What are Tax Yield Investments?

Tax yield investments, also known as tax-efficient investments, are financial instruments that offer attractive returns while providing tax advantages for investors. These investments are designed to minimize the amount of taxes paid on generated income or capital gains. By taking advantage of various tax exemptions, deductions, or favorable tax treatment, tax yield investments can help investors maximize their after-tax returns.

One of the primary goals of tax yield investments is to reduce the tax burden on investment income, allowing investors to keep more of their earnings. These investments are particularly beneficial for individuals in higher tax brackets, as they can significantly lower their tax liability.

Tax yield investments come in various forms, including municipal bonds, real estate investment trusts (REITs), master limited partnerships (MLPs), treasury inflation-protected securities (TIPS), and tax-free money market funds. Each of these investment options has its own unique characteristics and tax advantages.

When considering tax yield investments, it is essential to be aware of the tax implications and benefits associated with each investment category. For example, municipal bonds are issued by state and local governments and offer tax-free interest income at the federal level. These bonds can be an attractive option for investors seeking tax-free income.

On the other hand, REITs are companies that own, operate, or finance income-generating properties. They offer tax advantages by distributing at least 90% of their taxable income to shareholders in the form of dividends, which are taxed at the shareholder’s individual tax rate. REITs can provide a steady income stream while offering potential tax benefits.

MLPs are publicly traded partnerships that are engaged in the production, transportation, storage, or processing of natural resources. They provide tax benefits by passing through the majority of their earnings to investors without being subject to corporate income tax. MLPs can offer high yields and tax advantages, but they also come with potential risks and complexities.

TIPS are government-issued bonds that protect investors against inflation by adjusting their principal value based on changes in the Consumer Price Index (CPI). The interest income from TIPS is subject to federal income tax, but the inflation adjustment is tax-deferred until the bonds are sold or mature. This can provide investors with a tax-efficient way to preserve purchasing power.

Tax-free money market funds invest in short-term, high-quality debt securities and seek to provide income exempt from federal income tax. These funds can be an attractive option for investors seeking stability, liquidity, and tax advantages.

Overall, tax yield investments offer the potential for attractive returns while minimizing the impact of taxes on investment income. However, it is crucial to evaluate each investment option carefully and consider factors such as risk tolerance, investment objectives, and tax implications before making any investment decisions.

Understanding Tax Yield

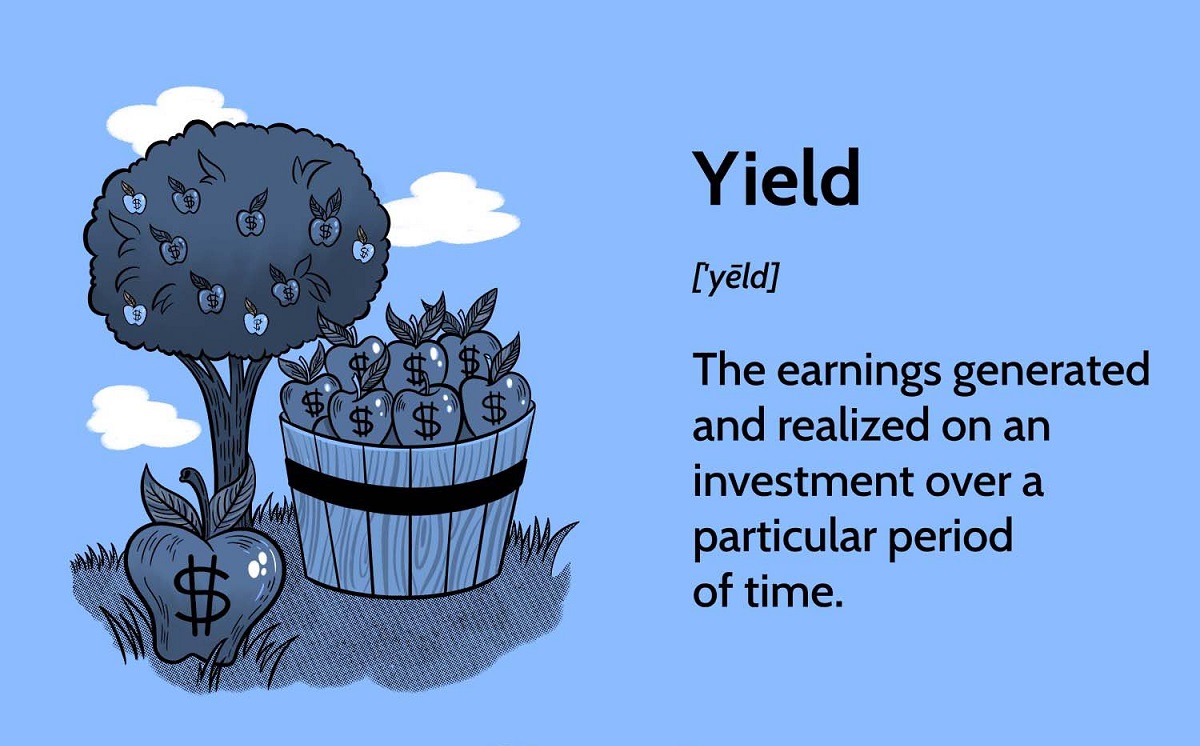

Tax yield is a measure of the after-tax income or returns generated by an investment. It takes into account the impact of taxes on investment earnings and provides investors with a clearer picture of their actual returns. By understanding tax yield, investors can make more informed decisions and optimize their investment strategies.

The calculation of tax yield involves considering the tax rates applicable to different types of income, such as dividends, interest, and capital gains. These rates vary depending on an individual’s tax bracket and the holding period of the investment. By factoring in the tax consequences, investors can assess the true profitability of an investment.

One of the primary reasons individuals invest in tax yield investments is to minimize the amount of taxes paid on investment income. These investments are designed to take advantage of various tax deductions, exemptions, or preferential tax treatment, allowing investors to retain a larger portion of their earnings. By reducing the tax burden, tax yield investments can enhance the overall return on investment.

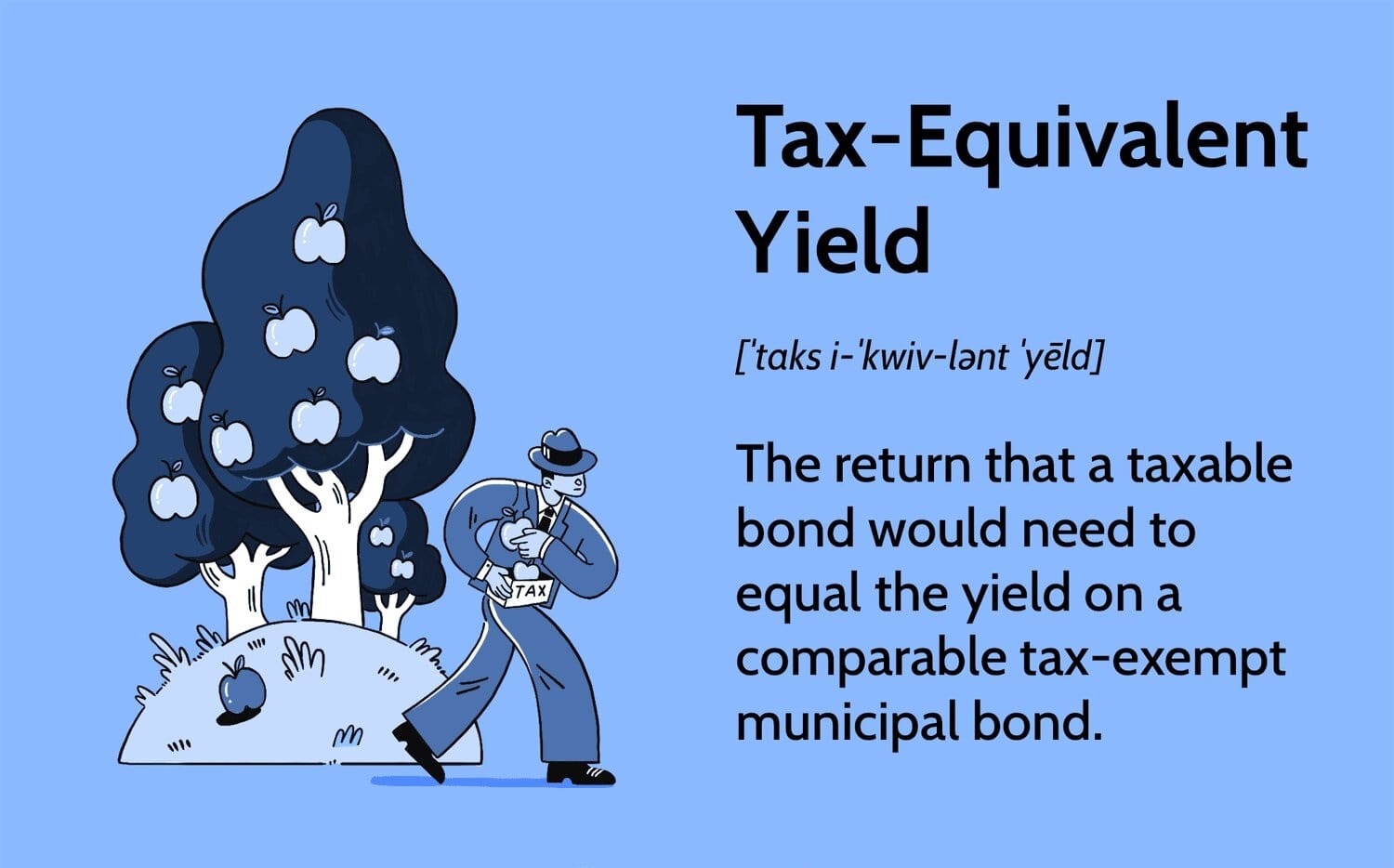

For example, let’s consider two investment options: a taxable bond and a tax-free municipal bond. The taxable bond offers an interest rate of 5%, while the tax-free municipal bond offers a slightly lower interest rate of 4%. At first glance, the taxable bond appears to provide a higher yield. However, when factoring in the impact of taxes, the tax-free municipal bond may actually yield a higher after-tax return. Depending on an individual’s tax bracket, the tax-free interest income from the municipal bond can outweigh the higher interest rate of the taxable bond, resulting in a higher tax yield.

It’s important to note that tax yield is just one aspect to consider when evaluating investment options. Other factors such as risk, liquidity, and investment objectives should also be taken into account. A high tax yield investment may come with higher risks or may not align with an individual’s investment goals. Therefore, it’s crucial to assess the overall suitability of an investment before making any decisions solely based on tax yield.

Additionally, tax laws and regulations may change over time. What may be considered a tax-efficient investment today may not hold the same advantages in the future. Staying informed about any changes to tax laws and consulting with a tax advisor can help investors make more informed decisions and adapt their investment strategies accordingly.

Understanding tax yield is essential for investors looking to optimize their after-tax returns. By considering the impact of taxes and evaluating the overall suitability of an investment, investors can make more informed decisions and potentially enhance their investment outcomes.

Types of Tax Yield Investments

There are several types of tax yield investments that offer attractive returns while providing tax advantages for investors. These investments are designed to minimize tax liabilities and enhance after-tax income. Below are some of the common types of tax yield investments:

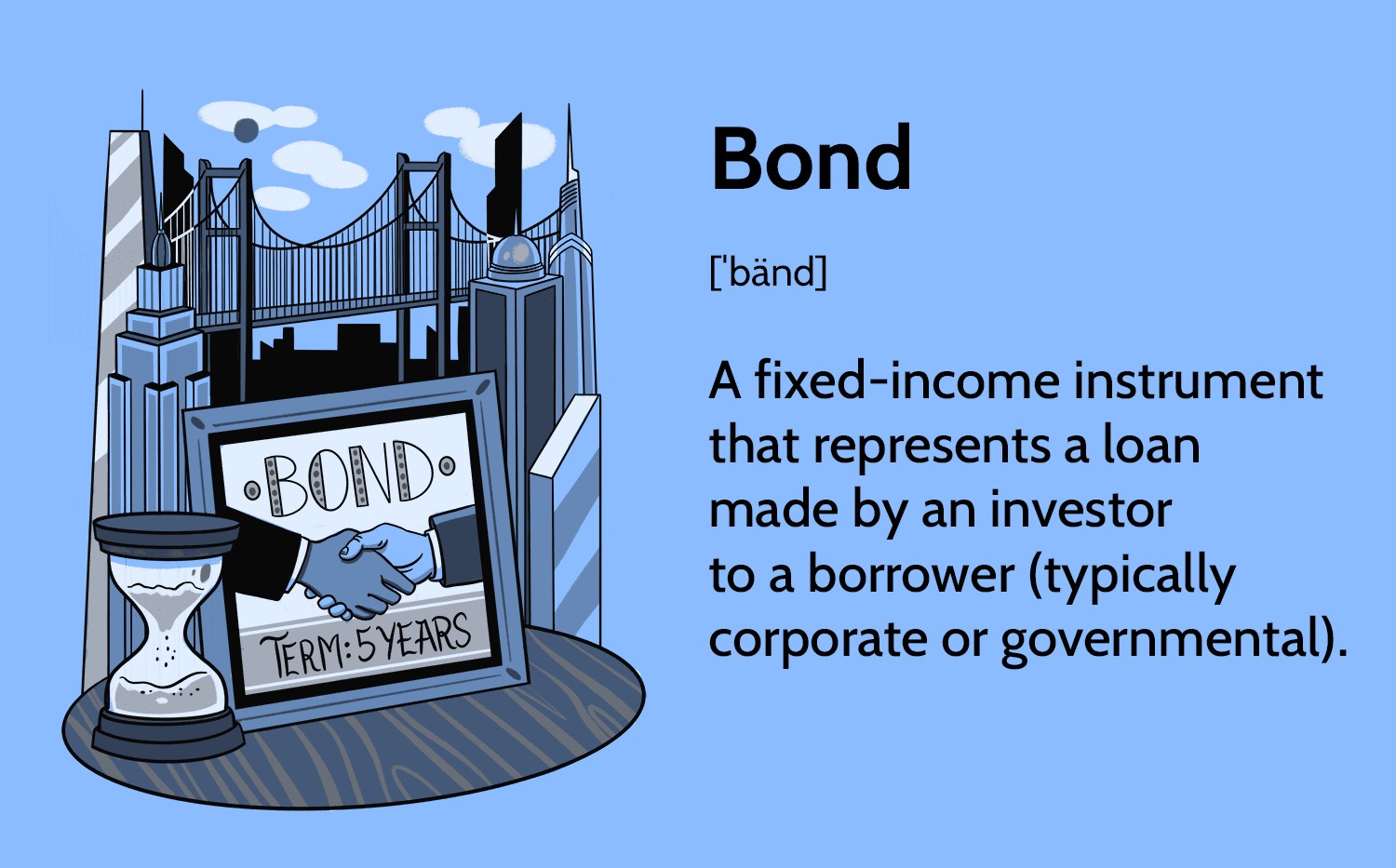

Municipal Bonds: Municipal bonds are issued by state and local governments to finance public projects such as infrastructure development. One of the main advantages of municipal bonds is that the interest income is typically exempt from federal taxes. In some cases, the interest may also be exempt from state and local taxes if the investor resides in the same state as the issuer.

Real Estate Investment Trusts (REITs): REITs are companies that own, operate, or finance income-generating real estate properties. These investment vehicles are required to distribute a significant portion of their taxable income to shareholders in the form of dividends. The distributions from REITs are generally taxable at the individual’s tax rate, but they may qualify for certain tax deductions or preferential tax treatment.

Master Limited Partnerships (MLPs): MLPs are publicly traded partnerships that primarily operate in the energy infrastructure sector. These entities pass through most of their income to investors and are not subject to corporate income tax. MLPs can offer attractive yields and potential tax advantages. However, they come with additional tax reporting complexities, and investors may be subject to certain tax implications upon the sale of MLP units.

Treasury Inflation-Protected Securities (TIPS): TIPS are government-issued bonds that provide protection against inflation. The principal value of TIPS is adjusted based on changes in the Consumer Price Index (CPI). While the interest income from TIPS is subject to federal income tax, the inflation adjustment is tax-deferred until the bonds are sold or mature. TIPS can be a tax-efficient investment option for those concerned about preserving purchasing power.

Tax-Free Money Market Funds: Tax-free money market funds invest in short-term, high-quality debt instruments. These funds seek to provide income that is exempt from federal income tax. Tax-free money market funds can offer stability, liquidity, and a potential tax advantage for investors in higher tax brackets.

It’s important to note that each type of tax yield investment comes with its own set of advantages and considerations. While these investments can offer potential tax benefits, investors should assess their risk tolerance, investment goals, and tax implications before making any investment decisions.

Furthermore, tax laws and regulations may change, which can impact the tax treatment of these investments. Staying informed and consulting with a tax professional can help investors navigate the complexity of tax yield investments and make informed decisions based on their individual circumstances.

Municipal Bonds

Municipal bonds, also known as munis, are debt securities issued by state and local governments to finance a wide range of public projects such as schools, roads, hospitals, and water treatment facilities. These bonds are considered a type of tax yield investment as they offer tax advantages for investors.

One of the primary advantages of municipal bonds is that the interest income generated from them is typically exempt from federal income tax. In certain cases, the interest income may also be free from state and local taxes if the investor resides in the same state as the issuer. This tax-exempt feature makes municipal bonds attractive to investors in higher tax brackets seeking to minimize their tax liabilities.

There are two main types of municipal bonds:

- General Obligation Bonds (GO Bonds): These bonds are backed by the taxing power of the issuing municipality or state. They are considered relatively safe investments as they have a low default risk. GO bonds are typically used to fund projects that benefit the entire community, such as schools or infrastructure improvements.

- Revenue Bonds: Revenue bonds are backed by the revenue generated from a specific project or source, such as toll roads, airports, or utilities. The repayment of these bonds depends on the success and revenue generation of the specific project. Revenue bonds may carry slightly more risk than GO bonds as their repayment is tied to the performance of the underlying project.

Municipal bonds come in various maturities, ranging from short-term (less than a year) to long-term (up to 30 years or more). The interest rates on municipal bonds are typically lower than those on taxable bonds issued by corporations or the federal government due to their tax advantages.

Investors can purchase municipal bonds directly from the issuing entity or through a broker. It’s important to note that while the interest income from municipal bonds is generally tax-free, any capital gains realized upon the sale of these bonds are subject to capital gains tax. Additionally, some municipals may be subject to the Alternative Minimum Tax (AMT), which can impact the tax treatment of the investment for certain individuals.

Before investing in municipal bonds, investors should carefully evaluate the creditworthiness of the issuing municipality or state. Credit ratings agencies assign ratings to municipal bonds based on the issuer’s ability to repay the debt. Higher-rated bonds carry lower default risk but may offer lower yields, while lower-rated bonds may offer higher yields but come with increased credit risk.

In summary, municipal bonds provide investors with a tax-efficient way to earn income while supporting essential public projects. By offering tax-exempt interest income, these bonds can help investors reduce their overall tax burden. However, it’s important to conduct thorough research, assess credit risk, and consider individual circumstances before investing in municipal bonds.

Real Estate Investment Trusts (REITs)

Real Estate Investment Trusts (REITs) are investment vehicles that own, operate, or finance income-generating properties. They offer investors an opportunity to invest in a diversified portfolio of real estate assets without the need for direct property ownership. REITs are considered tax yield investments as they provide tax advantages and potential steady income streams for investors.

One of the primary benefits of investing in REITs is their ability to distribute a significant portion of their taxable income to shareholders. REITs are required by law to distribute at least 90% of their taxable income in the form of dividends. These dividends are generally taxed at the individual’s tax rate, providing potential tax advantages for investors seeking regular income.

REITs can be classified into different categories based on the type of real estate assets they invest in:

- Equity REITs: These REITs primarily focus on owning and managing income-generating properties such as office buildings, shopping centers, apartments, and industrial facilities. Equity REITs derive their income from rental payments and capital appreciation of the underlying properties.

- Mortgage REITs: Mortgage REITs invest in real estate mortgages and mortgage-backed securities. They earn income from the interest and fees generated by these mortgage investments. Mortgage REITs can provide higher yields but may come with additional risks due to exposure to interest rate fluctuations and credit risk.

- Hybrid REITs: Hybrid REITs combine both equity and mortgage investments, providing exposure to both rental income and mortgage-related income streams. These REITs offer a balanced approach and the potential for diversification.

Investing in REITs can offer several advantages. First, REITs provide investors with an opportunity to participate in the income potential of real estate without the need for significant capital or direct property management responsibilities. Additionally, REITs offer liquidity, as their shares can be bought and sold on stock exchanges like any other publicly traded security.

However, it’s crucial to consider the risks associated with REIT investments. Real estate markets can be subject to fluctuations, and the performance of REITs may depend on factors such as property occupancy rates, rental rates, and overall economic conditions. Investors should assess the specific REIT’s track record, management expertise, and the quality of its real estate portfolio before making any investment decisions.

Lastly, it’s important to note that the tax treatment of REITs can vary depending on the individual’s tax situation. While the dividends received from REITs are generally taxed at the individual’s tax rate, they may qualify for certain deductions or preferential tax treatment. Consulting with a tax professional can provide guidance on the specific tax implications of investing in REITs.

In summary, REITs offer investors an opportunity to participate in the income potential of real estate while providing potential tax advantages. They can provide both income and diversification to investment portfolios. However, thorough research and due diligence are essential to understand the specific risks, potential returns, and tax implications associated with investing in REITs.

Master Limited Partnerships (MLPs)

Master Limited Partnerships (MLPs) are publicly traded partnerships that primarily operate in the energy infrastructure sector. They offer investors a unique investment opportunity to participate in the income generated by the production, transportation, storage, or processing of natural resources. MLPs are considered tax yield investments as they can provide tax advantages and the potential for attractive yields.

One of the key advantages of investing in MLPs is their tax structure. MLPs are structured as partnerships and are not subject to corporate income tax. Instead, they pass through the majority of their income to investors in the form of quarterly distributions. These distributions are generally taxed at the investor’s individual tax rate, potentially offering tax advantages for those in lower tax brackets.

Investing in MLPs can offer several potential benefits. First, MLPs tend to generate stable and predictable cash flows, as their operations are often tied to long-term contracts or regulated industries. This can provide investors with a steady income stream, making MLPs attractive for income-focused investors.

Another advantage of MLPs is their potential for high yields. Due to the pass-through structure, MLPs are required to distribute the majority of their income to investors. As a result, MLPs often offer higher yields compared to other traditional income investments.

However, it’s important to consider the risks associated with investing in MLPs. MLPs are subject to risks related to commodity price fluctuations, regulatory changes, and economic conditions. Additionally, MLPs can have complex tax reporting requirements, which may involve the filing of a Schedule K-1 tax form, and investors may be subject to unrelated business taxable income (UBTI) in certain circumstances.

Furthermore, MLP investments can have exposure to interest rate risk, as rising interest rates can impact the cost of borrowing for MLPs and affect their profitability. Investors should carefully assess the specific MLP’s financials, management expertise, industry trends, and risk factors before making any investment decisions.

Finally, it’s important to note that the tax treatment of MLP investments can vary depending on an individual’s tax situation. MLP distributions are generally considered a return of capital and can result in a reduction of the investor’s tax basis. This can have potential tax implications upon the sale of MLP units.

In summary, MLPs offer investors a unique opportunity to benefit from the income potential of energy infrastructure investments. They can provide tax advantages and attractive yields. However, investors should carefully evaluate the risks, tax implications, and suitability of MLP investments within their overall investment strategy.

Treasury Inflation-Protected Securities (TIPS)

Treasury Inflation-Protected Securities (TIPS) are government-issued bonds that provide investors with protection against inflation. These securities offer an opportunity to preserve purchasing power and maintain the real value of investments over time. TIPS are considered tax yield investments, as they can provide potential tax advantages and serve as a hedge against inflation.

One of the key features of TIPS is their inflation adjustment. The principal value of TIPS is adjusted based on changes in the Consumer Price Index (CPI), a measure of inflation. As the CPI rises, the principal value of TIPS increases, which provides investors with protection against the eroding effects of inflation.

While the principal value of TIPS is adjusted based on inflation, the coupon payments they provide are fixed. These payments are made semi-annually and are calculated based on the inflation-adjusted principal value. The interest income from TIPS is subject to federal income tax, but the inflation adjustment is not taxed until the bonds are sold or mature.

Investing in TIPS can offer several advantages. First, TIPS provide a measure of predictability and stability as the real value of the investment is protected against inflation. This can be particularly beneficial during periods of rising prices when traditional fixed-income investments may lose purchasing power.

Another advantage of TIPS is their potential tax efficiency. While the interest income from TIPS is subject to federal income tax, investors may be able to defer the tax on the inflation adjustment until the bonds are sold or mature. This can provide a tax-efficient way to preserve wealth and potentially reduce the overall tax burden on investment income.

However, it’s important to consider the potential risks associated with TIPS. TIPS are still subject to interest rate risk, meaning that their market value can fluctuate based on changes in interest rates. Additionally, the inflation adjustment may not fully protect against all forms of inflation, as it is based on the changes in the CPI, which may not capture the individual’s specific inflation experience.

When investing in TIPS, investors should carefully evaluate their investment objectives, risk tolerance, and investment horizon. TIPS can be purchased directly from the U.S. Treasury through auctions or in the secondary market through brokers.

Lastly, it’s important to note that the tax treatment of TIPS can vary depending on individual circumstances. Investors should consult with a tax professional to understand the specific tax implications of investing in TIPS.

In summary, TIPS offer investors a way to preserve purchasing power and protect against inflation. They provide potential tax advantages and can be a valuable addition to an investment portfolio, particularly for investors concerned about maintaining the real value of their investments over time.

Tax-Free Money Market Funds

Tax-free money market funds are investment vehicles that invest in short-term, high-quality debt securities, such as Treasury bills, municipal securities, and other tax-exempt instruments. These funds seek to provide investors with income that is exempt from federal income tax. Tax-free money market funds are considered tax yield investments, as they offer potential tax advantages while providing stability and liquidity.

One of the main advantages of tax-free money market funds is the exemption from federal income tax on the interest income. This tax advantage can be particularly beneficial for investors in higher tax brackets who are looking for ways to minimize their tax liabilities. By investing in tax-free money market funds, investors can earn income without having to include it in their taxable income for federal tax purposes.

Tax-free money market funds typically invest in short-term debt securities with maturities of less than one year. These securities are considered low-risk investments, as they are issued by government entities or highly rated institutions. The focus on high-quality debt instruments helps to preserve the principal value of the investment while providing a stable income stream for investors.

In addition to the potential tax advantages, tax-free money market funds offer other benefits. They provide liquidity, allowing investors to easily access their funds when needed. This makes them suitable for short-term cash management needs or as a safe haven for preserving capital while earning some income.

It’s important to note that while tax-free money market funds provide federal tax advantages, they may still be subject to state and local taxes, depending on the investor’s residency and the securities held by the fund. Investors should consider their individual tax situation and consult with a tax professional to understand the specific tax implications associated with investing in tax-free money market funds.

When considering tax-free money market funds, it’s also important to assess the fund’s expenses, past performance, and credit quality of the underlying assets. Investors should evaluate the fund’s management team, track record, and investment strategy to ensure alignment with their investment objectives and risk tolerance.

In summary, tax-free money market funds offer investors a tax-efficient way to earn income while preserving stability and liquidity. With their exemption from federal income tax, these funds can be especially attractive for individuals seeking to reduce their tax burden while maintaining easy access to their funds. However, investors should carefully consider their specific tax situation and evaluate various fund options before making any investment decisions.

Advantages of Tax Yield Investments

Tax yield investments offer several advantages for investors who are looking to maximize their after-tax income and minimize their tax liabilities. These investments can be a valuable addition to an investment portfolio. Here are some of the key advantages of tax yield investments:

1. Tax Efficiency: Tax yield investments are designed to optimize tax advantages and minimize the impact of taxes on investment income. By taking advantage of various tax exemptions, deductions, or favorable tax treatment, these investments help investors retain a larger portion of their earnings. This can result in higher after-tax returns compared to non-tax-advantaged investments.

2. Potential for Higher Returns: Tax yield investments can offer attractive returns, sometimes higher than traditional taxable investments. This is possible due to the tax advantages associated with these investments, which can enhance overall returns. By reducing the tax burden on investment income, tax yield investments help investors unlock the potential for higher net earnings.

3. Diversification: Tax yield investments come in various forms and asset classes, such as municipal bonds, real estate investment trusts (REITs), and master limited partnerships (MLPs). This diversity allows investors to diversify their portfolios and spread risk across different investment options. Diversification can help reduce overall portfolio risk and potentially enhance long-term returns.

4. Stability and Income: Many tax yield investments, such as municipal bonds and certain REITs, provide stable income streams. They often distribute regular dividends or interest payments, which can be particularly appealing for income-focused investors. These investments provide the potential for steady cash flow and can contribute to overall portfolio stability.

5. Hedging Against Inflation: Some tax yield investments, like Treasury Inflation-Protected Securities (TIPS), offer protection against inflation. These investments adjust their principal value based on changes in the Consumer Price Index (CPI), helping investors preserve their purchasing power in inflationary periods. By providing a hedge against inflation, tax yield investments can help maintain the real value of investments over time.

6. Flexibility and Liquidity: Many tax yield investments offer flexibility and liquidity for investors. These investments can be bought or sold on exchanges like stocks or redeemed directly from the issuer. This liquidity allows investors to access their funds whenever needed and provides flexibility in managing their investment portfolios.

7. Potential Tax-Free Income: Some tax yield investments, such as municipal bonds, offer tax-free interest income at the federal level. This can be particularly beneficial for investors in higher tax brackets who seek sources of tax-free income. Tax-free income can help reduce overall tax liabilities and increase the net return on investment.

Overall, tax yield investments provide a range of advantages that can enhance investors’ after-tax returns and overall portfolio performance. However, investors should carefully evaluate each investment option’s specific tax implications and consider their individual financial goals, risk tolerance, and tax situation before making any investment decisions.

Disadvantages of Tax Yield Investments

While tax yield investments offer several advantages, it’s essential to consider the potential disadvantages associated with these investment options. Here are some of the key disadvantages of tax yield investments:

1. Limited Accessibility: Some tax yield investments may have specific eligibility criteria or minimum investment requirements, making them less accessible to certain investors. For example, certain types of tax-free municipal bonds may be limited to residents of a particular state. Investors should carefully consider the accessibility of tax yield investments before making any commitments.

2. Specific Risks: Each tax yield investment comes with its own set of risks. For instance, municipal bonds may carry credit risk or interest rate risk. REITs may be affected by real estate market volatility or changes in interest rates. MLPs can have commodity price risk and specific regulatory risks. Investors should thoroughly assess the risks associated with each investment option and be aware of the potential fluctuations in income or capital values.

3. Complexity: Some tax yield investments, such as MLPs, can be complex in terms of tax reporting requirements and partnership structures. Investors may be required to deal with additional documentation, such as Schedule K-1 forms, when reporting their taxes. It is crucial for investors to understand the tax implications and complexities associated with each investment option.

4. Tax Law Changes: Tax laws and regulations can change over time, impacting the tax treatment of these investments. Changes in tax policies or legislation may affect the expected tax advantages of tax yield investments. Investors should stay informed about any potential tax law changes and consult with tax professionals to navigate the potential impact on their investments.

5. Volatility and Market Risk: Tax yield investments, like any other investment, are subject to market volatility and risks associated with the specific asset class or market segment. Changes in interest rates, economic conditions, or investor sentiment can impact the performance of these investments. Investors should be prepared for potential market fluctuations and price volatility.

6. Liquidity Constraints: Some tax yield investments, such as certain types of bonds or limited partnership interests, may have limited liquidity. Investors may face challenges in buying or selling these investments, especially during times of market stress or when there is a lack of willing buyers or sellers.

7. Potential Yield Trade-Offs: In certain cases, tax yield investments may offer lower nominal yields compared to similar taxable investments. While the tax advantages can enhance the after-tax returns, investors should carefully evaluate the potential yield trade-offs and compare the net returns of tax yield investments with their taxable counterparts.

Despite these potential disadvantages, tax yield investments can still be valuable components of a well-diversified investment portfolio. It’s important for investors to carefully consider their individual circumstances, risk tolerance, and investment goals before making any investment decisions.

Factors to Consider before Investing in Tax Yield Investments

Before investing in tax yield investments, it’s important to carefully consider several factors to ensure they align with your financial goals and risk tolerance. Here are some key factors to evaluate before investing in tax yield investments:

1. Investment Objectives: Assess your investment objectives to determine if tax yield investments are suitable for your financial goals. Consider whether your primary focus is income generation, capital preservation, long-term growth, or a combination of these factors. Aligning your investment objectives with the specific advantages and characteristics of tax yield investments is essential.

2. Risk Tolerance: Evaluate your tolerance for risk. Different tax yield investments carry varying levels of risk, such as credit risk, interest rate risk, or market volatility. Determine how comfortable you are with potential fluctuations in income or capital values and choose investments that align with your risk tolerance.

3. Tax Implications: Understand the tax implications of each investment option. Tax yield investments offer various tax advantages, but it’s crucial to assess how these advantages apply to your individual tax situation. Consider consulting with a tax professional to fully understand the potential tax benefits and implications of each investment.

4. Investment Time Horizon: Determine your investment time horizon. Some tax yield investments may have short-term characteristics, while others may require a longer-term commitment to fully benefit from their tax advantages or potential returns. Align your investment horizon with the specific characteristics and requirements of each investment option.

5. Research and Due Diligence: Conduct thorough research and due diligence on each investment option. Understand the fundamentals, historical performance, management team, and any associated risks. Review financial statements, prospectuses, and other relevant information to make informed investment decisions.

6. Diversification: Consider the importance of diversification in your investment portfolio. Evaluate how each tax yield investment option complements your existing holdings and helps in spreading risk across different asset classes and sectors. Diversification can potentially help reduce the overall risk in your portfolio.

7. Liquidity: Assess the liquidity of the investment. Some tax yield investments may have limited liquidity or longer lock-up periods, which may affect your ability to access your funds when needed. It’s important to evaluate whether the investment aligns with your liquidity needs and cash flow requirements.

8. Professional Advice: Consider seeking advice from financial advisors, tax advisors, or investment professionals with expertise in tax yield investments. They can provide guidance and help evaluate the suitability of each investment option based on your individual circumstances and financial goals.

9. Economic and Market Conditions: Evaluate the current economic and market conditions. Consider how factors such as interest rates, inflation expectations, and industry-specific trends may impact the performance of tax yield investments. Keeping an eye on the broader economic context can provide valuable insights.

By carefully considering these factors and conducting due diligence, you can make informed decisions when investing in tax yield investments. It’s important to regularly review your investments and adjust your portfolio as needed, given the evolving market and economic conditions.

Conclusion

Tax yield investments offer unique advantages to investors who are seeking to optimize their after-tax returns and minimize their tax liabilities. These investments, such as municipal bonds, REITs, MLPs, TIPS, and tax-free money market funds, provide potential tax advantages, income streams, stability, and diversification. However, it’s essential to carefully evaluate several factors before investing in tax yield investments.

Understanding investment objectives, risk tolerance, and tax implications is crucial. Investors should assess their investment time horizon, conduct thorough research, and consider the liquidity and diversification benefits of each investment option.

Additionally, staying informed about changes in tax laws and regulations is important as it can impact the tax treatment of these investments. Seeking professional advice from financial and tax advisors can provide valuable insights and help align tax yield investments with individual circumstances and financial goals.

Ultimately, tax yield investments can be a beneficial addition to an investment portfolio, offering potential tax advantages and attractive returns. However, investors should carefully assess the specific advantages and disadvantages of each investment option and make informed decisions based on their individual circumstances.

By considering these factors and conducting the necessary due diligence, investors can optimize their after-tax returns, potentially enhance their investment outcomes, and navigate the complexities of tax yield investments.