Introduction

In today’s modern world, technology has revolutionized the way we shop, pay for goods and services, and manage our finances. Among the various innovative financial solutions that have emerged, Afterpay has gained significant popularity, providing a convenient and flexible alternative to traditional credit. However, customers may find themselves questioning why their Afterpay credit limit has suddenly been lowered.

Understanding the factors that influence changes in your Afterpay credit limit can help shed light on this situation. In this article, we will explore the reasons why Afterpay may lower your credit limit and provide insights on how to potentially address this issue.

Before diving into the specific factors that can lead to a decrease in your Afterpay credit limit, it’s important to have a clear understanding of what Afterpay is and how it works.

Afterpay is a buy-now-pay-later service that allows customers to make purchases and pay them off in four interest-free installments. It offers a convenient alternative to traditional credit cards, as it does not require a credit check or charge any interest on repayments.

With Afterpay, customers can enjoy the convenience of splitting their payments over time without incurring any additional costs – as long as they make their payments on time. Many people appreciate the financial flexibility and budgeting benefits that Afterpay provides.

However, it’s essential to keep in mind that Afterpay, like any other financial service provider, has certain criteria and risk assessment measures in place to ensure responsible lending practices. This includes periodically evaluating and adjusting customers’ credit limits based on various factors.

Now that we have a basic understanding of Afterpay, let’s dive into the factors that can potentially lead to a decrease in your credit limit.

Understanding Afterpay

Before delving into the reasons behind Afterpay lowering your credit limit, it is crucial to have a clear understanding of how Afterpay operates and what it offers to consumers.

Afterpay is a popular payment platform that allows customers to make purchases and split their payments into four equal installments. This service has gained widespread popularity due to its convenience and flexibility, making it an attractive alternative to traditional credit cards.

One of the main advantages of Afterpay is that it does not charge any interest on repayments. As long as the customer makes their payments on time, they will not incur any additional fees. This feature has made Afterpay particularly appealing to budget-conscious consumers who want to spread out their payments without the burden of accruing interest charges.

Another key aspect of Afterpay is its simplicity and easy accessibility. Unlike traditional credit cards that require a lengthy application process and credit checks, Afterpay does not perform a credit check when customers sign up for the service. This means that individuals with limited or no credit history can still access Afterpay and enjoy its benefits.

Afterpay also offers a seamless shopping experience, both online and in-store. Customers can choose Afterpay as their payment option during the checkout process and pay the first installment upfront, while the subsequent payments are automatically deducted from their linked account or card on a scheduled basis.

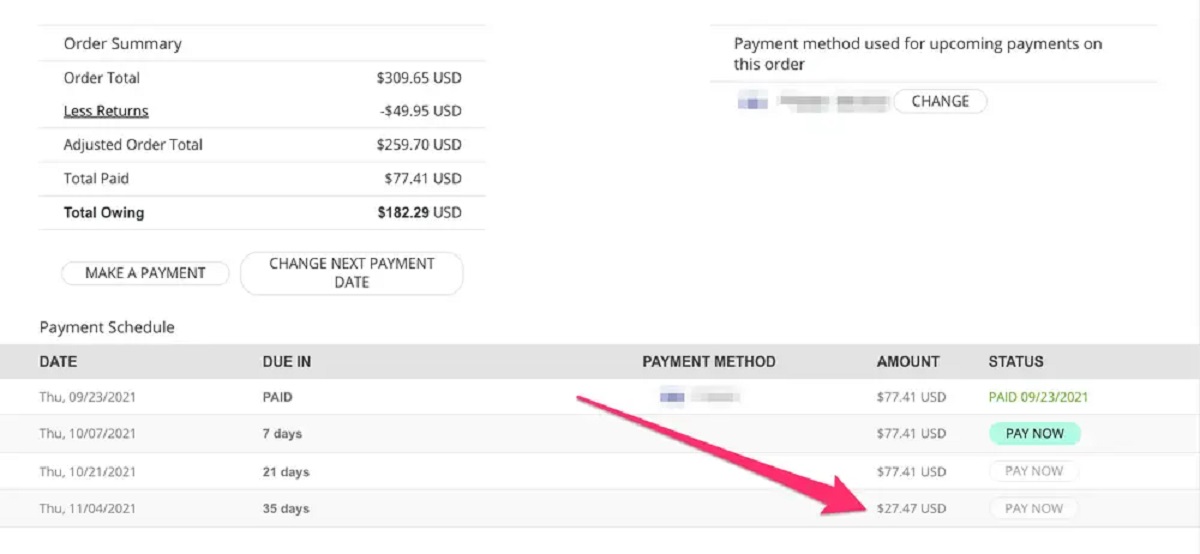

It is important to note that Afterpay is not a free pass to unlimited spending. While it may not charge interest or fees for timely repayments, late fees may apply if a payment is missed or delayed. These fees can vary depending on the country and the specific terms agreed upon at the time of signing up for Afterpay.

Overall, Afterpay is designed to provide consumers with greater financial flexibility and the ability to manage their purchases more effectively. However, it is essential to utilize Afterpay responsibly and understand the factors that can impact your credit limit.

What is a credit limit?

A credit limit refers to the maximum amount of credit that a lender or financial institution is willing to extend to a borrower. It represents the upper threshold of funds that a borrower can access through a credit card, line of credit, or a buy-now-pay-later service like Afterpay.

When it comes to Afterpay, your credit limit determines the maximum amount you can spend using the service. It is important to note that the credit limit is not a fixed amount but is subject to change based on various factors.

The credit limit is determined by Afterpay based on their risk assessment model, which takes into consideration numerous factors, including your financial history, payment behavior, income, and employment status. The goal of setting a credit limit is to ensure responsible lending and help customers manage their payments responsibly.

Your credit limit acts as a safeguard to prevent excessive spending and potential financial strain. It is designed to protect both you as the customer and Afterpay as the service provider. By setting a reasonable credit limit, Afterpay aims to promote responsible spending habits and minimize the risk of customers accumulating unmanageable debt.

Understanding your credit limit is crucial to effectively managing your finances and utilizing Afterpay wisely. It is important to keep in mind that your credit limit is not a reflection of your worth or financial stability. Instead, it is a tool put in place to ensure responsible use of credit and to help you maintain a healthy financial balance.

Knowing your credit limit can help you make informed decisions about your purchases and ensure that you stay within your means. It is advisable to keep track of your current credit limit and any changes that may occur in order to avoid any surprises or difficulties in utilizing Afterpay for your future purchases.

Now that we have a basic understanding of credit limits and their importance, let’s explore the factors that can potentially lead to a decrease in your Afterpay credit limit.

Factors that can affect your Afterpay limit

Various factors can influence Afterpay’s decision to lower your credit limit. Understanding these factors can provide insights into why your credit limit may have changed. Here are some common elements that can impact your Afterpay limit:

- Changes in spending behavior: Afterpay may evaluate your spending patterns and adjust your credit limit based on your recent purchase history. If you have been consistently spending at or near your credit limit, it may signal to Afterpay that you are potentially at risk of financial strain.

- Late or missed payments: Consistently making late payments or missing payments altogether can negatively impact your credit limit. Afterpay aims to encourage responsible repayment, and a history of missed or late payments can signal a higher risk of defaults.

- Credit history changes: If there have been significant changes in your credit history, such as the addition of new credit accounts or negative marks, Afterpay may reassess your creditworthiness and adjust your credit limit accordingly.

- Changes in income or employment status: Afterpay may consider changes in your income or employment status to determine your ability to manage repayments. If you experience a decrease in income or a change in employment, it may impact your credit limit.

- Changes in the Afterpay risk model: Afterpay regularly reviews and updates their risk model based on market conditions and internal criteria. These updates can lead to changes in credit limits for customers as Afterpay seeks to mitigate potential risks.

It’s important to note that while these factors can influence your Afterpay credit limit, not all customers will experience a decrease in their limit due to these factors. Afterpay takes a holistic approach in assessing customers’ creditworthiness, considering multiple factors to arrive at a decision.

If your Afterpay credit limit has been lowered, it doesn’t necessarily mean that you have done something wrong. It may simply be a result of Afterpay’s risk assessment process and their commitment to responsible lending practices.

Now that we understand the factors that can influence your Afterpay credit limit, let’s explore what steps you can take to request a limit increase or manage your current limit effectively.

Changes in spending behavior

One of the factors that can potentially lead to a decrease in your Afterpay credit limit is changes in your spending behavior. Afterpay closely monitors your spending patterns to assess your creditworthiness and the level of risk associated with extending your credit limit. Here’s how changes in spending behavior can impact your Afterpay limit:

Consistently maxing out your credit limit: If you frequently spend the maximum amount available on your Afterpay credit limit, it can signal to Afterpay that you may be at a higher risk of financial strain. Maxing out your credit limit regularly may indicate that you are relying heavily on credit and may struggle to make timely payments. As a result, Afterpay may choose to lower your credit limit to help you maintain a healthier balance between your income and expenses.

Excessive spending habits: If you have a history of excessive spending or making impulse purchases, it can raise concerns for Afterpay. Irresponsible spending habits can indicate a higher risk of accumulating unmanageable debt and may lead to a decrease in your credit limit.

Increased frequency of purchases: If you have significantly increased your frequency of purchases using Afterpay, it can be viewed as a potential red flag. Afterpay may interpret this as an unsustainable spending habit and adjust your credit limit accordingly to mitigate the risk.

Large purchases: Making large purchases that are close to or exceed your current credit limit can also impact your Afterpay limit. Afterpay evaluates the size of your purchases in relation to your available credit and may lower your credit limit if they deem the amount too high, especially if it surpasses your previous spending patterns.

It’s essential to remember that Afterpay’s primary concern is to ensure responsible lending and help customers avoid financial difficulties. By monitoring your spending behavior and adjusting your credit limit accordingly, Afterpay aims to assist you in managing your expenses within your means.

If you have noticed a decrease in your Afterpay credit limit due to changes in your spending behavior, it may be a sign to reassess your financial habits. Understanding your financial goals, budgeting effectively, and practicing responsible spending can help you regain confidence in managing your credit and potentially increase your credit limit over time.

Now that we’ve explored the impact of changes in spending behavior on your Afterpay credit limit, let’s move on to the next factor: late or missed payments.

Late or missed payments

Consistently making late payments or missing payments altogether can have a significant impact on your Afterpay credit limit. Afterpay places great importance on responsible repayment and is committed to ensuring that customers meet their payment obligations. Here’s how late or missed payments can affect your Afterpay limit:

Incurring late fees: When you make a payment after the due date, Afterpay may charge you a late fee. These fees can vary depending on the country and the terms agreed upon when signing up for Afterpay. Accumulating late fees can indicate to Afterpay that you may not have the necessary financial means to manage repayments effectively. This can lead to a decrease in your credit limit as Afterpay seeks to minimize the risk of defaults.

Negative impact on your credit history: Late or missed payments can also have an adverse effect on your credit history. Afterpay may report these late or missed payments to credit bureaus, potentially resulting in a negative mark on your credit report. Such negative marks can impact your creditworthiness and may lead to a decrease in your Afterpay credit limit or make it more challenging to access credit in the future.

Higher risk assessment: Consistently demonstrating a pattern of late or missed payments can raise concerns regarding your ability to manage your debts. Afterpay evaluates your payment behavior to assess the level of risk associated with extending your credit limit. If you have a history of late or missed payments, Afterpay may lower your credit limit to minimize the risk of non-payment.

It is essential to prioritize making your Afterpay payments on time. Prompt payments not only help you avoid late fees but also demonstrate responsible financial behavior to Afterpay. By consistently meeting your payment obligations, you can maintain a healthy credit limit and potentially increase it in the future.

If you have experienced late or missed payments in the past, it is crucial to assess your financial situation and make necessary adjustments. Creating a budget, tracking your expenses, and setting reminders for payment due dates can help you stay on top of your Afterpay obligations and avoid any negative impact on your credit limit.

Now that we’ve explored the impact of late or missed payments on your Afterpay credit limit, let’s move on to the next factor: credit history changes.

Credit history changes

Your credit history is an important factor that Afterpay considers when determining your credit limit. Changes in your credit history can have a direct impact on your Afterpay credit limit. Here’s how credit history changes can affect your Afterpay limit:

Addition of new credit accounts: Opening new credit accounts, such as credit cards or loans, can affect your credit limit. Afterpay takes into account your overall credit utilization and the potential impact of additional credit accounts on your ability to manage repayments. If you have recently opened multiple credit accounts, it may result in a decrease in your Afterpay credit limit as Afterpay seeks to mitigate the risk associated with increased credit utilization.

Negative marks on your credit report: If your credit report shows negative marks, such as late payments, defaults, or bankruptcy, it can impact your creditworthiness. Afterpay may review your credit history periodically and adjust your credit limit accordingly. Negative marks on your credit report can signal a higher risk of non-payment, leading to a decrease in your Afterpay credit limit.

Improvement in your credit history: On the flip side, positive changes in your credit history can have a positive impact on your Afterpay credit limit. If you have been actively working on improving your credit score and have a track record of timely payments and responsible credit management, Afterpay may recognize your efforts and potentially increase your credit limit over time.

It’s crucial to regularly review your credit report and ensure its accuracy. If you notice any errors or discrepancies, take the necessary steps to rectify them. Keeping your credit history in good shape demonstrates your financial responsibility and can positively influence your Afterpay credit limit.

While credit history is an important factor, it’s worth noting that Afterpay does not perform a hard credit check when you sign up for their service, which means that your credit score is not directly impacted by using Afterpay. However, Afterpay may report late or missed payments to credit bureaus if you fail to meet your payment obligations, which can negatively affect your credit history and limit your ability to access credit in the future.

Now that we’ve explored the impact of credit history changes on your Afterpay credit limit, let’s move on to the next factor: changes in income or employment status.

Changes in income or employment status

Changes in your income or employment status can have a significant impact on your Afterpay credit limit. Afterpay takes into consideration your ability to manage repayments based on your financial stability. Here’s how changes in income or employment status can affect your Afterpay limit:

Decrease in income: If you experience a decrease in your income, it can impact your Afterpay credit limit. Afterpay considers your income as a vital factor in assessing your ability to make timely repayments. A decrease in income may lead Afterpay to lower your credit limit to align with your current financial situation.

Change in employment status: Afterpay also takes into account your employment status when assessing your credit limit. If there has been a change in your employment, such as a job loss or a transition to a new job, it may affect your creditworthiness. Afterpay may lower your credit limit to account for the potential instability associated with a change in employment.

Unstable or irregular income: If your income is irregular or unstable, it can present challenges in managing your repayments. Afterpay evaluates the consistency and stability of your income when determining your credit limit. If your income is unpredictable, it may lead to a decrease in your Afterpay credit limit to ensure responsible lending practices.

It is essential to communicate any significant changes in your income or employment status to Afterpay. By proactively informing them of your current situation, you can potentially work together to find a solution or explore alternative options to manage your repayments effectively.

If you anticipate a decrease in income or a change in employment status, it may be prudent to reassess your financial commitments and adjust your spending accordingly. This can help you avoid any potential financial strain and ensure that you stay within your means while utilizing Afterpay.

Now that we’ve explored the impact of changes in income or employment status on your Afterpay credit limit, let’s move on to the next factor: changes in the Afterpay risk model.

Changes in the Afterpay risk model

The Afterpay risk model is a key component in determining your credit limit and assessing your creditworthiness. Afterpay regularly reviews and updates its risk model based on market conditions, industry trends, and internal criteria. These updates can have an impact on your Afterpay credit limit. Here’s how changes in the Afterpay risk model can affect your credit limit:

Market conditions and industry trends: Afterpay considers market conditions and industry trends when assessing risk. If there are changes in consumer spending behavior, economic factors, or shifts in the industry landscape, Afterpay may adjust its risk model accordingly. This can potentially lead to changes in credit limits for customers to ensure responsible lending practices.

Internal criteria and risk assessment: Afterpay’s risk model takes into account various internal criteria and risk assessment factors. These may include factors such as payment history, credit utilization, credit scores, and other indicators of creditworthiness. If there are changes or refinements in the risk model, it can impact your Afterpay credit limit as Afterpay seeks to align its lending practices with the updated criteria.

Objective of risk mitigation: Afterpay’s risk model aims to minimize the risk of non-payment and ensure responsible lending. If the risk model identifies certain patterns or trends that indicate a higher likelihood of defaults or financial strain, Afterpay may lower credit limits to mitigate potential risks and protect both the customer and the company.

It’s important to note that changes in the Afterpay risk model are not solely based on individual customer behavior but are a result of broader considerations. While these changes may lead to a decrease in your credit limit, they are implemented with the objective of maintaining a sustainable and responsible lending environment for both customers and Afterpay.

If you experience a decrease in your Afterpay credit limit due to changes in the risk model, it’s important to understand that these changes are made to ensure responsible lending practices. Assess your financial situation, adapt your spending habits accordingly, and work towards maintaining a positive credit history to potentially increase your credit limit over time.

Now that we’ve explored the impact of changes in the Afterpay risk model on your credit limit, let’s move on to the next section: how to request a limit increase.

How to request a limit increase

If you find that your Afterpay credit limit is not sufficient for your needs, you may consider requesting a limit increase. While Afterpay does not guarantee that all requests will be granted, it is worth exploring the possibility. Here are some steps you can take to request a limit increase:

- Ensure a good payment history: Before requesting a limit increase, it is crucial to demonstrate a history of responsible payments. Make sure you consistently make your repayments on time and avoid late or missed payments. A positive payment history can strengthen your case for a credit limit increase.

- Track your spending: Keep track of your Afterpay purchases and actively manage your spending. By showing that you can effectively manage your repayments and stay within your means, you can build a stronger case for a limit increase.

- Improve your credit history: Work on improving your credit history by making timely payments on all your credit accounts, including Afterpay. Maintaining a good credit history can demonstrate your creditworthiness and increase the chances of a limit increase.

- Reach out to Afterpay: Contact Afterpay’s customer support and inquire about the possibility of a limit increase. Provide them with relevant information about your financial situation, such as changes in income or employment status. Be prepared to provide any additional documentation or explanation that may support your request.

- Be patient: It’s important to understand that Afterpay evaluates limit increase requests on a case-by-case basis. They consider various factors, including your payment history, spending behavior, and overall creditworthiness. It may take some time for Afterpay to review your request and make a decision.

Remember, while requesting a limit increase can be beneficial, it is essential to carefully consider your financial situation. Requesting an increase beyond your means can lead to unnecessary debt and financial stress. Ensure that you can comfortably manage any increase in your credit limit and adjust your spending accordingly.

If your request for a limit increase is not approved, it’s important to continue practicing responsible financial habits. Focus on maintaining a positive payment history, keeping your credit utilization low, and building a stronger credit profile over time. As you demonstrate continued responsible credit usage, your chances of a future limit increase may improve.

Now that we’ve explored how to request a limit increase, let’s summarize the key points discussed in this article.

Summary

In this article, we have explored the factors that can lead to a decrease in your Afterpay credit limit and discussed how to potentially address this issue. Here are the key points to remember:

– Afterpay is a buy-now-pay-later service that allows customers to make purchases and split their payments into four interest-free installments.

– Your credit limit represents the maximum amount of credit that Afterpay is willing to extend to you.

– Afterpay may lower your credit limit based on factors such as changes in spending behavior, late or missed payments, credit history changes, changes in income or employment status, and updates to the Afterpay risk model.

– To request a limit increase, ensure a good payment history, track your spending, improve your credit history, reach out to Afterpay’s customer support, and be patient as they review your request.

It’s important to manage your Afterpay account responsibly, make timely repayments, and stay within your financial means. By doing so, you can maintain a healthy credit limit, potentially increase it over time, and continue enjoying the benefits of Afterpay’s convenient and flexible payment solution.

If you have any further questions or concerns about your Afterpay credit limit, it is advisable to reach out to Afterpay directly for personalized assistance and guidance.