Introduction

Welcome to our article on the effects of investments by stockholders on the accounting equation. As businesses grow and seek additional funding to support their operations or expansion plans, stockholders play a crucial role by providing financial resources. These investments have a direct impact on a company’s financial position and influence the accounting equation, which is a fundamental concept in financial accounting.

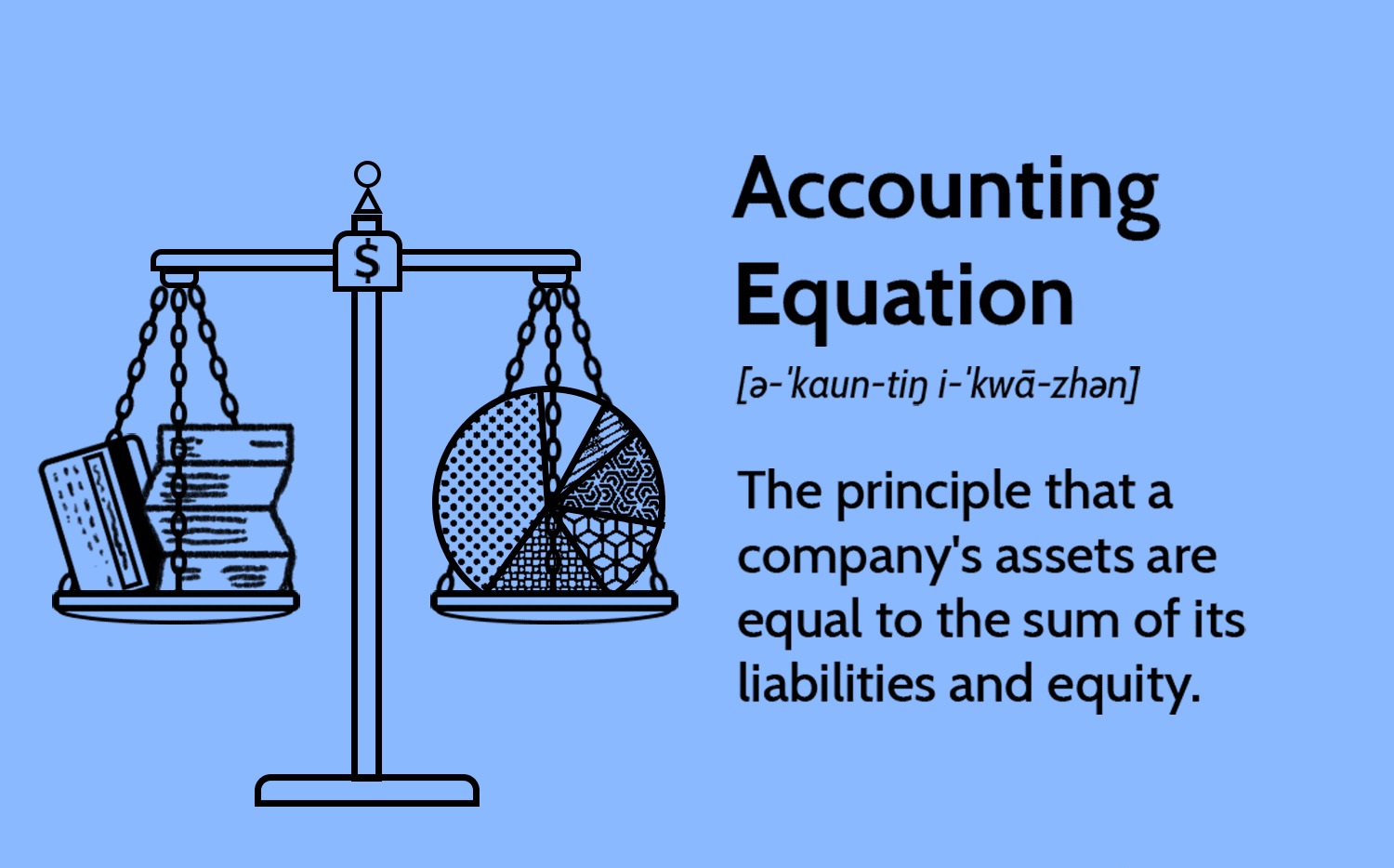

The accounting equation, also known as the balance sheet equation, states that the assets of a company are equal to the sum of its liabilities and stockholders’ equity. It serves as the foundation for recording and reporting a company’s financial transactions and determining its overall financial health.

Investments by stockholders refer to the infusion of capital into a company by individuals or entities in exchange for ownership shares, which entitle them to a portion of the company’s profits and assets. This influx of funds can come in various forms, such as cash, equipment, property, or services, and has specific implications for the components of the accounting equation.

In this article, we will explore the different types of stockholders’ investments, delve into the effects they have on the various elements of the accounting equation, and provide examples to illustrate these concepts. By understanding how investments by stockholders impact the accounting equation, individuals and businesses can gain valuable insights into the financial implications of these transactions.

The Accounting Equation

The accounting equation, also known as the balance sheet equation, is a fundamental principle in financial accounting that represents the relationship between a company’s assets, liabilities, and stockholders’ equity. It serves as the basis for recording and reporting a company’s financial transactions and determining its financial position.

The equation is expressed as follows: Assets = Liabilities + Stockholders’ Equity. It states that the assets owned by a company are always equal to the sum of its liabilities and stockholders’ equity.

Assets refer to the economic resources owned or controlled by a company, which can include cash, property, equipment, inventory, investments, and more. Liabilities, on the other hand, represent the company’s debts or obligations to external parties, such as loans, accounts payable, and accrued expenses.

Stockholders’ equity, also known as shareholders’ equity, represents the residual interest in the company’s assets after deducting liabilities. It is the ownership stake held by the stockholders, and it includes the initial investment made by stockholders and retained earnings generated from the company’s profits.

The accounting equation provides a snapshot of a company’s financial health at a specific point in time. Any changes to the elements of the equation, such as investments by stockholders, affect the company’s overall financial position.

By understanding the accounting equation, investors, creditors, and other stakeholders can assess a company’s financial performance and evaluate its ability to meet its obligations. It also serves as a foundation for preparing financial statements, such as the balance sheet, income statement, and cash flow statement, which provide valuable insights into a company’s financial activities.

In the following sections, we will explore the effects of investments by stockholders on the components of the accounting equation and examine how these transactions impact a company’s financial position.

Investments by Stockholders

Investments by stockholders refer to the contributions made by individuals or entities in exchange for ownership shares in a company. These investments are a crucial source of capital for businesses, as they provide the financial resources needed to support operations, fund expansion plans, and pursue growth opportunities.

Stockholders’ investments can take various forms, including cash, property, equipment, services, or intellectual property. When stockholders make investments, they become shareholders and have a proportional claim on the company’s assets and earnings.

There are two main types of stockholders’ investments: equity investments and debt investments. Equity investments involve the purchase of shares or ownership stakes in a company, while debt investments involve lending money to the company in the form of bonds, notes, or other types of debt instruments.

Equity investments provide capital to the company without creating a liability. The invested amount is added to the company’s stockholders’ equity, increasing the owners’ interests in the company’s assets and earnings. These investments can be made during the company’s initial public offering (IPO), private placements, or subsequent capital raises.

On the other hand, debt investments create a liability for the company. When stockholders lend money to the company, either directly or through the purchase of bonds or other debt securities, the company incurs a debt obligation. The borrowed funds are recorded as a liability on the company’s balance sheet and represent an obligation to repay the stockholders at a future date, typically with interest.

Both equity and debt investments have an impact on a company’s financial position and the components of the accounting equation. Equity investments increase the company’s assets and stockholders’ equity, while debt investments increase liabilities and may also impact stockholders’ equity through interest expense and potential changes in the value of the debt.

Overall, investments by stockholders play a vital role in the financial structure and growth of a company. They provide the necessary funds to support business activities and can have a significant impact on a company’s financial position and performance.

Types of Stockholders’ Investments

Stockholders’ investments can take different forms, depending on the terms and conditions agreed upon between the stockholders and the company. These investments can vary in their characteristics and implications for a company’s financial position. Let’s explore some of the common types of stockholders’ investments:

- Cash Contributions: This is the most common type of stockholders’ investment, where individuals or entities provide cash in exchange for ownership shares. Cash contributions increase the company’s cash assets, as well as its stockholders’ equity.

- Property and Equipment: Stockholders can also contribute property or equipment to a company instead of cash. These non-cash assets are valued at their fair market value when determining the impact on the accounting equation. The company’s assets increase, and stockholders’ equity reflects the value of the contributed assets.

- Services: In some cases, stockholders may provide services to the company instead of cash or other assets. The value of these services is recorded as an intangible asset, and the company’s stockholders’ equity increases to reflect the fair value of the services rendered.

- Convertible Securities: Stockholders may also invest in convertible securities, such as convertible bonds or preferred shares. These securities can be converted into common shares at a predetermined price and time. The initial investment is recorded as a liability or equity, depending on the terms of the convertible security.

- Stock Options and Warrants: Stock options and warrants give stockholders the right to purchase shares at a predetermined price within a specified period. These investments can have a dilutive effect on existing stockholders’ equity if the options or warrants are exercised.

These are just a few examples of the types of stockholders’ investments that can occur. The specific terms and conditions of each investment are typically outlined in agreements between the stockholders and the company, such as subscription agreements, purchase agreements, or convertible security contracts.

It is important for companies to carefully evaluate and disclose the terms of stockholders’ investments in their financial statements to provide transparency to stakeholders. Additionally, businesses should ensure compliance with regulatory requirements and accounting standards when accounting for these investments.

Understanding the different types of stockholders’ investments allows companies and investors to assess the potential impact on the company’s financial position and the rights and benefits conferred to stockholders through these investments.

Effect on Assets

Investments by stockholders have a direct impact on a company’s assets – the economic resources owned or controlled by the business. The specific effect on assets depends on the type and nature of the stockholders’ investments. Let’s examine the typical effects:

1. Cash Contributions: When stockholders make cash contributions, the company’s cash assets increase. Cash is considered a current asset and is recorded at the amount received from the stockholders.

2. Non-cash Contributions: If stockholders contribute non-cash assets, such as property or equipment, the company’s non-cash assets increase. These assets are recorded at their fair market value on the date of the contribution.

3. Services Contributions: Contributions in the form of services can also impact assets. The value of the services rendered by stockholders is recorded as an intangible asset, such as goodwill or intellectual property, if it can be reliably measured and meets the recognition criteria.

4. Convertible Securities: If stockholders invest through convertible securities, such as convertible bonds, the initial investment is initially recorded as a liability, not as an asset. However, when the securities are converted into common shares, the company’s assets increase due to the increase in stockholders’ equity.

5. Stock Options and Warrants: Stock options and warrants don’t have an immediate impact on assets. However, if these options or warrants are exercised, the company may issue additional shares, resulting in an increase in cash or other assets, depending on the terms of the agreement.

The investment of capital by stockholders increases a company’s total assets, whether through an increase in cash or the acquisition of non-cash assets. This infusion of funds strengthens the company’s financial position and provides additional resources to support its operations, investment in new projects, or repayment of liabilities.

It is crucial for companies to accurately record and appropriately classify stockholders’ investments in their accounting records and financial statements. This ensures the transparency and reliability of financial information for decision-making purposes by company management, investors, and other stakeholders.

Next, let’s explore the effect of stockholders’ investments on a company’s liabilities.

Effect on Liabilities

Investments by stockholders can also have an impact on a company’s liabilities – the obligations or debts owed by the business. The effect on liabilities depends on the type of stockholders’ investments and the terms agreed upon. Let’s explore the typical effects:

1. Cash Contributions: When stockholders make cash contributions, it does not directly affect liabilities. The funds received are recorded as an increase in stockholders’ equity rather than creating a new liability for the company.

2. Debt Investments: If stockholders provide funds to the company through debt investments, such as loans, bonds, or other debt instruments, it increases the company’s liabilities. The borrowed funds represent an obligation to repay the stockholders at a future date, typically with interest. The amount of the debt investment is recorded as a liability on the company’s balance sheet.

It’s important to note that the impact of debt investments on liabilities may vary depending on the terms of the investment. For example, if the debt investment is convertible into equity, it may be initially classified as a liability until conversion occurs.

3. Convertible Securities: Stockholders’ investments in convertible securities, such as convertible bonds or preferred shares, initially create a liability for the company. However, when the securities are converted into common shares, the liability decreases, and stockholders’ equity increases.

4. Stock Options and Warrants: Stock options and warrants do not directly impact liabilities. These instruments give stockholders the right to purchase shares at a predetermined price within a specified period. The related obligations arise only if the stockholders exercise their options or warrants.

In summary, investments by stockholders can have varying effects on a company’s liabilities. Cash contributions typically do not affect liabilities directly, while debt investments and convertible securities increase the company’s obligations. Conversely, when convertible securities are converted, a liability is reduced, and stockholders’ equity increases.

Accurate accounting and disclosure of stockholders’ investments in liabilities are essential to provide transparency and reliability in financial reporting. Understanding the impact on liabilities allows stakeholders to assess a company’s debt obligations and evaluate its ability to meet its financial commitments.

Now, let’s explore how investments by stockholders affect stockholders’ equity, a critical component of the accounting equation.

Effect on Stockholders’ Equity

Investments by stockholders have a significant impact on a company’s stockholders’ equity – the residual interest in the company’s assets after deducting liabilities. The effect on stockholders’ equity depends on the type and terms of the stockholders’ investments. Let’s explore the typical effects:

1. Cash Contributions: When stockholders make cash contributions, it directly increases stockholders’ equity. The contributed amount is recorded as additional paid-in capital, which represents the excess of the total cash contributed by stockholders over the par value or stated value of the shares issued.

2. Non-cash Contributions: Non-cash contributions, such as property, equipment, or services, also impact stockholders’ equity. The fair market value of the contributed assets or services is recorded as an increase in stockholders’ equity.

3. Debt Investments: Debt investments, such as loans or bonds made by stockholders, do not directly impact stockholders’ equity. The borrowed funds create a liability for the company but do not affect the stockholders’ equity until the interest or principal repayments have an impact on retained earnings or common stock.

4. Convertible Securities: Stockholders’ investments in convertible securities initially increase both liabilities and stockholders’ equity. When the convertible securities are converted into common shares, the liability is reduced, and stockholders’ equity increases proportionally.

5. Stock Options and Warrants: Stock options and warrants do not have an immediate impact on stockholders’ equity. However, if these options or warrants are exercised, additional shares are issued, which can dilute existing stockholders’ equity.

Investments by stockholders directly contribute to stockholders’ equity by increasing the capital contributed to the company. The resulting increase in stockholders’ equity represents the ownership interest and residual claim on the company’s assets after deducting liabilities.

Accurate recording and reporting of stockholders’ investments in the stockholders’ equity section of the balance sheet are crucial for transparency and compliance with accounting standards. This allows stakeholders to assess the financial health of the company and understand the ownership structure and the value available to stockholders.

Next, let’s examine the overall impact of stockholders’ investments on the accounting equation, which ties together the effects on assets, liabilities, and stockholders’ equity.

Effect on the Accounting Equation

Investments by stockholders have a direct impact on the accounting equation, which represents the relationship between a company’s assets, liabilities, and stockholders’ equity. Understanding the effects on each component helps provide a comprehensive view of a company’s financial position. Let’s explore how stockholders’ investments impact the accounting equation:

The accounting equation is expressed as: Assets = Liabilities + Stockholders’ Equity. Any changes in assets, liabilities, or stockholders’ equity will affect the equality of the equation.

Effect on Assets: Stockholders’ investments typically increase a company’s assets. Cash contributions directly increase the cash asset, while non-cash contributions, such as property or equipment, increase the non-cash assets. The value of services rendered by stockholders might increase intangible assets. These changes demonstrate how stockholders’ investments positively impact the asset side of the equation.

Effect on Liabilities: Stockholders’ investments can also impact a company’s liabilities. Debt investments create an increase in liabilities as the company incurs a debt obligation to the stockholders. Convertible securities initially increase liabilities, but when converted into equity, they reduce liabilities. It’s important to note that cash contributions, on their own, do not directly affect liabilities.

Effect on Stockholders’ Equity: Stockholders’ investments directly impact the stockholders’ equity component of the accounting equation. Cash contributions increase stockholders’ equity through additional paid-in capital. Non-cash contributions increase stockholders’ equity by recognizing the fair value of the contributed assets or services. Convertible securities, when converted into equity, increase stockholders’ equity. However, stock options and warrants do not have an immediate impact on stockholders’ equity until they are exercised.

By examining the effects on assets, liabilities, and stockholders’ equity, we can see how stockholders’ investments impact the accounting equation. The investments contribute to the overall financial position of the company, increasing its assets and potentially affecting the liabilities and stockholders’ equity proportionally.

Accurate and proper recording of stockholders’ investments is essential to maintain the balance in the accounting equation. This ensures the integrity and reliability of financial statements and provides stakeholders with a clear understanding of the company’s financial position and performance.

Now, let’s illustrate the application of these concepts through examples of stockholders’ investments and their effect on the accounting equation.

Examples

To further understand the effects of stockholders’ investments on the accounting equation, let’s consider a few examples:

Example 1:

Company ABC is a startup that receives a cash investment of $100,000 from a group of stockholders in exchange for ownership shares. The effects on the accounting equation would be:

- Assets: Cash increases by $100,000.

- Liabilities: No change since it was a cash contribution.

- Stockholders’ Equity: Additional paid-in capital increases by $100,000, resulting in an increase in stockholders’ equity.

Example 2:

Company XYZ receives a property contribution valued at $50,000 from a stockholder as their investment. The effects on the accounting equation would be:

- Assets: Non-cash assets increase by $50,000 to reflect the fair market value of the property.

- Liabilities: No change since it was a non-cash contribution.

- Stockholders’ Equity: Additional paid-in capital increases by $50,000, resulting in an increase in stockholders’ equity.

Example 3:

Company DEF issues convertible bonds worth $500,000 to stockholders. The bonds can be converted into common shares of the company at a predetermined price within a specified period. The effects on the accounting equation would be:

- Assets: No immediate impact on assets.

- Liabilities: The company records a liability of $500,000 for the convertible bonds.

- Stockholders’ Equity: At issuance, there is an increase in stockholders’ equity, as additional paid-in capital and the liability for the convertible bonds are both recognized in the equity section. When the bonds are converted, the liability decreases, and common stock increases by the converted amount, maintaining the balance in the accounting equation.

These examples highlight the practical application of stockholders’ investments on the accounting equation. Each investment type has unique effects on assets, liabilities, and stockholders’ equity, showcasing the importance of accurately recording and reporting these transactions in financial statements.

It is crucial for companies to consolidate all stockholders’ investments and track the corresponding changes in assets, liabilities, and stockholders’ equity. This ensures the equation remains balanced and provides stakeholders with an accurate representation of the company’s financial position.

Now that we have explored examples of the effects of stockholders’ investments, let’s summarize the key concepts discussed in this article.

Conclusion

Investments by stockholders play a significant role in a company’s financial structure and overall performance. Understanding the effects of these investments on the accounting equation is crucial for accurately assessing a company’s financial position and making informed business decisions.

The accounting equation, which states that assets equal liabilities plus stockholders’ equity, serves as the foundation for recording and reporting a company’s financial transactions. Stockholders’ investments, whether in the form of cash, non-cash contributions, debt investments, or convertible securities, directly impact the components of the equation.

Cash contributions increase the company’s cash assets and stockholders’ equity, while non-cash contributions contribute to non-cash assets and stockholders’ equity. Debt investments increase liabilities, and when convertible securities are converted into equity, the liabilities decrease, and stockholders’ equity increases. Stock options and warrants do not have an immediate impact on the accounting equation until they are exercised.

Accurate and transparent accounting of stockholders’ investments ensures the integrity of financial statements and provides stakeholders with a clear understanding of a company’s financial health. It is essential for companies to properly record and report these investments, classifying them in the appropriate sections of the balance sheet and disclosing the terms and conditions in the notes to the financial statements.

By comprehending the effects of stockholders’ investments on the accounting equation, individuals and businesses can better evaluate a company’s financial position, assess its ability to meet financial obligations, and make informed investment decisions.

In conclusion, investments by stockholders have a profound impact on a company’s financial structure, influencing the assets, liabilities, and stockholders’ equity components of the accounting equation. Understanding these effects allows for a holistic view of a company’s financial position and aids in effective financial management.