and checking that the transactions within the block are valid.

- Linking to Previous Blocks: The validated block is added to the blockchain by linking it to the previous block. Each block contains the hash of the previous block in its block header, forming a chain of blocks. This chain structure ensures the immutability and integrity of the blockchain.

- Confirmation Process: Once a block is added to the blockchain, the transactions contained within it receive their initial confirmation. As more blocks are added on top of it, subsequent confirmations increase, making the transaction more secure and less prone to manipulation.

Adding a transaction to the blockchain provides a transparent and immutable record of the transaction’s occurrence. The decentralized nature of the blockchain prevents any single entity from altering or tampering with the recorded transactions, enhancing the security and trustworthiness of the Bitcoin network.

By following this process, Bitcoin transactions become permanent and publicly visible on the blockchain, contributing to the overall transparency and reliability of the network.

Miners Confirm the Transaction

Miners play a vital role in the Bitcoin network by confirming transactions and adding them to the blockchain. They contribute their computational power to secure the network and validate the authenticity of transactions. Let’s explore how miners confirm Bitcoin transactions:

- Transaction Broadcasting: Once a transaction is created and propagated throughout the network, it reaches the miners. Miners actively listen for incoming transactions and collect them in a pool known as the mempool.

- Transaction Selection: Miners choose which transactions to include in the next block by considering factors such as transaction fees and the size of the transaction. Transactions with higher fees tend to be prioritized as miners are incentivized to maximize their earnings.

- Block Mining: Miners compete with each other to solve a complex mathematical puzzle through a process called mining. This puzzle requires substantial computational power to find a solution, known as the proof of work, that meets the network’s difficulty level.

- Adding Transactions to a Block: Once a miner successfully solves the puzzle, they create a new block, including the selected transactions from the mempool. The miner appends the block to the existing blockchain and broadcasts it to the network.

- Verification and Consensus: Other network nodes, including miners, validate the newly solved block by ensuring that the proof of work is correct and the included transactions are valid. Once a majority of nodes reach a consensus, the block is considered confirmed and added as a permanent part of the blockchain.

- Transaction Finality: When a transaction is included in a confirmed block, it gains its first confirmation. With each subsequent block added to the blockchain, the transaction receives additional confirmations, increasing its level of finality and reducing the risk of double spending or reversal.

- Blockchain Security: The decentralized and distributed nature of the blockchain, along with the consensus mechanism used by miners, ensures the security and integrity of transactions. The computational power needed to tamper with the blockchain increases as more blocks are added, making it financially impractical to alter past transactions.

Miners confirm Bitcoin transactions by dedicating their computational resources to secure the network and validate transactions. Their role in the consensus process ensures the trustworthiness, immutability, and overall integrity of the Bitcoin blockchain.

By performing complex computations and competing to solve puzzles, miners contribute to the decentralized nature of the Bitcoin network and maintain its robustness and security.

Updates to Wallet Balances

When a Bitcoin transaction is confirmed and added to the blockchain, it results in updates to the wallet balances of both the sender and the recipient. These updates reflect the movement of Bitcoin from one wallet to another. Let’s explore how wallet balances are updated after a transaction:

- Recipient’s Balance: Once a transaction is confirmed and included in a block on the blockchain, the recipient’s wallet balance is updated to reflect the newly received Bitcoins. The wallet software fetches the transaction details from the blockchain and updates the recipient’s balance accordingly.

- Deducting the Sender’s Balance: Simultaneously, the sender’s wallet deducts the sent amount from their balance. This deduction ensures that the sender cannot spend the same funds again, preventing double spending or overspending the available balance.

- Unspent Transaction Outputs (UTXOs): In Bitcoin, the balance of a wallet is determined by the sum of its unspent transaction outputs (UTXOs). Every UTXO represents the leftover amount from previous transactions that has not been spent. When a transaction occurs, the spent UTXOs are consumed, resulting in an updated balance for the wallet.

- Change Outputs: In some cases, when the sent amount is less than the total UTXOs available in the sender’s wallet, the remaining amount is transferred back to the sender as a “change” output. This change output becomes a new UTXO and contributes to the overall balance in the sender’s wallet.

- Reconciling with the Blockchain: Wallet software continuously synchronizes with the blockchain to ensure balance accuracy. It scans the blockchain to match the received transactions for each wallet and updates the balance accordingly. This process ensures that the wallet’s balance is in sync with the confirmed transactions on the blockchain.

- Wallet Security and Backup: Wallet owners should ensure the security of their private keys and regularly back up their wallets. In case of device loss or damage, a wallet backup allows for the recovery of private keys, which are required to access and control the associated Bitcoin balance.

Updates to wallet balances occur seamlessly and autonomously in the Bitcoin network. These updates reflect the transfer of Bitcoin from the sender to the recipient, ensuring accurate records of ownership and enabling users to track their available balance for future transactions.

By maintaining a secure and up-to-date wallet, users can confidently manage their Bitcoin balances and participate effectively in the decentralized economy facilitated by the blockchain.

Transaction Fees

Transaction fees are an integral part of Bitcoin transactions and play a crucial role in incentivizing miners to include transactions in blocks. In the Bitcoin network, transaction fees are voluntary and are paid by the sender to prioritize their transaction and help facilitate its confirmation. Let’s explore transaction fees in more detail:

- Importance of Transaction Fees: Transaction fees help prevent spam and incentivize miners to include transactions in blocks. When the number of transactions exceeds the capacity of a block, miners prioritize transactions with higher fees, ensuring faster confirmations.

- Fee Calculation: Transaction fees are calculated based on the size of the transaction in bytes. Larger transactions with more inputs and outputs require more data, resulting in higher fees. Wallet software usually provides recommendations on appropriate fee amounts to ensure reasonable confirmation times.

- Dynamic Fee Market: The Bitcoin network operates on a dynamic fee market, where fees fluctuate based on the supply and demand for block space. During periods of high network congestion, fees tend to rise as users compete to have their transactions prioritized by miners.

- Fee Structure: Fees consist of two components: the base fee and the fee rate. The base fee is a fixed amount, while the fee rate is the fee per byte of transaction data. Together, these components determine the total fee required for the transaction.

- Wallet Flexibility: Wallet software often allows users to adjust the transaction fee manually. Users can choose to pay a higher fee for faster confirmations or opt for a lower fee to save costs, accepting potentially longer confirmation times during periods of high network congestion.

- Economic Incentives: Miners are economically motivated to prioritize transactions with higher fees. While some miners may prioritize transactions solely based on fees, others may consider a combination of fees and other factors, such as transaction size or priority.

- Transaction Fee Impact: The fee paid does not affect the finality or security of a transaction. However, higher fees increase the probability of faster confirmations. Users should carefully consider their desired confirmation time and weigh it against the associated fee when making transaction decisions.

Transaction fees are an essential aspect of the Bitcoin network, providing a mechanism to prioritize transactions and ensure the efficiency and reliability of the system. By appropriately setting transaction fees, users can strike a balance between desired confirmations and cost-effectiveness.

Understanding transaction fees empowers users to navigate the dynamic fee market and make informed decisions regarding their Bitcoin transactions, optimizing the balance between speed, cost, and confirmation requirements.

Conclusion

Bitcoin transactions are the lifeblood of the decentralized digital currency, enabling individuals to securely and transparently send and receive Bitcoins. Understanding the process of how Bitcoin transactions work is crucial for anyone seeking to participate in the world of cryptocurrencies.

In this article, we have explored the key steps involved in Bitcoin transactions, from generating a Bitcoin wallet and creating a transaction to verifying the transaction and adding it to the blockchain. We have also discussed the role of miners in confirming transactions and the concept of transaction fees.

Bitcoin transactions operate on a decentralized network known as blockchain, which ensures transparency, security, and immutability. By following the steps involved in Bitcoin transactions, users can engage in reliable and secure peer-to-peer transactions, free from the control of intermediaries.

Through the process of generating a Bitcoin wallet, users can securely store and manage their Bitcoins. Creating a transaction involves specifying the recipient’s address, the amount of Bitcoin to be sent, and signing the transaction with the sender’s private key.

Transactions are then verified by multiple nodes within the network, ensuring their validity and preventing fraudulent activities. Validated transactions are added to the blockchain by miners, who compete to solve complex mathematical puzzles through the process of mining. The inclusion of transactions in the blockchain enhances security and guarantees the integrity of the network.

Transaction fees play a vital role in incentivizing miners and prioritizing transactions. By paying an appropriate fee, users can expedite the confirmation process and ensure speedy transactions, especially during periods of high network congestion.

In conclusion, understanding how Bitcoin transactions work empowers individuals to navigate the cryptocurrency landscape with confidence. By following the steps outlined in this article and remaining aware of the dynamics of the blockchain and transaction fees, users can engage in secure, efficient, and reliable Bitcoin transactions.