Introduction

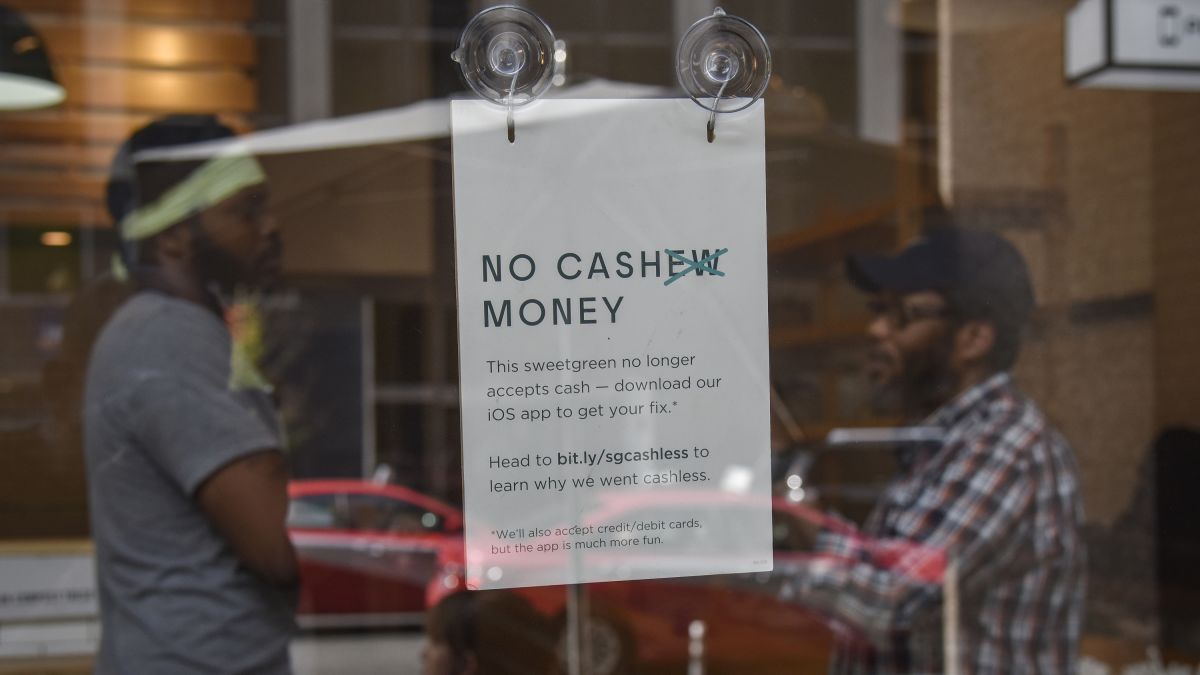

The shift towards a cashless society has been gaining momentum in recent years. More and more stores are embracing the idea of going cashless, where customers can only make payments using debit or credit cards, mobile payment apps, or other digital payment methods. This trend has sparked debates and raised questions about the benefits and potential drawbacks of eliminating cash transactions in retail establishments.

The primary goal of going cashless is to enhance convenience and efficiency for both retailers and customers. With digital transactions, there is no longer a need for cashiers to count bills and coins, which can be time-consuming and prone to error. Additionally, customers can enjoy faster checkout experiences, as they don’t have to fumble for exact change or wait for a cashier to provide it.

Another key aspect driving the adoption of cashless systems is safety and security. The risk of theft and fraud associated with cash handling is significantly reduced when there is no physical currency exchanged. Digital transactions leave a trail of electronic records that can be tracked and monitored, making it easier to detect and prevent fraudulent activities. For customers, this provides a sense of peace of mind, knowing that their financial information is better protected.

Cost savings are also a motivating factor for stores to go cashless. Managing and processing cash can be expensive, with costs such as cash handling fees, security measures, and the need for additional staff to handle cash transactions. By eliminating cash, retailers can reduce these overhead costs and allocate resources more efficiently.

In today’s digital age, customer preferences and expectations are shifting towards convenience and technology-driven solutions. Many individuals now prefer the convenience of using mobile payment apps or contactless cards instead of carrying cash. By going cashless, stores can meet these evolving customer demands and provide a seamless, technology-driven shopping experience.

Looking into the future, the trend towards a cashless society is expected to continue with advancements in technology. Innovations such as biometric authentication, blockchain, and digital wallets are revolutionizing the way payments are made. These developments offer increased convenience and security, further reinforcing the case for going cashless.

Convenience and Efficiency

One of the primary reasons why stores are increasingly going cashless is the desire to enhance convenience and efficiency for both retailers and customers. Digital transactions offer a variety of advantages in terms of streamlining the payment process and improving the overall shopping experience.

By eliminating the need for physical cash, stores can significantly reduce the time it takes for customers to make a payment. With traditional cash transactions, customers often have to search for exact change or wait for the cashier to provide it. This can be time-consuming, especially during peak hours when there is a long line of customers waiting to make their purchases. However, with a cashless system, customers can simply swipe their cards, tap their phones, or use other digital payment methods to complete their transactions quickly and easily. This not only saves time for the customers but also allows stores to process more transactions in a shorter period, leading to increased efficiency.

Furthermore, going cashless eliminates the need for cashiers to count and handle physical currency. Counting cash can be prone to errors, and mistakes can lead to discrepancies in cash register balances. By transitioning to digital payments, stores can eliminate the manual handling and counting of bills and coins, reducing the risk of human error. This, in turn, improves the accuracy of transaction records and helps maintain more precise financial records for the store.

In addition to speeding up the checkout process, a cashless system also simplifies the reconciliation of sales and the management of store finances. Retailers can easily access transaction data and generate reports on sales volumes, revenue, and other financial metrics. This digital record-keeping allows for more efficient bookkeeping and simplifies the end-of-day cash reconciliation process. Instead of sorting and counting cash, store employees can focus on other essential tasks, such as restocking merchandise or providing better customer service.

Overall, the convenience and efficiency of cashless systems benefit both retailers and customers. Customers can enjoy shorter wait times at the checkout counter and a smoother payment experience. Retailers can streamline their operations, improve accuracy in financial reporting, and increase productivity. As technology continues to advance, the convenience and efficiency of cashless systems are expected to further improve, providing an even more seamless and efficient shopping experience for everyone involved.

Safety and Security

Another compelling reason why stores are transitioning to cashless payment systems is to prioritize safety and security. Digital transactions offer enhanced safeguards compared to handling physical cash, addressing concerns related to theft, fraud, and personal safety.

Handling large amounts of cash increases the risk of theft for both retailers and customers. By going cashless, stores can significantly reduce the likelihood of theft incidents occurring within their premises. With no physical cash on hand, there is no incentive for criminals to target the store for cash-related crimes. This not only helps protect the retailer’s assets but also creates a safer shopping environment for customers. By promoting a more secure shopping environment, stores can attract more customers and build trust in their brand.

Furthermore, digital transactions leave a clear electronic trail, making it easier to detect and prevent fraud. Cash transactions, on the other hand, can be more susceptible to fraudulent activities, such as counterfeit bills or stolen cash. By eliminating cash, stores can mitigate these risks and enhance their overall security measures. Digital payment methods often incorporate encryption and authentication protocols, ensuring the integrity and confidentiality of financial information. Retailers can implement additional security measures, such as using POS systems with advanced security features and adopting multi-factor authentication for online transactions. These measures help protect customers’ financial data from unauthorized access and minimize the potential for fraud.

For customers, cashless transactions offer a sense of peace of mind in terms of personal and financial safety. Carrying large sums of cash can make individuals vulnerable to theft or loss. With a cashless system, there is no need to carry physical currency, as payments can be made conveniently through cards or mobile payment apps. In the event of a misplaced or lost card, customers can quickly notify their bank or payment service provider to suspend or cancel the card, minimizing the risk of unauthorized use. Additionally, digital payments can offer added security features such as biometric authentication or PIN codes, providing an extra layer of protection.

Overall, the safety and security benefits of cashless payment systems make them an attractive option for both retailers and customers. By reducing the risk of theft and fraud, stores can create a secure shopping environment and build trust with their clientele. Customers can enjoy the peace of mind that comes with secure transactions and minimized personal risk. As technology continues to advance, cashless systems will continue to evolve with even stronger security measures, further reinforcing the safety and security advantages they offer.

Cost Savings

In addition to convenience and security, one of the key driving factors behind stores going cashless is the potential for cost savings. Managing and processing physical cash can be an expensive endeavor, and transitioning to digital payments can help businesses reduce overhead costs and allocate resources more efficiently.

Firstly, handling cash comes with various fees and expenses. Stores often incur costs associated with cash handling, such as bank deposit fees, armored car services, and cash counting machines. These expenses can quickly add up, especially for businesses that generate a significant amount of cash transactions on a daily basis. By going cashless, retailers can eliminate or significantly reduce these costs, freeing up financial resources that can be allocated towards other areas of the business.

Another cost-saving advantage of transitioning to cashless systems is the reduction in security expenses. Retailers that handle cash often need to invest in security measures to protect their physical cash, such as surveillance cameras, safes, and additional security personnel. These security measures can be a substantial financial burden for stores. However, by reducing or eliminating cash transactions, the need for these security measures decreases, resulting in cost savings for the business.

Moreover, managing cash requires additional labor and time. Counting and reconciling cash at the end of the day can be a time-consuming task, requiring employees to dedicate hours to sorting, counting, and recording cash transactions. By adopting a cashless system, stores can streamline their operations and reduce the time spent on cash-related tasks. Employees can focus on other value-added activities, such as providing better customer service or managing inventory, leading to increased productivity.

Additionally, the risk of human error associated with cash handling can lead to financial losses for businesses. Counting cash manually is prone to errors, and discrepancies in cash registers can lead to financial discrepancies that affect the accuracy of financial records. By going cashless, stores can reduce the risk of human error and maintain more precise financial records, minimizing the potential for financial losses.

Overall, the cost-saving benefits of going cashless can have a significant impact on a store’s bottom line. By eliminating cash-related fees, reducing security expenses, streamlining operations, and minimizing the risk of human error, stores can allocate financial resources more efficiently and generate cost savings. These savings can be reinvested into the business, such as enhancing customer experiences, expanding product offerings, or improving infrastructure and technology. As businesses continue to seek ways to optimize their operations, the cost-saving advantages of cashless systems make them an appealing choice.

Customer Preferences and Expectations

As technology continues to advance and shape various aspects of our lives, customer preferences and expectations are evolving, particularly in the realm of convenience and seamless experiences. The shift towards a cashless society aligns with these changing preferences and offers a range of benefits that cater to customer expectations.

More and more individuals are embracing the convenience of digital payment methods. Carrying cash can be cumbersome, and the need for exact change can create hassle and delay at the checkout counter. By going cashless, stores can cater to customers who prefer the simplicity and ease of paying through cards, mobile payment apps, or other digital means. This enhances the overall shopping experience by offering a faster and more streamlined payment process.

Alongside the convenience factor, customers also expect a certain level of technology integration and innovation in their shopping experiences. With the rise of smartphones and contactless payment methods, a cashless payment system is seen as a forward-thinking and technologically advanced solution. By adopting digital payment options, retailers can position themselves as modern and tech-savvy establishments, appealing to a broader customer base.

Furthermore, the younger generation, in particular, has grown up in a digital world, where online shopping and digital payments are the norm. These customers have come to expect frictionless and seamless transactions across both physical and online retail channels. Going cashless allows businesses to provide consistency in the overall payment experience, offering the same level of convenience and ease, whether customers are shopping in-store or online.

Security and trust are also central to customer preferences and expectations. Many individuals are concerned about the safety of carrying cash, as physical currency can be lost, stolen, or counterfeit. By transitioning to cashless payments, stores can offer increased security measures, such as encrypted transactions and fraud-detection systems. This gives customers confidence that their financial information is better protected, fostering trust and loyalty towards the brand.

Moreover, the COVID-19 pandemic has accelerated the adoption of contactless payment methods. Customers are now more conscious of minimizing physical contact and reducing the risk of transmission. Going cashless provides a hygienic and touch-free payment option, addressing these concerns and aligning with the hygiene practices individuals have adopted during these times.

In summary, customer preferences and expectations are shifting towards convenience, technology integration, security, and hygiene. Going cashless aligns with these expectations by offering a streamlined payment process, innovative technology solutions, enhanced security measures, and touch-free transactions. By meeting these evolving customer demands, businesses can position themselves as customer-centric and stay ahead of the competition in an increasingly digital and technology-driven marketplace.

Future Trends and Technology

The transition towards a cashless society is not just a current trend but a glimpse into the future of payments and retail. Rapid advancements in technology are driving innovative solutions that are reshaping the way transactions are conducted and transforming the retail landscape.

One of the most significant future trends in cashless payments is the integration of biometric authentication. Biometric data, such as fingerprints or facial recognition, can be used to verify the identity of individuals during payment transactions. This technology not only increases security by providing unique and tamper-proof identification but also enhances convenience by eliminating the need for cards or passwords. With a simple touch or a glance, customers can securely authenticate their transactions, ushering in a new era of seamless and frictionless payments.

The rise of blockchain technology also holds promise for the future of cashless payments. Blockchain is a decentralized ledger system that ensures transparency, security, and immutability of transactions. By leveraging blockchain, digital payments can become even more secure and efficient. Smart contracts powered by blockchain can automate payment processing, eliminating middlemen and reducing transaction costs for retailers. Additionally, blockchain can enable instant settlement of transactions, bypassing the traditional banking infrastructure and potentially improving liquidity for businesses.

Digital wallets are another exciting development in the cashless payment landscape. These virtual wallets allow users to store multiple payment methods, such as credit cards or bank accounts, in one convenient and secure mobile app. Digital wallets offer a seamless and integrated payment experience, allowing customers to make transactions both online and in-store with just a few taps on their smartphones. As technology continues to evolve, we can expect digital wallets to incorporate more features, such as loyalty programs, personalized offers, and integration with other platforms and services, further enhancing the customer experience.

Internet of Things (IoT) technology is also expected to play a significant role in the future of cashless payments. Connected devices, such as smart home assistants, wearables, and even vehicles, can serve as payment devices, allowing customers to make seamless and secure transactions from various touchpoints. For example, customers could make a payment by simply saying a command to their smart speaker or tapping their smartwatch on a payment terminal. This convergence of IoT and cashless payments will enable effortless and ubiquitous transactions, transforming the way we shop and interact with our environment.

As technology continues to advance and consumer expectations evolve, the future of cashless payments holds great potential. Biometric authentication, blockchain, digital wallets, and IoT technology are just a few examples of the innovations that will shape the landscape. As these technologies mature and become more widespread, we can anticipate a more seamless, secure, and integrated payment experience for both retailers and customers.

Potential Challenges

While the transition towards a cashless society brings numerous benefits, there are also potential challenges that need to be considered. These challenges revolve around accessibility, security, and the need to address the concerns of certain segments of the population.

One of the primary challenges is ensuring equal access to digital payment methods for all individuals. While the adoption of smartphones and internet connectivity is widespread, there are still segments of the population, particularly older adults and underserved communities, who may not have access to or be comfortable with digital payment technologies. It is essential to bridge the digital divide and provide alternative solutions to ensure that everyone can participate in the cashless economy, such as providing options for card payments and offering assistance for those who may have difficulties using digital payment platforms.

Another challenge is the potential for increased vulnerability to cyber threats. As the reliance on digital transactions grows, cybercriminals become more incentivized to target these systems. To mitigate this risk, businesses need to invest in robust cybersecurity measures, including data encryption, secure payment gateways, and continual monitoring for suspicious activities. Additionally, educating customers about online security best practices and raising awareness about potential scams can help minimize the risk of fraud.

Moreover, the transition to cashless payments may face resistance from individuals who are hesitant to give up the physicality and anonymity associated with using cash. Some individuals may be concerned about the privacy implications of digital transactions, especially when it comes to the collection and use of personal data by payment providers. Addressing these concerns by implementing transparent data protection policies and allowing customers to have control over their personal information is crucial to alleviate such resistance and build trust in cashless systems.

In certain situations, a lack of reliable internet connectivity or power outages can hinder the ability to process digital payments. This is particularly relevant in areas with poor infrastructure or during natural disasters. To overcome this challenge, backup solutions, such as offline transaction processing capabilities or alternative payment methods, can be implemented to ensure uninterrupted service for customers and retailers.

Lastly, the rapid pace of technological advancements requires ongoing adaptation and training for both retailers and consumers. It can be challenging for some individuals to keep up with the evolving digital landscape and adopt new technologies. Providing education and support to employees and customers will be crucial in ensuring a smooth transition and widespread acceptance of cashless payment systems.

In summary, while the transition to a cashless society offers numerous benefits, there are hurdles that need to be addressed. Ensuring equal access to digital payment methods, enhancing cybersecurity measures, addressing privacy concerns, managing connectivity and power stability issues, and providing ongoing education and training are essential to overcome these challenges and create a seamless and inclusive cashless payment ecosystem for all stakeholders.

The Cashless Debate

The shift towards a cashless society has sparked a debate, with advocates and critics offering differing perspectives on the implications and consequences of going cashless. While some argue that digital payments offer numerous benefits, others express concerns about exclusion, privacy, and the potential impact on marginalized groups.

Advocates of the cashless movement highlight the convenience, efficiency, and safety advantages of digital payments. They argue that cashless transactions streamline processes, reduce the risk of robberies, and enhance the overall shopping experience. Additionally, they emphasize the potential for cost savings and improved financial management for businesses. Supporters point to the widespread adoption of digital payment methods, along with the rising generation of tech-savvy individuals comfortable with mobile transactions, as evidence of the inevitability and desirability of a cashless society.

On the other hand, critics voice concerns over the exclusionary effect of going cashless. They argue that certain segments of the population, such as the elderly, low-income individuals, and those without access to technology, may face barriers to participating in the digital economy. These individuals often rely on cash for their financial transactions, and the push towards cashless payments could further alienate and marginalize them. Additionally, critics raise concerns about the potential erosion of privacy, as digital transactions leave a digital trail that can be tracked and analyzed by businesses and governments. They fear the loss of anonymity and the potential misuse of personal data.

Another point of contention in the cashless debate is the impact on small businesses and local economies. Some argue that cashless systems disproportionately benefit larger corporations that can afford the necessary technology and infrastructure, while potentially disadvantaging small businesses that may struggle to adapt. Critics also express concerns about the potential for job losses, particularly for individuals employed in cash-intensive industries, such as cashiers and bank tellers. Additionally, the widespread adoption of cashless payments could result in a reduction in informal economies and the associated cash-based activities.

Furthermore, critics contend that relying solely on digital payments increases reliance on electronic systems, making society more vulnerable to disruptions caused by power outages, system failures, or cyber-attacks. They argue that having a diverse range of payment options, including cash, provides a necessary buffer against such disruptions and ensures access to transactions even in challenging circumstances.

The cashless debate is multifaceted and continues to evolve as technology advances and societal needs and expectations change. While the benefits of convenience, efficiency, and safety are tempting, it is essential to address the concerns raised by critics to ensure a more inclusive and equitable transition to a cashless society. Striking a balance between the advantages of digital payments and the need to accommodate diverse populations and preserve privacy and financial autonomy is crucial for navigating the complexities of the cashless debate.

Conclusion

The shift towards a cashless society presents numerous advantages and considerations for retailers, customers, and society as a whole. Convenience, efficiency, safety, and cost savings are among the significant benefits associated with digital payment methods. By embracing cashless systems, businesses can streamline operations, enhance the customer experience, and allocate resources more efficiently. For customers, cashless transactions offer convenience, speed, and the peace of mind that comes with enhanced security measures.

However, the transition to a cashless society is not without its challenges. Concerns about exclusion, privacy, and the impact on marginalized communities must be addressed to ensure an inclusive transition. It is crucial to provide alternatives and support for those who may face difficulties accessing or utilizing digital payment technologies. Safeguarding privacy and ensuring the security of digital transactions are paramount to build trust and maintain consumer confidence.

The cashless debate prompts us to consider the potential impact on small businesses, job markets, and local economies. Balancing the benefits of digital payments while preserving the viability of small businesses and addressing the needs of cash-dependent individuals is essential. Maintaining a diverse range of payment options, including cash, can provide resilience in the face of technological disruptions.

As technology continues to advance, the future of cashless payments holds great potential. Biometric authentication, blockchain, digital wallets, and IoT technology are shaping the landscape of cashless transactions. These innovations offer the promise of even more seamless, secure, and integrated payment experiences.

In conclusion, the transition towards a cashless society offers numerous benefits and challenges. Striking a balance between the advantages of digital payments and the need to address concerns regarding accessibility, privacy, and equity will be crucial for a successful and inclusive transition. By embracing technological progress, while ensuring inclusivity and safeguarding individual rights, the potential benefits of a cashless society can be realized for the betterment of both retailers and customers.