Introduction

When it comes to managing your finances, finding ways to reduce your tax liability is always a smart move. One effective strategy is taking advantage of tax deductions, which can help lower your taxable income and potentially boost your overall savings. While there are many deductions available, one area worth exploring is tax-deductible investments.

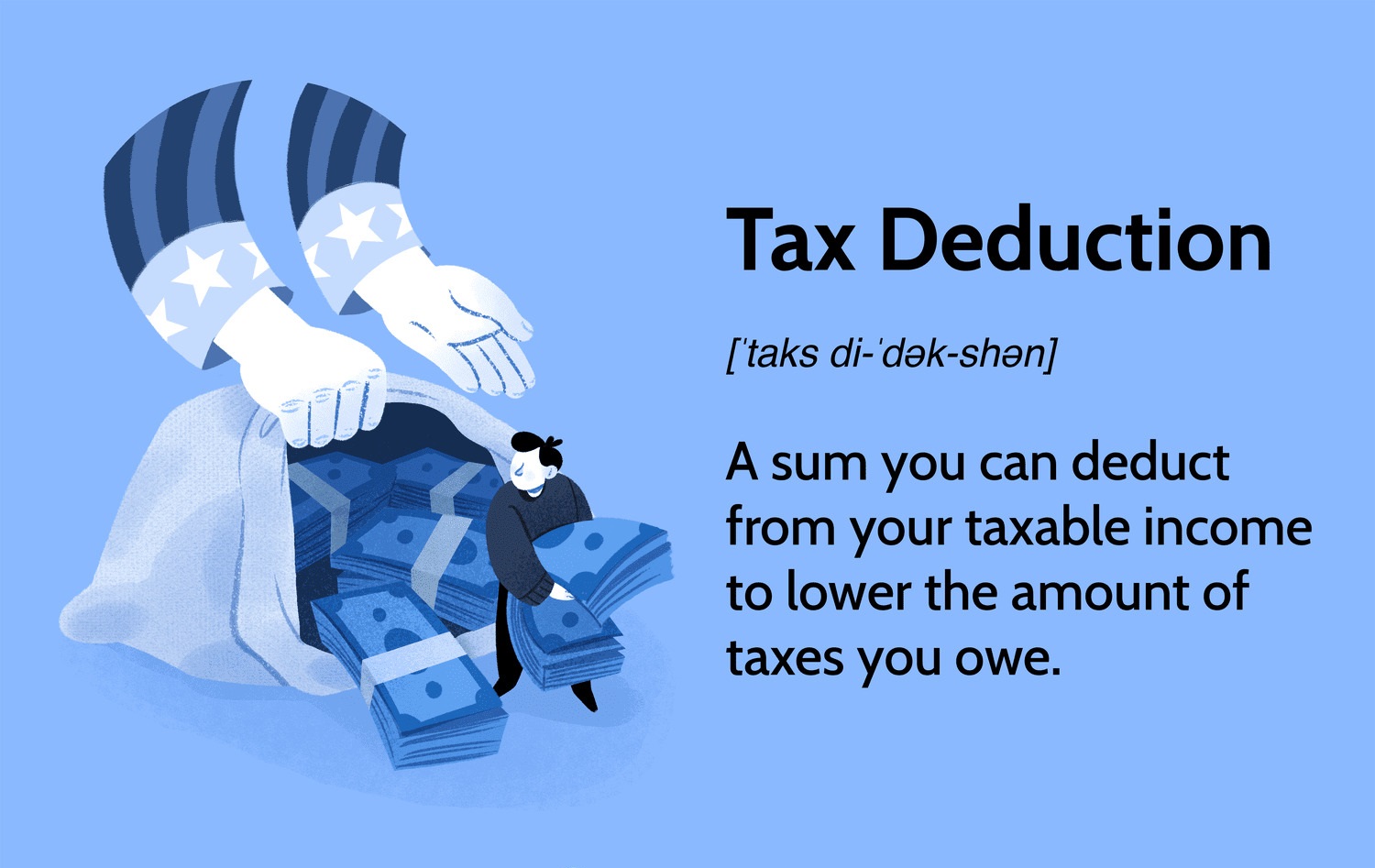

A tax deduction is a provision in the tax code that allows you to reduce your taxable income by subtracting certain eligible expenses or investments. By doing so, you can potentially lower the amount of income taxes you owe. Tax-deductible investments are investments that offer the advantage of reducing your taxable income and ultimately decreasing your tax liability.

Understanding which investments are tax deductible is key to maximizing your tax benefits. Whether you’re planning for retirement, funding your child’s education, or exploring other investment opportunities, being aware of the tax deductions available can make a significant difference in your financial planning. In this article, we will explore various types of tax-deductible investments that can help you optimize your tax savings.

What is a Tax Deduction?

A tax deduction is a financial benefit provided by the government that allows individuals and businesses to lower their taxable income. It serves as a way to incentivize certain behaviors or stimulate economic growth by providing a reduction in the amount of taxes owed to the government.

When you claim a tax deduction, you are essentially reducing your taxable income by subtracting eligible expenses or investments from your total earnings. The lowered taxable income results in a reduction in the amount of income tax you owe, potentially leading to significant savings. It’s important to note that tax deductions are different from tax credits, which directly reduce the amount of tax owed.

To take advantage of tax deductions, you must meet specific criteria and document your eligible expenses or investments. This may require keeping thorough records, such as receipts, statements, or documentation from qualified organizations. It’s crucial to understand the requirements for each deduction and ensure you meet the necessary criteria to claim them.

It’s also important to note that tax deductions can vary depending on the tax laws of your country or jurisdiction. Therefore, familiarizing yourself with the specific tax regulations and seeking professional advice can help you make the most of available deductions.

By strategically utilizing tax deductions, you can lower your taxable income, potentially reduce the amount of taxes owed, and optimize your overall financial situation. Understanding how tax deductions work and which expenses or investments qualify can help you make informed decisions and improve your financial planning.

Types of Tax Deductible Investments

There are various types of tax-deductible investments that offer opportunities for individuals and businesses to lower their taxable income. These investments can range from retirement accounts to energy-efficient home improvements. Understanding the different options available can help you make informed financial decisions and maximize your tax savings. Let’s explore some of the most common types of tax-deductible investments:

- Retirement Accounts: Contributions to certain retirement accounts, such as a traditional IRA or a 401(k) plan, are often tax-deductible. These contributions can reduce your taxable income and help you save for retirement.

- Education Savings Accounts: Investments made in education savings accounts, such as a 529 plan or a Coverdell Education Savings Account (ESA), can provide tax benefits. Contributions to these accounts may be eligible for a tax deduction, and withdrawals used for qualified education expenses can be tax-free.

- Health Savings Accounts: Health Savings Accounts (HSAs) offer individuals with high-deductible health insurance plans an opportunity to save for medical expenses on a tax-free basis. Contributions to an HSA are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

- Real Estate Investments: Investing in real estate can offer tax benefits such as mortgage interest deductions, property tax deductions, and depreciation deductions. These deductions can help reduce taxable income and provide potential savings.

- Small Business Investments: Certain investments made in a small business or startup may be eligible for tax deductions. For example, investments in a Qualified Small Business (QSB) can provide tax benefits like the Qualified Small Business Stock (QSBS) exclusion, which allows for the exclusion of capital gains upon selling eligible stock.

- Energy-Efficient Home Improvements: Making energy-efficient upgrades to your home, such as installing solar panels or energy-efficient windows, may qualify for tax credits or deductions. These deductions can help offset the cost of the improvements and promote environmental sustainability.

- Charitable Contributions: Donations made to qualified charitable organizations can be tax-deductible. Keeping records of your charitable contributions and itemizing them on your tax return can help lower your taxable income.

- Investment Expenses: Some investment-related expenses, such as fees paid to financial advisors or custodial fees, may be tax-deductible. These deductions can help offset the costs associated with managing your investments.

It’s important to note that the specific rules and eligibility criteria for tax-deductible investments can vary. Consulting with a tax professional or financial advisor can provide personalized advice tailored to your unique financial situation.

Retirement Accounts

Retirement accounts are a popular type of tax-deductible investment that offer individuals the opportunity to save for their future while enjoying potential tax benefits. Contributions made to certain retirement accounts can be tax-deductible, which can reduce your taxable income and potentially lower your tax liability.

One common retirement account that offers tax benefits is a traditional Individual Retirement Account (IRA). Contributions made to a traditional IRA are often tax-deductible, meaning you can deduct the contributed amount from your taxable income for the year in which you made the contribution. The IRS sets annual contribution limits for traditional IRAs, and individuals who are not covered by an employer-sponsored retirement plan may be eligible for a full tax deduction. For those who are covered by a retirement plan at work, the deductibility of IRA contributions may be limited based on their income level.

Another retirement account that provides tax advantages is an employer-sponsored retirement plan, such as a 401(k) or 403(b) plan. Contributions made to these plans are typically made on a pre-tax basis, meaning they are deducted from your income before taxes are calculated. This reduces your taxable income for the year and allows you to defer paying taxes on the contributed amount until you make withdrawals from the account in retirement.

By contributing to a tax-deductible retirement account, you not only save for your future but also enjoy immediate tax benefits. The deducted amount lowers your taxable income, potentially resulting in a lower tax bill. Additionally, the earnings within the account can grow tax-deferred until you withdraw them during retirement, allowing for potential tax savings in the long run.

It’s important to keep in mind that there are rules and regulations surrounding withdrawals from retirement accounts. Withdrawals before a certain age may be subject to early withdrawal penalties and taxes. It’s advisable to consult with a financial advisor or tax professional to understand the specific guidelines and make informed decisions regarding your retirement savings and tax deductions.

Education Savings Accounts

Education savings accounts are a valuable tool for parents and guardians looking to save for their child’s education expenses. These accounts provide tax advantages and allow individuals to set aside funds specifically for education-related costs. Contributions made to education savings accounts, such as a 529 plan or a Coverdell Education Savings Account (ESA), may be eligible for a tax deduction.

A 529 plan is a tax-advantaged savings plan designed specifically for education expenses. These plans are offered by states or educational institutions and allow individuals to contribute funds that can grow tax-free. While contributions to a 529 plan are not tax-deductible at the federal level, many states offer tax deductions or credits for contributions made to these accounts. The specific tax benefits vary by state, so it’s important to review the rules and regulations of your state’s 529 plan.

On the other hand, a Coverdell Education Savings Account (ESA) is a tax-advantaged account that allows individuals to save for qualified education expenses from kindergarten through college. Contributions to a Coverdell ESA are not tax-deductible at the federal level, but they can grow tax-free. However, there are income eligibility limits for contributing to a Coverdell ESA, and the maximum annual contribution limit is $2,000 per beneficiary.

By contributing to an education savings account, you have the opportunity to reduce your taxable income and save for education expenses simultaneously. Whether you choose a 529 plan or a Coverdell ESA, it’s important to evaluate the specific tax benefits and eligibility criteria associated with each account type.

When it comes time to use the funds from an education savings account, withdrawals used for qualified education expenses are usually tax-free. This includes tuition, fees, books, supplies, and even certain room and board expenses. However, it’s important to review the specific guidelines and restrictions set forth by each account to ensure compliance and maximize the tax benefits.

When considering education savings accounts, it’s advisable to consult with a financial advisor or tax professional who can provide personalized guidance based on your financial goals and circumstances. They can help you understand the potential tax deductions and navigate the various education savings account options available to you.

Health Savings Accounts

Health Savings Accounts (HSAs) are tax-advantaged accounts designed to help individuals with high-deductible health insurance plans save for medical expenses. Contributions made to an HSA are typically tax-deductible, providing a valuable opportunity to lower your taxable income and potentially reduce your tax liability.

To be eligible for an HSA, you must have a high-deductible health insurance plan, as defined by the IRS. High-deductible health plans have higher deductibles and lower premium costs compared to traditional health insurance plans. HSA contributions can be made by both the individual and their employer, and the total amount contributed is subject to annual limits set by the IRS.

The tax benefits of an HSA extend beyond the initial contribution. The funds within an HSA can grow tax-free, and withdrawals used for qualified medical expenses are also tax-free. Qualified medical expenses include a wide range of healthcare costs, such as doctor visits, prescription medications, hospital expenses, and certain medical supplies.

One unique aspect of HSAs is that the funds can be carried over from year to year, offering an opportunity for long-term savings and accumulation. Unlike flexible spending accounts (FSAs) that impose a “use it or lose it” rule, unused HSA funds can be carried over and continue to grow tax-free indefinitely, even if you change health insurance plans or retire.

Additionally, individuals age 55 or older can make catch-up contributions to their HSA, allowing them to save even more for healthcare expenses as they near retirement.

Health Savings Accounts are a valuable tool for managing healthcare costs and saving for future medical expenses. The tax-deductible contributions reduce your taxable income, the funds grow tax-free, and withdrawals used for qualified medical expenses are tax-free. However, it’s important to note that non-qualified withdrawals may be subject to income tax and potential penalties.

As with any tax-advantaged account, it’s recommended to consult with a financial advisor or tax professional to fully understand the benefits, limitations, and eligibility requirements of a Health Savings Account. They can help you make informed decisions regarding contributions, investment options, and potential tax savings.

Real Estate Investments

Real estate investments can provide both financial returns and tax benefits. Investing in real estate can offer various tax deductions that can help lower your taxable income and potentially reduce your overall tax liability.

One common tax deduction associated with real estate investments is the deduction for mortgage interest. If you have a mortgage on a rental property or a second home, the interest you pay on that mortgage may be tax-deductible. This deduction can significantly reduce your taxable income and provide savings on your annual tax bill.

In addition to the deduction for mortgage interest, property owners can also deduct property taxes paid on their real estate investments. Property taxes can be a significant cost for real estate owners, but the ability to deduct these expenses can help offset the financial burden.

Another tax benefit of real estate investments is the potential for depreciation deductions. Over time, the value of a property can depreciate due to wear and tear or obsolescence. The IRS allows property owners to deduct a portion of this depreciation as an expense on their tax returns. This depreciation deduction can help decrease taxable income and increase cash flow from the property.

Investing in real estate also opens up possibilities for other deductions, such as repairs and maintenance expenses, property management fees, and insurance costs. These deductions can reduce the taxable income generated by your real estate investment and provide additional savings.

It’s important to note that the rules and regulations surrounding real estate tax deductions can be complex. Rental properties, in particular, have specific guidelines and requirements. It’s advisable to consult with a tax professional or real estate expert who can guide you through the intricacies of real estate tax deductions and ensure compliance with tax laws.

Real estate investments offer not only the potential for financial growth but also tax advantages that can enhance your overall investment strategy. By taking advantage of tax deductions related to mortgage interest, property taxes, depreciation, and other associated expenses, you can optimize your real estate investment and maximize your tax savings.

Small Business Investments

Investing in a small business can offer not only the potential for financial growth but also tax benefits. Certain investments made in a small business or startup can be eligible for tax deductions, providing opportunities to lower your taxable income and potentially reduce your tax liability.

One significant tax advantage for small business investments is the Qualified Small Business Stock (QSBS) exclusion. Under certain conditions, investors who purchase qualified small business stock may be able to exclude a portion of their capital gains from taxable income. This exclusion can provide substantial tax savings for those who invest in eligible small businesses.

In addition to the QSBS exclusion, small business investors may also benefit from deductions related to business expenses. If you invest in a small business or startup and actively participate in its operations, you might be able to deduct certain expenses related to the business. These deductions can include travel expenses, office supplies, professional fees, and more.

Furthermore, if your small business investment results in a loss, you may be able to deduct the loss against other income. This deduction can help offset taxes owed on other sources of income, potentially reducing your overall tax liability.

It’s important to note that small business investment tax deductions can have specific requirements and limitations. The IRS has guidelines on what qualifies as a small business and the eligibility criteria for various deductions. Seeking advice from a tax professional or accountant who is well-versed in small business investments can ensure you take advantage of all available tax benefits while complying with tax regulations.

Investing in a small business offers the potential for financial gain, and the tax benefits associated with these investments can further enhance the overall return on investment. By understanding and utilizing the available tax deductions, you can optimize your tax savings and make your small business investment even more financially rewarding.

Energy-Efficient Home Improvements

Investing in energy-efficient home improvements not only helps contribute to a greener environment but can also offer tax benefits. Making certain upgrades to your home that improve its energy efficiency can potentially qualify you for tax credits or deductions, resulting in savings on your tax bill.

The federal government and some state governments offer tax incentives for energy-efficient home improvements. One example is the Residential Energy Efficient Property Credit, which provides a tax credit for certain renewable energy systems installed in your home, such as solar panels or wind turbines. This credit allows you to offset a percentage of the costs of the qualifying renewable energy systems and potentially save on your taxes.

In addition to tax credits, energy-efficient home improvements may also qualify for tax deductions. For example, the Non-Business Energy Property Tax Credit allows you to claim a deduction for the installation of qualifying energy-efficient improvements, such as energy-efficient windows, insulation, or HVAC systems. The deduction can reduce your taxable income for the year and potentially lead to tax savings.

It’s important to note that the specific tax incentives and eligibility criteria for energy-efficient home improvements can vary by jurisdiction and change over time. Consulting with a tax professional or researching the applicable tax laws in your area can help you identify the available incentives and determine whether your planned upgrades qualify for tax savings.

Before making energy-efficient home improvements, it’s advisable to keep detailed records of the expenses, including receipts and installation documentation. These records will be necessary to support your tax credits or deductions when filing your tax return.

Investing in energy-efficient home improvements not only helps save on energy costs but also offers potential tax advantages. Taking advantage of available tax credits and deductions can provide financial incentives to make environmentally-friendly upgrades to your home.

Charitable Contributions

Contributing to charitable organizations not only allows you to support causes you care about but can also provide valuable tax benefits. Charitable contributions made to qualified organizations may be tax-deductible, offering an opportunity to lower your taxable income and potentially reduce your overall tax liability.

When making charitable contributions, it’s important to ensure that the organization is recognized by the IRS as a qualified tax-exempt entity. Qualified organizations can include nonprofit organizations, charities, religious institutions, educational institutions, and more.

One option for deducting charitable contributions is itemizing deductions on your tax return. By itemizing, you can deduct the total amount of your qualifying charitable donations from your taxable income. It’s essential to keep proper documentation of your contributions, such as receipts, acknowledgment letters, or donation statements, to support your deduction claims.

The tax deduction for charitable donations can be a significant incentive for individuals to contribute generously. Additionally, certain donations, such as appreciated stocks or property, may offer additional tax advantages. When donating appreciated assets, you may be able to deduct the fair market value of the asset, while avoiding capital gains tax on the appreciation.

It’s worth noting that there are limitations on the deductibility of charitable contributions. The IRS sets specific percentage limits on the amount you can deduct based on your adjusted gross income (AGI). Consulting with a tax professional can help you navigate these limitations and optimize your deductions.

Remember that the true spirit of charitable giving is to support causes and organizations that align with your values and goals. While tax benefits may be a motivating factor, prioritize the impact you can have through your contributions and choose reputable organizations that are doing meaningful work.

By making charitable contributions, you not only help make a difference in the world but also have the opportunity to lower your taxable income and potentially reduce your tax liability. Understanding the guidelines for deducting charitable contributions and staying organized with proper documentation can ensure that you maximize these tax benefits.

Investment Expenses

Investing in financial markets often comes with associated expenses, but the good news is that some of these expenses may be tax-deductible. Deducting investment expenses can help lower your taxable income, potentially reducing your overall tax liability.

Investment expenses that may be eligible for deductions can include fees paid to financial advisors, custodial fees, subscription fees for investment publications, and certain legal and accounting fees related to your investments. These deductions can be particularly beneficial for individuals who actively manage their investment portfolios and incur various expenses in the process.

It’s important to note that investment expenses can only be deducted if they exceed a certain threshold. The IRS allows deductions for investment expenses that exceed 2% of your adjusted gross income (AGI). Therefore, it’s important to keep track of the costs associated with your investments and ensure that they meet the threshold for deductibility.

When claiming investment expense deductions, it’s crucial to keep thorough records and maintain proper documentation. This may include invoices, receipts, and statements that clearly identify the nature and purpose of the expense. Having accurate records will be essential when substantiating your deductions in case of an audit or when filing your tax return.

It’s worth noting that investment expenses are classified as miscellaneous itemized deductions, which means they are subject to the phase-out rule. The phase-out rule reduces the overall amount of itemized deductions you can claim if your income exceeds a certain threshold. Understanding how the phase-out rule may impact your investment expense deductions can help you plan accordingly.

While investment expenses can be deductible, it’s important to evaluate the overall impact of these expenses on your investment returns. Consider the potential tax benefits in relation to the fees you incur and the performance of your investments. It’s advisable to consult with a financial advisor or tax professional to determine whether the deductions outweigh the costs and make informed decisions regarding your investment expenses.

By deducting eligible investment expenses, you can lower your taxable income and potentially reduce your tax liability. Keeping accurate records, understanding the deductible expenses, and seeking professional advice can help you maximize the tax benefits associated with your investment activities.

Conclusion

Understanding the various types of tax-deductible investments can be instrumental in maximizing your tax benefits and optimizing your overall financial planning. From retirement accounts to real estate investments, small business investments to charitable contributions, and energy-efficient home improvements to investment expenses, there are numerous avenues to explore for potential tax deductions.

By strategically utilizing tax deductions related to these investments, you can lower your taxable income, potentially reduce your tax liability, and ultimately enhance your financial situation. However, it’s important to familiarize yourself with the specific rules, regulations, and eligibility criteria for each deduction to ensure compliance and maximize your savings.

To navigate the complex landscape of tax-deductible investments, it’s advisable to seek the guidance of a financial advisor or tax professional. They can provide personalized advice based on your unique financial goals and circumstances, helping you make informed decisions and optimize your tax savings.

Remember, while tax deductions can provide significant benefits, it’s equally important to consider the financial merits and potential risks of any investment. Ensure that your investment decisions align with your long-term financial objectives and conduct thorough research before committing funds.

Ultimately, by understanding and harnessing the power of tax-deductible investments, you can improve your financial well-being, save on taxes, and pave the way for a more secure and prosperous future.