Introduction

When it comes to managing finances, investments play a crucial role in the success of businesses and individuals alike. Whether it’s stocks, bonds, or other financial instruments, investments offer the potential for growth and profitability. But have you ever wondered where investments are reflected on the balance sheet? In this article, we will explore the various aspects of investments, their classification, and how they are presented on the balance sheet.

Investments, in a financial context, refer to assets that are acquired with the intention of generating future returns. These returns can be in the form of income, such as dividends or interest, or through the appreciation in the value of the investment itself. Companies often invest their excess funds to earn a higher return than what would be achievable through traditional savings accounts or cash holdings.

Investments can be classified into two main categories: current investments and long-term investments. Current investments are those that have a maturity of less than one year or are intended to be converted into cash within the next operating cycle. On the other hand, long-term investments are held for a more extended period, typically exceeding one year.

There are several types of investments that companies can make, each with its own characteristics and risks. One common type is equity investments, which involve purchasing shares of ownership in a company. These investments provide the investor with the opportunity to participate in the company’s profits and exercise voting rights in corporate matters.

Debt investments, on the other hand, involve lending money to another party, typically through bonds or other debt securities. In exchange for the funds, the issuer promises to repay the principal amount along with periodic interest payments. Debt investments provide a fixed income stream and are generally considered less risky than equity investments.

Other investments, such as real estate, commodities, or alternative investments like hedge funds or private equity, offer additional diversification and potential returns. These investments may have unique accounting or valuation requirements based on their nature and characteristics.

In the next sections, we will delve into how investments are presented on the balance sheet, the accounting methods used, and the disclosure requirements associated with them. Understanding these aspects is essential for accurately portraying the financial position and performance of a company. So, let us now move on to further explore the exciting world of investments and their impact on the balance sheet.

Definition of Investments

It is important to have a clear understanding of what investments are before delving into their presentation on the balance sheet. In simple terms, investments are assets acquired with the expectation of earning a return in the future. They are made with the intention of generating income or capital appreciation.

Investments come in various forms and can include stocks, bonds, mutual funds, real estate, commodities, and more. Each type of investment has its own risk and return characteristics, and individuals and businesses choose their investments based on their financial goals and risk tolerance.

Investments can be classified into two broad categories, which are current investments and long-term investments. Current investments are those that are expected to be converted into cash within a year or the operating cycle of a business. These investments are typically liquid and include short-term securities such as Treasury bills or money market funds.

On the other hand, long-term investments are held for an extended period, exceeding one year. They are not intended to be converted into cash in the short term and can include stocks, bonds, real estate properties, or even ownership stakes in other businesses.

The purpose of investments is to grow wealth over time by earning a return on the initial capital invested. This return can come in the form of dividends for stocks or interest payments for bonds. In the case of real estate, investments can generate income through rental payments or capital appreciation upon selling the property.

Investments can also provide advantages in terms of diversification. By allocating funds to different types of assets or industries, investors can spread their risk and reduce the impact of any individual investment’s performance on their overall portfolio.

It’s worth noting that investments are subject to market risks and fluctuations. The value of investments can rise or fall based on various factors such as economic conditions, industry trends, geopolitical events, or changes in interest rates. As a result, careful analysis, research, and ongoing monitoring are essential for making informed investment decisions.

In summary, investments are assets acquired with the expectation of generating future returns. They can take various forms and are classified as current or long-term depending on their liquidity and time horizon. Investments are critical for wealth growth and can provide income, capital appreciation, and diversification benefits. Understanding the definition and classification of investments is fundamental to comprehending their presentation on the balance sheet and their overall impact on financial statements.

Classification of Investments

Investments can be classified into different categories based on their nature, duration, and purpose. This classification helps in understanding the financial position and strategy of a company. Generally, investments are categorized as either current investments or long-term investments.

Current Investments:

Current investments, also known as short-term investments, are assets that are expected to be converted into cash or consumed within the next year or operating cycle, whichever is longer. These investments are highly liquid and are usually held to earn a quick return or to meet short-term funding needs.

Examples of current investments include marketable securities such as treasury bills, commercial paper, or money market funds. These financial instruments are typically low-risk and offer a stable return. Companies often utilize current investments to park their excess funds temporarily and earn interest or dividends until they are required for other purposes.

Long-term Investments:

Long-term investments, as the name suggests, are assets that are held for an extended period, typically exceeding one year. These investments are not expected to be readily converted into cash within the short term and represent a commitment of funds for a more extended period.

Long-term investments can include stocks, bonds, real estate properties, venture capital, or ownership interests in other businesses. The purpose of these investments is to generate income or achieve capital appreciation over time. Companies might invest in various sectors or industries to diversify their investment portfolio and potentially increase their returns.

While long-term investments are less liquid compared to short-term investments, they have the potential to provide higher returns. However, they are also exposed to market risks and fluctuations, and their valuation may change from period to period.

It’s important to note that the classification of an investment can change based on its original intent and the circumstances surrounding it. For example, a long-term investment might become a current investment if the company decides to sell it in the short-term due to a sudden need for cash or a change in investment strategy.

In summary, investments are classified into current investments and long-term investments. Current investments are highly liquid assets that are expected to be converted into cash within a year, while long-term investments are held for an extended period, exceeding one year. Understanding the classification of investments is essential for accurately reflecting them on the balance sheet and assessing their impact on a company’s financial standing and strategy.

Current Investments

Current investments, also known as short-term investments, are assets that are expected to be converted into cash or consumed within the next year or operating cycle, whichever is longer. These investments are typically highly liquid and serve as a temporary repository for excess funds until they are needed for other purposes.

One common type of current investment is marketable securities, which include Treasury bills, commercial paper, money market funds, and short-term bonds. These financial instruments are issued by governments, corporations, or financial institutions and offer a relatively low-risk investment option. Marketable securities provide companies with a means to earn short-term returns while maintaining liquidity and preserving capital.

Money market funds are a popular choice for companies as they provide easy access to cash, often with minimal investment risk. These funds invest in highly liquid, short-term debt instruments, such as government securities and certificates of deposit. Money market funds offer stable and competitive yields, making them an attractive option for parking excess cash temporarily.

Commercial paper is another type of current investment commonly used by businesses. It is a short-term debt instrument issued by corporations to raise funding for various purposes, such as financing operations or meeting working capital needs. Commercial paper is considered safe, as it is typically issued by well-established companies with a strong credit rating.

Treasury bills, also known as T-bills, are short-term debt securities issued by governments to finance their operations. These investments are backed by the respective government’s creditworthiness, making them a low-risk option. Treasury bills have a fixed maturity of less than one year, with varying terms ranging from a few days to several months. They are bought at a discount and redeemed at face value upon maturity, providing investors with interest income.

Companies may also hold certificates of deposit (CDs) as current investments. CDs are time deposits offered by banks and credit unions, with fixed terms ranging from a few months to several years. They provide a predictable return and are FDIC-insured, making them a secure option for short-term investments.

These current investments are typically reported at their fair value on the balance sheet. Fair value is the amount that can be received from selling the investment in an orderly transaction between market participants at the measurement date. Any changes in the fair value of current investments are recognized in the income statement as unrealized gains or losses.

In summary, current investments are short-term assets that are expected to be converted into cash or consumed within the next year or operating cycle. They offer companies a means to earn short-term returns while maintaining liquidity. Common types of current investments include marketable securities like Treasury bills, commercial paper, money market funds, and certificates of deposit. These investments are reported at their fair value on the balance sheet, with any changes in value recognized in the income statement.

Long-term Investments

Long-term investments are assets that are held for an extended period, typically exceeding one year. Unlike current investments that are intended to be converted into cash within a short timeframe, long-term investments reflect a commitment of funds for a more extended period, often with the aim of generating income or achieving capital appreciation.

One common type of long-term investment is equity investments, which involve purchasing shares of ownership in other companies. Companies may acquire equity investments in other businesses with the expectation of earning a return through dividends or capital appreciation. These investments provide the investing company with potential participation in the profits and decision-making processes of the investee.

Bonds and other debt securities also fall under the category of long-term investments. When companies invest in debt instruments, they essentially lend money to another party in exchange for regular interest payments and the repayment of the principal amount at maturity. These investments provide a fixed income stream and are generally considered less risky than equity investments.

Real estate properties can also be considered long-term investments. Companies may acquire properties for rental income or capital appreciation over time. Real estate investments can be lucrative but also involve additional considerations such as property management, maintenance costs, and market conditions.

Furthermore, companies may invest in other types of long-term assets like venture capital or private equity. These investments typically involve providing funding to start-ups or high-growth companies in exchange for an ownership stake. Venture capital investments are typically riskier but offer the potential for significant returns if the investee company succeeds.

Long-term investments are reported on the balance sheet at their original cost or fair value, depending on the accounting method chosen. The cost method is used when companies do not have significant influence over the investee, and the investment is initially recorded at the purchase price. Under the equity method, the investment is initially recorded at cost, but the investor’s share of the investee’s earnings or losses is subsequently recognized in the income statement. The fair value method is used when investments are actively traded, and the market price is readily available.

It’s important for companies to regularly assess the value of their long-term investments and evaluate any impairment in their carrying value. If the fair value of the investment drops below its carrying value and the decline is considered to be other than temporary, an impairment loss is recognized in the income statement.

In summary, long-term investments represent assets held for an extended period, typically exceeding one year. They include equity investments, debt securities, real estate properties, and other long-term assets like venture capital. These investments can be reported on the balance sheet at cost or fair value, depending on the accounting method used. Regular assessments are necessary to determine any impairment in their value and to ensure accurate reporting of long-term investment holdings.

Types of Investments

Investments come in various forms and asset classes, each with its own characteristics, risks, and potential returns. Understanding the different types of investments is crucial for constructing a diversified portfolio that aligns with financial goals and risk tolerance. Let’s explore some of the common types of investments:

Stocks:

Stocks, also known as shares or equities, represent ownership in a company. When individuals or businesses invest in stocks, they become shareholders and have a claim on the company’s assets and earnings. Stocks offer the potential for capital appreciation and may also provide dividends if the company distributes profits to its shareholders.

Bonds:

Bonds are debt instruments issued by governments, municipalities, or corporations to raise capital. When investors purchase bonds, they are essentially lending money to the issuer in exchange for regular interest payments and the repayment of the principal amount at maturity. Bonds are generally considered lower risk than stocks, as they provide fixed income and have a specified maturity date.

Mutual Funds:

Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other assets. They are managed by professional fund managers who make investment decisions on behalf of the fund. Mutual funds offer investors the opportunity to gain exposure to a wide range of securities and asset classes, even with a relatively small investment amount.

Exchange-Traded Funds (ETFs):

Similar to mutual funds, ETFs also pool investors’ money and invest in a diversified portfolio of securities. However, ETFs are traded on stock exchanges, providing investors with the ability to buy and sell shares throughout the trading day at market prices. ETFs offer flexibility and transparency, and they often track specific indexes or sectors.

Real Estate:

Real estate investments involve acquiring properties, such as residential or commercial buildings, with the expectation of earning income through rental payments or capital appreciation. Real estate can provide stable cash flow and act as a hedge against inflation. Investors can participate in real estate through direct ownership, real estate investment trusts (REITs), or real estate crowdfunding platforms.

Commodities:

Commodities are basic goods or raw materials that are traded in markets. Common examples include gold, silver, oil, natural gas, agricultural products, and metals. Commodities can provide a hedge against inflation and serve as a diversification tool in investment portfolios. Investors can gain exposure to commodities through futures contracts, exchange-traded funds, or commodity-specific funds.

Derivatives:

Derivatives are financial instruments whose value is derived from an underlying asset or benchmark. Options and futures contracts are examples of derivatives. They allow investors to speculate on the price movements of assets or manage risks associated with their investment holdings. Derivatives can be complex and have potential for significant gains or losses.

These are just a few examples of the types of investments available in the financial markets. It’s important for investors to thoroughly research and understand the characteristics, risks, and potential returns of each investment type before making any investment decisions. Building a well-diversified portfolio that includes a mix of different asset classes can help mitigate risk and maximize potential returns.

Equity Investments

Equity investments, also known as stock investments, involve the purchase of shares or ownership stakes in companies. When individuals or businesses invest in equities, they become shareholders and have a proportional claim on the company’s assets, earnings, and voting rights.

Equity investments offer the potential for capital appreciation and can provide investors with a share of the company’s profits. If the company performs well and its stock price increases, investors can benefit from the rise in value. Additionally, some companies may also distribute a portion of their profits to shareholders in the form of dividends.

There are different types of equity investments, each with its own characteristics and level of risk:

Common Stocks:

Common stocks represent ownership in a company and typically carry voting rights. Shareholders of common stocks have the opportunity to participate in the company’s decision-making processes by voting on important matters such as the appointment of board members or significant corporate actions. Common stocks also allow investors to benefit from capital appreciation and dividend distributions.

Preferred Stocks:

Preferred stocks also represent ownership in a company, but they have different characteristics compared to common stocks. Preferred stockholders typically have a higher claim on the company’s assets and earnings compared to common shareholders. They have a fixed dividend rate and are paid dividends before common shareholders. However, preferred shareholders usually do not have voting rights.

Publicly Traded Stocks:

Publicly traded stocks are listed on stock exchanges and can be bought and sold by individual and institutional investors. These stocks are subject to market demand and supply, and their prices fluctuate based on various factors such as company performance, market conditions, and investor sentiment. Publicly traded stocks offer liquidity as they can be easily converted into cash.

Private Equity:

Private equity investments involve buying shares or ownership stakes in companies that are not publicly traded. Private equity investors typically invest in established companies that require capital for growth, expansion, or restructuring. Private equity investments often involve a longer holding period compared to publicly traded stocks and are subject to liquidity restrictions.

Equity investments can provide opportunities for long-term growth and the potential for significant returns. However, they also come with risks. The value of equity investments can fluctuate, and investors may experience losses if the company’s performance deteriorates or if market conditions are unfavorable.

Investors interested in equity investments should conduct thorough research and analysis to understand the company’s financial health, industry dynamics, competitive position, and growth prospects. It’s essential to assess the company’s management team, strategy, and potential risks before making investment decisions.

In summary, equity investments involve purchasing shares or ownership stakes in companies. They offer the potential for capital appreciation and participation in the company’s profits. Common stocks and preferred stocks are common types of equity investments, while publicly traded stocks and private equity investments provide different investment opportunities. Equity investments come with risks, and investors should conduct proper due diligence before making investment decisions.

Debt Investments

Debt investments involve lending money to another party in exchange for regular interest payments and the repayment of the principal amount at maturity. These investments offer a fixed income stream and are considered less risky compared to equity investments. Debt investments provide investors with the opportunity to earn a return while preserving capital.

There are various types of debt investments, each with its own characteristics and risk profiles:

Bonds:

Bonds are debt securities issued by governments, municipalities, or corporations. When investors purchase bonds, they essentially lend money to the issuer, who promises to repay the principal amount at maturity along with periodic interest payments. Bonds are typically issued with a fixed-term and a specified interest rate. They provide a stable income stream and are considered relatively safe investments, especially when issued by creditworthy entities.

Treasury Securities:

Treasury securities are bonds issued by the government to finance its operations and pay off existing debt. Treasury securities include Treasury bills (T-bills), Treasury notes, and Treasury bonds. These investments are considered the safest in the fixed-income market since they are backed by the full faith and credit of the government. Treasury securities are often used by investors as a benchmark for other debt investments.

Municipal Bonds:

Municipal bonds, also known as munis, are debt securities issued by state or local governments to fund public infrastructure projects. Municipal bonds offer tax advantages, as the interest income is typically exempt from federal income tax and, in some cases, state and local taxes. The creditworthiness of municipal bonds varies depending on the financial health of the issuing municipality.

Corporate Bonds:

Corporate bonds are debt securities issued by corporations to raise capital for various purposes, such as financing operations, expansions, or acquisitions. Corporate bonds may offer higher yields compared to government or municipal bonds, reflecting the higher level of risk associated with investing in corporate debt. The creditworthiness of corporate bonds depends on the financial health and credit rating of the issuing company.

Convertible Bonds:

Convertible bonds are debt instruments that give bondholders the option to convert their bonds into a specified number of the issuer’s common shares. These bonds offer the potential for capital appreciation if the underlying stock price increases. Convertible bonds provide investors with a combination of fixed-income stability and the opportunity to participate in potential equity growth.

High-Yield Bonds:

High-yield bonds, also known as junk bonds, are debt securities issued by companies with lower credit ratings or higher levels of financial risk. These bonds offer higher yields to compensate investors for the increased risk. High-yield bonds can provide attractive returns but also involve a greater potential for default and financial loss.

When investing in debt instruments, investors should consider factors such as credit quality, interest rate risk, maturity, and liquidity. It’s crucial to conduct thorough research and assess the financial health and creditworthiness of the issuer before making investment decisions. Diversification within the debt investment portfolio can also help reduce risk.

In summary, debt investments involve lending money to entities in exchange for fixed interest payments and the return of principal at maturity. Bond investments, including Treasury securities, municipal bonds, and corporate bonds, are common types of debt investments. Convertible bonds provide an opportunity to convert debt into equity, while high-yield bonds offer higher returns but greater risk. Understanding the characteristics and risks associated with debt investments is essential for prudent investment decision-making.

Other Investments

In addition to equity and debt investments, there are several other types of investments that individuals and businesses can consider. These alternative investments provide opportunities for diversification and potential returns outside of traditional financial markets. Let’s explore some common examples of other investments:

Real Estate Investments:

Real estate investments involve the purchase, ownership, management, or rental of properties, such as residential homes, commercial buildings, or land. Real estate provides opportunities for income generation through rental payments and the potential for capital appreciation over time. Investors can invest directly in properties or through real estate investment trusts (REITs) and real estate crowdfunding platforms.

Commodities:

Commodities are physical goods or raw materials that can be traded in markets. Common examples of commodities include gold, silver, oil, natural gas, agricultural products, and metals. Investing in commodities can provide a hedge against inflation and diversify an investment portfolio. Investors can gain exposure to commodities through futures contracts, exchange-traded funds (ETFs), or commodity-specific funds.

Hedge Funds:

Hedge funds are investment vehicles managed by professional fund managers who employ various investment strategies across different asset classes. Hedge funds may utilize leverage and derivatives to potentially generate higher returns. These funds often cater to high-net-worth individuals and institutional investors and may have specific investment restrictions and higher fees compared to traditional investment funds.

Private Equity:

Private equity investments involve purchasing shares or ownership stakes in companies that are not publicly traded. Private equity investors typically provide capital to companies for various purposes, such as growth, acquisitions, or restructuring. These investments often involve taking an active role in the management and strategic decisions of the investee company. Private equity investments can provide the potential for significant returns but are typically illiquid and involve a longer investment horizon.

Venture Capital:

Venture capital investments focus on financing early-stage or high-growth companies with the potential for impressive returns. Venture capitalists provide capital and expertise to help these companies grow and succeed. These investments carry a higher level of risk but offer the opportunity to participate in the growth of innovative and disruptive businesses.

Collectibles and Art:

Investing in collectibles, such as rare coins, stamps, or vintage cars, and art can provide the potential for capital appreciation over time. The value of collectibles and art can be influenced by factors such as rarity, demand, and market trends. Investing in collectibles requires knowledge, expertise, and a willingness to hold the investment for a longer period.

These alternative investments offer diversification and the potential for attractive returns. However, they often come with unique risks, illiquidity, and specialized knowledge requirements. It’s important for investors to thoroughly research and understand these investments before committing capital. Consulting with professionals or financial advisors who specialize in alternative investments can provide valuable guidance and help make informed investment decisions.

In summary, other investments encompass a variety of non-traditional asset classes beyond equities and debt. Real estate, commodities, hedge funds, private equity, venture capital, and collectibles are some common examples of alternative investments. These investments provide opportunities for diversification and potential returns, but they also come with unique risks and requirements. Thorough research and understanding of the specific investment type are essential for successful investments in these alternative sectors.

Presentation on the Balance Sheet

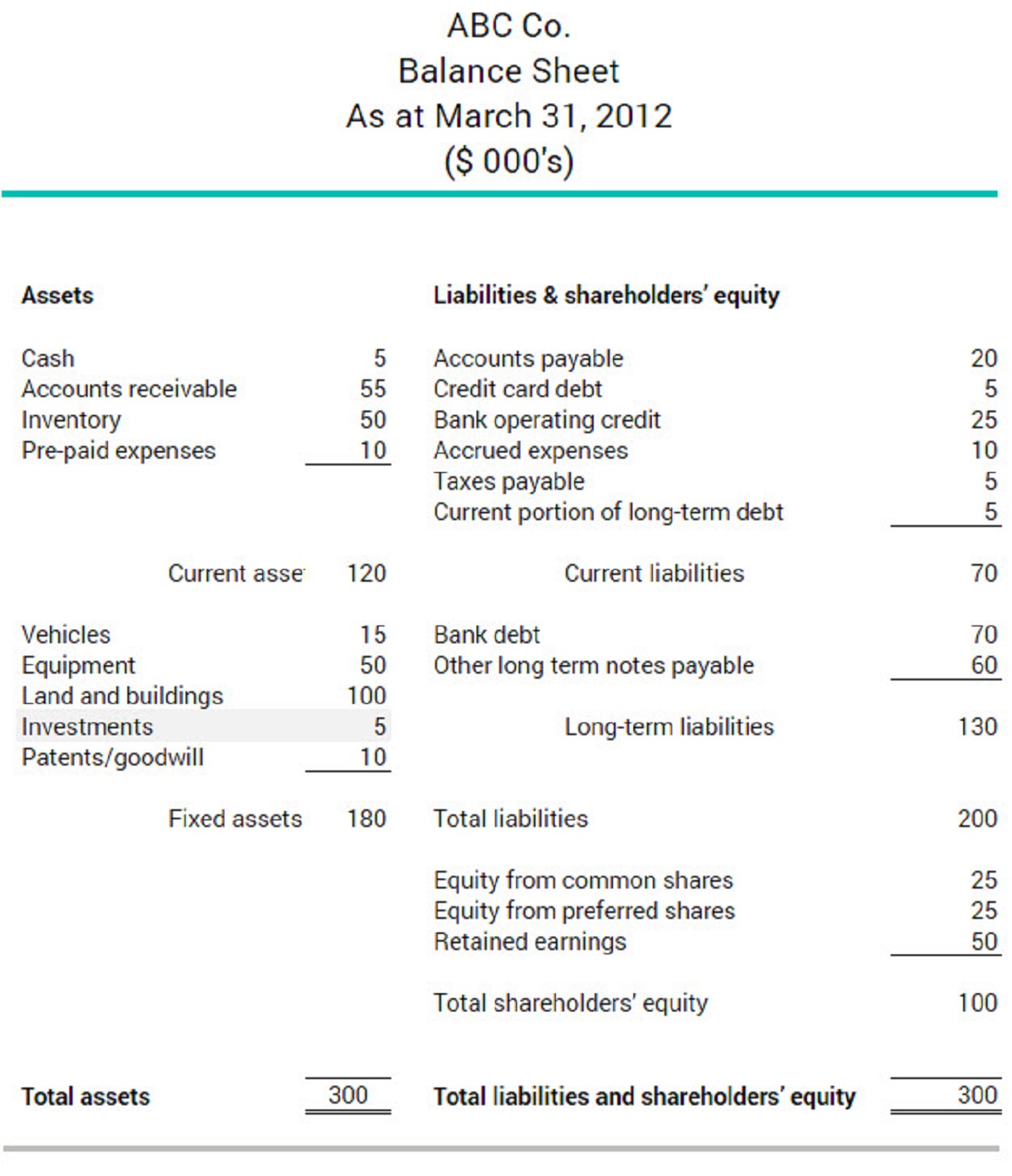

The presentation of investments on the balance sheet is crucial for accurately portraying a company’s financial position. Investments are reported as assets on the balance sheet and are categorized based on their classification, whether they are current or long-term investments.

Current Investments on the Balance Sheet:

Current investments, also known as short-term investments, are reported under the current assets section of the balance sheet. They are typically presented after cash and cash equivalents. Current investments are valued at their fair value, which represents the amount that can be received from selling the investment in an orderly transaction between market participants at the measurement date.

In the balance sheet, current investments are reported individually or grouped together under a single line item. The specific details of each investment, such as the type, quantity, and fair value, may be disclosed in the accompanying footnotes or in a separate schedule.

Long-term Investments on the Balance Sheet:

Long-term investments, on the other hand, are reported as non-current assets on the balance sheet. They represent investments that are held for a more extended period, usually exceeding one year. The balance sheet typically provides separate line items for long-term investments, allowing investors and stakeholders to differentiate them from current investments.

Similar to current investments, long-term investments are valued at their fair value or historical cost, depending on the accounting method used. The fair value of these investments may also be disclosed in the footnotes or a separate schedule to provide additional information to users of the financial statements.

It’s important to note that any changes in the fair value of investments are recorded in the income statement, either as realized gains or losses if the investments are sold, or as unrealized gains or losses if the investments are still held at the reporting date.

Disclosure of investments on the balance sheet includes providing relevant information about the nature, terms, and risks associated with the investments. This information helps users of the financial statements better understand the composition and valuation of the investment portfolio.

Furthermore, companies may be required to disclose additional information in the footnotes or in separate schedules, such as the maturity profile of investments, contractual terms, restrictions on sale or transferability, and any related-party transactions. These disclosures enhance the transparency of the company’s investment activities and provide insights into the potential risks and impacts on the financial statements.

In summary, investments are presented on the balance sheet as assets, with current investments categorized separately from long-term investments. The fair value or historical cost of investments is reported, with any changes in value disclosed in the income statement. Companies are also required to provide additional information and disclosures in the footnotes or separate schedules to enhance transparency. The presentation of investments on the balance sheet is vital for stakeholders to assess a company’s financial position and understand the composition and valuation of its investment portfolio.

Current Investments on the Balance Sheet

Current investments, also known as short-term investments, are an important component of the balance sheet as they reflect assets that are expected to be converted into cash within a year or the operating cycle of a business. These investments are highly liquid and are typically held to earn a quick return or to meet short-term funding needs.

On the balance sheet, current investments are listed under the current assets section, usually following cash and cash equivalents. They provide insights into a company’s available resources that can be easily converted into cash within a relatively short period.

Current investments are typically reported at their fair value, which represents the amount that can be received from selling the investment in an orderly transaction between market participants at the measurement date. Fair value provides a more accurate representation of the investment’s worth compared to historical cost.

In terms of presentation, current investments can be listed individually or aggregated under a single line item, depending on the level of detail desired by the company and the reporting standards followed. It is common to see current investments grouped together under a general category, such as “Marketable Securities”, to provide a clear and concise representation.

The balance sheet may also provide additional information about each current investment, such as the type, quantity, and fair value, in the accompanying footnotes or in a separate schedule. These disclosures offer transparency and allow users of the financial statements to gain a better understanding of the specific investments and their impact on the company’s financial position.

Additionally, the classification and subsequent presentation of current investments on the balance sheet help stakeholders assess the liquidity of a company. By distinguishing current investments from long-term assets, such as property or long-term investments, it becomes easier to evaluate a company’s short-term financial health and ability to meet its obligations.

It’s worth noting that any changes in the fair value of current investments are recorded in the income statement. These changes can be recognized as either realized gains or losses if the investments are sold, or as unrealized gains or losses if the investments are still held at the reporting date. This provides a clearer picture of the financial performance and investment activities of the company.

In summary, current investments are an integral part of the balance sheet and represent highly liquid assets that are expected to be converted into cash within a year or the operating cycle of a business. They are typically reported at their fair value and can be listed individually or grouped together under a general category. The presentation of current investments provides important insights into a company’s short-term liquidity and investment activities.

Long-term Investments on the Balance Sheet

Long-term investments are assets held for an extended period, typically exceeding one year, and provide a glimpse into a company’s commitment towards generating income or achieving capital appreciation over the long term. These investments are an essential component of the balance sheet and serve as indicators of a company’s long-term investment strategy.

On the balance sheet, long-term investments are classified as non-current assets, also known as long-term assets or investments. They appear after current assets, reflecting their nature as assets that are not expected to be readily converted into cash within the short term.

The presentation of long-term investments on the balance sheet provides stakeholders with a clear understanding of the company’s commitment of funds for future growth and income generation. These investments can include equity investments in other companies, debt securities, real estate investments, or ownership interests in other entities.

Long-term investments are typically presented separately from current investments to distinguish between the two categories. This separation helps users of financial statements differentiate assets that are intended for more immediate liquidity versus those designed to provide longer-term benefits.

Long-term investments are reported on the balance sheet at either fair value or historical cost, depending on the accounting method adopted by the company. Fair value reflects the current market value of the investment, providing a more accurate representation of its worth. On the other hand, historical cost represents the original purchase price of the investment.

Disclosures related to long-term investments may provide additional insights in the footnotes or a separate schedule. These disclosures can include details about the specific investments, such as the type, quantity, cost, fair value, and any restrictions or contingencies associated with the investments.

It’s important to note that any changes in the fair value of long-term investments are typically not recognized in the income statement unless they are deemed to be other-than-temporary impairments. These changes are instead reflected in the balance sheet as unrealized gains or losses, directly impacting the shareholder’s equity section of the financial statements.

The presentation of long-term investments on the balance sheet offers transparency to stakeholders, allowing them to assess the company’s capital allocation decisions and long-term growth strategies. It helps evaluate the company’s investment portfolio and potential risks associated with those investments.

In summary, long-term investments on the balance sheet represent assets held for an extended period, exceeding one year. They provide insights into a company’s long-term investment strategy, and their separate presentation distinguishes them from current investments. Long-term investments are reported at either fair value or historical cost and are subject to additional disclosures about the investments in the footnotes or separate schedules.

Accounting Methods for Investments

Accounting methods for investments play a crucial role in accurately recording and reporting the value of investments on a company’s financial statements. The accounting method chosen depends on various factors, including the level of influence and control the investor has over the investee company. Let’s explore some common accounting methods for investments:

Cost Method:

The cost method is generally used when the investor does not have significant influence over the investee company. Under this method, investments are initially recorded at cost, representing the amount paid to acquire the investment. Subsequently, the investment is reported on the balance sheet at the original cost, unless its value has been impaired.

Any income received from the investment is recorded as dividend income or interest income in the income statement. However, changes in the fair value of the investment are typically not recognized, unless impairment occurs.

Equity Method:

The equity method is used when the investor has significant influence, but not control, over the investee company’s financial and operating decisions. Under this method, the investor initially records the investment at cost. Then, the investor’s share of the investee’s earnings or losses is recognized in the income statement, increasing or decreasing the carrying value of the investment on the balance sheet.

Additionally, dividends received from the investee are considered a reduction of the investment’s carrying value unless the dividends represent a return of capital. In such cases, the dividends are recognized as income.

Fair Value Method:

The fair value method is used when the investor has control or significant influence over the investee and the investment is actively traded on a market. Under this method, investments are recorded on the balance sheet at their fair value, which represents the current market price or the price that can be obtained through an orderly transaction.

Any changes in the fair value of the investment are recognized in the income statement, impacting the net income and the carrying value of the investment on the balance sheet.

The choice of accounting method for investments depends on factors such as the level of control, influence, the nature of the investment, and applicable accounting standards. It is important for companies to carefully assess the nature of their investment and the relevant accounting guidelines when determining the appropriate method.

It’s worth noting that proper disclosure of the accounting method used for investments is important to ensure transparency in financial reporting. Investors and stakeholders rely on this information to understand how the value of the investment is determined and how it impacts the financial statements.

In summary, accounting methods for investments include the cost method, equity method, and fair value method. The cost method is used when the investor lacks significant influence, while the equity method is suitable for investments where significant influence exists. The fair value method is applied to investments actively traded on the market and provides transparency regarding the current market value. The choice of accounting method depends on various factors and should be disclosed to provide clear and accurate financial reporting.

Cost Method

The cost method is an accounting method used to record investments when the investor does not have significant influence over the investee company. It is typically applied when the investor owns less than 20% of the voting shares or has no ability to exercise control or influence over the investee’s financial and operating decisions.

Under the cost method, investments are initially recorded at cost, representing the amount paid to acquire the investment. This cost includes any transaction fees or other directly attributable costs. Subsequently, the investment is reported on the balance sheet at the original cost unless there is evidence of impairment, which is determined by assessing whether the carrying value of the investment has fallen below its recoverable amount.

The income received from the investment, such as dividends or interest, is recognized as dividend income or interest income in the income statement. It is reported separately from the revenue derived from the operating activities of the business. Dividends received reduce the carrying value of the investment on the balance sheet unless they represent a return of capital. In such cases, the dividends are recognized as income.

Changes in the fair value of the investment are generally not recognized in the financial statements unless there is evidence of impairment. However, it is important to monitor the investment’s market value to assess the need for an impairment test. If an impairment occurs, the carrying value of the investment is reduced to its recoverable amount, and the impairment loss is recognized in the income statement as an expense.

The cost method is commonly used for investments in small or non-publicly traded companies where the investor has little influence or control. It provides a straightforward and conservative approach to valuing investments on the balance sheet. However, it may not fully reflect the underlying value or market conditions associated with the investment.

Proper disclosure of investments accounted for using the cost method is necessary to provide transparency in financial reporting. The financial statements should disclose the nature and extent of the investments, including the cost of each investment and any information about the investee’s financial position and performance that is relevant to understanding the carrying value of the investment.

It’s important to understand that the choice of accounting method, such as the cost method, depends on the specific circumstances and applicable accounting standards. Companies should consider factors such as the level of control or influence, the nature of the investment, and the relevant accounting guidelines when determining the appropriate method for their investments.

In summary, the cost method is an accounting method used for investments when the investor lacks significant influence over the investee. Investments are initially recorded at cost and subsequently reported on the balance sheet at the original cost unless impaired. Dividend income is recognized separately, and changes in fair value are generally not recognized. Proper disclosure is important to ensure transparency in financial reporting.

Equity Method

The equity method is an accounting method used to record investments in situations where the investor has significant influence, but not control, over the investee company. It is generally applied when the investor owns between 20% and 50% of the voting shares of the investee.

Under the equity method, investments are initially recorded at cost and subsequently adjusted to reflect the investor’s share of the investee’s earnings or losses. The investor’s proportional share of the investee’s net income increases the carrying value of the investment on the balance sheet, while the share of net losses reduces the carrying value.

Dividends received from the investee are considered a return of the investor’s investment and are generally not recorded as income. However, if the dividends are deemed to represent a return on the initial investment, they are recognized as income and reduce the carrying value of the investment on the balance sheet. Any excess of dividends received over the investor’s share of the investee’s cumulative earnings is considered a return of capital and reduces the carrying value beyond the original cost.

The investor’s share of the investee’s earnings or losses is recognized in the income statement under the equity method. This income or loss is typically reported as a separate line item, distinct from the ordinary operating income or loss of the investor. The investor’s share of the investee’s earnings is reported as revenue, whereas the share of net losses is recognized as an expense.

It is essential for the investor to closely monitor the investee’s financial position and performance to determine the appropriate adjustments under the equity method. If the investor’s influence decreases to the point where significant influence no longer exists, the equity method is discontinued, and the investment is subsequently accounted for using the cost or fair value method, depending on the circumstances.

Proper disclosure of investments accounted for using the equity method is important to ensure transparency in financial reporting. The financial statements should disclose the nature and extent of the investments, including the investor’s percentage ownership, the investee’s financial position and performance, and any significant transactions or events that impact the carrying value of the investment.

In summary, the equity method is an accounting method used when the investor has significant influence, but not control, over the investee. Investments are initially recorded at cost and subsequently adjusted based on the investor’s share of the investee’s earnings or losses. Dividends received and excess of dividends over the share of earnings can impact the carrying value. The investor’s share of earnings or losses is recognized as revenue or expense in the income statement. Proper disclosure is important for transparent financial reporting.

Fair Value Method

The fair value method is an accounting method used to record investments when the investor has control or significant influence over the investee, and the investment is actively traded on the market. Under the fair value method, investments are initially recorded at fair value, which represents the current market price or the price that can be obtained through an orderly transaction between market participants.

With the fair value method, the investment is subsequently reported on the balance sheet at its fair value, which is updated at each reporting period. Any changes in the fair value of the investment are recognized in the income statement, impacting the net income and the carrying value of the investment on the balance sheet.

Determining the fair value of an investment requires considering market prices, observable inputs, or other relevant valuation techniques. This method provides a more accurate representation of the investment’s worth based on current market conditions, as opposed to historical cost or other accounting methods.

Dividend income and interest income earned from investments accounted for using the fair value method are recognized as income in the income statement and reported separately from the ordinary operating income of the investor. Any gains or losses resulting from changes in the fair value of the investment are reported as separate line items in the income statement.

Proper disclosure of investments accounted for using the fair value method is important to ensure transparency in financial reporting. The financial statements should disclose significant information about the investments, including details about their nature, valuation techniques used, and any restrictions or contingencies associated with the investments.

It’s important to note that the fair value method is typically used for investments that are actively traded on the market. For investments that do not have quoted market prices, or for which the fair value cannot be reliably determined, alternative accounting methods such as the cost method or equity method may be employed.

In summary, the fair value method is an accounting method used when the investor has control or significant influence over the investee, and the investment is actively traded on the market. Investments are valued at their fair value, which is updated at each reporting period. Changes in fair value affect the net income and the carrying value of the investment on the balance sheet. Proper disclosure of these investments is important for transparent financial reporting.

Disclosure Requirements for Investments

Disclosure requirements for investments are necessary to provide transparency and ensure that users of financial statements have relevant and reliable information about a company’s investment activities. These requirements aim to provide a clear understanding of the nature, risks, and financial impact of investments. Let’s explore some common disclosure requirements for investments:

Nature and Types of Investments:

Companies are required to disclose the nature and types of investments held, including details such as equity investments, debt investments, real estate properties, or ownership interests in other entities. This disclosure helps users of financial statements understand the range and composition of a company’s investment portfolio.

Valuation Methods and Fair Value:

Disclosure of the valuation methods used to determine the fair value of investments is essential. Companies should provide relevant information about the inputs and techniques employed in valuing investments, whether through quoted market prices, observable inputs, or other relevant valuation methods. This disclosure helps stakeholders assess the reliability and accuracy of the fair value measurement.

Significant Risks and Concentration:

Companies are required to disclose any significant risks associated with their investments. This includes risks related to market conditions, industry-specific factors, or specific investee companies. Additionally, if there are concentration risks whereby a significant portion of the investment portfolio is held in a few investments, this should be disclosed to highlight the potential impact on the company’s financial position.

Restrictions and Contingencies:

Companies should disclose any significant restrictions or contingencies associated with their investments. This includes contractual limitations on the ability to sell or transfer the investments, legal or regulatory restrictions, or the existence of any contingent liabilities or obligations that may impact the value or future cash flows of the investments.

Related-Party Transactions:

Disclosure of any investments involving related parties, such as affiliates, subsidiaries, or key management personnel, is necessary to avoid any conflicts of interest or potential abuse of related-party transactions. Complete and transparent information should be provided about investments made with related parties, including the terms, conditions, and pricing of such transactions.

Impairment and Fair Value Changes:

Companies should disclose any impairments of investments, whether recognized through the income statement or directly impacting the carrying value of the investments on the balance sheet. Additionally, any gains or losses resulting from changes in the fair value of investments should be disclosed, including the impact on the income statement and any related tax effects.

These are just a few examples of the disclosure requirements for investments. The specific requirements may vary based on applicable accounting standards, regulatory guidelines, and the nature of the investments held by the company. The purpose of these disclosures is to ensure that users of financial statements have a comprehensive understanding of a company’s investment activities and the associated risks and impacts on its financial position and performance.

In summary, disclosure requirements for investments include providing information about the nature and types of investments held, the valuation methods and fair value determination, significant risks and concentration, restrictions or contingencies, related-party transactions, and impairments or changes in fair value. These disclosures are essential for transparent financial reporting and to assist stakeholders in evaluating the impact and risks related to a company’s investment activities.

Summary

Investments are integral to the financial landscape, providing opportunities for growth, income generation, and diversification. Understanding the classification, presentation, and accounting methods for investments is crucial for accurate financial reporting and analysis.

Investments can be classified as current or long-term, depending on their expected conversion into cash. Current investments are highly liquid and typically include marketable securities, such as Treasury bills, commercial paper, and money market funds. Long-term investments, on the other hand, have a longer holding period and may consist of equity investments, debt securities, real estate properties, or ownership stakes in other entities.

The presentation of investments on the balance sheet is essential for stakeholders to assess a company’s financial position. Current investments appear in the current assets section, reported at their fair value, while long-term investments are presented as non-current assets. The accounting methods for investments include the cost method, equity method, and fair value method, each used based on the level of control, influence, and market tradability.

The disclosure requirements for investments ensure transparency in financial reporting. Companies are required to disclose the nature, types, and valuation methods of their investments. Additionally, they must disclose significant risks, concentration, restrictions, contingencies, related-party transactions, impairments, and changes in fair value. These disclosures provide users of financial statements with comprehensive information to assess the composition, risks, and impact of investments on a company’s financial position and performance.

In summary, investments play a vital role in financial management, offering opportunities for growth and diversification. Understanding the classification, presentation, accounting methods, and disclosure requirements for investments is key to providing accurate and transparent financial information. By adhering to these standards, companies can better communicate their investment activities and their implications for the overall financial health of the organization.

Conclusion

Investments are an essential aspect of financial management, providing opportunities for growth, income generation, and diversification. Classifying, presenting, and accounting for investments accurately are crucial for transparent financial reporting and informed decision-making.

Throughout this article, we have explored the different types of investments, such as equity investments and debt investments, as well as other investment categories like real estate and commodities. We discussed how investments are presented on the balance sheet based on their classification as current or long-term and the corresponding accounting methods used, including the cost method, equity method, and fair value method.

Disclosure requirements for investments ensure transparency, allowing stakeholders to obtain relevant and reliable information. These requirements encompass the nature and types of investments, valuation methods, risks and concentrations, restrictions and contingencies, related-party transactions, and impairments or changes in fair value. Compliance with these disclosure requirements is essential to provide a comprehensive understanding of a company’s investment activities.

In conclusion, investments play a significant role in financial management and can have a substantial impact on a company’s financial position and performance. Understanding the different types of investments, their classification, presentation on the balance sheet, accounting methods, and disclosure requirements is fundamental for accurate financial reporting and effective decision-making. By adhering to these principles, companies can communicate their investment strategies, risks, and potential returns, providing stakeholders with the necessary information to evaluate their financial health and make informed investment decisions.