Introduction

Online shopping has become increasingly popular in recent years, with consumers embracing the convenience and ease of purchasing items with just a few clicks. Alongside this trend, new payment methods have emerged to cater to the changing needs of shoppers. One such payment option is Afterpay.

Afterpay is a service that allows shoppers to make purchases and pay for them in installments, without the need for a credit card. It offers a budget-friendly alternative to traditional credit options, attracting a wide range of consumers who are looking for more flexible payment options.

In this article, we will dive into the world of Afterpay and answer some common questions, such as: What is Afterpay? How does it work? Why is Afterpay appearing on my bank statement? Is Afterpay a credit card? Can Afterpay affect my credit score? And finally, how can you use Afterpay responsibly?

Whether you are new to Afterpay or have been using it for a while, it’s important to have a clear understanding of how it works and its potential impact on your financial situation. By equipping yourself with knowledge and responsible practices, you can make informed decisions and effectively manage your Afterpay payments.

What is Afterpay?

Afterpay is a buy-now-pay-later service that allows consumers to make purchases and pay for them in an installment plan, without the need for a credit card or upfront payment. It enables shoppers to split their purchases into four equal payments, with the first payment due at the time of purchase and the remaining three payments charged every two weeks.

One of the key features of Afterpay is its simplicity and accessibility. Unlike traditional credit options, Afterpay does not require a credit application, and there are no interest charges or hidden fees if payments are made on time. It offers instant approval for eligible shoppers, making it a convenient option for those who may not have access to credit cards or prefer not to use them.

Afterpay partners with a wide range of online and offline retailers, allowing consumers to use the service to make purchases across various sectors, including fashion, beauty, electronics, and more. It has gained popularity among millennials and Gen Z shoppers who value flexibility and budget-friendly payment options.

By breaking down the total cost of the purchase into smaller, manageable payments, Afterpay aims to provide a more affordable and transparent shopping experience. It gives consumers the ability to buy desired items without straining their financial resources, making it an attractive option for both planned and impulse purchases.

Overall, Afterpay combines the convenience of online shopping with the flexibility of installment payments, offering a new way for consumers to make purchases and manage their finances. It has revolutionized the payment landscape and continues to gain traction as a preferred payment method among tech-savvy shoppers.

How does Afterpay work?

Afterpay works by allowing shoppers to split their purchases into four equal payments, which are automatically charged to their chosen payment method. Here’s a step-by-step breakdown of how Afterpay works:

- Select Afterpay at checkout: When shopping online or in-store, select Afterpay as your payment method at the checkout.

- Registration and approval: If you are a first-time user, you will need to create an Afterpay account and provide some personal and payment information. Afterpay will perform a quick eligibility check, and if approved, you can proceed with your purchase.

- Pay the first installment: At the time of purchase, you will be required to pay the first installment. This amount is typically a quarter of the total purchase price, but may vary depending on the retailer.

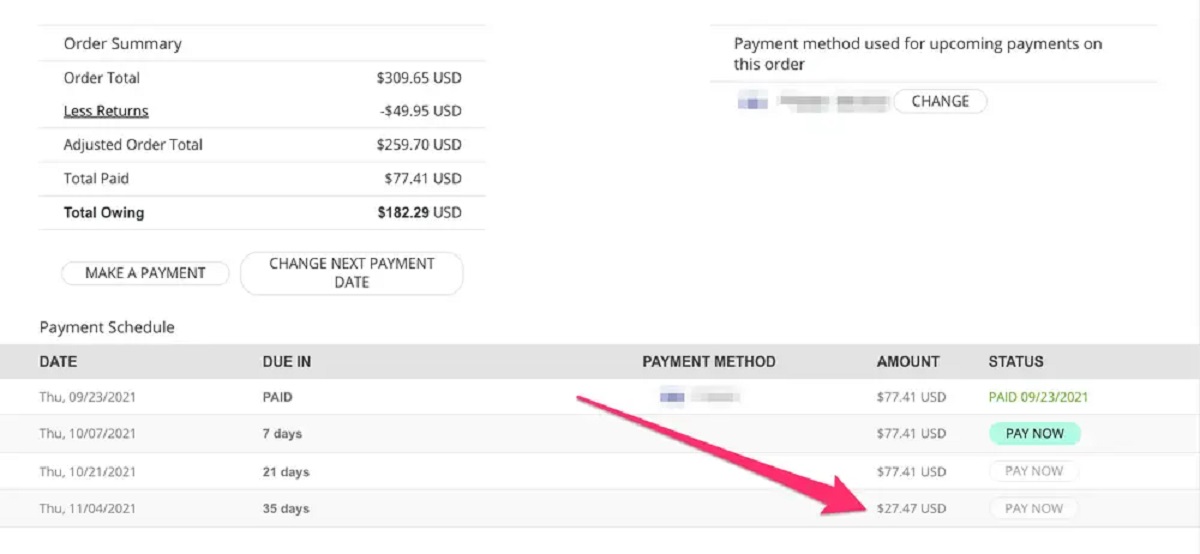

- Payment schedule: The remaining three installments will be automatically charged to your payment method every two weeks. Ensure that you have sufficient funds in your account to cover these payments.

- Managing your payments: Afterpay provides a user-friendly interface where you can manage your payments and view your payment schedule. You can also make additional payments or pay off your balance early if desired.

It’s important to note that Afterpay is a responsible lending service, and they have limits in place to ensure borrowers do not take on more debt than they can handle. The amount you can spend with Afterpay may depend on your creditworthiness and previous purchase history with the service.

In addition, Afterpay charges late fees for missed payments, so it’s vital to stay on top of your payment schedule. Late fees can vary depending on the total purchase price and the number of previous late payments. To avoid any issues, it’s recommended to link a payment method that you regularly monitor and ensure sufficient funds are available.

Overall, Afterpay simplifies the payment process by spreading out the cost of purchases over time. It offers flexibility and convenience, empowering consumers to shop responsibly while maintaining control over their finances.

Why is Afterpay appearing on my bank statement?

If you notice the name “Afterpay” appearing on your bank statement, it is likely due to a recent purchase you made using the Afterpay payment method. Afterpay works by charging your linked payment method in four equal installments, and these charges will be reflected on your bank statement.

Afterpay is designed to provide transparency in your payment history, helping you keep track of your purchases and ensuring that you are aware of the total cost of your transactions. Each installment payment will be clearly stated on your bank statement, along with the corresponding date and amount.

It’s important to review your bank statement regularly to reconcile your Afterpay payments and ensure they align with your budget and financial goals. This helps you maintain control over your spending and keep track of your financial commitments.

If you do not remember making a purchase through Afterpay or notice any discrepancies in the transactions listed on your bank statement, it is advisable to contact Afterpay customer support for assistance. They will be able to provide you with detailed information about the transactions and help resolve any issues or concerns you may have.

Remember, Afterpay is a legitimate payment service that is widely accepted by various retailers. It offers a convenient and flexible option for making purchases and managing your finances. By staying vigilant and monitoring your bank statements, you can ensure that your Afterpay transactions are accurate and in line with your purchasing activity.

Is Afterpay a credit card?

No, Afterpay is not a credit card. It is a buy-now-pay-later service that offers an alternative payment method for consumers. While both credit cards and Afterpay provide a way to make purchases without immediate payment, there are some fundamental differences between the two.

One of the main distinctions is that Afterpay does not require a credit application or a traditional line of credit. When you use Afterpay, you are essentially dividing the total cost of your purchase into four equal installments. You are not borrowing money from a lender, nor are you being charged interest on your payments.

On the other hand, credit cards involve a credit agreement with a financial institution. When you use a credit card, you are borrowing money from the card issuer to make your purchase, and you are required to repay this borrowed amount at a later date. Credit cards often come with interest charges, late payment fees, and other potential costs.

Afterpay operates on a different model. It charges late fees for missed payments, but these fees are typically lower than the interest rates associated with credit cards. Afterpay’s focus is on providing a transparent and easily manageable payment plan, making it a popular choice for consumers who prefer a more controlled means of paying for their purchases.

Additionally, Afterpay does not report your payment activity to credit bureaus, which means it does not directly impact your credit score. However, late or missed payments can be recorded and may impact your eligibility for future Afterpay purchases.

In summary, Afterpay is not a credit card. It is a convenient payment service that allows you to split your purchase into manageable installments, without the need for a credit check or a traditional credit line. It offers a flexible and budget-friendly alternative to credit cards, appealing to consumers seeking more control over their spending and payments.

Can Afterpay affect my credit score?

Using Afterpay does not directly impact your credit score. Afterpay does not conduct a credit check when you use their service, and they do not report your payment activity to credit bureaus. This means that your Afterpay transactions, whether paid on time or missed, do not appear on your credit report and do not affect your credit score.

However, it’s important to keep in mind that while Afterpay itself does not affect your credit score, it can indirectly impact your creditworthiness in certain situations. For example:

- Missed or late payments: Afterpay charges late fees for missed payments, which could accumulate if you consistently fail to make payments on time. While these fees do not directly affect your credit score, they could create financial strain and lead to difficulties in meeting other financial obligations, potentially impacting your creditworthiness.

- Limiting available credit: If you have outstanding Afterpay balances, this may affect your available credit limit if you hold a credit card or other form of credit. Lenders may take into account your existing debts when considering your creditworthiness for new credit applications.

- Future credit applications: Although Afterpay itself does not impact your credit score, some lenders may take into account your Afterpay usage when assessing your overall financial commitments. If you have significant Afterpay debt or a history of missed payments, it could potentially factor into their decision to approve or deny your credit application.

It’s important to manage your Afterpay payments responsibly and ensure that you have the funds available to meet your payment obligations. By doing so, you can avoid late fees and maintain control over your finances, which ultimately contributes to your overall financial well-being.

While Afterpay itself does not have a direct impact on your credit score, it’s crucial to be mindful of your financial responsibilities and use Afterpay in a way that aligns with your budget and financial goals. By practicing responsible financial habits, you can maintain a good credit standing and make informed decisions when it comes to managing your finances.

How can I use Afterpay responsibly?

While Afterpay offers a convenient and flexible payment option, it’s important to use it responsibly to avoid potential financial challenges. Here are some tips for using Afterpay in a responsible manner:

- Create a budget: Before using Afterpay, assess your financial situation and create a budget to determine how much you can afford to spend. Plan your purchases accordingly and ensure that the installment payments fit within your budget.

- Shop with intention: Avoid impulse purchases and only use Afterpay for items you actually need or have planned to purchase. Think about whether the item is essential and aligns with your long-term financial goals.

- Stay within your means: Be mindful of your spending limits and avoid creating unnecessary debt. Stick to purchases that you can comfortably afford to repay in installments without putting a strain on your monthly budget.

- Monitor your payments: Keep track of your Afterpay payment schedule and ensure that you have enough funds available in your account to cover the installment payments. Set reminders or use Afterpay’s mobile app to help you stay on top of your payments.

- Pay on time: Make each installment payment on time to avoid incurring late fees. Late fees can add up quickly and impact your financial stability. Prioritize your Afterpay payments and consider automating them if possible.

- Review return policies: Familiarize yourself with the return policies of the retailers you shop with using Afterpay. If you need to return an item, make sure you understand the process and any potential refunds or adjustments to your Afterpay payments.

- Keep your information secure: Protect your Afterpay account and personal information. Use strong, unique passwords for all your online accounts and be cautious of phishing attempts or suspicious requests for personal information.

- Track your overall debt: Understand your total outstanding debts, including any Afterpay balances, and regularly review your financial situation. Be aware of your overall financial obligations and manage them responsibly.

By following these tips, you can use Afterpay as a helpful tool for managing your cash flow and making purchases without relying on credit cards or impacting your credit score. Responsible usage of Afterpay allows you to enjoy the convenience of buy-now-pay-later services while maintaining control over your financial well-being.

Tips for managing Afterpay payments

Effectively managing your Afterpay payments is key to avoiding late fees and maintaining control over your finances. Here are some tips to help you stay on top of your Afterpay payments:

- Plan your purchases: Before using Afterpay, plan your purchases and ensure they align with your budget. Only buy items that you need and are confident you can afford to pay off in installments.

- Set up reminders: Use reminders on your phone or calendar to keep track of your payment due dates. Set alerts a few days before each payment to give yourself enough time to ensure funds are available.

- Link a reliable payment method: Link a payment method, such as a bank account or debit card, that you actively monitor. This will help you stay aware of the payment due dates and avoid any issues with insufficient funds.

- Create a separate account: Consider setting up a separate bank account or earmarking funds specifically for your Afterpay payments. This will help you easily track your Afterpay expenses and ensure that the necessary funds are available.

- Pay attention to transaction notifications: Keep an eye out for transaction notifications from Afterpay. These notifications will provide details on upcoming payments, giving you a heads-up and allowing you to plan accordingly.

- Avoid missed or late payments: Missing or making late payments can result in late fees and potentially impact your ability to continue using Afterpay in the future. Make it a priority to pay your installments on time to avoid any penalties or complications.

- Review your Afterpay history: Regularly review your Afterpay transaction history to ensure everything is accurate. This will help you identify any payment discrepancies or potential issues with your account.

- Communicate with Afterpay: If you are facing financial difficulties and are unable to make a payment, reach out to Afterpay. They may be able to provide assistance or work out a payment plan that suits your current financial situation.

By implementing these tips, you can effectively manage your Afterpay payments and avoid any unnecessary fees or complications. Responsible management ensures a smooth payment experience and helps you maintain financial control while utilizing Afterpay’s convenient buy-now-pay-later service.

Conclusion

Afterpay has revolutionized the way we shop by providing a convenient and flexible payment option. With its buy-now-pay-later model, it allows consumers to make purchases and pay for them in installments, offering an alternative to traditional credit cards and upfront payments.

Throughout this article, we’ve explored what Afterpay is, how it works, and its impact on bank statements. We’ve also discussed the differences between Afterpay and credit cards, as well as its potential effects on credit scores. Additionally, we’ve provided tips on using Afterpay responsibly and managing payments effectively.

Using Afterpay responsibly involves careful planning, budgeting, and staying on top of payment schedules. By establishing a clear understanding of your finances and making informed purchasing decisions, you can leverage Afterpay as a useful tool without falling into debt or compromising your financial stability.

Remember, while Afterpay can offer convenience and flexibility, it’s important to be mindful of your spending habits and financial obligations. Regularly review your Afterpay transactions, keep track of payment due dates, and communicate with Afterpay if you encounter any difficulties.

By using Afterpay responsibly, you can enjoy the perks of a pay-over-time service while staying in control of your financial well-being. As always, maintaining a balanced approach to your financial decisions and maintaining good financial habits contribute to a healthy and sustainable financial future.

So, take the leap, explore Afterpay as a payment option, and enjoy the convenience and flexibility it offers. And remember, with responsible usage, you can make the most of this innovative payment solution while keeping your financial goals on track.