Introduction

Welcome to the world of personal finance! When it comes to managing your money, two commonly used terms are investments and savings. While both play an important role in building wealth and securing a financial future, they are not interchangeable. Understanding the key differences between investments and savings is crucial for making informed decisions about your financial goals and strategies.

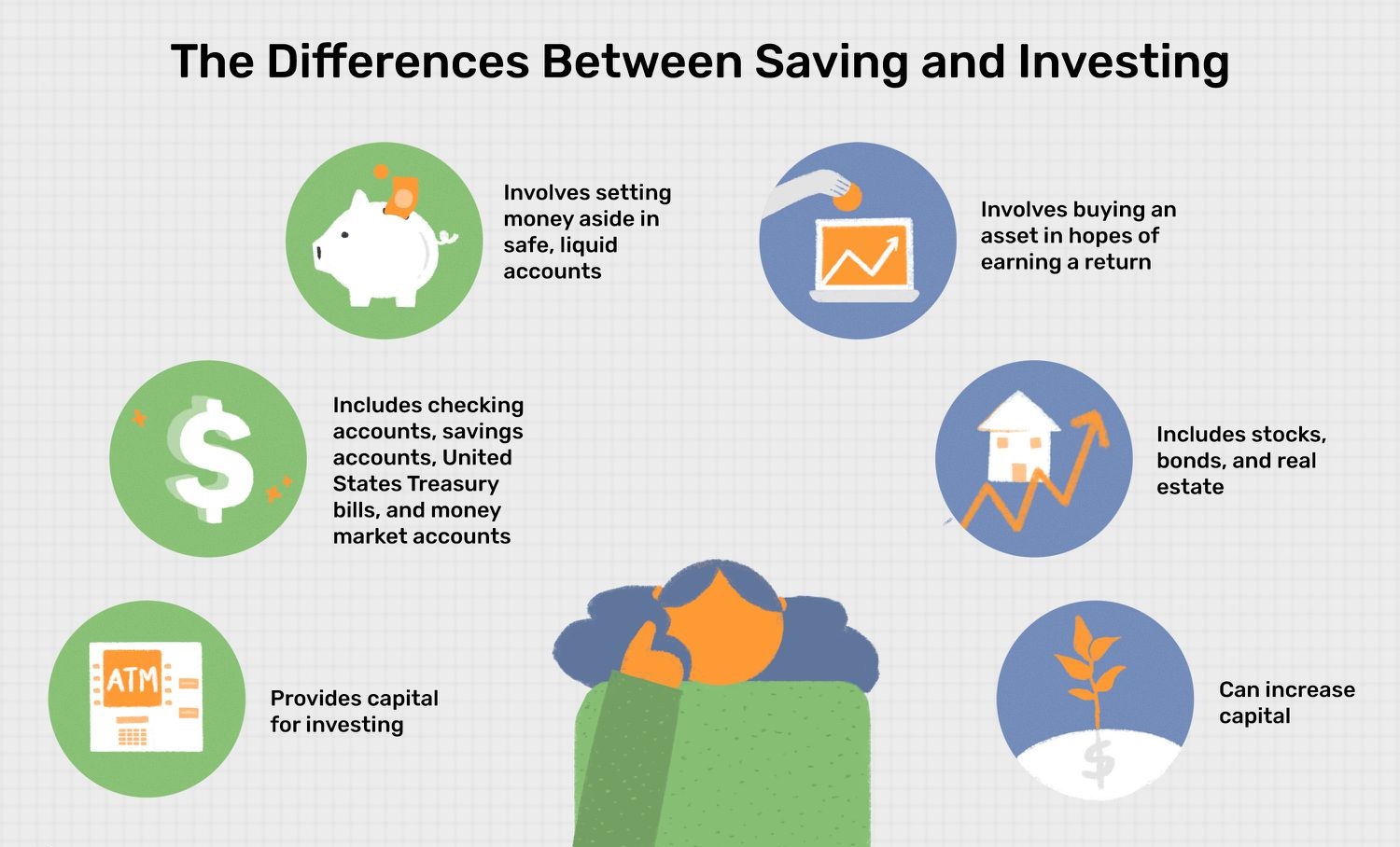

Simply put, savings refer to the money you set aside in a secure and easily accessible account, usually a savings account or a certificate of deposit (CD). The primary purpose of savings is to provide a safety net for emergencies or unexpected expenses.

On the other hand, investments involve putting your money into various assets with the intention of generating a return over time. This could include buying stocks, bonds, real estate, or even starting a business. The goal of investments is to grow your wealth and potentially earn a higher return compared to traditional savings accounts.

While savings and investments differ in their objectives, there are several key factors that distinguish the two:

Definition and Purpose

Savings are typically held in low-risk and easily accessible accounts, such as a savings account or a money market account. The purpose of saving is primarily to preserve capital and have funds readily available for short-term needs or emergencies. Savings accounts usually offer a lower interest rate compared to investments but come with minimal risk. The main goal of saving is to protect your money and maintain its value over time.

Investments, on the other hand, involve committing funds to assets with the expectation of generating a higher return over the long term. The purpose of investing is to grow your wealth and achieve financial goals such as retirement, purchasing a home, or funding your children’s education. Unlike savings accounts, investments carry a certain level of risk, as the value of the assets can fluctuate based on market conditions. However, higher risk generally offers the potential for higher returns.

The key difference between savings and investments lies in their earning potential. With savings, your funds earn interest, usually at a fixed rate, which helps offset inflation and maintains your purchasing power. While the interest earned on savings might be minimal, the principal amount remains secure.

Investments, on the other hand, have the potential for greater returns but also carry the risk of losses. The returns from investments can come in different forms, such as dividends from stocks, interest income from bonds, or capital gains from selling assets at a higher price than what was initially paid. The purpose of investments is to generate income or capital gains over time, potentially outperforming the rate of inflation and helping you build wealth.

In summary, savings provide a secure way to store your money and have it readily available for short-term needs, while investments are focused on growing your wealth over the long term. Both have their place in a well-rounded financial strategy, and understanding their definitions and purposes is pivotal in making informed decisions about managing your funds.

Risk and Return

When it comes to savings and investments, one of the crucial factors to consider is the relationship between risk and return. In general, the higher the potential return, the higher the level of risk involved.

Savings accounts are known for their low risk. The funds deposited in a savings account are typically insured by the government up to a certain limit, such as the FDIC insurance in the United States. While savings accounts offer stability and guarantee the preservation of your capital, the returns are relatively modest. The interest rates on savings accounts are typically lower than inflation rates, meaning your purchasing power could slowly erode over time.

Investments, on the other hand, carry varying levels of risk depending on the asset class. Stocks, for example, are considered riskier than bonds or real estate. The value of stocks can fluctuate greatly due to market conditions, company performance, and other external factors. However, with higher risk comes the potential for higher returns. Historically, stocks have provided higher average long-term returns compared to savings accounts or bonds.

Diversification can play a crucial role in managing risk within investments. By diversifying your investment portfolio across different asset classes and geographic regions, you can potentially reduce the impact of any one investment performing poorly. This strategy aims to balance the risk and return by spreading your investments across a range of assets.

It’s important to note that risk tolerance varies from person to person based on their financial situation, goals, and comfort level with uncertainty. Before making any investment decisions, it’s advisable to assess your risk tolerance and consult with a financial advisor who can help guide you towards suitable investments that align with your risk appetite.

Overall, while savings accounts offer stability and low risk, investments have the potential to provide higher returns but carry a level of risk. Understanding your risk tolerance and finding the right balance between risk and return are crucial considerations when deciding how to allocate your financial resources.

Liquidity

Liquidity is another important factor that sets savings and investments apart. Liquidity refers to how quickly and easily an asset or investment can be converted into cash without significant loss in value.

Savings accounts are highly liquid. You can access your funds at any time, either by withdrawing cash from an ATM or transferring money electronically. Most savings accounts do not have restrictions or penalties for accessing your funds, allowing you to use them for immediate needs or emergencies.

Investments, on the other hand, can vary in terms of liquidity. Some investments, such as stocks and exchange-traded funds (ETFs), are considered highly liquid as they can be bought and sold on stock exchanges during market hours. You have the flexibility to sell your investments and convert them into cash relatively quickly.

Other investments, like real estate or certain types of bonds, may have lower levels of liquidity. Selling such assets can take longer, and you may need to find a buyer who is willing to purchase the asset at a fair market price. Additionally, there may be fees or penalties associated with selling certain investments before a specified time, such as early withdrawal penalties for certificates of deposit (CDs) or surrender charges for annuities.

It’s essential to consider the liquidity of your investments based on your financial needs. If you anticipate needing funds in the short term, allocating a portion of your savings to highly liquid assets can provide peace of mind and quick access to cash. Conversely, if you have a longer-term investment horizon and can afford to tie up your funds for an extended period, less liquid investments may offer higher potential returns.

Overall, savings accounts are generally more liquid than most investments. However, it is important to strike a balance between liquidity and potential returns based on your financial goals and needs.

Time Horizon

Time horizon refers to the length of time you plan to hold an investment or keep your savings untouched. It plays a crucial role in determining the most suitable approach for managing your finances.

When it comes to savings, the time horizon is typically short-term. Savings accounts are designed for holding money that you may need in the near future, such as for emergency expenses or short-term financial goals. The funds in a savings account are easily accessible and can be withdrawn at any time without incurring penalties or fees.

Investments, on the other hand, are usually geared towards long-term goals. The longer your time horizon, the more likely you are to weather short-term market fluctuations and benefit from the potential growth of your investments. Investments generally require a longer holding period to fully realize their earning potential.

For example, when saving for retirement, you typically have a long time horizon, often spanning decades. This extended timeline allows you to invest in assets that have the potential to grow significantly over time, such as stocks or real estate, despite short-term volatility. On the other hand, if you’re saving for a short-term goal like a down payment for a house in a few years, it may be more prudent to allocate those funds to a savings account or other low-risk, liquid investments.

Understanding your time horizon is important in determining the appropriate mix between savings and investments. If you have a longer time horizon, you may be more inclined to take on more risk and allocate a larger portion of your funds towards investments with higher growth potential. Conversely, a shorter time horizon calls for a more conservative approach, with a greater emphasis on preserving capital and maintaining liquidity.

It’s essential to reassess your time horizon regularly and adjust your savings and investment strategies accordingly. As your goals and time horizon change, you may need to rebalance your portfolio or reallocate your funds to align with your new objectives.

In summary, the time horizon plays a critical role in determining whether to allocate your funds to savings or investments. Short-term goals often call for readily accessible savings, while long-term goals offer the opportunity to take on more risk and potential growth through investments.

Taxation

Taxation is an important aspect to consider when comparing savings and investments. The way your savings and investments are taxed can have a significant impact on your overall returns.

When it comes to savings accounts, the interest you earn is generally subject to taxation. In many countries, the interest income from savings accounts is considered taxable income and must be reported on your annual tax return. The tax rate applied to this interest income depends on your income tax bracket. It’s important to note that some countries may offer specific tax advantages or exemptions for certain types of savings accounts, such as tax-free savings accounts (TFSA) or individual retirement accounts (IRA) in the United States.

Investments, on the other hand, have a more complex tax landscape. Different investment vehicles are subject to different tax rules, and the tax treatment can vary depending on factors such as the type of investment, the duration of the investment, and your country’s tax laws.

For example, stocks held for the long-term may be subject to capital gains tax when sold. The tax rate applied to the capital gains depends on the holding period and your income tax bracket. Dividends from stocks may also be subject to taxation, although some countries offer preferential tax rates on dividend income.

Bond investments may generate interest income, which is generally taxable. The tax treatment of bond income can vary depending on factors such as the type of bond (government, corporate, municipal), the duration of the bond, and your country’s tax laws.

Real estate investments have their own set of tax rules. Rental income from properties is typically subject to taxation, and depending on your country’s tax laws, you may be able to deduct certain expenses related to property ownership.

It’s crucial to consult with a tax professional or financial advisor who can guide you on the specific tax implications of your savings and investment strategies. They can help you maximize tax advantages, minimize tax liabilities, and ensure compliance with the tax regulations in your country.

In summary, savings accounts are generally subject to tax on the interest earned, while the taxation of investments varies depending on the type of investment and your country’s tax laws. Understanding the tax implications of your savings and investments is important for planning your finances and optimizing your after-tax returns.

Inflation

Inflation is the gradual increase in the prices of goods and services over time, resulting in the erosion of purchasing power. It is an important factor to consider when evaluating the impact of savings and investments on your financial well-being.

Savings accounts, while providing a safe place to store your money, often struggle to keep pace with inflation. The interest rates offered on savings accounts are typically lower than the rate of inflation. As a result, the real value of your savings may decrease over time. For example, if the inflation rate is 3% and your savings account is earning an interest rate of 1%, your purchasing power is effectively decreasing by 2% each year.

Investments, on the other hand, offer the potential to outpace inflation and preserve your purchasing power. Certain investments, such as stocks and real estate, have historically provided returns that surpass the rate of inflation over the long term. By investing in assets that have the potential for growth, you can increase the value of your investments and mitigate the impact of inflation.

It’s important to note that not all investments are guaranteed to outperform inflation. Some investments may be more susceptible to inflation risks, such as fixed-income investments like bonds. Inflation erodes the purchasing power of future bond payments, which can impact the overall return on investment.

When considering the impact of inflation on your savings and investments, it’s essential to take a long-term view. While short-term fluctuations in prices may occur, focusing on long-term investment strategies that have historically outpaced inflation can help you effectively combat the erosion of purchasing power. Additionally, regularly assessing and adjusting your investment mix can help ensure that you are positioned to take advantage of opportunities that arise in response to inflationary conditions.

In summary, inflation erodes the value of savings over time, while investments have the potential to outpace inflation and preserve purchasing power. By carefully selecting investments that historically demonstrate the ability to outperform inflation and regularly reviewing your investment strategy, you can minimize the impact of inflation on your long-term financial goals.

Conclusion

Understanding the differences between savings and investments is crucial for effective financial planning. Both play significant roles in building wealth, securing your financial future, and achieving your goals. By considering key factors such as risk and return, liquidity, time horizon, taxation, and inflation, you can make informed decisions on how to allocate your funds.

Savings accounts provide a secure and easily accessible way to set aside money for short-term needs or emergencies. They offer stability and preserve capital, but the returns may be minimal, and they may struggle to keep up with inflation over time.

Investments, on the other hand, involve putting your money into various assets with the long-term goal of generating higher returns. While investments carry varying levels of risk, they have the potential to outpace inflation and grow your wealth over time. However, investments may be less liquid, subject to taxation, and require careful consideration of risk tolerance and time horizon.

Ultimately, finding the right balance between savings and investments depends on your individual financial goals, risk tolerance, time horizon, and liquidity needs. Assessing your financial situation, consulting with professionals, and regularly reviewing your financial strategy are essential to ensure that you are making the most of your savings and investments.

In summary, savings and investments serve different purposes and offer unique advantages. A well-rounded financial strategy may incorporate both, with savings providing stability and liquidity for short-term needs, and investments offering growth potential and the ability to outpace inflation over the long term. By understanding these differences and making informed decisions, you can work towards achieving your financial goals and securing a prosperous future.