Introduction

Welcome to the world of banking where an array of acronyms and terms can leave even the most financially savvy individuals scratching their heads. One commonly used acronym is CD, which stands for Certificate of Deposit. If you’ve ever wondered what CD means in the banking industry, you’ve come to the right place.

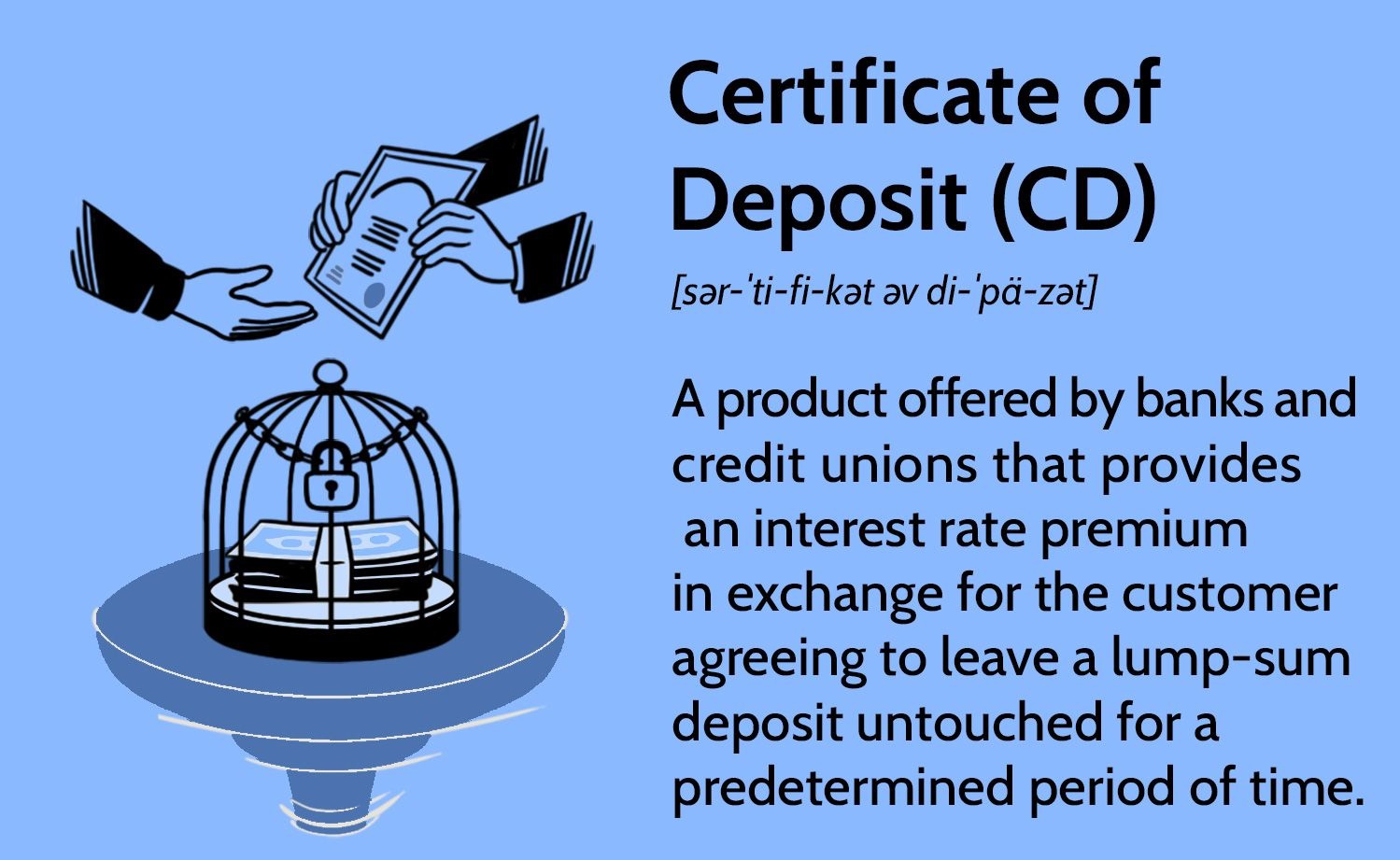

A Certificate of Deposit is a financial product offered by banks and credit unions that allows individuals to earn interest on their deposited funds over a fixed period of time. It is a type of time deposit, meaning that the funds are locked in for a predetermined period, ranging from a few months to several years.

CDs are often seen as a low-risk investment option as they offer guaranteed returns and are backed by the financial institution. This makes them an attractive choice for individuals who prioritize stability and predictability in their financial ventures.

In the following sections, we will explore the concept of CDs in more detail, including how they work, the different types available, and the advantages and disadvantages of investing in them. We will also discuss important considerations to keep in mind before opening a CD account and provide guidance on how to go about opening one.

Whether you’re a seasoned investor looking to diversify your portfolio or someone new to the world of finance seeking safe ways to grow your savings, understanding what CDs are and how they function is crucial. So, let’s delve into the world of CDs and uncover the benefits and potential drawbacks they offer to investors.

Definition of CD

A Certificate of Deposit, commonly referred to as a CD, is a financial product that allows individuals to deposit money into a bank or credit union for a fixed period of time at a specified interest rate. It is essentially a contract between the depositor and the financial institution.

When opening a CD, the depositor agrees to keep their money in the account for a predetermined period, known as the term or maturity period. This can range from a few months to several years, depending on the terms offered by the bank. During this period, the funds are not accessible without incurring a penalty.

The interest rate offered by the bank is typically higher than that of a regular savings account, making CDs an attractive option for individuals looking to accrue a fixed amount of interest on their savings. The interest can be compounded and paid out at regular intervals or upon maturity of the CD.

CDs are considered to be low-risk investments as they are insured by the Federal Deposit Insurance Corporation (FDIC) up to $250,000 per depositor per institution. This means that even if the bank were to face financial difficulties, the deposited amount (up to the insured limit) would be protected.

It’s important to note that CDs are not intended for frequent transactions or day-to-day banking needs. Instead, they serve as a vehicle for individuals to save money and earn interest over a fixed period of time.

In summary, a Certificate of Deposit is a financial instrument that allows individuals to deposit money with a bank or credit union for a specific term, at a predetermined interest rate. It offers a secure way to earn interest on savings and provides peace of mind with its FDIC insurance coverage.

How CDs Work

Understanding how CDs work is crucial before deciding to invest in them. CDs operate on a simple principle: the longer you keep your money in the account, the higher the interest rate you can earn. Here’s a breakdown of how CDs work:

1. Opening an Account: To open a CD, you’ll need to choose a bank or credit union and complete the account opening process. You’ll typically be asked to provide personal information, such as your name, address, and social security number.

2. Selecting the Term: CDs come with specific terms, ranging from a few months to several years. The term you choose determines the maturity date and the interest rate you’ll earn.

3. Depositing Funds: Once you’ve chosen the term, you’ll need to deposit the desired amount into the CD account. Some institutions may have minimum deposit requirements, so be sure to check before opening the account.

4. Earning Interest: The interest rate on a CD is fixed for the duration of the term. This means that regardless of any fluctuations in the market, you’ll continue to earn the same interest rate until the CD matures.

5. Compounding and Payout: Depending on the terms of your CD, interest can be compounded (added to the principal) or paid out at regular intervals, such as monthly or quarterly. Alternatively, the interest may be paid out in a lump sum upon maturity.

6. Early Withdrawal Penalties: If you need to access the funds before the CD matures, you may incur an early withdrawal penalty. This penalty is typically a percentage of the interest earned or a set number of days’ interest. It’s important to consider the potential penalties before opening a CD.

7. CD Renewal or Closure: Near the maturity date, the bank may offer you options to renew the CD for another term or close the account. If you choose to renew, the interest rate and terms may differ from your initial CD.

Overall, investing in a CD involves depositing a fixed amount of money for a predetermined term at an agreed-upon interest rate. The longer you keep the funds in the CD, the more interest you’ll earn. It’s important to carefully consider the term and any liquidity needs before committing to a CD.

Types of CDs

When it comes to investing in CDs, there are various types available to suit different financial goals and preferences. Here are some of the common types of CDs:

1. Traditional CDs: These are the standard CDs offered by banks, where you deposit a fixed amount of money for a specific term and earn a predetermined interest rate.

2. High-Yield CDs: High-yield CDs offer higher interest rates compared to traditional CDs. These rates are typically offered by online banks or credit unions and can vary based on the length of the term and the amount deposited.

3. Jumbo CDs: Jumbo CDs are ideal for individuals who have a large sum of money to invest. These CDs require a higher minimum deposit amount, usually upwards of $100,000, and often come with higher interest rates.

4. Callable CDs: Callable CDs provide the issuer (the bank) with the option to “call back” or terminate the CD before it reaches its maturity date. While this allows the issuer to take advantage of falling interest rates, it also introduces some level of risk for the investor.

5. Bump-Up CDs: Bump-up CDs give investors the option to increase their interest rate to take advantage of rising rates during the term of the CD. This flexibility can be especially beneficial in a rising rate environment.

6. IRA CDs: IRA CDs are specifically designed for retirement savings. These CDs are held within an Individual Retirement Account (IRA) and offer tax advantages, such as contributions being tax-deductible or tax-free growth.

7. Step-Up CDs: Step-up CDs offer a gradually increasing interest rate over the term of the CD. These CDs provide the benefit of potentially earning higher interest rates as time goes on.

It’s important to research and compare the features, terms, and rates of different types of CDs before making a decision. Consider your financial goals, risk tolerance, and liquidity needs to determine which type of CD aligns best with your requirements.

By understanding the various types of CDs available, investors can choose the one that suits their individual preferences and optimize their earnings potential.

CD Terms and Rates

CD terms and rates play a crucial role in determining the potential earnings and liquidity of your investment. Here’s what you need to know about CD terms and rates:

1. Term Length: CD terms can vary widely, ranging from as short as a few months to as long as several years. The term you choose will impact the interest rate offered and the accessibility of your funds. Generally, longer-term CDs tend to offer higher interest rates.

2. Fixed Rates: Most CDs offer fixed interest rates, meaning the rate remains the same throughout the term of the CD. This provides stability and allows you to accurately predict your earnings at maturity.

3. Annual Percentage Yield (APY): The APY represents the actual annual rate of return, taking into account compounding interest. It is a crucial factor to consider when comparing different CD options and comparing the potential earnings from various institutions.

4. Promotional Rates: Banks sometimes offer promotional rates to attract customers. These rates may be higher than standard rates but typically apply for a limited time. It’s important to carefully review the terms and conditions to understand when and how the promotional rate may change.

5. Relationship Rates: Some financial institutions offer relationship rates to customers who have multiple accounts or meet specific criteria. These rates reward customer loyalty and can result in higher interest earnings on CDs.

6. Penalties for Early Withdrawal: CD terms typically come with restrictions on accessing funds before the CD matures. If you need to withdraw funds early, you may face penalties, such as forfeiting a portion of the interest earned or paying a set number of days’ interest. Be sure to understand the penalties associated with early withdrawal before investing in a CD.

When comparing CD terms and rates, it’s essential to consider your financial goals and liquidity needs. Longer-term CDs may offer higher interest rates but can tie up your funds for an extended period. Shorter-term CDs may provide more flexibility but may have lower interest rates.

Lastly, shop around and compare rates offered by different financial institutions to ensure you’re getting the best possible return on your investment. Understanding CD terms and rates will help you make an informed decision and maximize your earnings potential.

Advantages of CDs

Investing in Certificates of Deposit (CDs) offers several advantages that make them an appealing option for many individuals. Here are some of the key advantages of CDs:

1. Guaranteed Returns: CDs provide a fixed return on investment, with the interest rate locked in for the entire term of the CD. This guarantee gives investors peace of mind, knowing exactly how much they will earn at maturity.

2. Low-Risk Investment: CDs are considered low-risk investments because they are backed by the Federal Deposit Insurance Corporation (FDIC), up to $250,000 per depositor per institution. This security ensures that even in the event of a bank failure, your deposited amount (up to the insured limit) will be protected.

3. Stable and Predictable: The fixed interest rate and term length of CDs make them a stable and predictable investment option. This feature makes them especially attractive for individuals who prioritize capital preservation and prefer a low-risk investment strategy.

4. Diversification: CDs offer a means of diversifying your investment portfolio. By allocating a portion of your savings to CDs, you can balance risk and potentially enhance your overall investment performance. CDs can complement other higher-risk investments, such as stocks or bonds, by providing a secure source of income.

5. Higher Interest Rates: Compared to regular savings accounts, CDs often offer higher interest rates. This can enable individuals to earn more interest on their savings over time, helping their funds grow at a faster rate.

6. Flexibility in Term Length: CD terms can vary, allowing individuals to choose a duration that aligns with their financial goals. Whether you’re looking to save for a short-term goal or invest for the long haul, there is a CD term that can match your timeline.

7. Tax Benefits: Certain types of CDs, such as Individual Retirement Account (IRA) CDs or other tax-advantaged CDs, offer tax benefits. Contributions to these accounts may be tax-deductible or offer tax-free growth, providing a way to save for retirement while enjoying potential tax advantages.

Keep in mind that while CDs offer numerous advantages, they may not be suitable for everyone. Consider your financial goals, liquidity needs, and risk tolerance before investing in CDs to ensure they align with your overall investment strategy.

Overall, the advantages of CDs make them an attractive investment option for those seeking stability, guaranteed returns, and potential growth on their savings without taking on high levels of risk.

Disadvantages of CDs

While Certificates of Deposit (CDs) have their advantages, there are also several disadvantages to consider before investing. Being aware of these drawbacks can help you make an informed decision. Here are some of the disadvantages of CDs:

1. Limited Liquidity: One of the main drawbacks of CDs is the limited liquidity they offer. Once you deposit your funds into a CD, they are tied up for the duration of the term. Withdrawing the funds before the CD matures may result in penalties and the loss of potential interest earnings.

2. Opportunity Cost: By investing in a CD, you are committing your funds to a fixed interest rate for a specific term. If interest rates rise during that term, you may miss out on potentially higher returns from other investment opportunities.

3. Inflation Risk: CDs may be subject to inflation risk. If the rate of inflation exceeds the interest earned on the CD, the purchasing power of your funds may decrease over time. This means that the real value of your savings may not keep pace with inflation.

4. Lower Yields: While CDs may offer higher interest rates compared to regular savings accounts, they generally provide lower yields compared to some other investment options, such as stocks or bonds. These lower yields can limit the potential for significant earnings growth.

5. Locked-in Rates: Once you open a CD, the interest rate is fixed for the term of the CD. While this stability can be an advantage, it can also be a disadvantage if interest rates gradually increase, as you won’t benefit from the higher rates.

6. Early Withdrawal Penalties: If you need access to your funds before the CD matures, you may face early withdrawal penalties. These penalties can eat into your potential earnings and diminish the overall benefits of the CD.

7. Lack of Flexibility: CDs are rigid in terms of account management and flexibility. Once you open a CD, you typically cannot make additional contributions or change the term or interest rate. This lack of flexibility can limit your ability to adapt your savings strategy to changing circumstances.

It’s important to carefully consider the disadvantages of CDs in relation to your financial goals and needs. If liquidity, potential alternative investment opportunities, or flexibility are important to you, then CDs may not be the most suitable option.

Despite these drawbacks, CDs can still serve as a valuable tool for those seeking stable returns and low-risk investments. Assessing your individual circumstances and weighing the pros and cons will help you determine if CDs align with your overall financial strategy.

Considerations Before Opening a CD Account

Before opening a Certificate of Deposit (CD) account, it’s essential to consider several factors to ensure that it aligns with your financial goals and needs. Here are some key considerations to keep in mind:

1. Financial Goals: Clarify your financial goals and determine if a CD fits into your overall strategy. Are you saving for a short-term goal, such as a vacation or down payment, or a long-term goal, like retirement? Understanding your goals will help you select an appropriate CD term and rate.

2. Liquidity Needs: Assess your liquidity needs before committing to a CD. CDs typically have limited liquidity, meaning you may face penalties or restrictions if you need to access your funds before the CD matures. Ensure that you have sufficient funds available for emergencies or unexpected expenses outside of the CD.

3. Time Horizon: Consider your time horizon and how long you can comfortably lock up your money in a CD. Longer-term CDs generally offer higher interest rates, but they tie up your funds for an extended period. Shorter-term CDs provide more flexibility but may have lower interest rates.

4. Interest Rates: Research and compare interest rates offered by different financial institutions. While interest rates can vary, it’s important to balance the desire for higher returns with the level of risk you’re willing to take. Consider the current market rates and any potential changes in interest rates before committing to a CD.

5. Penalties and Terms: Familiarize yourself with the terms and conditions of the CD, including any penalties for early withdrawal. Understand the specific terms of the CD, such as compounding frequency, interest payout options, and renewal terms. Read the fine print to avoid any surprises or misunderstandings.

6. CD Insurance: Verify that the financial institution offering the CD is FDIC-insured (for banks) or NCUA-insured (for credit unions) to ensure the safety of your funds. This insurance provides protection for your deposits up to the insured limit, typically $250,000 per depositor per institution.

7. Alternatives: Explore alternative investment options and compare their potential returns, risk levels, and liquidity. Consider whether a CD is the best fit for your needs, or if other investments, such as stocks, bonds, or mutual funds, may better align with your financial goals and risk tolerance.

By carefully considering these factors, you can make an informed decision when opening a CD account. Evaluating your financial goals, liquidity needs, time horizon, interest rates, terms, and alternatives will help ensure that a CD is the right choice for you.

How to Open a CD Account

Opening a Certificate of Deposit (CD) account is a straightforward process, but there are a few steps to follow. Here’s a guide on how to open a CD account:

1. Research and Compare: Start by researching different financial institutions and comparing their CD offerings. Look for competitive interest rates, terms, and any additional features or benefits that may be important to you.

2. Choose the Type and Term: Select the type of CD that best aligns with your financial goals and risk tolerance. Consider the term length that suits your needs, whether it’s a short-term CD of several months or a long-term CD that spans multiple years.

3. Gather Required Information: Compile the necessary documents and information to open the CD account. This typically includes your identification documents (such as a driver’s license or passport), social security number, and proof of address.

4. Select the Financial Institution: Decide on the financial institution where you want to open the CD account. This could be a bank, credit union, or online financial institution. Consider factors such as reputation, customer service, and convenience of branch locations or online accessibility.

5. Visit the Institution or Apply Online: Depending on your preference and the institution’s options, either visit a local branch or apply online to open the CD account. Online applications are convenient and can often be completed from the comfort of your own home.

6. Complete the Application: Follow the instructions provided by the financial institution to complete the CD account application. Provide all necessary information accurately and thoroughly to ensure a smooth application process.

7. Deposit Funds: Once your application is approved, you will be required to deposit funds into the CD account. Some institutions may have minimum deposit requirements, so ensure you’re aware of the amount needed before opening the account.

8. Confirm Account Details: Review the account details, including the term length, interest rate, and any special features of the CD. Make sure you understand the terms and conditions, including any penalties for early withdrawal or renewal options.

9. Manage and Monitor the CD: After successfully opening the CD account, stay on top of the account by monitoring its progress and reviewing account statements. Take note of the maturity date and any upcoming deadlines, such as the option to renew or close the CD.

Opening a CD account is a relatively simple process, but it’s essential to choose the right financial institution and terms that align with your financial goals. Understanding the steps involved will help ensure a smooth application and ultimately help you achieve your savings objectives.

Using CDs for Financial Goals

Certificates of Deposit (CDs) can be a valuable tool in achieving various financial goals. Whether you’re saving for a short-term expense or looking to grow your wealth over the long term, CDs offer several benefits. Here’s how you can use CDs to help achieve your financial goals:

1. Emergency Fund: CDs can serve as a safe and easily accessible emergency fund. By keeping a portion of your savings in a short-term CD, you can earn a higher interest rate than a regular savings account while still having the flexibility to access your funds in case of unexpected expenses.

2. Short-Term Savings Goals: If you have a specific short-term savings goal, such as purchasing a car, planning a wedding, or taking a dream vacation, opening a CD with a term that aligns with your timeframe can be beneficial. You’ll earn interest on your savings while keeping the funds safely locked away until you’re ready to use them.

3. Down Payment for a Home: Saving for a down payment on a home can be a significant financial milestone. Opening a CD with a longer-term horizon can help you earn a higher interest rate and grow your savings over time. This disciplined approach can bring you closer to achieving your goal of homeownership.

4. Retirement Planning: While CDs may not offer the same level of growth as riskier investments like stocks or mutual funds, they can still play a role in retirement planning. Utilizing long-term CDs within an Individual Retirement Account (IRA) can provide a secure and stable way to grow your retirement savings with tax advantages.

5. Education Savings: CDs can be utilized as a part of your strategy for saving for education expenses, such as college tuition. By opening CDs with staggered maturity dates, you can create a “laddering” system, allowing access to funds at various intervals while maximizing interest earnings.

6. Supplementing Income: Retirees or individuals seeking additional income can use CDs to generate regular interest payments. By staggering the maturity dates of multiple CDs, you can create a continuous stream of interest income that can supplement your other sources of income.

When using CDs for financial goals, it’s important to consider the term length, interest rate, and liquidity needs. Assess your specific goals, time horizon, and risk tolerance to determine the most suitable CD strategy for your needs.

Remember that while CDs offer stability and security, they may not provide the same level of growth as other investment options. It’s essential to strike a balance between the potential return and the level of risk that aligns with your financial objectives.

By incorporating CDs into your financial planning, you can take advantage of their benefits to help you reach your short-term and long-term financial goals.

Conclusion

Certificates of Deposit (CDs) offer a secure and reliable way to save and grow your money. They provide guaranteed returns, low-risk investment opportunities, and flexible terms to suit various financial goals. By understanding what CDs are and how they work, you can make informed decisions about adding them to your financial strategy.

CDs come with their advantages, such as guaranteed returns, stability, and potential tax benefits. They are particularly beneficial for individuals seeking low-risk investments, diversification, and steady income. However, it’s crucial to consider the disadvantages, such as limited liquidity, potential opportunity costs, and lower yields compared to higher-risk investments.

Before opening a CD account, carefully consider your financial goals, liquidity needs, and time horizon. Research different financial institutions, compare interest rates, and understand the specific terms and penalties associated with the CD. By doing so, you can ensure that a CD aligns with your overall financial strategy and goals.

In summary, CDs provide individuals with a safe and stable avenue to save and grow their money. Whether you’re looking to supplement your income, save for short-term expenses, or plan for long-term financial goals, CDs offer a valuable tool to accomplish these objectives. By combining sound financial planning, strategic use of CDs, and diversification across various investment vehicles, you can build a strong financial foundation and secure your financial future.