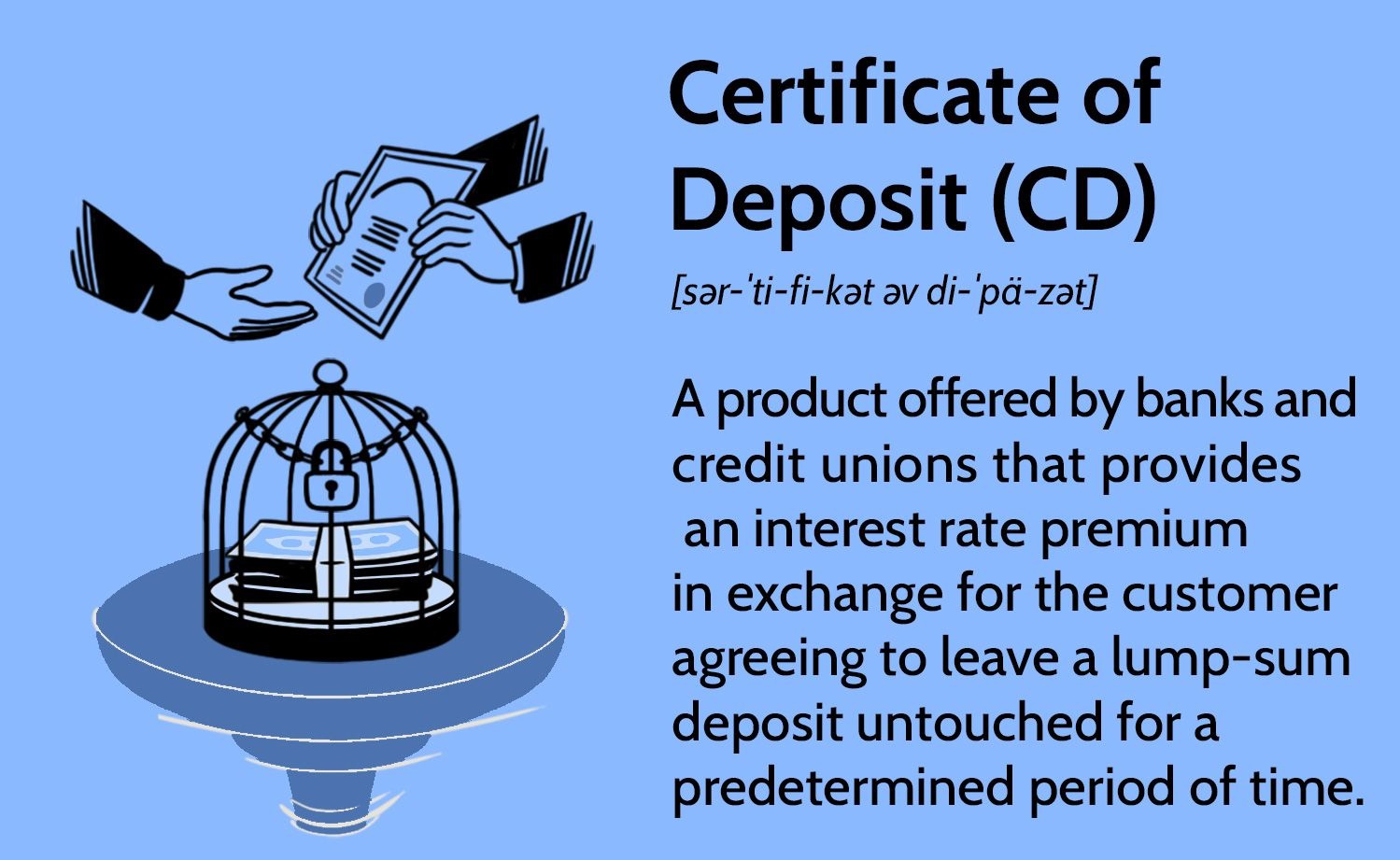

What is a Certificate of Deposit (CD)?

A Certificate of Deposit, commonly referred to as a CD, is a type of savings account offered by banks and credit unions. It is an investment vehicle that allows you to deposit a sum of money for a fixed period of time, typically ranging from a few months to several years. In return for keeping your funds locked in the CD, the financial institution pays you interest on your investment.

CDs are considered to be low-risk investments because they are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor. This means that even if the bank fails, your funds will still be protected.

CDs offer a fixed interest rate, meaning the rate is set when you open the account and remains the same throughout the term of the CD. This can be advantageous if you prefer a predictable and stable return on your investment.

Unlike regular savings accounts, CDs have a maturity date. Once the CD reaches its maturity date, you can choose to withdraw the funds and the accrued interest or roll it over into a new CD. It’s important to note that there may be penalties for early withdrawal before the maturity date.

CDs are a popular choice for individuals who want to save money while earning a higher interest rate compared to a regular savings account. They are a relatively safe investment option, making them suitable for conservative investors who prioritize capital preservation.

Overall, CDs provide a secure and controlled way to grow your money over a fixed period of time. They offer a combination of safety, stability, and potentially higher returns, making them an attractive choice for those looking to achieve specific financial goals or diversify their investment portfolio.

When should you consider a CD?

While a Certificate of Deposit (CD) may not be the best banking choice for every situation, there are several scenarios where it can be highly beneficial. Consider a CD when:

- You want to save for a specific goal: If you have a specific financial objective, such as saving for a down payment on a house or funding a vacation, a CD can help you stay focused and disciplined. By locking in your funds for a fixed period, you are less likely to be tempted to spend the money elsewhere.

- You don’t need immediate access to your money: Unlike a regular savings account where you can withdraw funds at any time, a CD requires you to keep your money invested for a set period. If you have other emergency savings or don’t anticipate needing the funds in the near future, a CD can offer higher interest rates in exchange for limited liquidity.

- You want a guaranteed return on your investment: CDs provide a fixed interest rate, ensuring that you will earn a predetermined amount on your investment. This can be particularly appealing if you are risk-averse and prefer stability over potentially higher but uncertain returns.

- You can afford to lock in your funds for a fixed period: When opening a CD, you agree to keep your money invested for a specified duration, known as the term. Understand the terms and ensure that you won’t need access to the funds before the CD matures. If you can afford to set aside the money for the specified time, a CD can be an effective investment vehicle.

- You want to diversify your investment portfolio: If your investment portfolio primarily consists of stocks and bonds, adding a CD can help diversify your holdings. CDs are considered low-risk investments, providing a stable and predictable return. By diversifying, you can mitigate potential risks and find a balance between higher-risk and lower-risk investments.

- You want to reduce risks in your investment: In times of market volatility or economic uncertainty, CDs can serve as a safe haven for your money. They are insured by the FDIC, guaranteeing the safety of your principal investment up to the maximum limit. This can provide peace of mind and protect your savings in turbulent times.

- You want to earn higher interest rates: Compared to traditional savings accounts, CDs often offer higher interest rates. If you’re seeking ways to grow your savings with a relatively low level of risk, a CD can be an attractive option to earn a better return on your money.

- You want to save for retirement or a big purchase: If you have long-term financial goals, such as retirement or buying a home, a CD can be a reliable tool for saving. By choosing a CD with a longer term, you can potentially earn higher interest rates and maximize your savings for the future.

- You need a low-risk investment option: If you are risk-averse and prioritize the preservation of your capital, a CD can be a suitable low-risk investment option. You can invest your money without worrying about market fluctuations or potential losses typically associated with riskier investments.

- You want to teach children about savings and investments: CDs can be an excellent tool to educate children about the importance of saving and investing. By opening a CD in their name, you can show them how their money can grow over time and instill valuable financial habits from an early age.

- You want to avoid the temptation of spending your savings: If you struggle with impulsive spending or constantly dipping into your savings, a CD can create a barrier between you and your funds. With limited access to the money until the CD matures, you are less likely to frivolously spend your savings and can focus on long-term financial goals.

Considering these factors will help you determine if a CD aligns with your financial needs and objectives. Keep in mind that while CDs offer various benefits, they may not be suitable for everyone’s financial situation. Assess your goals, risk tolerance, and liquidity needs to determine if a CD is the best banking choice for you.

When you want to save for a specific goal

Saving for a specific goal is a common scenario where a Certificate of Deposit (CD) can be the best banking choice. Here are a few reasons why a CD can be advantageous when you have a specific financial objective:

Focus and discipline: When you have a specific goal in mind, such as purchasing a car or funding a wedding, it’s important to stay focused and disciplined with your savings. A CD can help you achieve this by requiring you to lock in your funds for a fixed period of time. This can prevent you from being tempted to spend the money frivolously or use it for other expenses.

Higher interest rates: Compared to regular savings accounts, CDs often offer higher interest rates. This means that your savings can grow at a faster rate over time, helping you reach your goal more quickly. By taking advantage of the higher interest rates offered by CDs, you can maximize your savings and increase your chances of achieving your specific financial goal.

Predictable returns: One of the key benefits of CDs is their fixed interest rates. When you open a CD, the interest rate is set at the beginning, and it remains the same throughout the term of the CD. This predictability allows you to calculate and plan for the exact amount you will earn on your investment. When saving for a specific goal, having a predictable return can be helpful in determining how much you need to save and how long it will take to reach your target.

Capital preservation: Saving for a specific goal often involves protecting the capital you have accumulated. Unlike other investment options that may carry risks, CDs are considered low-risk investments. They are insured by the FDIC up to $250,000 per depositor, providing an added layer of security. This assurance allows you to have peace of mind knowing that your money is safe and will be available when you need it to achieve your goal.

Term options: CDs offer various term options, ranging from a few months to several years. This flexibility allows you to choose a term that aligns with your specific goal. For shorter-term goals, you can opt for a shorter-term CD, while longer-term goals may require a CD with a longer term. By selecting the appropriate term, you can ensure that your money will be available when you need it to accomplish your goal.

When saving for a specific goal, it’s essential to consider your time frame, risk tolerance, and liquidity needs. While CDs can provide numerous benefits, they may not be suitable for goals that require immediate access to funds or those with a longer time horizon that may benefit from other investment options. Assess your specific goal and determine if a CD aligns with your overall financial strategy.

When you don’t need immediate access to your money

When you have funds that you don’t need immediate access to, a Certificate of Deposit (CD) can be the best banking choice. Here’s why:

Higher interest rates: CDs typically offer higher interest rates compared to regular savings accounts. By depositing your money into a CD, you can earn a higher return on your investment. This can be particularly advantageous if you don’t need immediate access to the funds and are willing to lock them in for a specific term.

Financial goal allocation: If you have already set aside emergency savings or funds for daily expenses, putting additional savings into a CD can help you allocate your money for specific financial goals or purposes. Whether you’re saving for a down payment on a house, a college education, or a dream vacation, a CD allows you to set aside funds and watch them grow over time.

Limited spending temptation: By depositing your money into a CD, you create a barrier between your savings and impulsive spending. Since CDs have a fixed term and may incur penalties for early withdrawal, you are less likely to access the funds for unnecessary expenses. This can serve as a way to maintain financial discipline and prevent you from dipping into your savings when it’s not necessary.

Stable returns: CDs offer a fixed interest rate, guaranteeing a predictable return on your investment. This can be beneficial if you are looking for stability and don’t want to worry about fluctuations in interest rates or market conditions. The stability of returns can help you plan and budget more effectively for future financial needs.

Eliminate market risks: Unlike investments in stocks or bonds, CDs are not subject to market risks. They provide a safe haven for your money, as they are backed by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor. This means your funds are protected, regardless of market conditions or economic downturns.

Financial peace of mind: If you don’t need immediate access to your money, investing in a CD can provide you with peace of mind. Knowing that your funds are secure and earning a competitive interest rate allows you to focus on other aspects of your financial life without worrying about market volatility or the need to actively manage your investments.

Keep in mind that CDs are not suitable if you anticipate needing access to your funds in the near term or if you want to take advantage of potential higher returns from other investment options. Assess your financial situation, goals, and liquidity needs to determine if a CD aligns with your overall financial strategy.

When you want a guaranteed return on your investment

If you’re seeking a guaranteed return on your investment, a Certificate of Deposit (CD) can be the best banking choice for you. Here’s why:

Fixed interest rates: When you open a CD, the interest rate is set at the beginning and remains fixed throughout the term of the CD. This means that you are guaranteed to earn a specific rate of return on your investment. Unlike other investment options that may be subject to market fluctuations and uncertain returns, a CD provides stability and predictability.

Predictable income: The fixed interest rate of a CD ensures that you’ll receive a specific amount of income from your investment. This can be particularly beneficial if you rely on a steady income stream or want to plan your budget with certainty. With a CD, you can calculate and anticipate the exact amount of interest you will earn over the term of the investment.

Capital preservation: CDs are considered low-risk investments, making them an ideal choice when you want to preserve your capital. CD accounts are typically insured by the Federal Deposit Insurance Corporation (FDIC), providing coverage of up to $250,000 per depositor. This means that even if the bank fails, your principal investment is protected.

Protect against market volatility: Investing in stocks or bonds carries the risk of market volatility, where the value of your investments can fluctuate. However, with a CD, you are shielded from these market risks. The fixed interest rate and maturity date provide a level of stability and protect your investment against the uncertainties of the financial markets.

Eliminate credit risk: CDs are backed by the issuing financial institution, meaning they are not subject to credit risk. As long as the bank or credit union is insured by the FDIC, your investment is secure even if the institution faces financial difficulties. This adds an additional layer of protection and ensures that your principal investment will be returned to you at maturity.

Simplicity and ease of investment: Investing in a CD is simple and straightforward. You can easily open a CD account at most banks or credit unions with a minimum deposit amount. The process is typically hassle-free and doesn’t require any complex investment decisions or ongoing management, making it an accessible option for individuals who prefer a hands-off investment approach.

A CD offers peace of mind by providing a guaranteed return on your investment. It is a reliable and low-risk option for individuals who prioritize preserving capital and want to avoid the uncertainties of other investment choices. However, it’s important to note that the fixed interest rate of a CD may be lower compared to potential returns from higher-risk investments. Consider your financial goals, risk tolerance, and time horizon to determine if a CD aligns with your investment strategy.

When you can afford to lock in your funds for a fixed period

A Certificate of Deposit (CD) can be the best banking choice when you have the ability to lock in your funds for a fixed period of time. Here’s why:

Higher interest rates: CDs often offer higher interest rates compared to regular savings accounts. By choosing a CD, you can take advantage of these higher rates and potentially earn more on your investment. This can be especially beneficial if you have the ability to keep your funds locked in for a longer period.

Stable and predictable returns: When you opt for a CD, you know exactly how much interest you will earn over the specified term. This predictability allows for better financial planning and budgeting. By locking in your funds, you can have a clear expectation of the return you will receive at the end of the CD’s maturity.

Financial goal alignment: If you have specific financial goals, such as saving for a down payment on a house or funding a child’s education, a CD can be an effective tool. By setting aside a portion of your funds in a CD, you can ensure that they are dedicated to achieving these goals. The fixed term of the CD provides a disciplined approach to saving and helps you stay on track to reach your objectives.

Taking advantage of market conditions: If you believe that interest rates may decrease in the future, locking in your funds with a CD allows you to secure a higher interest rate now. By doing so, you can benefit from the current market conditions and potentially earn more on your investment than if you were to leave the funds in a regular savings account.

Discipline and avoiding impulsive spending: By putting your funds into a CD, you remove the temptation to spend the money impulsively. The locked-in nature of a CD discourages withdrawing the funds before the maturity date and promotes disciplined saving for the allotted time period. This can be particularly beneficial if you struggle with controlling your spending or need a more structured approach to saving.

Taking advantage of penalty-free withdrawal options: While early withdrawal from a CD may come with penalties, some institutions offer penalty-free or partial withdrawal options. If you have the flexibility to plan for unexpected expenses or emergencies, these withdrawal options can provide you with the necessary access to funds while still benefiting from the higher interest rates offered by a CD.

Before investing in a CD, assess your financial situation, liquidity needs, and goals. Ensure that you have the financial capability to afford locking in your funds for the specified term. While CDs offer attractive interest rates, they may not be suitable if you require immediate access to your funds or anticipate needing them in the near future.

When you want to diversify your investment portfolio

A Certificate of Deposit (CD) can be a valuable addition to your investment portfolio when you want to diversify your holdings. Here’s why:

Low-risk investment: CDs are considered low-risk investments. They provide a guaranteed return on your investment and are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor. By including CDs in your portfolio, you can help mitigate the overall risk of your investments and add stability to your portfolio.

Steady and predictable returns: With a CD, you know exactly how much interest you will earn over the specified term. The fixed interest rate provides stability and predictability in terms of returns. This can be particularly valuable when you want to balance higher-risk investments in your portfolio with a safer and more consistent income stream.

Capital preservation: CDs are designed to protect and preserve your capital. The guaranteed return and FDIC insurance ensure that your principal investment is secure. By including CDs in your portfolio, you allocate a portion of your funds to a low-risk, capital-preserving asset.

Counterbalance market volatility: Investments such as stocks and bonds are subject to market volatility and fluctuations. Adding CDs to your portfolio can act as a counterbalance to market risks. When the stock market experiences downturns or uncertainty, the stability of CDs can help cushion the impact of market volatility on your overall investment returns.

Flexibility in term options: CDs offer various term options, ranging from a few months to several years. This flexibility allows you to choose CDs with terms that align with your investment goals and time horizons. You can diversify your portfolio by selecting CDs of different durations, enabling you to meet both short-term and long-term financial objectives.

Income generation: If you’re seeking a reliable income stream from your investments, CDs can play a role in generating stable interest income. By strategically incorporating CDs with varying maturity dates into your portfolio, you create consistent cash flows that can supplement other sources of income or fulfill specific financial needs.

Portfolio rebalancing: Adding CDs to your portfolio provides an opportunity for periodic rebalancing. As other investments fluctuate in value, the stable returns of CDs can help you maintain your desired asset allocation. By regularly assessing your portfolio and adjusting the proportion of CDs, you can realign your investments with your risk tolerance and long-term goals.

Diversification is a key strategy for mitigating risk and optimizing returns in an investment portfolio. When incorporating CDs into your portfolio, consider your investment objectives, risk tolerance, and desired asset allocation. By diversifying across different asset classes, including CDs, you can achieve a well-rounded investment strategy that balances risk and potential returns.

When you want to reduce risks in your investment

When it comes to investing, it’s natural to seek ways to reduce risks and protect your hard-earned money. Adding a Certificate of Deposit (CD) to your investment portfolio can be an effective strategy for risk reduction. Here’s why:

Low-risk investment: CDs are considered low-risk investments. They offer a guaranteed return on your investment, and most importantly, they are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor. This insurance provides an additional layer of protection and reduces the risk of losing your principal investment.

Capital preservation: Preservation of capital is a primary concern for many investors, especially those with a conservative risk appetite. CDs are designed to safeguard your capital, providing a secure and stable investment option. With a CD, you can have peace of mind knowing that your initial investment will be intact at maturity, regardless of market conditions.

Stable and predictable returns: CDs offer fixed interest rates, ensuring a predictable return on your investment. This predictability can be especially valuable in times of market volatility or economic uncertainty. Knowing exactly how much you will earn from your CD investment allows for better financial planning and a more stable income stream.

Hedging against market fluctuations: Investing solely in stocks or bonds exposes your portfolio to market volatility. By diversifying with CDs, you can hedge against these fluctuations. CDs provide stability and act as a counterbalance to the more volatile investments in your portfolio. This helps to reduce the overall risk of your investment holdings.

Insulation from interest rate changes: Interest rates can have a significant impact on investment returns. When interest rates fall, bonds and other fixed-income investments may suffer. However, with a CD, you are protected from such changes as your interest rate is locked in at the time of purchase. This security shields your investment from potential decreases in interest rates.

Lower exposure to market risks: The stock market can be unpredictable, with the potential for significant downturns. By allocating some of your investment funds to CDs, you decrease your exposure to market risks. This diversification of asset classes helps to reduce the overall volatility of your portfolio and provides a more stable foundation for your investments.

Peace of mind: Investing in CDs can provide you with peace of mind, particularly if you have a lower risk tolerance. The assurance of a guaranteed return, principal protection, and stable income stream can alleviate the stress and anxiety associated with more volatile investment options. This emotional peace of mind can lead to better decision-making and a more positive investing experience.

While CDs offer lower risk, it’s important to consider your specific investment goals and risk appetite. If you’re seeking higher potential returns or have a longer investment horizon, other investment vehicles might better suit your needs. Be sure to assess your overall investment strategy and select the right balance of risk and stability that aligns with your financial objectives.

When you want to earn higher interest rates

When seeking higher returns on your investments, a Certificate of Deposit (CD) can be the best banking choice. Here’s why:

Competitive interest rates: CDs typically offer higher interest rates compared to regular savings accounts. By depositing your funds into a CD, you can earn a more attractive return on your investment. This can be particularly beneficial when you want to maximize the growth of your savings or generate additional income.

Fixed interest rates: When you open a CD, the interest rate is fixed for the term of the investment. This stability ensures that your returns remain consistent, even if interest rates in the market decline. By locking in a higher interest rate, you can take advantage of favorable market conditions and earn more on your investment over time.

Higher yields for longer terms: CDs with longer terms often come with higher interest rates. If you have a longer investment horizon and can afford to lock in your funds for an extended period, you may be rewarded with even higher yields. This can be advantageous if you’re saving for long-term goals, such as retirement or a child’s education.

Enhanced growth of savings: By earning higher interest rates on your CD, your savings can grow at a faster pace. This accelerated growth can help you reach your financial goals more quickly or build a larger nest egg over time. If you’re looking to compound your savings and boost your overall wealth, a CD with competitive interest rates can be an effective tool.

Protection against market fluctuations: Investing in stocks or other market-based instruments comes with the risk of market volatility. CDs, on the other hand, provide a safe haven for your money. They are not affected by market fluctuations, allowing you to earn a consistent return on your investment regardless of economic conditions.

Stress-free investment: Investing in CDs is simple and straightforward. Once you open a CD, you don’t need to actively manage or monitor the investment. This passive approach can be particularly appealing if you prefer a hands-off investment strategy with minimal time and effort required.

Security and peace of mind: CDs are backed by the Federal Deposit Insurance Corporation (FDIC), offering insurance coverage of up to $250,000 per depositor. This guarantee ensures the safety of your principal investment, providing peace of mind and security. Whether you’re saving for short-term goals or long-term objectives, the protection offered by CDs can help you invest with confidence.

When seeking higher interest rates, carefully consider the terms, rates, and duration of CDs available. Compare different offerings from various financial institutions to find the best rates that align with your investment goals. Keep in mind that while CDs offer attractive returns, they may not provide the same level of liquidity as other investment options. Therefore, assess your financial needs and liquidity requirements before committing to a CD investment.

When you want to save for retirement or a big purchase

Whether you’re saving for retirement or a significant purchase, a Certificate of Deposit (CD) can be an excellent banking choice. Here’s why:

Long-term savings: Saving for retirement or a big purchase typically requires a long-term approach. CDs with longer terms can be a suitable option for these goals. By depositing your funds into a CD, you commit to leaving the money invested for a specific period, allowing it to grow steadily over time.

Stable and predictable returns: CDs offer fixed interest rates, which means your returns are predictable. This stability allows for better financial planning, and it helps you build a more accurate picture of your future finances. By choosing a CD, you can have confidence in the consistent growth of your savings, whether it’s for retirement or a major expense.

Protection against market volatility: Investments such as stocks and mutual funds are prone to market fluctuations. However, CDs provide a safe haven for your savings. Their guaranteed return and protection from market volatility make them an attractive option for individuals who want to safeguard their money while saving for retirement or a big purchase.

High-interest potential for longer terms: CDs with longer terms often come with higher interest rates. This means that the longer you’re willing to leave your funds invested, the more you can potentially earn on your savings. For long-term financial goals like retirement, taking advantage of CDs with extended terms can help you maximize your savings and accumulate a larger nest egg.

Diversification of investment portfolio: Including CDs in your investment portfolio helps diversify your holdings. If you already have investments in stocks or bonds, adding CDs can balance your risk exposure. CDs provide a low-risk, stable component to your portfolio, which can help mitigate potential volatility from other investments.

Discipline in savings: Saving for retirement or a big purchase requires discipline. CDs can aid in this process by locking in your funds for a predetermined period. This discourages impulsive spending and helps you stay focused on your long-term financial goals, ensuring that your savings continue to grow steadily without interruptions.

Protection of principal: CDs offer the security of FDIC insurance, meaning your principal investment is protected up to $250,000 per depositor, per institution. This protection ensures the safety of your savings, so you can have peace of mind knowing that your funds will be available when you need them most.

When saving for retirement or a significant purchase, carefully consider your time horizon, risk tolerance, and liquidity needs. Evaluate the available CD options, including their interest rates, term lengths, and penalties for early withdrawal. By aligning your savings strategy with your specific goals, a CD can be a valuable tool to help you achieve a financially secure retirement or fulfill your long-awaited purchase.

When you need a low-risk investment option

When you prioritize low-risk investments, a Certificate of Deposit (CD) can be the ideal banking choice. Here’s why:

Capital preservation: CDs are designed to safeguard your initial investment. They offer a guaranteed return on your funds and provide protection against potential market volatility. By choosing a CD, you can have peace of mind knowing that your principal amount will be preserved, regardless of economic conditions.

FDIC insurance: CDs are typically insured by the Federal Deposit Insurance Corporation (FDIC), up to $250,000 per depositor, per institution. This insurance coverage ensures that your investment is protected in the event of bank failure. The assurance of FDIC insurance adds an extra layer of security and makes CDs a trusted low-risk investment option.

Stability of returns: CDs offer fixed interest rates, which means your returns remain constant throughout the term of the investment. This stability allows for better financial planning and helps you accurately forecast your earnings. By choosing a CD, you can rely on a predictable income stream without worrying about market fluctuations.

Protection against market volatility: Investing in stocks or bonds exposes your portfolio to market risks and volatility. CDs, on the other hand, provide a safe haven for your money. They are not affected by the ups and downs of the stock market, making them an attractive choice for risk-averse investors who want stability and predictability in their investments.

Minimal credit risk: CDs are backed by the issuing financial institution, reducing the credit risk associated with other types of investments. As long as the bank or credit union is insured by the FDIC, your investment is secure. This gives you confidence that your savings will be returned to you at maturity, regardless of the financial health of the institution.

Ease of investment: Opening a CD is a simple and straightforward process. Most banks and credit unions offer CD options, allowing you to easily allocate your funds into this low-risk investment. This accessibility and ease of investment make CDs a convenient choice, especially for those seeking simplicity and stability in their financial portfolios.

Flexibility in terms: CDs come with a variety of term options, ranging from a few months to several years. This flexibility allows you to select a term that aligns with your financial goals and liquidity needs. You can choose a shorter term if you anticipate needing the funds in the near future, or a longer term for longer-term savings goals.

When you require a low-risk investment option, carefully consider your financial goals, risk tolerance, and liquidity requirements. Assess the available CDs from different financial institutions, comparing interest rates, terms, and penalties for early withdrawal. By incorporating low-risk investments like CDs into your portfolio, you can achieve a balanced approach to wealth preservation and steady income generation.

When you want to teach children about savings and investments

Introducing children to the concepts of savings and investments at a young age can set them on a path towards financial literacy and success. Using a Certificate of Deposit (CD) can be a valuable tool in teaching them about these important financial principles. Here’s why:

Safe and secure investment: CDs are considered low-risk investments with guaranteed returns. This makes them an ideal way to introduce children to the world of investing without exposing them to the higher risks associated with stocks or bonds. By discussing the security and stability of a CD, children can understand the importance of making safe choices with their money.

Interest and compounding: CDs provide an opportunity to teach children about the concept of earning interest and how it can grow their savings over time. You can explain the basics of simple interest and even introduce them to the idea of compounding interest, showcasing how their money can work for them and grow exponentially as they continue to save.

Long-term savings goals: Encouraging children to save for long-term goals, such as buying a car or going to college, can be made more tangible with the use of a CD. Discuss the concept of setting aside money in a CD for a specific period of time to accrue interest and achieve their desired goal. This helps instill the importance of patience and delayed gratification in reaching financial milestones.

Understanding terms and maturity dates: Introducing children to the idea of investing in CDs helps them understand the concept of terms and maturity dates. Explain how a CD has a predetermined period, during which their money is locked in, and that they will receive both their original investment and the interest earned at the end of the term. This promotes a greater understanding of financial contracts and the importance of honoring them.

Teaching financial responsibility: Opening a CD account can teach children about the importance of setting aside money regularly and being consistent with their savings habits. They can observe how their savings grow over time and learn the value of patience and discipline when it comes to managing their finances.

Money management skills: Monitoring a CD allows children to develop essential money management skills. Encourage them to keep track of their deposits, interest earned, and the maturity date of the CD. This hands-on experience helps develop financial management habits, such as record-keeping and tracking financial progress.

Building a strong foundation: By incorporating CDs into their financial education, children can develop a strong foundation in savings and investing principles that will serve them well into adulthood. The lessons learned from CD investments can translate to other investment opportunities they may encounter in the future.

When teaching children about savings and investments, it’s important to use age-appropriate language and concepts. Explain the basics of CDs in a way they can understand and relate to. Encourage open discussions about money, savings goals, and the importance of making informed financial decisions. By incorporating CDs into their financial education, you can empower children to develop smart money habits and set them on the path to financial success.

When you want to avoid the temptation of spending your savings

It’s not uncommon for individuals to struggle with the temptation of spending their savings instead of saving it for future needs or goals. In such cases, a Certificate of Deposit (CD) can be an effective banking choice. Here’s why:

Locking in your funds: When you open a CD, you commit to keeping your money invested for a specific period of time. This “lock-in” feature can help you avoid the temptation of spending your savings impulsively. The locked-in nature of a CD acts as a barrier, making it less likely that you will dip into the funds for non-essential expenses.

Penalty for early withdrawal: CDs often come with penalties for withdrawing funds before the maturity date. Knowing that early withdrawal will result in a financial cost can further deter you from spending your savings unnecessarily. The potential penalty acts as an additional incentive to maintain the discipline of leaving your savings untouched.

Creating a savings plan: By earmarking a portion of your funds for a CD, you establish a structured savings plan. This plan sets clear boundaries on your savings and prevents you from freely accessing the money without a purpose. The knowledge that your savings are growing steadily in a CD can provide motivation to resist the urge to spend impulsively.

Stable and predictable returns: CDs offer fixed interest rates, which means your returns are guaranteed and predictable. This stability can reinforce the value of saving and deter you from spending your savings on fleeting desires. By focusing on the consistent growth of your savings through the CD, you can develop a long-term mindset and resist the temptation to spend in the short term.

Protection against impulsive purchases: Having a portion of your savings in a CD makes it less accessible for impulsive purchases. The process of withdrawing funds from a CD typically involves waiting until the maturity date or incurring a penalty. This delay gives you time to reconsider impulsive buying decisions and encourages more thoughtful spending habits.

Alternative cash flow options: If unexpected expenses arise and you need access to funds, some banks offer CD options with penalty-free or partial withdrawal options. These features provide flexibility and ensure that you have access to emergency funds while avoiding the temptation to spend your entire savings. However, it’s important to carefully consider these options and understand any limitations or applicable fees.

Building savings discipline: By utilizing CDs as part of your savings strategy, you can develop discipline when it comes to managing your finances. The act of committing to a long-term CD encourages regular saving habits and reinforces the importance of prioritizing future needs over immediate gratification.

When you want to avoid the temptation of spending your savings, incorporating CDs into your financial plan can provide structure, discipline, and motivation. By establishing a savings strategy with CDs, you can protect your savings from impulsive spending and work toward your long-term financial goals.

When you want a stable and predictable income stream

When seeking a stable and predictable income stream, a Certificate of Deposit (CD) can be an excellent choice. Here’s why:

Fixed interest rates: CDs offer fixed interest rates, which means that your income stream remains consistent throughout the term of the investment. This predictability allows for better financial planning and budgeting, as you know exactly how much income you can expect to receive from your CD.

Regular interest payments: Depending on the terms of your CD, interest payments can be made at regular intervals, such as monthly, quarterly, semiannually, or annually. This structure ensures a predictable income stream and provides you with a regular flow of funds, which can be especially beneficial for individuals who rely on a steady income or need regular payouts.

Reliable source of income: If you have specific financial needs or require a stable income stream, CDs can serve as a reliable source of income. They provide a guaranteed return on your investment, offering peace of mind and financial stability. This reliability can be particularly valuable during retirement or when managing living expenses.

Risk reduction: Investing in stocks or other market-based instruments carries the risk of market volatility and potential losses. In contrast, CDs come with minimal risk and offer a stable income stream. This reduces the uncertainty associated with other investment options and allows you to enjoy a more predictable cash flow.

Supplemental income: CDs can be a valuable addition to your investment portfolio, providing a supplemental income stream. By strategically diversifying your investments, you can combine income from CDs with other sources, such as bonds or dividend-paying stocks, to create a more reliable and diversified income portfolio.

Lower stress and worry: Having a stable and predictable income stream from CDs can alleviate financial stress and worry. With a fixed interest rate and regular payments, you can feel more confident and secure in your financial situation. This stability reduces the need to constantly monitor market fluctuations and allows you to focus on other aspects of your life.

Passive income generation: CDs offer a passive income stream, requiring minimal effort or ongoing management. Once you invest in a CD, you can rely on the fixed interest payments without the need for active intervention. This passive income can provide you with more time and freedom to pursue other interests or enjoy a comfortable retirement.

When seeking a stable and predictable income stream, carefully consider the terms, interest rates, and duration of CDs available. Assess your financial goals, risk tolerance, and liquidity needs to determine the appropriate allocation of funds to CDs. Remember that CDs may not provide the highest returns compared to other investment options, but their stability and reliability make them an attractive choice for generating a consistent income stream.