Introduction

Welcome to the world of tokenization – a powerful method used in the payments industry to enhance security and protect sensitive cardholder data. In an era where digital transactions are becoming the norm, it is imperative to implement robust technologies that safeguard financial information from potential fraud and unauthorized access.

Tokenization serves as a shield against data breaches by substituting sensitive payment information, such as credit card numbers or bank account details, with a unique identifier known as a token. This process ensures that the original data remains securely stored in a controlled environment while the token is used for payment transactions.

In this article, we will delve into the intricacies of tokenization in payments, explaining how it works and its benefits compared to other security measures like encryption. We will also explore how tokenization is implemented in various payment methods, including credit card payments, mobile payments, web payments, and contactless payments.

So, whether you’re a merchant looking to enhance your payment security or a consumer curious about the technology behind secure transactions, join us on this exciting journey to discover the inner workings of tokenization.

What is Tokenization?

Tokenization is a method used in the payments industry to secure sensitive cardholder data. It involves the process of substituting sensitive payment information, such as credit card numbers, with a unique identifier known as a token. This token acts as a stand-in for the actual data and can be safely used for payment transactions.

Unlike encryption, which converts data into a coded form that can be reversed, tokenization replaces the original data with a non-sensitive token that has no mathematical relationship to the original information. This makes it virtually impossible for hackers to reverse-engineer the token and retrieve the actual payment data.

When a payment is made using tokenization, the token is passed through the payment system instead of the actual card details. This not only protects the cardholder’s sensitive information but also provides a seamless and secure payment experience for both the merchant and the customer.

It’s important to note that tokenization does not occur on the customer’s device or the merchant’s point-of-sale system. Instead, it takes place within a secure, PCI-compliant environment, often provided by a trusted third-party tokenization service provider.

Each token is unique to a specific merchant and is meaningless outside of their system. This means that even if a token is intercepted, it cannot be used for fraudulent transactions because it is not associated with the original payment data or the customer’s account.

The use of tokenization has gained traction in recent years as the payments industry strives to enhance data security and protect against rising threats of data breaches and identity theft. By employing tokenization, businesses can significantly reduce their risk of storing and transmitting sensitive payment information.

Now that you have a basic understanding of tokenization, let’s explore how this process works in greater detail.

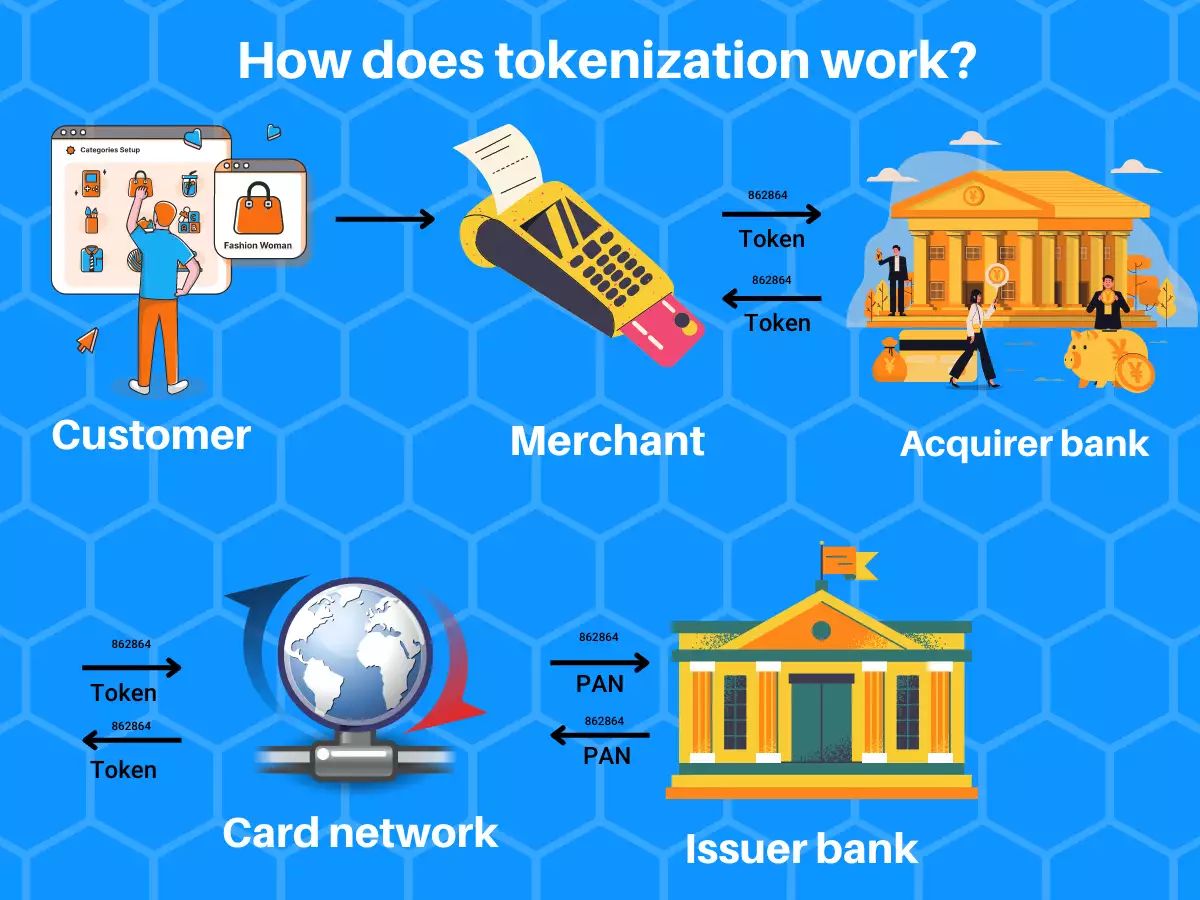

How Tokenization Works

Tokenization involves several steps to securely replace sensitive payment information with tokens. Let’s walk through the process:

Step 1: Data Capture

When a customer initiates a payment, their card information is collected through a secure channel. This can happen either physically, like swiping a credit card in a point-of-sale (POS) terminal, or virtually, such as entering card details on a website or mobile app.

Step 2: Tokenization

Once the card information is captured, the sensitive data is securely sent to a tokenization service provider. This provider employs advanced algorithms to generate a unique token that will replace the payment data. The token is then returned to the merchant for use in subsequent transactions.

Step 3: Secure Storage

The tokenized data is securely stored in the tokenization service provider’s system. This is done in a protected environment that adheres to rigorous security standards and is regularly audited to ensure compliance with industry regulations like the Payment Card Industry Data Security Standard (PCI DSS).

Step 4: Authorization and Payment

When a customer makes a payment using the token, the transaction details are transmitted to the merchant’s payment gateway. The payment gateway sends the token to the tokenization service provider, which decrypts the token and retrieves the corresponding payment information for authorization.

Step 5: Token Lifecycle Management

Throughout the customer’s relationship with the merchant, the tokenization service provider manages the lifecycle of the tokens. This includes actions like token issuance, token suspension or deletion in case of lost or stolen cards, and token updates to reflect changes in the underlying payment information.

By following this process, tokenization ensures that sensitive payment data is never exposed or transmitted in an unsecure manner. Instead, only the token is used during transactions, providing an additional layer of security against potential data breaches.

Now that we understand how tokenization works, let’s explore the benefits it offers in terms of security, compliance, and user experience.

Step 1: Data Capture

The first step in the tokenization process is the capture of the customer’s payment data. This data includes sensitive information such as credit card numbers, expiration dates, and CVV codes. The method of data capture can vary depending on the payment channel used by the customer, whether it be a physical point-of-sale (POS) terminal, a website, a mobile app, or any other payment interface.

When a customer makes a payment using a physical card, the merchant or the payment service provider uses a POS terminal to capture the necessary card information. The card is either swiped, inserted, or tapped, and the terminal securely reads the relevant data from the card’s magnetic strip or chip. This data is then encrypted and transmitted to the tokenization service provider, who will generate the corresponding token and return it to the merchant.

For online payments, customers typically enter their card information on a secure web page, often referred to as a payment gateway. The payment gateway ensures that the data is encrypted during transmission and forwards it to the tokenization service provider. The provider then generates the token and sends it back to the payment gateway for storage and use in future transactions.

In the case of mobile payments, data capture can occur directly through a mobile app or a mobile wallet. Customers may need to scan their cards using their device’s camera or manually enter the card details. Again, the encrypted data is sent to the tokenization service provider, who transforms it into a token and returns it to the mobile app or wallet for secure storage.

It is essential to note that during the data capture stage, stringent security measures are in place to ensure the protection of customer data. This includes the use of strong encryption algorithms, secure protocols for data transmission, and adherence to industry regulations such as the Payment Card Industry Data Security Standard (PCI DSS).

By capturing the customer’s payment data securely, tokenization sets the foundation for subsequent steps in the process. With sensitive information protected, businesses can focus on providing a secure and seamless payment experience for their customers.

Step 2: Tokenization

After the customer’s payment data is captured, the next step in the tokenization process is the actual tokenization of the sensitive information. Tokenization is carried out by a trusted third-party service provider who specializes in securing payment data and generating unique tokens for each transaction.

The tokenization service provider employs advanced mathematical algorithms to transform the sensitive payment data into a token. This token is a randomized series of characters that has no meaningful relationship to the original data. It is important to note that the tokenization process is irreversible, ensuring that the original payment data remains secure.

The generation of the token involves several layers of security measures to protect against unauthorized access. These measures include encryption, de-identification techniques, and the use of secure key management systems. By employing these methods, the tokenization service provider ensures that the tokens it generates are strong, unique, and resilient against attacks.

Once the token is created, it is associated with the original payment data in the tokenization service provider’s system. This association allows for the retrieval of the original data when the token is used in subsequent transactions. However, it is important to note that the token itself does not reveal any sensitive information about the customer’s payment details.

The token is then securely transmitted back to the merchant, who stores it in their system for future use. The token is specifically linked to the customer and the merchant’s unique identifier, ensuring that it can only be used for transactions between the two parties.

By tokenizing the sensitive payment data, businesses can significantly reduce the risk of exposing customer information to potential vulnerabilities. In the event of a data breach, the tokens are of no use to hackers as they do not contain any meaningful information about the customer’s payment details.

Through tokenization, businesses can enhance the security of their payment ecosystem and provide their customers with peace of mind knowing that their sensitive information is protected. Moving on to the next step, let’s explore how the tokenized data is stored securely.

Step 3: Secure Storage

Once the token is generated, the sensitive payment data is securely stored in the tokenization service provider’s system. This step is crucial in ensuring the confidentiality and integrity of the data throughout its lifecycle.

The tokenization service provider employs robust security measures to protect the stored data. This includes encryption of the data at rest, which involves converting the information into an unreadable format using advanced cryptographic algorithms. The encrypted data is then stored in a secure database or file system that is access-controlled and regularly audited.

Additionally, the tokenization service provider adheres to industry standards such as the Payment Card Industry Data Security Standard (PCI DSS) to ensure the highest level of security. These standards set guidelines for secure storage, transmission, and processing of payment card data.

The tokenization service provider’s infrastructure is designed to have multiple layers of security, including firewalls, intrusion detection systems, and data loss prevention mechanisms. These security measures help protect against unauthorized access and ensure that customer data remains safeguarded.

Moreover, the tokenization service provider implements strict access controls and authentication protocols to regulate access to the stored data. Only authorized personnel with appropriate credentials and permissions can access the sensitive information, further limiting the risk of unauthorized access.

Regular security audits and assessments are conducted to validate the effectiveness of the implemented security measures. These audits help identify vulnerabilities, implement necessary patches and updates, and ensure ongoing compliance with industry regulations and best practices.

By securely storing tokenized payment data, businesses can significantly reduce the risk of data breaches and preserve customer trust. Tokenization not only protects the customer’s sensitive information but also relieves businesses of the burden of storing and managing large volumes of payment data, reducing their security risk and compliance responsibilities.

With the sensitive payment data securely stored, the next step is to authorize and process the payment using the token. Let’s explore this step in further detail.

Step 4: Authorization and Payment

Once the tokenized payment data is securely stored, the next step in the tokenization process is the authorization and payment stage. This involves using the token to facilitate the transaction without exposing the actual sensitive payment information.

When a customer initiates a payment using the token, the transaction details are transmitted to the merchant’s payment gateway. The payment gateway acts as an intermediary, facilitating the secure transfer of information between the merchant, the tokenization service provider, and the payment processor.

The payment gateway receives the token from the merchant and forwards it to the tokenization service provider for decryption. The tokenization service provider retrieves the corresponding payment data associated with the token in their secure system.

Once the payment data is decrypted, it is used to authorize the transaction with the payment processor. This involves checking the availability of funds, verifying the legitimacy of the transaction, and ensuring it complies with the business’s defined rules and risk parameters.

If the transaction is authorized, the payment processor generates an authorization code, indicating that the payment is approved. This code is then sent back to the merchant’s payment gateway, which communicates the authorization status to the customer and completes the payment process.

Throughout this entire process, the actual sensitive payment data is never exposed or transmitted, ensuring the highest level of security. Instead, the token acts as a surrogate for the payment data, allowing for seamless and secure transaction processing.

From the customer’s perspective, using tokens for payment provides a convenient and frictionless experience. They are not required to enter their sensitive payment information for every transaction, reducing the potential for mistakes or vulnerabilities during data entry.

Additionally, by eliminating the need to transmit the sensitive payment data, businesses can ensure a more efficient and streamlined payment process. This reduces the time and effort required for data transmission and processing, improving the overall efficiency of their payment operations.

Tokenization enables businesses and their customers to enjoy the benefits of a secure and seamless payment experience, with the added reassurance that their payment information is protected from potential data breaches.

Now that we understand the authorization and payment process using tokenization, let’s explore the importance of token lifecycle management in maintaining a secure payment ecosystem.

Step 5: Token Lifecycle Management

Token lifecycle management is an integral part of the tokenization process, ensuring that the tokens remain secure, up-to-date, and in sync with the underlying payment information. This step involves various actions throughout the lifespan of the tokens, from their issuance to their eventual suspension or deletion.

Token Issuance: When a customer initiates a transaction, the tokenization service provider generates a unique token and associates it with the customer’s payment data. This step ensures that each transaction has a distinct token, enhancing security and preventing fraudulent use of tokens.

Suspension and Deletion: In certain scenarios, such as when a card is reported lost or stolen, the token needs to be suspended or deleted. This prevents unauthorized individuals from using the token for fraudulent transactions. Tokenization service providers have mechanisms in place to promptly suspend or delete tokens upon receiving such notifications from the merchant or customer.

Token Updates: As customer payment information changes, such as a card expiration date or a card replacement, the tokens need to be updated to reflect the new details. This ensures that the tokens remain valid and can be used for authorized transactions in the future. Tokenization service providers facilitate this process and ensure that the tokens are always associated with the correct and up-to-date payment information.

Token Expiration: Tokens can be set to expire after a certain period, typically for security reasons. This ensures that the tokens have a limited lifespan and reduces the risk of unauthorized use. When a token expires, it becomes invalid, and subsequent transactions with that token will be declined.

By effectively managing the lifecycle of tokens, businesses can maintain a secure payment ecosystem. The tokenization service provider plays a crucial role in ensuring that tokens are issued, updated, and managed properly throughout their lifespan.

Token lifecycle management also allows businesses to maintain compliance with industry regulations and standards. For example, the Payment Card Industry Data Security Standard (PCI DSS) requires businesses to regularly review and update their tokenization processes to protect against potential vulnerabilities and ensure the ongoing security of customer payment information.

By implementing robust token lifecycle management practices, businesses can mitigate the risk of unauthorized access, data breaches, and fraudulent activities. These practices provide an additional layer of security and peace of mind for both the merchant and the customer.

Now that we have explored the token lifecycle management aspect of tokenization, let’s discuss the numerous benefits that tokenization offers in terms of enhanced security, simplified compliance, and improved user experience.

Benefits of Tokenization

Tokenization offers a range of benefits that make it a preferred method for securing sensitive payment data. Let’s explore the key advantages:

Enhanced Security: Tokenization provides a high level of security by substituting sensitive payment data with tokens. This ensures that the actual payment information is not exposed during transactions, significantly reducing the risk of data breaches and unauthorized access. Even if a token is intercepted, it cannot be used to retrieve the original payment data.

Simplified Compliance: Tokenization helps businesses simplify their compliance efforts by reducing the scope of PCI DSS compliance requirements. Since sensitive payment data is not stored or transmitted in clear text, businesses can streamline their compliance processes and focus on protecting the tokens instead. This reduces the cost, complexity, and potential liabilities associated with compliance.

Improved User Experience: Tokenization enhances the user experience by eliminating the need for customers to repeatedly enter their sensitive payment information. Once a token is generated, it can be securely stored for future transactions, ensuring a convenient and frictionless payment process. Additionally, tokenization reduces the risk of errors during data entry, resulting in smoother and more reliable transactions.

Minimized Risk of Data Breaches: By implementing tokenization, businesses significantly reduce the risk of data breaches and the associated financial and reputational damage. Since sensitive payment data is not stored or transmitted, the value of the data to potential attackers is greatly reduced. This deters cybercriminals and provides peace of mind to both customers and businesses.

Flexibility and Scalability: Tokenization offers flexibility and scalability for businesses of all sizes. Whether it’s a small online store or a large enterprise with multiple payment channels, tokenization can be seamlessly integrated into existing systems and processes. As the business grows, tokenization can easily adapt to accommodate increased transaction volumes and additional payment methods.

Reduced Processing Costs: Tokenization can lead to cost savings for businesses by reducing the amount of sensitive payment data that needs to be stored and processed. Storing tokens instead of actual cardholder data simplifies the infrastructure required for secure storage and processing, resulting in lower costs for maintaining compliance and managing payment systems.

Overall, tokenization is a powerful tool that addresses the critical need for securing sensitive payment data. The enhanced security, simplified compliance, improved user experience, minimized risk of data breaches, flexibility, scalability, and cost savings make tokenization an invaluable component of a robust and secure payment ecosystem.

Now that we have explored the benefits of tokenization, let’s delve into a comparison between tokenization and encryption, two popular methods used for data security in payments.

Enhanced Security

One of the primary advantages of tokenization in payment systems is its enhanced security capabilities. By replacing sensitive payment data with tokens, tokenization effectively shields the actual data from potential threats and unauthorized access.

Tokenization ensures that sensitive payment information such as credit card numbers, bank account details, and personally identifiable information (PII) is never exposed during payment transactions. Instead, a randomly generated token is used as a stand-in for the actual data.

Unlike encryption, which can be reversed with the right decryption key, tokenization renders the token meaningless to cybercriminals. Even if a token is intercepted, it cannot be used to decipher or retrieve the original payment data. This significantly reduces the risk of data breaches stemming from intercepted or stolen tokens.

Furthermore, tokenization operates under the principle of data devaluation. Tokens are typically one-time use or limited use, meaning that even if a token is compromised, it has no value beyond a specific transaction or merchant environment. This further mitigates the impact of potential data breaches and protects cardholder data from unauthorized use.

In addition to securing sensitive payment data during transmission, tokenization also offers robust security for data storage. The tokens are stored in a tokenization service provider’s secure environment, protected with industry-standard security measures, encryption, and access controls. This ensures that even if an attacker gains access to the token vault, the tokens remain useless without the original data and merchant context.

By implementing tokenization, businesses can significantly reduce their exposure to data breaches and the associated risks. Tokenization provides a proactive and comprehensive approach to data security in payment systems, protecting cardholder data at every stage of the transaction lifecycle.

Beyond providing a secure payment environment, tokenization also offers peace of mind to both merchants and customers. Customers can have confidence in their transactions, knowing that their sensitive payment information is well-protected. Merchants can focus on providing exceptional customer experiences and growing their businesses, without the constant fear of data breaches and their detrimental effects.

With the increasing challenges posed by cyber threats, tokenization has emerged as a crucial method for enhancing security in the payment industry. Its ability to replace sensitive payment data with tokens, protect data during transmission and storage, and minimize the risk of data breaches makes it an indispensable tool in safeguarding sensitive payment information.

Now that we have explored the enhanced security benefits of tokenization, let’s compare tokenization with encryption, another widely used method for protecting payment data.

Simplified Compliance

Tokenization not only enhances security in payment systems but also simplifies the compliance efforts for businesses. Compliance with industry regulations, such as the Payment Card Industry Data Security Standard (PCI DSS), is crucial to ensure the protection of cardholder data and maintain customer trust.

One of the main advantages of tokenization is that it reduces the scope of PCI DSS compliance requirements. By replacing sensitive payment data with tokens, businesses no longer need to store, transmit, or process the actual cardholder data. This significantly reduces the complexity and burden of complying with the extensive security measures outlined in the PCI DSS.

Since tokens are used in place of payment data, the storage and processing of tokens are subject to fewer compliance requirements compared to handling actual cardholder data. With tokenization, businesses can focus their compliance efforts on securing the token data rather than dealing with the more stringent requirements associated with handling sensitive payment information.

Another aspect of compliance made simpler through tokenization is the management of customer consent and data retention policies. Tokenization enables businesses to handle customer data in compliance with privacy regulations and consent requirements. Since only tokens are stored and processed, businesses can easily manage customer data retention and deletion requests without compromising transactional integrity.

Furthermore, tokenization offers transparent and auditable security measures, making compliance audits less daunting. The use of tokenization service providers who comply with industry regulations and undergo regular security assessments further simplifies compliance efforts for businesses. These providers handle and store the tokens securely, thereby demonstrating their commitment to security and compliance.

By streamlining compliance obligations, tokenization allows businesses to focus on core operations and customer service, rather than dedicating excessive resources to compliance-related tasks. This not only saves time and effort but also reduces the risk of non-compliance, which can result in fines, reputational damage, and loss of customer trust.

For businesses operating in highly regulated industries, such as banking or healthcare, tokenization offers an additional layer of compliance assurance. It provides a secure and reliable method of protecting payment data while facilitating compliance with industry-specific regulations and requirements.

Overall, the simplicity and efficiency of compliance achieved through tokenization make it an attractive option for businesses seeking secure payment solutions without the burden of extensive regulatory obligations. Tokenization’s ability to reduce compliance scope and ensure data protection helps businesses navigate the complex landscape of data security and privacy regulations.

Now that we have explored the benefits of simplified compliance through tokenization, let’s discuss how it improves the user experience in payment transactions.

Improved User Experience

Tokenization not only enhances security and simplifies compliance but also greatly improves the user experience in payment transactions. By streamlining the payment process and ensuring a seamless and convenient experience, tokenization benefits both merchants and customers alike.

One of the key advantages of tokenization is the elimination of the need for customers to repeatedly enter their sensitive payment information. Once a token is generated, it can be securely stored and used for future transactions. This eliminates the inconvenience and potential errors associated with manually entering payment details, making the checkout process faster and more efficient.

With tokenization, customers can make purchases with just a few clicks or taps. Whether they are shopping online, using a mobile app, or making an in-store payment, the token serves as a secure and quick method for initiating transactions. This simplicity reduces friction in the payment process, leading to a more positive overall experience for customers.

Moreover, tokenization enhances security without compromising convenience. Customers can trust that their sensitive payment data is protected, as tokens have no mathematical relationship to the original payment information. This reassurance builds confidence and peace of mind, ultimately resulting in a better user experience.

Additionally, tokenization facilitates a consistent and personalized experience for customers across multiple platforms and devices. As tokens are associated with a specific customer and merchant, they can be used seamlessly across different payment channels, such as online, mobile, or in-store payments. This omni-channel capability enhances convenience and provides a unified experience for customers, regardless of how they choose to pay.

For merchants, tokenization also improves the user experience by enabling faster and more secure transaction processing. With tokens, merchants can streamline their payment operations as they no longer need to handle, store, and transmit sensitive payment data. This reduces the complexity and associated costs of maintaining secure systems and complying with data protection regulations.

In summary, tokenization enhances the user experience in payment transactions by simplifying the payment process, eliminating the need for repetitive data entry, and providing a secure and seamless experience for customers. By improving convenience and boosting customer confidence, tokenization enables merchants to create a positive and satisfying payment experience, leading to increased customer loyalty and satisfaction.

Now that we have explored the benefits of tokenization in terms of security, compliance, and user experience, let’s compare tokenization with another widely used security measure in the payment industry: encryption.

Tokenization vs. Encryption

Tokenization and encryption are two widely used methods for securing sensitive data in the payment industry. While both techniques aim to protect data, they differ in their approach and effectiveness in certain aspects.

Data Protection: Encryption works by converting sensitive data into an unreadable format using complex algorithms. The encrypted data can be reversed using a decryption key when necessary. On the other hand, tokenization replaces sensitive data with random tokens that hold no meaningful relationship to the original information. Tokenization is considered more secure than encryption because tokens cannot be mathematically reversed or used to retrieve the original data.

Scope of Protection: Encryption protects data during transmission and storage. However, the original sensitive data is still present in the system and can be exposed if not adequately safeguarded. In contrast, tokenization completely removes sensitive data from the merchant’s environment, reducing the risk of data breaches and the scope of compliance requirements. Tokens are used in place of the original data, minimizing the impact of a potential breach.

Compliance Simplification: Encryption alone is not sufficient to simplify compliance efforts. Merchants using encryption must still comply with the extensive security requirements of data handling and storage outlined by the Payment Card Industry Data Security Standard (PCI DSS). Tokenization, on the other hand, reduces the scope of compliance by eliminating the storage and transmission of sensitive data. With tokenization, businesses can focus on securing the tokens and managing a smaller and less complex compliance environment.

User Experience: Encryption may require customers to manually enter their payment information each time they make a transaction, as the encrypted data needs to be decrypted for processing. This can be time-consuming and inconvenient. Tokenization provides a smoother user experience by allowing customers to store and reuse tokens for future transactions. This eliminates the need for repetitive data entry and enhances the speed and convenience of the payment process.

Value of Data: Encrypted data, if compromised, still holds some value to potential attackers who have the decryption key. Tokenized data, however, has no value outside of the specific merchant’s system. Tokens are useless if intercepted or stolen, as they cannot be used to obtain the original payment data.

Overall, while encryption provides a layer of security for data in transit and at rest, tokenization offers enhanced protection by completely removing sensitive data from the merchant’s environment. Tokenization simplifies compliance efforts, improves the user experience, and reduces the risk of data breaches by replacing sensitive data with tokens that hold no intrinsic value.

Both tokenization and encryption have their merits and may be employed in combination for a comprehensive security approach. However, when it comes to protecting sensitive payment information in a highly secure and streamlined manner, tokenization emerges as a preferred method within the payment industry.

With a clear understanding of the differences between tokenization and encryption, let’s explore tokenization in the context of different payment methods, starting with credit card payments.

Tokenization in Different Payment Methods

Tokenization is a versatile security measure that can be applied to various payment methods, providing a unified and secure experience across different platforms and channels. Let’s explore how tokenization is implemented in different payment methods:

Tokenization in Credit Card Payments: Tokenization is widely used in credit card payments, both online and in-store. When a customer makes a payment, the card details are securely captured and sent to a tokenization service provider. The provider generates a unique token that represents the card data and returns it to the merchant. This token is then used in subsequent transactions, eliminating the need to store and transmit sensitive card information. Merchants can securely process payments using the token while maintaining a high level of security for cardholder data.

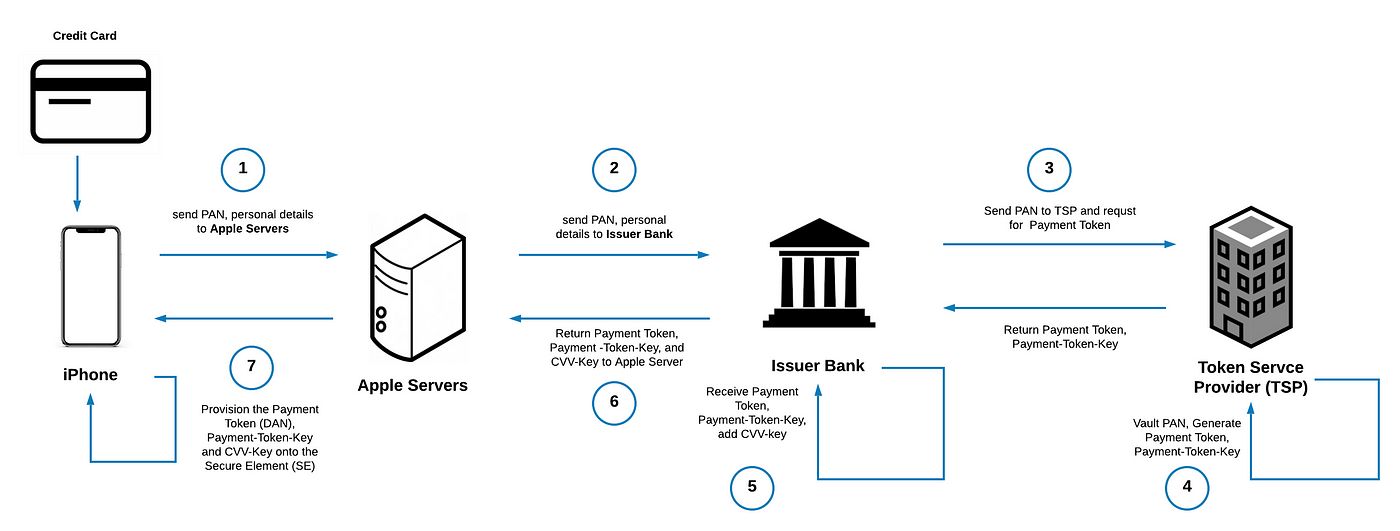

Tokenization in Mobile Payments: Tokenization plays a crucial role in securing mobile payment transactions. When a customer adds their payment card to a mobile wallet, such as Apple Pay or Google Pay, the wallet provider tokenizes the card details and associates them with the customer’s device. When the customer initiates a payment using their mobile device, the token is transmitted instead of the actual card information. This ensures that the sensitive card data is protected throughout the transaction process, making mobile payments secure and convenient.

Tokenization in Web Payments: Tokenization is utilized in web payments to improve security and streamline the checkout experience. When a customer makes a payment on a website, the payment gateway tokenizes the card details and passes the token to the merchant for storage. This enables customers to save their payment information securely for future use. When they return to the website, the token can be used to process payments without requiring the re-entry of sensitive card information. Tokenization in web payments enhances security, reduces friction, and improves conversion rates.

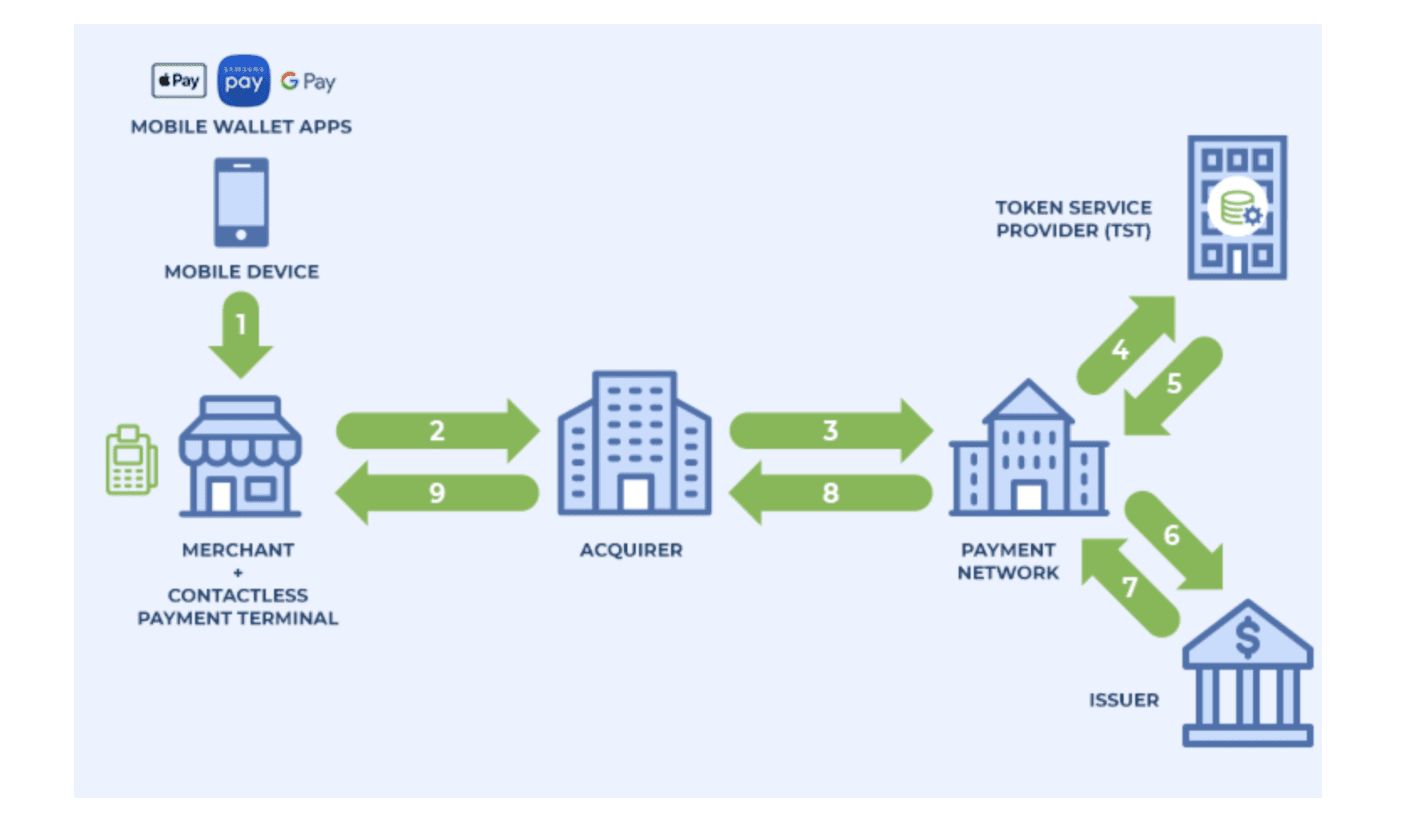

Tokenization in Contactless Payments: Contactless payments, such as those made using Near Field Communication (NFC) technology or contactless cards, also benefit from tokenization. Tokenization ensures that the actual card details are not exposed during the payment process. Instead, a token associated with the card data is transmitted and used to authorize the transaction. With tokenization, customers can enjoy convenient and secure tap-and-go payments while minimizing the risk of data compromise.

Tokenization provides a consistent and secure approach to payment processing across different methods, platforms, and devices. By replacing sensitive payment data with tokens, businesses can ensure a seamless, convenient, and secure payment experience for their customers, regardless of the payment method they choose.

Now that we have explored tokenization in various payment methods, let’s conclude our discussion with a brief summary of its benefits and significance in the payments industry.

Tokenization in Credit Card Payments

Tokenization plays a crucial role in securing credit card payments by replacing sensitive card data with tokens. This method offers enhanced security and reduces the risk of data breaches, providing a seamless and secure experience for both merchants and customers.

When a customer makes a credit card payment, the card details are securely captured and transmitted to a tokenization service provider. The provider generates a unique token that represents the card data and returns it to the merchant. This token is then stored in the merchant’s system for future transactions.

By using tokens, merchants can process payments without storing or transmitting actual cardholder data, significantly reducing the risk of data breaches. Tokens have no intrinsic value and cannot be mathematically reversed to retrieve the original payment information. Even if intercepted, tokens are meaningless to attackers.

Tokenization also enhances the user experience in credit card payments. Customers no longer need to repeatedly enter their card information for each transaction. Instead, they can securely store their payment details as tokens. This simplifies the checkout process, reduces the potential for errors during data entry, and improves transaction speed and convenience.

Additionally, tokenization simplifies compliance efforts for merchants. Storing tokens instead of actual cardholder data reduces the scope of Payment Card Industry Data Security Standard (PCI DSS) compliance requirements. Merchants can focus on securing the tokens, which are less sensitive and pose a reduced compliance burden.

Tokenization in credit card payments also provides businesses with flexibility. Merchants can operate across multiple channels, such as e-commerce websites, mobile apps, and physical stores, using the same tokenized payment data. This omni-channel capability ensures a consistent and secure payment experience for customers, regardless of the payment channel they choose.

Overall, tokenization in credit card payments offers enhanced security, simplified compliance, improved user experience, and increased flexibility. This method allows merchants to process payments efficiently while maintaining the highest level of data protection. Customers can enjoy seamless and secure transactions, giving them peace of mind when making credit card payments.

Now that we have explored the role of tokenization in credit card payments, let’s conclude our discussion on the significance of tokenization in the broader payments industry.

Tokenization in Mobile Payments

Tokenization plays a vital role in securing mobile payments, providing a secure and convenient method for customers to make transactions using their mobile devices. With the increasing popularity of mobile wallets and mobile payment apps, tokenization ensures the protection of sensitive payment information in this rapidly growing payment method.

When a customer adds their payment card to a mobile wallet, such as Apple Pay or Google Pay, the wallet provider leverages tokenization to secure the card details. The payment card data is securely transmitted to a tokenization service provider, which generates a unique token that represents the card information.

Once the token is created, it is securely stored within the customer’s mobile device, often protected by additional security measures such as biometric authentication or PIN codes. When the customer initiates a payment using their mobile device, the token is transmitted instead of the actual card information. This ensures that the sensitive payment data is protected throughout the transaction process.

The use of tokens in mobile payments offers several benefits. Firstly, it enhances security by ensuring that the actual card information is never directly transmitted or stored in the merchant’s or payment processor’s systems. Tokens hold no intrinsic value and cannot be used to extract the original payment information.

Secondly, tokenization streamlines the checkout process for mobile payments. Customers can securely store their payment information as tokens within their mobile wallets, enabling quick and easy transactions with just a few taps. This eliminates the need to manually enter card details for each payment, enhancing convenience and reducing the potential for errors during data entry.

Tokenization also simplifies compliance with industry regulations, such as the Payment Card Industry Data Security Standard (PCI DSS). As sensitive payment data is replaced with tokens, the scope of compliance requirements is reduced, focusing primarily on securing the tokens themselves.

Moreover, tokenization provides a seamless and consistent user experience across different mobile payment platforms and devices. Tokens can be used securely across various merchants and payment apps, ensuring an effortless and secure payment experience for customers, regardless of their choice of mobile payment method.

In summary, tokenization in mobile payments enhances security, simplifies compliance, and offers a frictionless user experience. It enables customers to enjoy the convenience of mobile payments with the confidence that their sensitive payment data is protected throughout the transaction process.

Now that we have explored tokenization in the context of mobile payments, let’s conclude our discussion by summarizing the significance of tokenization in the broader payments industry.

Tokenization in Web Payments

Tokenization plays a significant role in improving the security and efficiency of web payments. Whether customers are shopping on e-commerce websites or subscribing to online services, tokenization ensures that their sensitive payment information is securely protected.

When a customer makes a payment on a website, tokenization is utilized to secure their payment data. The payment gateway responsible for processing the payment captures the customer’s card details and securely transmits them to a tokenization service provider. The provider then generates a unique token that represents the card data.

Instead of storing and transmitting the actual card information, the token is securely stored in the merchant’s system. When the customer returns to make another purchase on the same website, the token is used to process the payment without the need for the customer to re-enter their card details.

Tokenization in web payments provides enhanced security. By replacing the actual card data with tokens, businesses reduce the risk of data breaches. Tokens are meaningless to potential attackers and do not reveal any sensitive payment information. Even if intercepted, the tokens cannot be misused or reverse-engineered to obtain the original payment data.

The use of tokens also simplifies compliance efforts for businesses. Storing tokens instead of actual cardholder data reduces the scope of Payment Card Industry Data Security Standard (PCI DSS) compliance requirements. Businesses can focus on securing the tokens, which pose a lower risk and compliance burden compared to storing and protecting sensitive payment information.

Additionally, tokenization improves the user experience in web payments. Customers no longer need to repeatedly enter their card details for each transaction on their favorite websites. Instead, they can securely store their payment information as tokens, enabling quick and seamless checkout processes. This eliminates friction and streamlines the payment experience, improving customer satisfaction and reducing cart abandonment rates.

Furthermore, tokenization in web payments enables businesses to offer personalized and convenient services. By storing tokens associated with customer payment data, businesses can provide a more tailored and customized experience. For subscription-based services, tokens ensure smooth and uninterrupted recurring payments without the need for customers to manually renew their subscriptions.

In summary, tokenization in web payments offers enhanced security, simplified compliance, and an improved user experience. It enables customers to make payments conveniently on websites while ensuring their sensitive payment information remains secure. For businesses, tokenization enhances customer trust, streamlines operations, and bolsters security measures.

Having explored tokenization in various payment methods, let’s conclude our discussion now by highlighting the significance of tokenization in the broader payments industry.

Tokenization in Contactless Payments

Tokenization plays a crucial role in securing contactless payments by ensuring the protection of sensitive payment information during transactions. As contactless payments, enabled by Near Field Communication (NFC) technology, gain popularity, tokenization provides an essential layer of security.

When a customer initiates a contactless payment, whether with their mobile device or contactless card, tokenization comes into play. The sensitive payment data, such as the card details, is securely captured and replaced with a unique token by the issuing bank or the payment network.

These tokens act as a stand-in for the actual payment information during the transaction. When a customer taps their device or card to a contactless payment terminal, the token is transmitted securely to the payment processor for authorization and processing.

By using tokens, contactless payments ensure that the actual payment data remains secure. Tokens hold no intrinsic value and cannot be used to extract the original payment information. This significantly reduces the risk of data breaches and unauthorized access to sensitive payment data during contactless transactions.

Tokenization also offers the advantage of convenience and speed in contactless payments. Customers can tap their devices or cards to complete transactions quickly and seamlessly, without the need to manually enter their payment details. This frictionless experience enhances the overall convenience of contactless payments, enabling customers to make swift and secure transactions.

Moreover, tokenization in contactless payments maintains compatibility and interoperability across various devices and platforms. Tokens can be securely provisioned on different mobile devices and contactless cards, allowing for consistent and secure transactions across a wide range of payment acceptance points.

For merchants, tokenization reduces the complexity of payment acceptance in contactless transactions. By utilizing tokens, merchants can process payments without storing or transmitting actual cardholder data, simplifying their compliance with industry regulations such as the Payment Card Industry Data Security Standard (PCI DSS).

Overall, tokenization in contactless payments offers enhanced security, improved convenience, and compatibility across different platforms and devices. It ensures that sensitive payment information remains protected, enabling customers to enjoy fast and secure contactless transactions with confidence.

Now that we have explored tokenization in contactless payments, let’s conclude our discussion by summarizing the significance of tokenization in the broader payments industry.

Conclusion

Tokenization stands as a powerful and effective method for securing sensitive payment data in various payment methods. By replacing sensitive information with unique tokens, tokenization offers enhanced security, simplified compliance, and improved user experience across different payment channels and platforms.

The process of tokenization involves capturing payment data securely, generating tokens that act as surrogates for the data, securely storing those tokens, and leveraging them for subsequent transactions. This approach significantly reduces the risk of data breaches and unauthorized access to sensitive payment information.

Tokenization simplifies compliance efforts by reducing the scope of sensitive data that merchants must handle and comply with under industry regulations. By storing and transmitting tokens instead of actual payment data, businesses can streamline their compliance efforts and focus on securing the tokens themselves.

Furthermore, tokenization improves the user experience by eliminating the need for customers to repeatedly enter their sensitive payment information. Tokens can be securely stored and reused for future transactions, providing a quicker, smoother, and more convenient payment process for customers.

Tokenization finds application in various payment methods, including credit card payments, mobile payments, web payments, and contactless payments. It offers a consistent and secure approach to payment processing, regardless of the chosen payment method or device.

In today’s digital world, where the security of financial transactions is of paramount importance, tokenization emerges as a critical component of a robust and secure payment ecosystem. It allows businesses to protect sensitive payment information, build customer trust, simplify compliance, and create seamless payment experiences.

As the payments industry continues to evolve, tokenization remains a reliable and effective method to safeguard sensitive payment data in an ever-changing landscape of cyber threats and data breaches. Adopting tokenization can provide businesses with a competitive edge, as customers increasingly prioritize security and convenience when choosing payment options.

In conclusion, tokenization is a powerful security measure that addresses the challenges of securing payment data while maintaining a seamless user experience. By implementing tokenization, businesses can unlock the benefits of enhanced security, simplified compliance, and improved user experiences, leading to greater customer satisfaction and trust in the digital payment ecosystem.