What is Tokenization?

Tokenization is a data security technique that is widely used in the payments industry to protect credit card information. It involves replacing sensitive data, such as the credit card number, with a randomly generated string of characters called a token. This token acts as a substitute for the actual card data and is used for transactions, storage, and any other processes that require the card information.

Unlike encryption, which uses complex algorithms to encode data and requires a decryption key to retrieve the original information, tokenization works through a process of mapping the token to the original data in a secure database called a token vault. The actual card data is stored securely in this vault, rendering the token meaningless to anyone who gains unauthorized access to it.

One of the key advantages of tokenization is that it greatly reduces the risk of exposing sensitive card information in the event of a data breach. Even if a malicious actor manages to access the tokenized data, they will only obtain the meaningless tokens rather than the actual card details. This makes tokenization an effective method for protecting customer data and safeguarding against fraud.

Tokenization is widely adopted by merchants, financial institutions, and payment processors, as it provides an added layer of security to credit card transactions. When a customer makes a purchase, their card information is substituted with a token, which is then sent through the payment network. At the receiving end, the token is mapped back to the original card data in the token vault, allowing the transaction to be authorized without exposing the sensitive information.

In addition to enhancing security, tokenization also offers convenience. With tokenized payments, customers can make purchases without having to enter their card information every time. This is particularly beneficial for recurring payments or when using mobile wallets, as it eliminates the need to share card details with multiple merchants, reducing the potential for data breaches.

In summary, tokenization is a powerful technique that replaces sensitive card information with randomly generated tokens, providing an additional layer of security to credit card transactions. It reduces the risk of data breaches, offers convenience by eliminating the need for repetitive data entry, and strengthens customer confidence in the security of their payment details.

The Benefits of Tokenization in Credit Cards

Tokenization in credit cards offers several benefits that enhance security, streamline transactions, and protect sensitive cardholder information. Here are some of the key advantages of tokenization:

- Enhanced Security: Tokenization replaces sensitive card data with randomly generated tokens, ensuring that customer information is protected. The actual card details are stored securely in a token vault, reducing the risk of data breaches and unauthorized access to sensitive information.

- Reduced Fraud Risk: Tokenization plays a crucial role in combating fraud. As tokenized data holds no value to cybercriminals, even if they manage to intercept the tokens, they cannot use them for malicious activities. This significantly reduces the risk of unauthorized transactions and fraudulent activities.

- Streamlined Payments: With tokenized credit cards, customers can enjoy seamless and convenient transactions. Once their card information is tokenized, they can use the tokens for subsequent purchases without the need to input their card details repeatedly. This simplifies the checkout process, making it faster and smoother for customers.

- Secure Storage: Tokenization allows for secure storage and transmission of cardholder data. The original card information is stored securely in the token vault, while the tokens are used for processing transactions. This ensures that sensitive data is protected at all times, offering peace of mind to both customers and businesses.

- Compliance with Data Regulations: Tokenization helps businesses comply with data protection regulations such as the Payment Card Industry Data Security Standard (PCI DSS). By replacing card data with tokens, organizations can reduce their scope of compliance, as sensitive information is no longer stored within their systems.

Overall, tokenization in credit cards helps to strengthen security, reduce fraud risk, streamline payment processes, and ensure compliance with data protection regulations. By leveraging tokenization, both businesses and customers can benefit from enhanced data security and improved transaction convenience.

The Process of Tokenization

The process of tokenization involves several steps to ensure the secure replacement of sensitive card data with tokens. Here’s an overview of the tokenization process:

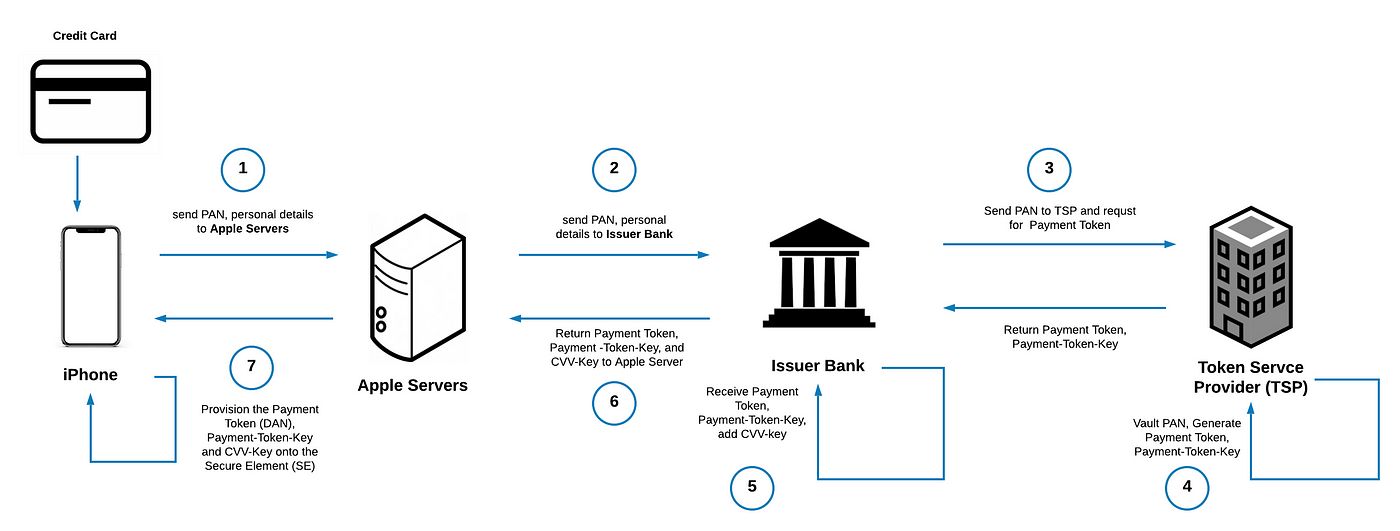

- Data Collection: When a customer initiates a transaction, their card information, including the credit card number, expiration date, and CVV, is collected by the merchant or payment processor. This data is considered highly sensitive and requires protection.

- Tokenization Request: The collected card data is sent to a tokenization service or solution, which generates a unique token to replace the card information. This token is a randomly generated string of characters that has no mathematical correlation to the original card data.

- Token Mapping: The token generated in the previous step is then mapped to the original card data in a secure database called a token vault. The actual card information is stored in this vault in an encrypted and protected format.

- Transaction Authorization: When a customer uses the tokenized card to make a subsequent transaction, the token is sent through the payment network. At the receiving end, the token is mapped back to the original card data in the token vault, allowing the transaction to be authorized without exposing the sensitive card details.

- Token Decryption: The authorized transaction is processed, and the payment is completed. Throughout this entire process, the card information remains securely stored in the token vault, ensuring the protection of sensitive customer data.

It’s important to note that tokenization maintains a one-to-one mapping between the token and the original card data, meaning that each token corresponds to a specific card. This ensures that the integrity of the data is maintained and allows for seamless retrieval of the original information when necessary.

Tokenization provides an added layer of security by ensuring that sensitive card data is never exposed during transactions or storage. Even if a data breach occurs, the stolen tokens are useless without access to the token vault and the encryption keys necessary to decrypt and retrieve the original card information.

Overall, the tokenization process involves data collection, token generation, token mapping, transaction authorization, and secure storage. By following these steps, businesses can protect sensitive cardholder data while facilitating secure and efficient payment transactions.

Types of Tokens Used in Credit Cards

Tokenization in credit cards utilizes different types of tokens to ensure the secure handling of sensitive cardholder data. Here are the common types of tokens used in credit card tokenization:

- Random Tokens: Random tokens are randomly generated strings of characters that have no mathematical correlation to the original card data. These tokens are unique for each transaction or card and are used to replace the actual card information, thereby protecting sensitive data from exposure.

- Persistent Tokens: Persistent tokens, also known as pseudonyms, are tokens that remain associated with a specific cardholder or account over time. These tokens can be used for recurring payments or for storing customer payment information securely for future transactions. Persistent tokens allow for convenient and seamless payments without the need to re-enter card details.

- Dynamic Tokens: Dynamic tokens, also referred to as dynamic card verification values (CVV), are temporary tokens assigned to a specific transaction. These tokens are often used for added security during online transactions. The dynamic token is generated at the time of the transaction and is valid only for that specific purchase.

- Format-Preserving Tokens: Format-preserving tokens maintain the same format and structure as the original card data, such as the same number of digits or specific patterns. These tokens retain the visual appearance of card data while replacing the sensitive information and can be used in systems that require specific data formats.

- Short-Lived Tokens: Short-lived tokens have a limited lifespan and are designed to be used for a specific time period or number of transactions. After the token expires or reaches its usage limit, it becomes unusable, adding an extra layer of security to the tokenized data.

Each type of token serves a specific purpose in credit card tokenization, allowing for secure transactions and protecting sensitive cardholder data. The choice of token type depends on factors such as the nature of the transaction, the need for persistence, and additional security requirements.

By implementing different types of tokens, businesses can tailor their tokenization approach to meet specific needs while maintaining the highest level of security. This ensures that sensitive card data is adequately protected throughout the payment process.

Tokenization vs. Encryption: What’s the Difference?

Tokenization and encryption are both methods used to protect sensitive data, but they differ in their approach and functionality. Here’s a comparison of tokenization and encryption in the context of credit card data:

1. Processing:

– Tokenization: Tokenization replaces sensitive card data with randomly generated tokens. The original card information is stored securely in a token vault, while the token is used for transaction processing and storage. Tokenization involves mapping the token back to the original data when necessary.

– Encryption: Encryption involves using complex algorithms to scramble the data and render it unreadable. Encrypted data requires a decryption key to decrypt and retrieve the original information. Encryption is reversible, meaning the encrypted data can be converted back to its original form with the proper decryption key.

2. Security:

– Tokenization: Tokenization provides an additional layer of security by replacing sensitive card data with tokens. As a result, even if the tokens are compromised, they hold no value and cannot be used for fraudulent activities. The actual card data is securely stored in the token vault.

– Encryption: Encryption protects data by converting it into an unreadable format that can only be deciphered with the correct decryption key. While encryption provides a high level of security, if the encryption key is compromised, it may render the data vulnerable to unauthorized access.

3. Data Protection:

– Tokenization: With tokenization, the sensitive card data is stored securely in a token vault, and the tokens are used for processing and storage. This reduces the risk of exposing the actual card information during transactions or storage, enhancing data protection.

– Encryption: Encryption protects data by transforming it into an unreadable format, ensuring that unauthorized individuals cannot access or understand the information. Encryption provides strong data protection during transmission and storage.

4. Reversibility:

– Tokenization: Tokenization is not reversible. Once the card data is tokenized, it cannot be reversed or converted back to its original form without access to the token vault and the corresponding encryption keys.

– Encryption: Encryption is reversible. With the correct decryption key, the encrypted data can be decrypted and converted back to its original format, allowing for the retrieval of the original information.

5. Compliance:

– Tokenization: Tokenization is often used to help businesses achieve compliance with data protection regulations, such as the Payment Card Industry Data Security Standard (PCI DSS). By tokenizing cardholder data, organizations reduce the scope of compliance and minimize the risk of data breaches.

– Encryption: Encryption is also commonly used to comply with data protection regulations. Implementing encryption ensures that sensitive data is secured and protected, meeting the requirements set forth by various compliance standards.

In summary, while both tokenization and encryption are effective methods for securing sensitive data, they differ in their approach and functionality. Tokenization replaces sensitive data with randomly generated tokens, ensuring that the actual card information remains protected and hidden. Encryption involves using complex algorithms to scramble the data, making it unreadable without the correct decryption key. Both methods offer additional layers of security and play essential roles in safeguarding sensitive information.

Tokenization in Mobile Wallets

The rise of mobile wallets has brought significant advancements in payment technology, and tokenization plays a crucial role in enhancing the security and convenience of mobile payment transactions. Here’s how tokenization is employed in mobile wallets:

1. Secure Storage of Card Information:

Mobile wallets, such as Apple Pay, Google Pay, and Samsung Pay, utilize tokenization to securely store users’ card information. When a user adds their credit or debit card to a mobile wallet, the card data is tokenized and stored securely on the device or in a cloud-based token vault. This ensures that the sensitive card details are protected both during storage and transmission.

2. Contactless Payments:

Tokenization enables the use of mobile wallets for contactless payments. Instead of sharing the actual card information during a transaction, the mobile wallet generates a unique token that represents the card data. This token is then used to authorize the payment, eliminating the need for physical card swiping or manual entry of card details. The tokenized transaction enhances security by preventing the exposure of sensitive card information to potential fraudsters.

3. Dynamic Tokens:

Mobile wallets often employ dynamic tokens for added security. Dynamic tokens are temporary tokens that are generated for each transaction. This means that every transaction made with a mobile wallet has a unique token, making it difficult for cybercriminals to intercept and misuse the tokenized data. Dynamic tokens enhance security by limiting the usability of stolen tokens and minimizing the risk of unauthorized transactions.

4. Simplified Checkout Experience:

Tokenization streamlines the checkout process for mobile wallet users. Once the card information is tokenized and securely stored, users can make purchases by simply authenticating themselves through biometrics or a PIN. The tokenized transaction details are sent from the mobile wallet to the payment processor or merchant, allowing for quick and convenient payments without the need to share actual card details or enter them manually.

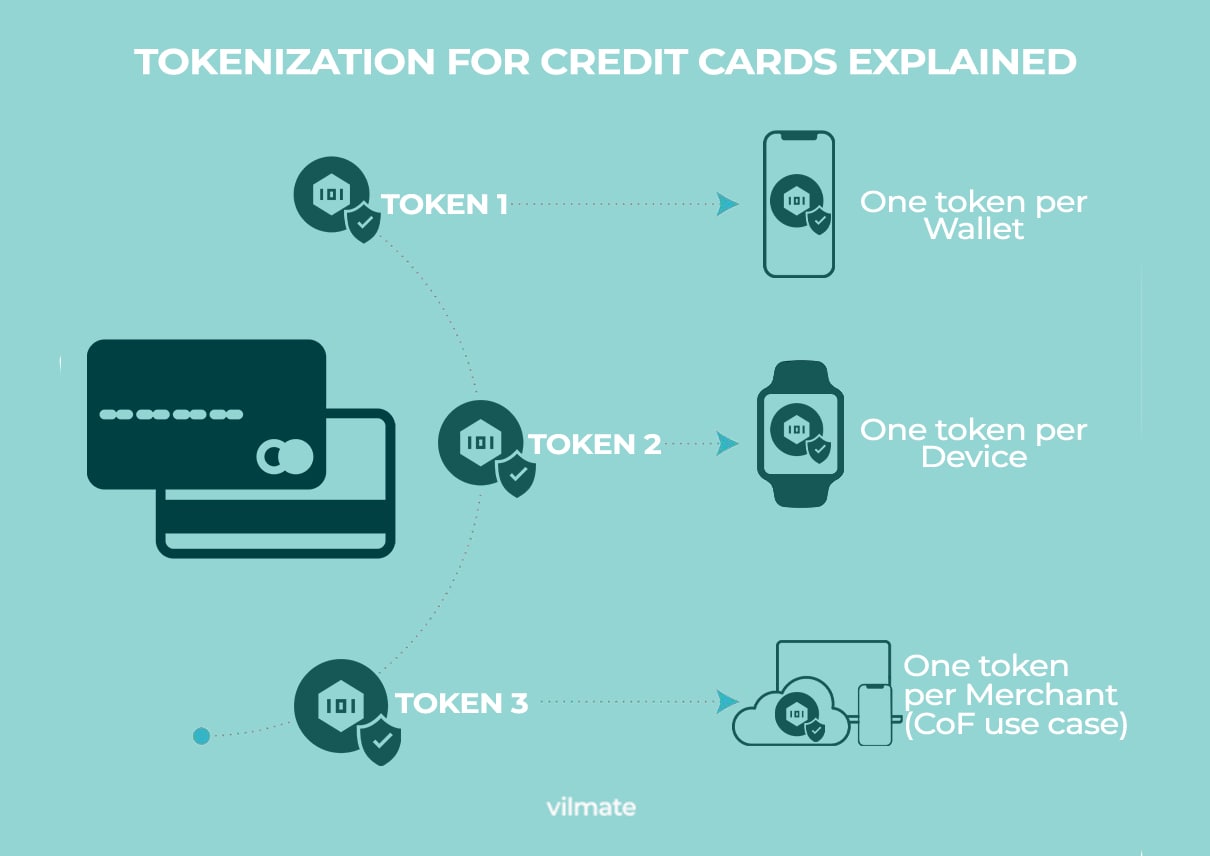

5. Multi-Platform Compatibility:

Tokenization in mobile wallets enables compatibility across different platforms and devices. Tokenized card information can be securely shared between devices, such as smartphones, tablets, and smartwatches, within the same mobile wallet ecosystem. This allows users to make payments using their preferred device without having to re-enter their card details.

6. Fraud Prevention:

Tokenization provides a robust defense against fraud in mobile wallets. Even if a cybercriminal gains access to the tokenized data, the tokens hold no value without access to the token vault and encryption keys. This significantly reduces the risk of unauthorized transactions and fraudulent activities, giving users peace of mind when using mobile wallets for payments.

In summary, tokenization is an essential technology that enhances the security and convenience of mobile wallet transactions. By tokenizing card information, mobile wallets provide secure storage, enable contactless payments, employ dynamic tokens for added security, simplify the checkout experience, ensure multi-platform compatibility, and aid in fraud prevention. As mobile payment technology continues to evolve, tokenization remains at the forefront of ensuring secure and seamless mobile transactions.

Tokenization and Contactless Payments

Tokenization plays a vital role in enabling secure and convenient contactless payments. Contactless payment methods, such as tap-and-go or wave-to-pay, utilize tokenization to enhance the security and speed of transactions. Here’s how tokenization and contactless payments work together:

1. Tokenized Transaction Data:

When a consumer initiates a contactless payment, their card information is tokenized. Instead of transmitting the actual card details, a unique token is generated to represent the card data. This token is used throughout the transaction process, ensuring that the sensitive card information remains protected.

2. Enhanced Security:

Tokenization enhances the security of contactless payments by preventing the exposure of actual card details. Tokens are random, unique strings of characters, and hold no intrinsic value to potential fraudsters. Even if a malicious actor intercepts the tokenized data during the payment process, they would be unable to use the tokens for unauthorized transactions.

3. Quick and Convenient Transactions:

Contactless payments powered by tokenization offer a faster and more convenient payment experience. Customers can simply tap or wave their tokenized payment method, such as a smartphone or a contactless card, on a compatible payment terminal, eliminating the need for physical card insertion or manual entry of card details. This speeds up the checkout process, reduces waiting times, and enhances overall customer convenience.

4. Dynamic Tokens for Enhanced Security:

Dynamic tokens are often employed in contactless payments to provide an additional layer of security. Dynamic tokens are temporary and are generated uniquely for each transaction. These tokens have limited validity and usage, further minimizing the risk of fraud. Utilizing dynamic tokens ensures that the tokenized data remains secure and reduces the chances of unauthorized transactions or fraudulent activities.

5. Protection Against Skimming Attacks:

Tokenization in contactless payments helps protect against skimming attacks, where criminals attempt to steal card information remotely. By replacing the sensitive card details with tokens, contactless payments add an extra layer of security. Even if a criminal intercepts the tokenized transaction data, they would not have access to the actual card information, significantly reducing the risk of card cloning or unauthorized use.

6. Cross-Compatible Contactless Payments:

Tokenization allows for cross-compatibility between various contactless payment methods and devices. Whether using a contactless card, a mobile wallet, or another tokenized payment method, the tokenized data can be securely transmitted and processed across different payment terminals. This interoperability provides flexibility for consumers and businesses, allowing them to choose their preferred contactless payment method.

Tokenization and contactless payments go hand in hand, providing a secure, convenient, and efficient payment experience. The utilization of tokenized data in contactless transactions enhances security, protects against fraud, ensures compatibility, and accelerates the adoption of contactless payment methods.

Tokenization and Fraud Prevention

Tokenization is a powerful tool in the fight against fraud, providing robust protection for sensitive cardholder data. By replacing actual card information with randomly generated tokens, tokenization offers several benefits for fraud prevention. Here’s how tokenization helps in mitigating fraud:

1. Ineffective Data for Cybercriminals:

Tokenization renders stolen data useless for cybercriminals. Even if they manage to obtain tokenized data, the tokens hold no intrinsic value, as they cannot be reversed or decoded without access to the token vault and encryption keys. This makes it extremely difficult for fraudsters to use stolen tokens in unauthorized transactions.

2. Improved Payment Card Security:

Tokenization significantly enhances the security of payment card data. By replacing sensitive card details with tokens, businesses reduce the risk of exposing actual card information during payment processing, storage, or transmission. This makes it difficult for fraudsters to intercept and exploit sensitive card data, reducing the chances of unauthorized transactions or fraudulent activities.

3. Dynamic Tokens:

Dynamic tokens, which are often used in tokenization, add an extra layer of security. These tokens are generated uniquely for each transaction or with a time limit, making them useless for fraudsters attempting to reuse stolen data. Dynamic tokens minimize the risk of token replay attacks and further strengthen the overall security of tokenized transactions.

4. Limiting Scope of Data Breaches:

Tokenization helps reduce the scope of data breaches. By tokenizing cardholder data, businesses can minimize the amount of sensitive information stored within their systems. Even if a data breach occurs, the stolen tokens hold no value without access to the token vault, limiting the potential damage that cybercriminals can cause.

5. Authentication and Authorization:

Tokenization can be combined with additional security measures, such as two-factor authentication or biometric verification, to enhance fraud prevention. By ensuring that only authorized users can complete transactions or access the token vault, tokenization adds an extra layer of protection against fraudulent activities.

6. Compliance with Security Standards:

Tokenization helps businesses comply with industry security standards and regulations, such as the Payment Card Industry Data Security Standard (PCI DSS). Implementing tokenization ensures that sensitive cardholder data is protected and helps meet the requirements for secure handling and storage of payment information.

Tokenization is a powerful tool in the fight against fraud. By replacing actual card information with tokens, tokenization makes stolen data useless, improves payment card security, utilizes dynamic tokens for added security, limits the impact of data breaches, strengthens authentication and authorization, and aids businesses in complying with security standards. With tokenization, businesses can effectively protect customer data and reduce the risk of fraudulent transactions.

Tokenization in E-commerce

Tokenization plays a critical role in enhancing security and protecting sensitive customer data in the realm of e-commerce. With the constant growth of online shopping, tokenization is increasingly adopted by e-commerce platforms and businesses. Here’s how tokenization is utilized in the context of e-commerce:

1. Secure Payment Transactions:

Tokenization ensures secure payment transactions in e-commerce. When customers enter their card information during the checkout process, the card details are immediately replaced with randomly generated tokens. This ensures that the sensitive card data is not stored or transmitted in its original form, reducing the risk of data breaches or unintended exposure.

2. Protection of Customer Data:

Tokenization safeguards customer data in e-commerce by keeping the actual card information secure. The tokens, which are stored in a secure token vault, hold no intrinsic value to potential attackers. Even if the tokens are compromised, they cannot be used to extract the original card details, ensuring the protection of sensitive customer information.

3. Streamlined Checkout Experience:

Tokenization simplifies the checkout process in e-commerce, making it quicker and more convenient for customers. Once the card information is tokenized, customers can choose to save the tokenized payment method for future purchases, eliminating the need to re-enter card details for subsequent transactions. This streamlines the checkout experience, reduces friction, and improves customer satisfaction.

4. Improved Conversion Rates:

Tokenization can contribute to higher conversion rates in e-commerce. By reducing the need for customers to repeatedly enter their card details, tokenization simplifies the payment process. This results in a smoother and more seamless checkout experience, enhancing customer trust and increasing the likelihood of completed transactions.

5. Enhancing Payment Security:

Tokenization significantly bolsters payment security in e-commerce. By tokenizing sensitive card data, businesses minimize the risk of unauthorized access to customer information and reduce the chances of fraudulent activity. Customers can shop with confidence, knowing that their payment details are protected within the tokenization process.

6. Compliance with Regulations:

Tokenization aids e-commerce businesses in complying with industry regulations and standards, such as the Payment Card Industry Data Security Standard (PCI DSS). By tokenizing cardholder data, businesses can reduce the scope of compliance, as sensitive information is not stored within their systems. This helps demonstrate a commitment to data security and protect customers’ privacy.

In summary, tokenization plays a crucial role in e-commerce by providing secure payment transactions, protecting customer data, streamlining the checkout experience, improving conversion rates, enhancing payment security, and facilitating compliance with industry regulations. By adopting tokenization in e-commerce, businesses can ensure the safeguarding of customer information and provide a secure and seamless shopping experience.

Challenges and Limitations of Tokenization

While tokenization offers significant benefits for data security and fraud prevention, it also faces certain challenges and limitations. Understanding these challenges is crucial for businesses implementing tokenization. Here are some of the key challenges and limitations associated with tokenization:

1. Token Vault Management:

Managing the token vault, which stores the mapping between tokens and original card data, can be complex, especially for organizations with a large number of customers or transactions. Properly securing the token vault and ensuring its accessibility can be a challenge, requiring robust data management and governance practices.

2. Legacy System Compatibility:

Integrating tokenization with legacy systems can be challenging. Older systems may not be designed to accommodate tokenized data, requiring significant effort and investment to upgrade or replace outdated infrastructure. This can slow down the implementation of tokenization and hinder its adoption in certain business environments.

3. Tokenization Across Multiple Platforms:

Ensuring seamless tokenization across various platforms, such as mobile wallets, e-commerce platforms, and point-of-sale systems, can be a complex endeavor. Tokenization needs to be implemented consistently and securely across all platforms to maintain a unified and reliable payment process for customers.

4. Tokenization Costs:

Implementing tokenization may come with additional costs. Businesses need to invest in the necessary infrastructure, including secure token vaults, strong encryption technologies, and compliance measures. Ongoing maintenance and monitoring of the tokenization system may also require dedicated resources, further adding to the overall cost.

5. Third-Party Dependencies:

Businesses that rely on third-party tokenization services may face dependencies and potential vulnerabilities. Outsourcing tokenization must be done carefully, ensuring that the third-party provider follows strict security protocols and adheres to data protection regulations. Businesses must evaluate the trustworthiness and reliability of third-party service providers to mitigate risks.

6. Regulatory Compliance:

While tokenization assists with achieving compliance with data security standards, businesses must still ensure they meet all relevant regulatory requirements. Complying with industry-specific regulations, such as the Payment Card Industry Data Security Standard (PCI DSS), can be complex and necessitates ongoing monitoring and assessment to maintain compliance.

7. Tokenization Scope and Integration:

Tokenization is primarily focused on protecting payment card data. However, businesses must carefully consider other types of sensitive information, such as personally identifiable information (PII), that may also require protection. Tokenizing additional data elements requires proper integration with existing systems and processes.

In overcoming these challenges, it is essential for businesses to conduct due diligence, establish robust security measures, evaluate compatibility with legacy systems, and ensure compliance with relevant regulations. Despite these challenges, tokenization remains a powerful and proven method for protecting sensitive data and reducing the risk of fraud.

How Tokenization Enhances Card Security

Tokenization is a key technology that significantly enhances card security by protecting sensitive cardholder data. Here are the ways in which tokenization enhances card security:

1. Data Protection:

Tokenization replaces sensitive card information, such as the card number and expiration date, with randomly generated tokens. This ensures that the actual card details are not stored or transmitted in their original form, making it extremely difficult for hackers or unauthorized individuals to access and misuse the information.

2. Secure Storage:

Tokenization ensures the secure storage of sensitive card data. The original card information is stored within a token vault, which is typically encrypted and protected using industry-standard security measures. Storing the card data securely reduces the risk of data breaches and unauthorized access to the cardholder’s information.

3. Fraud Prevention:

Tokenization plays a significant role in preventing fraud and unauthorized transactions. Even if a cybercriminal gains access to the tokenized data, the tokens themselves hold no intrinsic value and cannot be used to complete fraudulent transactions. The lack of usable card information in the tokens acts as a strong deterrent to fraudsters.

4. Tokenization Scope:

Tokenization is often implemented on a per-transaction or per-card basis, reducing the scope of exposure for sensitive data. Each token generated is unique and tied to specific card details, preventing the broad compromise of cardholder information even in the event of a data breach. This containment limits the potential impact should the tokenized data be compromised.

5. Compliance with Security Standards:

Tokenization helps businesses comply with industry security standards, such as the Payment Card Industry Data Security Standard (PCI DSS). By implementing tokenization, businesses reduce the amount of sensitive card data within their systems, simplifying compliance efforts and reducing the risk of penalties due to non-compliance.

6. Streamlined Transactions:

Tokenization enables secure and streamlined transactions for cardholders. Once card data is tokenized, customers can complete transactions with merchants without sharing their actual card details. This eliminates the need for repetitive data entry and reduces the risk of sensitive information being compromised through manual input errors or exposures.

7. Consumer Trust:

Tokenization builds consumer trust in card security. By employing tokenization, businesses demonstrate a commitment to protecting their customers’ card information. This reassures cardholders that their data is being handled securely, leading to increased confidence in conducting transactions with the business.

Through data protection, secure storage, fraud prevention, compliance with security standards, streamlined transactions, and fostering consumer trust, tokenization significantly enhances card security. The implementation of tokenization helps to safeguard sensitive cardholder data and provides peace of mind to both merchants and cardholders when engaging in payment transactions.

Conclusion

Tokenization is a powerful data security technique that revolutionizes the protection of sensitive cardholder information, especially in the context of credit cards. By replacing actual card data with randomly generated tokens, tokenization enhances security, streamlines transactions, and reduces the risk of fraud in various applications, including e-commerce and mobile payments.

Through the process of tokenization, sensitive card details are securely stored in a token vault, while tokens are used for transactions and storage. This method protects cardholder data from being exposed or misused, even in the event of a data breach.

Tokenization offers numerous benefits, including enhanced security, reduced fraud risk, streamlined payments, secure storage of card information, compliance with data regulations, and compatibility with various payment platforms. These advantages make tokenization a valuable tool for merchants, financial institutions, and payment processors to protect customer data, build trust, and ensure compliance with industry standards.

However, it is important to recognize the challenges and limitations that come with tokenization, such as token vault management, legacy system compatibility, tokenization costs, third-party dependencies, regulatory compliance, and integration across platforms. Businesses must address these challenges to ensure the successful implementation and ongoing effectiveness of tokenization.

Overall, tokenization significantly enhances card security by replacing sensitive card information with tokens, reducing the risk of data breaches and protecting cardholder data from unauthorized access. As technology advances and the importance of data security continues to grow, tokenization remains a powerful technique in safeguarding sensitive information, enabling secure transactions, and instilling customer confidence in the payment process.