Introduction

Fixed income investments are a popular form of investment that allow individuals to earn a regular stream of income. They are considered a relatively low-risk investment option compared to stocks and other more volatile asset classes. Fixed income investments are widely sought after by conservative investors who prioritize stability and consistent income over potential high returns.

Fixed income investments come in various forms, such as bonds, certificates of deposit (CDs), treasury bills, and preferred stocks. These investments pay investors a fixed amount of interest over a specific period of time, hence the term “fixed income”. This predictable income stream makes fixed income investments an attractive option for those looking for a reliable source of cash flow.

The primary aim of fixed income investments is to preserve capital while generating a steady income. Unlike the stock market, where the value of investments can rise or fall dramatically, fixed income investments provide a level of certainty and stability. This appealing trait makes these investments suitable for both individual investors and institutional investors who seek to balance their portfolio and mitigate risk.

In this article, we will delve deeper into the world of fixed income investments. We will explore how these investments work, the different types available, and the benefits and risks associated with investing in them. Additionally, we will discuss the key factors to consider when investing in fixed income securities and provide insights into how one can start investing in them.

What is a fixed income investment?

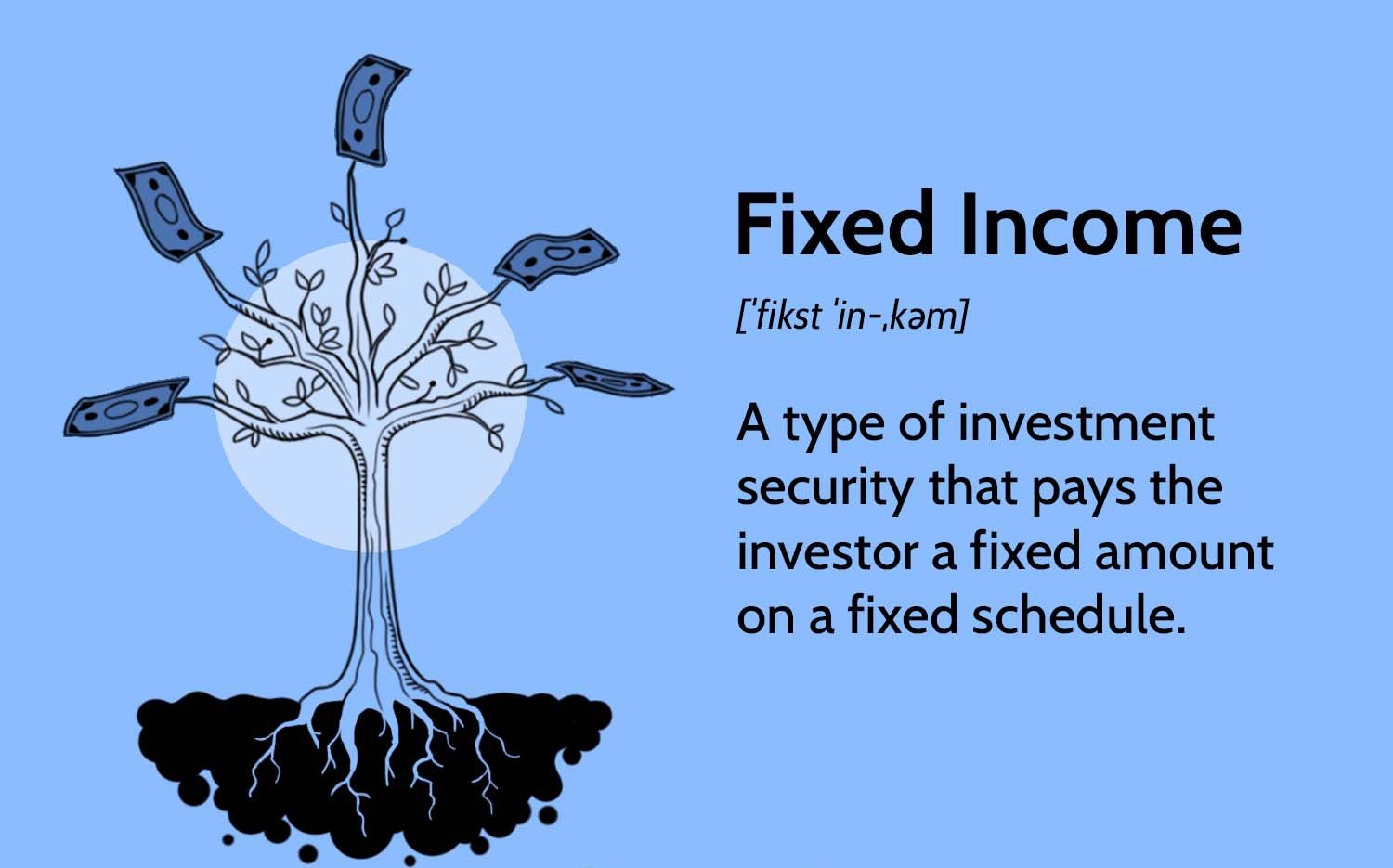

A fixed income investment, also known as a fixed interest investment, is a financial instrument that offers a fixed rate of return over a specified period of time. It is an investment vehicle where an investor lends money to a borrower, typically a government or corporation, in exchange for regular interest payments and the return of the principal amount at maturity.

The main characteristic of fixed income investments is their predictability in terms of cash flow. Unlike stocks, where the returns can be volatile and uncertain, fixed income investments provide a set stream of income. This income can be in the form of regular interest payments or coupon payments on bonds, or dividends on preferred stocks.

Fixed income investments are often considered less risky than equities because they have a fixed maturity date and predetermined interest or dividend payments. This makes them an attractive option for conservative investors, retirees, and those seeking a reliable source of income.

Bonds are the most common type of fixed income investment. A bond is essentially a loan made by an investor to a government or corporation. The borrower, or issuer, promises to repay the principal amount of the bond at maturity and pay periodic interest payments to the bondholder.

Other forms of fixed income investments include certificates of deposit (CDs), treasury bills, and preferred stocks. Each of these investment options has its own unique set of features and benefits. CDs, for instance, are time deposits offered by banks with a fixed interest rate and maturity date. Treasury bills are short-term government securities with maturities of one year or less, while preferred stocks represent ownership in a company and provide fixed dividends.

Overall, fixed income investments play a crucial role in diversifying investment portfolios and managing risk. They offer stability, reliable income, and a relatively lower level of volatility compared to other investment classes. Whether you are a conservative investor or someone looking for a reliable income stream, fixed income investments can be a valuable addition to your investment strategy.

How do fixed income investments work?

Fixed income investments work by investors lending money to an issuer, such as a government or corporation, in exchange for regular interest payments and the return of the principal amount at maturity. The issuer uses the funds raised from investors to finance projects or operations, and in return, promises to make timely interest payments and repay the principal amount.

When investing in fixed income securities like bonds, investors essentially become creditors to the issuer. The issuer sets a fixed interest rate, also known as the coupon rate, which determines the amount of interest the investor will receive over the life of the investment. The interest payments, typically made semi-annually or annually, provide a reliable source of income to the investor.

At the maturity date, the issuer repays the principal amount to the investor. This return of the principal amount is one of the key features that differentiate fixed income investments from other types of investments, such as stocks, where there is no obligation to repay the initial investment.

The pricing of fixed income investments is influenced by various factors, including the prevailing interest rates, creditworthiness of the issuer, and time to maturity. When interest rates rise, the market value of existing fixed income investments may decline since newly issued bonds tend to offer higher yields. Conversely, when interest rates fall, the market value of fixed income investments may increase as the fixed interest rate becomes more attractive to investors.

It is essential to assess the creditworthiness of the issuer before investing in fixed income securities. Credit ratings provided by independent rating agencies, such as Moody’s or Standard & Poor’s, give an indication of the issuer’s ability to meet its financial obligations. Higher-rated issuers are considered less risky and may offer lower interest rates, while lower-rated issuers may offer higher yields to compensate for the higher risk.

Investors can manage their exposure to various fixed income investments through diversification. By investing in a range of different issuers, industries, and maturities, investors can spread their risk and potentially increase their overall return. Bond mutual funds and exchange-traded funds (ETFs) offer convenient ways to gain exposure to a diversified portfolio of fixed income securities.

Overall, fixed income investments provide investors with a steady stream of income and the return of the principal amount at maturity. They work by investors lending money to issuers and receiving fixed interest payments in return. Understanding the dynamics of fixed income investments, including creditworthiness, interest rate movements, and diversification, is crucial for making informed investment decisions.

Types of fixed income investments

Fixed income investments come in various forms, each with its own unique characteristics and features. Here are some of the most common types of fixed income investments:

- Bonds: Bonds are debt securities issued by governments, municipalities, or corporations to raise capital. They pay regular interest payments, called coupon payments, to investors over a specified period of time until the bond reaches maturity. Government bonds, corporate bonds, municipal bonds, and treasury bonds are all examples of bonds.

- Certificates of Deposit (CDs): CDs are time deposits offered by banks and credit unions. They have fixed interest rates and maturity dates, typically ranging from a few months to several years. CDs are considered low-risk investments since they are insured by the Federal Deposit Insurance Corporation (FDIC) up to certain limits.

- Treasury Bills (T-bills): T-bills are short-term government securities issued by the U.S. Treasury. They have maturities of one year or less and are considered one of the safest investments available. T-bills are sold at a discount to their face value and do not pay regular interest payments. Instead, investors earn a return by receiving the full face value at maturity.

- Preferred Stocks: Preferred stocks are a type of equity investment that combines characteristics of both stocks and bonds. Preferred stockholders receive fixed dividend payments, similar to coupon payments on bonds, before common stockholders receive any dividends. Preferred stocks typically have a higher yield than bonds but also come with higher risk.

- Mortgage-backed Securities (MBS): MBS are securities backed by a pool of mortgages. Investors in MBS receive regular interest payments generated from the mortgage payments made by borrowers. These investments are backed by real estate, but their value can fluctuate based on changes in interest rates and the performance of the housing market.

- Corporate Notes: Corporate notes are debt securities issued by corporations with maturities ranging from a few weeks to several years. They are similar to bonds but typically have shorter terms and are issued in smaller denominations. Corporate notes can be a suitable option for those seeking fixed income investments with relatively higher yields.

Each type of fixed income investment has its own risk and return profile. Bonds and treasury securities are considered low-risk investments, while investments in preferred stocks and mortgage-backed securities carry higher levels of risk. It is important for investors to conduct thorough research and consider their risk tolerance and investment goals before choosing a specific type of fixed income investment.

Investors can also diversify their fixed income investments by combining various types of securities. This diversification helps to spread the risk and potentially improve the overall return of the investment portfolio.

Benefits of investing in fixed income

Investing in fixed income offers several benefits to investors. Here are some key advantages of adding fixed income securities to your investment portfolio:

- Steady stream of income: One of the primary benefits of investing in fixed income is the consistent stream of income it provides. Fixed income investments, such as bonds and preferred stocks, offer regular interest payments or dividends that can serve as a reliable source of cash flow. This income can be particularly beneficial for retirees or those seeking supplemental income.

- Lower volatility: Fixed income investments tend to have lower volatility compared to stocks and other high-risk investments. They are generally considered less volatile because they offer predictable income and the return of the principal amount at maturity. This stability can help reduce the overall risk in an investment portfolio and provide a level of comfort to risk-averse investors.

- Diversification: Fixed income investments provide an opportunity for portfolio diversification. By adding fixed income securities to a portfolio that also includes equities, real estate, and other assets, investors can spread their risk across different investment categories. This diversification can help cushion the impact of market fluctuations and contribute to overall portfolio stability.

- Capital preservation: Another key benefit of fixed income investments is the preservation of capital. Unlike stocks, where the value can fluctuate significantly, fixed income securities provide a level of assurance that the principal amount will be returned at maturity. This makes them an attractive option for conservative investors who prioritize the safety of their investment.

- Choice of investment options: Fixed income investments offer a wide range of investment options to suit different investor preferences. From government bonds to corporate notes and preferred stocks, there are various types of fixed income securities to choose from. This flexibility allows investors to tailor their fixed income investments to their risk tolerance, income needs, and investment objectives.

- Inflation protection: Some fixed income investments, such as Treasury Inflation-Protected Securities (TIPS), provide protection against inflation. TIPS adjust their principal value based on changes in the Consumer Price Index (CPI), which helps preserve purchasing power. This inflation protection feature can be especially valuable during periods of rising inflation.

While fixed income investments offer many benefits, it is important to note that they are not without risks. Interest rate risk, default risk, and liquidity risk are some of the potential risks associated with investing in fixed income securities. It is crucial for investors to carefully assess the risk-return profile of these investments and diversify their portfolio to manage risk effectively.

Overall, investing in fixed income offers stability, regular income, and a potential hedge against market volatility. By diversifying their investment portfolio and carefully selecting fixed income securities, investors can benefit from the advantages that these investments bring to the table.

Risks of investing in fixed income

While fixed income investments offer several benefits, they also come with their fair share of risks. It’s crucial for investors to understand and carefully evaluate these risks before investing in fixed income securities. Here are some of the key risks associated with investing in fixed income:

- Interest rate risk: Changes in interest rates can have a significant impact on fixed income investments. When interest rates rise, the market value of existing fixed income securities tends to decline. This happens because newly issued securities offer higher yields, making existing securities comparatively less attractive. Conversely, when interest rates fall, the value of fixed income investments may increase as the fixed interest rate becomes more desirable. Investors need to consider the potential impact of interest rate fluctuations on their fixed income investments.

- Default risk: Default risk refers to the possibility that the issuer of a fixed income security may fail to make interest payments or repay the principal amount as scheduled. This risk is more prevalent in corporate bonds and lower-rated securities issued by governments or corporations. Investors need to assess the creditworthiness of the issuer before investing in fixed income securities to mitigate default risk.

- Liquidity risk: Fixed income securities may have varying levels of liquidity. Liquidity risk arises when investors find it challenging to buy or sell a security at a fair price or within a desired timeframe. Less liquid fixed income investments, such as certain corporate bonds or securities with longer maturities, may pose a higher liquidity risk. Being unable to liquidate an investment when desired can impact an investor’s ability to access funds or make necessary portfolio adjustments.

- Reinvestment risk: Reinvestment risk refers to the potential disadvantageous impact of reinvesting interest or principal repayments at lower interest rates. If an investor’s fixed income investment matures or pays interest during a period of declining interest rates, reinvesting the funds may result in lower income generation. This risk can affect the overall return of a fixed income portfolio and needs to be considered when investing in long-term fixed income securities.

- Inflation risk: Inflation risk is the potential erosion of purchasing power due to rising prices. Fixed income investments with fixed interest rates may be particularly vulnerable to inflation risks. If the interest earned from the investment does not keep pace with inflation, the real value of the investment can diminish over time. Investors need to consider investments with inflation-protected features, such as Treasury Inflation-Protected Securities (TIPS), to mitigate inflation risk.

- Credit risk: Credit risk refers to the potential for an issuer to default on its financial obligations. This risk is more significant for fixed income securities issued by lower-rated entities or those with weak financial stability. Credit ratings provided by independent rating agencies can help investors assess the creditworthiness and default risk associated with fixed income investments.

It is essential for investors to carefully evaluate these risks and diversify their fixed income portfolio to manage exposure effectively. Diversification across issuers, industries, and maturities can help mitigate specific risks associated with individual securities. Additionally, monitoring market conditions and staying informed about interest rate movements and creditworthiness of issuers is crucial in managing risk within a fixed income investment strategy.

By understanding the risks involved and implementing appropriate risk management strategies, investors can make informed investment decisions and navigate the potential challenges associated with investing in fixed income securities.

Factors to consider when investing in fixed income

Investing in fixed income requires careful consideration of various factors to make informed investment decisions. Here are some key factors to consider when investing in fixed income securities:

- Investment goals and risk tolerance: Begin by assessing your investment goals and risk tolerance. Clearly define whether your focus is on income generation, capital preservation, or a balance of both. Understanding your tolerance for risk will help determine the appropriate mix of fixed income investments that align with your objectives.

- Issuer creditworthiness: Evaluate the creditworthiness of the issuer. Higher-rated issuers, such as governments or reputable corporations, typically offer a lower risk of default. Credit ratings provided by independent rating agencies can provide insights into an issuer’s financial stability and likelihood of meeting their payment obligations.

- Interest rate environment: Consider the prevailing interest rate environment. When interest rates are low, fixed income investments with longer maturities may offer higher yields but could be more susceptible to potential declines in value if rates rise. Conversely, in a rising interest rate environment, shorter-term investments may be favored to mitigate the impact of potential rate increases.

- Duration and maturity: Understand the concept of duration and the maturity of your fixed income investments. Duration measures the sensitivity of the price of a fixed income security to changes in interest rates. Longer duration securities are generally more sensitive to interest rate changes. Maturity refers to the length of time until the security’s principal amount is repaid. Consider your investment time horizon and risk tolerance to determine an appropriate mix of securities with varying durations and maturities.

- Income generation: Evaluate the income generation potential of fixed income investments. Assess the yield offered by the security, which represents the income generated relative to the initial investment. Compare the yield to prevailing interest rates to gauge whether the investment provides a competitive income stream based on current market conditions.

- Liquidity: Consider the liquidity of the investment. Some fixed income securities may have limited liquidity in the secondary market, making it challenging to sell the investment if needed. Assess your liquidity needs and consider investing in more liquid securities if immediate access to funds is a priority.

- Tax implications: Understand the tax implications of investing in fixed income securities. Interest income is generally subject to taxation at the federal, state, and local levels. Consider the tax consequences and consult with a tax advisor to optimize the after-tax returns of your fixed income investments.

- Diversification: Diversify your fixed income investments. Spreading your investments across different issuers, industries, and maturities can help mitigate specific risks associated with individual securities. Consider diversifying across various types of fixed income investments, such as government bonds, corporate bonds, or treasury bills, to reduce concentration risk.

By considering these factors, investors can make informed decisions when selecting fixed income securities. It is important to regularly review and reassess your fixed income portfolio to ensure it aligns with your investment goals, risk tolerance, and changing market conditions.

How to invest in fixed income securities

Investing in fixed income securities can be done through various avenues. Here are some common ways to invest in fixed income:

- Individual Bonds: One way to invest in fixed income is to purchase individual bonds directly. This involves researching and selecting specific bonds based on factors like creditworthiness, interest rates, and maturity dates. This approach allows investors to build a bond portfolio tailored to their preferences and investment goals.

- Bond Mutual Funds: Bond mutual funds pool money from multiple investors to invest in a diversified portfolio of bonds. These funds are managed by professional fund managers who conduct research, select bonds, and manage the portfolio. Investing in bond mutual funds is a convenient option for investors who prefer a hands-off approach and want access to a diversified portfolio within a single investment.

- Exchange-Traded Funds (ETFs): Fixed income ETFs are similar to bond mutual funds but trade on exchanges like stocks. ETFs represent shares of a diversified portfolio of fixed income securities. They provide the flexibility to buy and sell shares during market hours at market prices. Investing in fixed income ETFs offers liquidity, diversification, and transparency, making them popular among investors.

- Certificates of Deposit (CDs): Investing in CDs involves depositing funds with a bank or credit union for a specific period at a fixed interest rate. CDs are considered relatively low-risk investments due to their FDIC insurance coverage. They are suitable for investors looking for a fixed return over a specific time frame.

- Treasury Securities: Treasury securities are issued by the U.S. Department of the Treasury. They include treasury bills, notes, and bonds. Investors can purchase these securities directly from the Treasury through TreasuryDirect.gov or through brokers. Investing in treasury securities is considered low-risk as they are backed by the full faith and credit of the U.S. government.

- Preferred Stocks: Preferred stocks combine characteristics of both stocks and bonds. They offer fixed dividend payments, similar to coupon payments on bonds. Investors can buy preferred stocks directly from the stock market or through brokerage accounts. Preferred stocks can provide a mix of income generation and potential capital appreciation.

When investing in fixed income securities, it is important to conduct thorough research, assess risk factors, and consider your investment goals and risk tolerance. Here are some key steps to follow:

- Define your investment goals and risk tolerance.

- Educate yourself about the different types of fixed income securities available in the market.

- Research and analyze the creditworthiness of issuers and evaluate their financial stability.

- Determine the appropriate mix of fixed income securities based on your investment objectives.

- Select a method of investing, such as purchasing individual bonds, investing in bond mutual funds or ETFs, or considering other fixed income options.

- Open a brokerage account or establish a relationship with a financial advisor to facilitate your fixed income investments.

- Monitor market trends, interest rate movements, and the performance of your fixed income portfolio.

- Regularly review and reassess your fixed income investments to ensure they align with your goals and changing market conditions.

It is advisable to seek guidance from a financial advisor or investment professional who can provide personalized advice based on your individual circumstances and help you make informed decisions when investing in fixed income securities.

Conclusion

Fixed income investments offer a range of benefits to investors, including a steady stream of income, lower volatility, diversification, capital preservation, and a choice of investment options. Despite these advantages, it is crucial to be aware of the risks associated with fixed income investments, such as interest rate risk, default risk, liquidity risk, reinvestment risk, inflation risk, and credit risk.

When investing in fixed income securities, it is important to consider factors like investment goals, risk tolerance, issuer creditworthiness, interest rate environment, duration, income generation, liquidity, tax implications, and diversification. These factors will help investors make informed decisions and tailor their fixed income portfolio to their specific needs and objectives.

Investing in fixed income can be done through various avenues, including individual bonds, bond mutual funds, ETFs, CDs, treasury securities, and preferred stocks. Investors should choose the method that aligns with their investment strategy, risk tolerance, and desired level of involvement in the investment process.

Regular monitoring and evaluation of fixed income investments are crucial to ensure they continue to align with changes in market conditions and investment goals. As with any investment, it is recommended to seek guidance from a financial advisor or investment professional who can provide personalized advice based on individual circumstances.

By understanding the benefits, risks, and key factors involved in investing in fixed income securities, investors can make informed decisions and potentially benefit from the stability, income, and diversification these investments can offer in their overall investment portfolio.