Afterpay is one of the first “buy now, pay later” services to reach the global retail market. It makes it possible to acquire goods and services without forcing full payment upfront. Payments are diluted into installments of equal cost, which are then spread out over a given period to allow customers more time to pay their debt. It helps to reduce the financial burden on customers while also reducing risks for merchants. In this article, we’ll examine Afterpay, its inner workings, and how you can benefit from this new payment service.

What Is Afterpay?

Afterpay is a new payment method that makes it easier to pay for goods and services. It falls under the larger category of the budding ‘buy now, pay later’ (BNPL) trend in the retail industry. Traditional payment methods require you to pay the full amount. But with Afterpay, that total balance is divided into four equal amounts or installments that you can pay up in a matter of six weeks.

Afterpay is originally an Australian company founded in 2015. It has since expanded operations to the US, UK, Canada, and New Zealand. According to a report by the Market Herald, the company currently has over 9.9 million active users globally. Over 5.6 million customers are based in the US while over a million customers are based in the UK. The same reports indicate that an average of 17,000 people is joining the Afterpay online platform and app each day. Afterpay had also doubled its earnings from USD 264.1 million in 2019 to USD 519.2 million in 2020.

Earlier this year, American fintech company Square announced that they had purchased Afterpay for a total of USD 29 billion. Reports indicate the Square has plans to merge Afterpay with other services run by Square, such as Cash App. The integration will allow merchants partnered with Square to offer Afterpay as a payment method for their online stores.

How Does Afterpay Work?

While Afterpay’s payment scheme appears simple enough, there is a lot more going on under the surface. Let’s explore the basic role of Afterpay, how Afterpay payments are made, and other considerations.

Afterpay’s Role

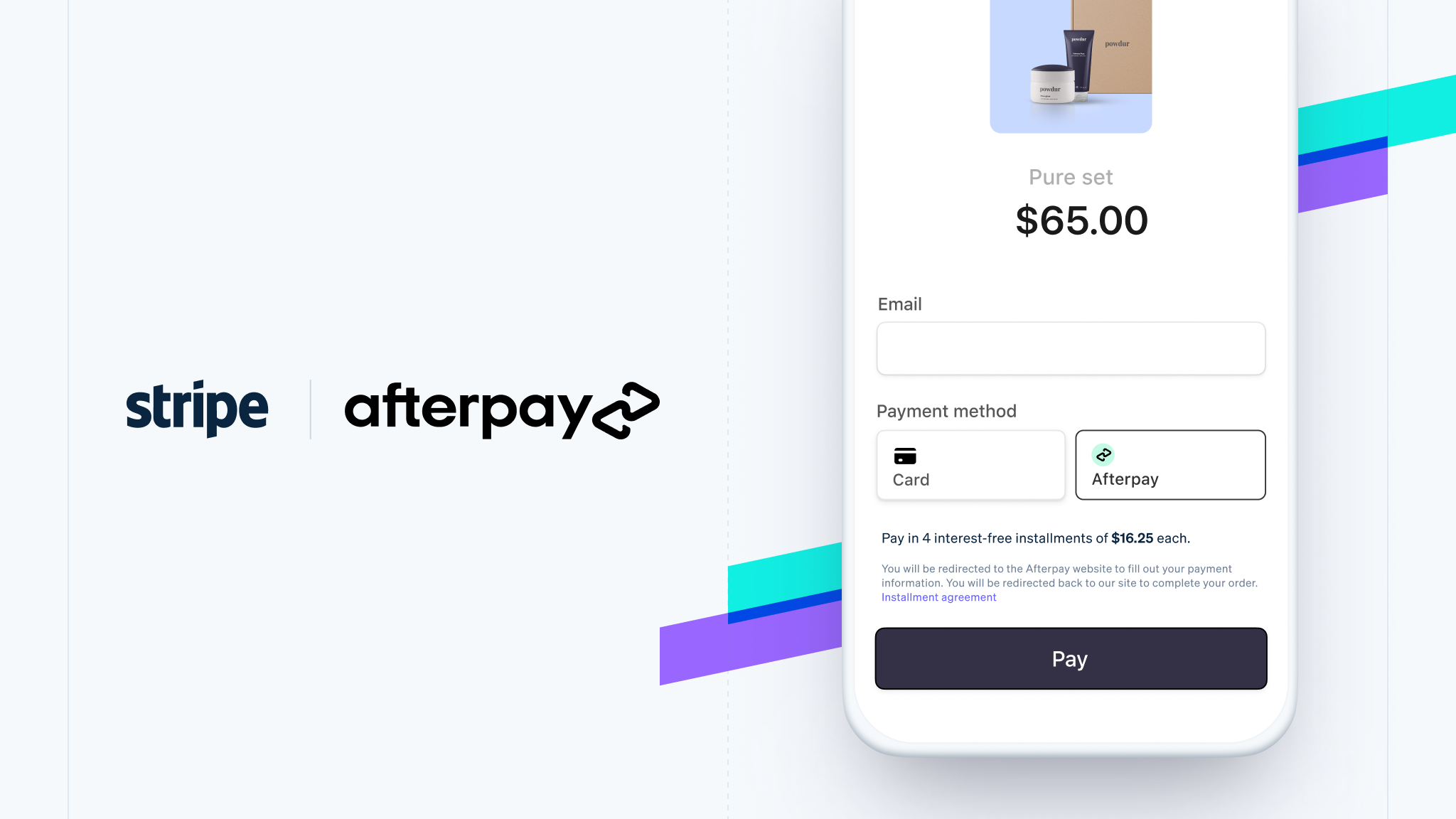

Afterpay is meant to serve as a mediator between the merchant and the customer. It pays the merchant for the cost of the goods sold, but then you owe Afterpay and have to pay them back.

Payments are divided into four installments, payable every two weeks. Customers are given a total of six weeks or a month and a half from the date of the purchase to pay the full balance. No interest payments or fees are charged upon purchase for as long you pay the full balance on time. Failure to pay the full balance on time will result in late fees.

It’s important to note that once the item or service is delivered, you will no longer be transacting with the merchant. By the time you have checked out from the online store, Afterpay has already paid for the full amount of your transaction. All of your subsequent payments should be made to Afterpay since your debt is already with them. This transfers payment risks from the merchant and onto Afterpay.

Process

Before you can use Afterpay, you need to sign up on their website. Part of the steps will be that the program will ask you to link up an active credit card or bank card. These will be used to fund the installments that you need to make to Afterpay.

After you’ve signed up for Afterpay, you can browse online stores that support it. Afterpay also has its own shopping portal within its app. When you’re ready to make a purchase, simply select Afterpay as your payment option. However, just make sure that the shop or online store supports Afterpay. Otherwise, you have to pay the full amount.

The online platform or app will automatically calculate the initial amount that you have to pay. After you’ve paid that amount, you can check out and wait for your item to be delivered. Naturally, you still have to pay the rest of the balance within eight weeks and Afterpay will help you with that. It offers automatic deductions from your card on the due dates. It also offers to send you reminders before it deducts the installments.

Penalties

Afterpay is a convenient way to get access to goods and services. However, it comes at a risk. If you fail to pay the total balance by the end of eight weeks, they will begin charging you late fees.

The late fees depend on the total amount of the order and the time elapsed since the due date. Afterpay follows a standard rule when it comes to late fees. They charge no more than 25 percent of the original cost for late fees regardless of how large the transaction is. They also charge an additional USD 7 if you haven’t paid one week after the original due date.

Spending Limits

Afterpay knows that its buy-now-pay-later scheme makes it vulnerable to overspending. As such, they have put in mechanisms to prevent it. For any single transaction, you can only purchase items or services that cost up to USD 1,500. They have also set a limit for outstanding balances at USD 2,000. Afterpay will disallow any purchase if you reach this mark until you’ve paid off the total balance.

What Can You Purchase With Afterpay?

Afterpay is useful for paying off any service or item, big or small. The only condition for the purchase is that it has to be below USD 1,500 for any single item or service. But of course, this type of payment service is always more advantageous when you’re purchasing something expensive, or something that you ideally pay for in smaller increments. Let’s say you purchased a plane ticket worth USD 1,000. With Afterpay, you can get your tickets right away as long as you pay up the initial installment (approximately USD 125). After that, you have eight weeks to complete the payment.

How Does Afterpay Make Money?

Afterpay doesn’t charge customers with interest fees and set charges. Instead, it earns its profits mostly from fixed charges on the merchant side, plus penalties for customers who fail to pay on time. More than eighty percent of its profits come from merchants’ fees, which are fixed charges set against merchandise and services being sold. There are the late fees, which account for nearly 20 percent of the company’s annual revenues. Here’s how that works:

Merchants’ Fees

As a payment service, the main customer of Afterpay is actually the merchants and not the buyers. It charges merchants a fixed fee of USD 0.30 per transaction, plus a commission of anywhere between 3% and 7% on each sale.

As you can imagine, this equates to a bit of a loss in revenue for the merchant. Any item that costs USD 50 with a commission of 5 percent automatically leads to a loss of UD 2.8 for that transaction. These charges are a little bit steeper than what some banks and credit card companies charge for their payment services, but later on, we’ll explain the benefits that offset the small losses that merchants have to take.

Late Fees

Another way that Afterpay generates revenues is by charging late fees. The actual charges depend on the original cost of the item or service. It also takes into account the time elapsed since the original due date. Here are the terms for late fees:

- For items or services that cost at or below USD 40, a maximum late fee of USD 10 will be charged.

- For any item or service that costs between USD 40 and below USD 272, a maximum of 25% of the original order will be charged.

- For items or services that cost above USD 272, a maximum late fee of USD 68 will be charged.

We know that the merchants’ fees serve as the main source of profit for Afterpay, and they use it to maintain their online platforms, but why is there a need for late fees? One way to look at late fees is as compensation to the payment service for breaching the agreement on your end. You can also think of it as a charge to extend the time you have to pay up your balance. It’s one way of extending credit, so the transaction will not be recorded negatively on your payment card. It also serves as a good source of revenue for Afterpay.

Afterpay: Advantages and Disadvantages

Afterpay is part of a larger buy-now-pay-later market that is expected to evolve rapidly within the next decade. The growth of the platform is majorly attributed to the unique benefits that it offers to its users. The benefits extend not only to the merchants but also to the customers of those merchants. Let’s take a look at some of the advantages and disadvantages of Afterpay.

Advantages: Merchants

Despite the costs that come with an Afterpay account, it offers a lot of advantages. The first advantage is that Afterpay assumes all payment risks. It pays the merchant the total cost of the item or service quickly and upfront. This removes the risk of default or fraud from the hands of the merchant to Afterpay.

The payment service also helps merchants increase their conversion rate by about 20 percent on average. The buy-now-pay-later scheme encourages customers to make purchases right off the bat. It also reduces the chances of customers abandoning the transaction. Afterpay may also increase customer satisfaction since they are able to pay at a more leisurely pace. By offering this payment solution, merchants can set themselves apart and encourage customers to come back for more. It’s also easy to set up Afterpay on online and shopping apps.

Advantages: Consumers

On the consumer side, Afterpay offers a faster and cheaper way access goods and services. Customers are able to receive the item or service right away without paying the full cost upfront. It spreads out the payments across four installments, which makes it easier to pay. On top of that, Afterpay doesn’t charge any interest rates or fees for the service. The commissions and fees used to maintain the platform are carried by the merchants.

Afterpay and other BNPL services also serve as an alternative for people who can’t qualify for credit cards or other banking services. It’s useful for people who need to purchase their necessities but can’t present the full amount upfront. It’s also useful in situations when the item or service is too expensive to cover in a single transaction (i.e., a car, a computer, a piece of furniture).

If you want to save a lot of money while online shopping, another effective strategy would be to use coupons. Check out this list of the best coupon websites to help you get discounts on nearly everything.

Disadvantages

While spreading out payments is convenient, it does come with risks. The most obvious risk relates to penalties due to late payments. If you don’t pay on time for whatever reason, you will be charged extra for the transaction.

There’s also the risk of having a harder time returning an item or canceling a transaction. In the case of Afterpay, they accept returns but take longer than normal to process requests. They still have to check with the merchant if they have received the item in good condition, and so on.

But the most dangerous risk is when customers overspend. Since you are not paying for the full amount outright, it can be easy to overestimate your capability to pay. As with credit card debt, it’s easy to fall into the hole of piling debt. It is for this reason that the company has established spending limits for individual accounts.

How to Shop with Afterpay

There are two parts to using Afterpay. You’ll first need to sign up for the service and link an active payment card to the service. After that, you can start browsing for items and services online.

Signing Up

Naturally, the first step is to become an Afterpay member. To do this, you’ll have to visit the Afterpay website or download the Afterpay mobile app and then register from there. To qualify, you need to be at least 18 years old and have an active credit card that you can link to your account. During the sign-up, you’ll be asked to provide your full name, email address, phone number, and an ID for the website. Then, you can begin shopping.

Afterpay Card

Afterpay is now offering its own version of a credit card called the Afterpay card. The card will allow you to shop in brick-and-mortar shops using Afterpay. Essentially, you just need to present the card in any store that supports Afterpay. If the store accepts it, you’ll only have to pay a quarter of the total cost in-store. The rest of your balance will have to be paid online. It’s meant to replace Afterpay’s current barcode system, which phases out during the second half of 2021.

There are other mobile payment apps that you can use to pay for your goods, but they do not offer payments in installments like Afterpay. Here are some of the best mobile payment apps that you can use for contactless payments.

Online Shopping

Once you have an Afterpay account, you can start shopping online. Afterpay is supported by thousands of online retailers, including big names like eBay, Nike, Urban Outfitters, and so much more. Discover your favorite stores that support Afterpay with this comprehensive list. Once you’re ready to make a purchase, add the item to the cart and select Afterpay as your payment method.

After you’ve selected Afterpay as your payment method, it should automatically divide the total cost into four installments. Follow through the checkout process and accept the deduction of the first installment from your payment card. After you have paid for the initial installment, the online store will ask you to fill in your delivery details.

Afterpay Notifications

The Afterpay online portal and app are also useful for more than just shopping. From there, you can check all your payment schedules and the total unpaid balance. Simply click on the Payment Schedules tab. You can also set the app to send you reminders a few days before an installment due date. The program will send reminders either via email or pop-up notifications on your phone.

Afterpay also offers its own automatic payments system. The way this works is that Afterpay automatically deducts the installment amount from your payment card on the due date. For example, let’s say that your installment fee for each of the three installments is USD 3o. You can then give Afterpay permission to deduct just that amount until you’ve paid the full amount.

Final Thoughts on Afterpay

Afterpay wasn’t always as in-demand as it is today. In fact, it may have only gained popularity once it spread to the UK and the US. Ever since that move, the payment service has become a global phenomenon embraced by mainstream brands across the industry. Its excellent payment strategy offers a lot of benefits for both sides of the transaction. And its integration with so many mainstream brands has made it the leading BNPL service in the world.

Afterpay has reimagined payment systems and the way consumers and merchants interact. It’s a brand that seeks to lessen the financial burden on the consumers while at the same time, protecting merchants from risks. This is a brand the consumers and merchants love and will continue to rely on long into the future.

If you enjoyed this article, you might also be interested in reading about the best e-commerce trends to look out for in 2021.