Introduction

Afterpay has become a widely popular payment option for online shoppers, allowing them to make purchases and split the cost into manageable installments. It offers convenience and flexibility, making it an attractive choice for many consumers. However, what happens when you fail to make a payment on time? In this article, we will explore the consequences of not paying Afterpay and what you need to know to avoid potential pitfalls.

Understanding the implications of missing an Afterpay payment is crucial to maintaining a healthy financial standing. While it may seem like a simple oversight, neglecting to fulfill your payment obligations can result in a cascade of consequences that can impact your credit score and financial well-being.

In the following sections, we will delve into the workings of Afterpay, its payment structure, and what transpires when you fall behind on your installment plan. We will also discuss the potential late fees, penalties, and steps you can take to resolve any delinquency. So, let’s dive into the world of Afterpay and discover the repercussions of not paying on time.

What is Afterpay?

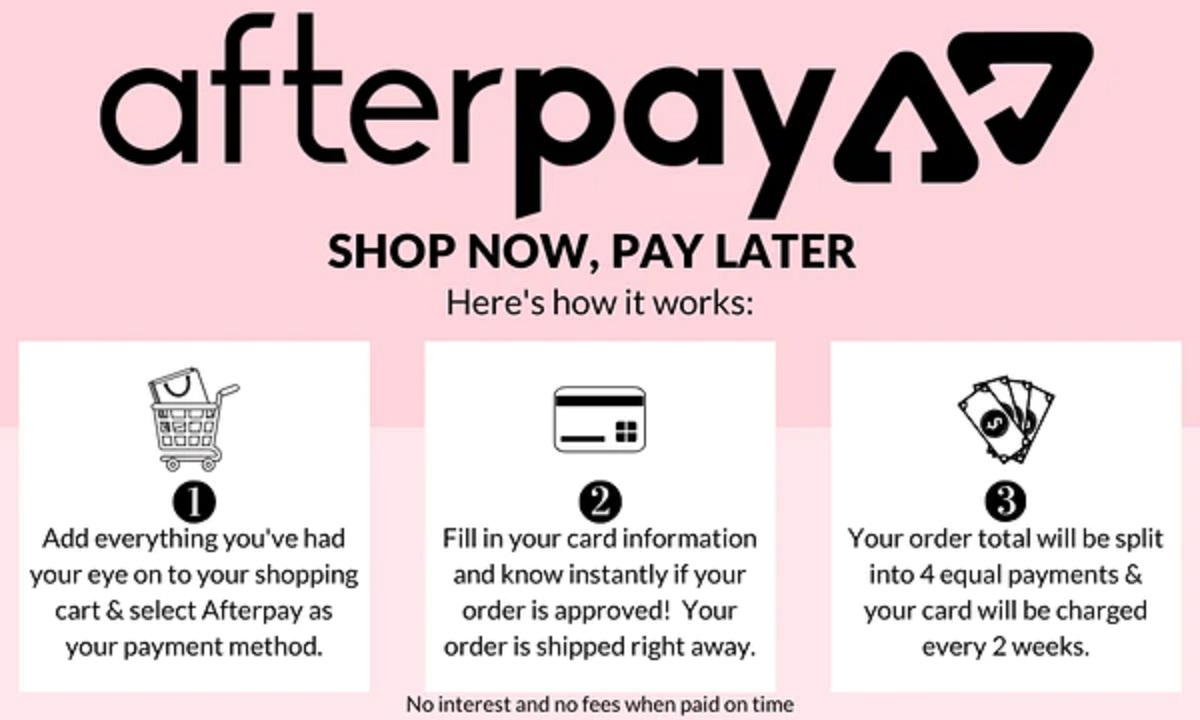

Afterpay is a financial service that allows shoppers to split their purchases into four equal installments, which are payable over a period of six weeks. It was established in Australia in 2014 and has since gained tremendous popularity around the world. Afterpay aims to provide a convenient and interest-free alternative to traditional credit by allowing customers to make purchases and pay them off in manageable installments.

The process of using Afterpay is relatively straightforward. When making a purchase online, customers can select Afterpay as their payment method at the checkout. Afterpay will then conduct a brief approval process to determine the customer’s eligibility. Once approved, the customer will pay the initial quarter of the purchase amount at the time of the transaction. The remaining three installments will be automatically deducted from the customer’s chosen payment method, typically every two weeks.

What sets Afterpay apart is its interest-free nature. While customers are required to pay the total amount, each installment is interest-free as long as it is paid on time. This allows shoppers to spread out their payments without incurring additional charges, making it an appealing option for those looking to manage their finances responsibly. However, failing to make a payment on time can lead to penalties and other consequences.

It is worth noting that Afterpay is not just limited to online shopping. In recent years, Afterpay has expanded its services to include physical retail stores, making it even more accessible to consumers. With a wide network of participating retailers, Afterpay offers customers the convenience of splitting payments for a variety of products and services, ranging from fashion and beauty to homeware and even travel experiences.

Now that we have a better understanding of what Afterpay is and how it works, let’s explore the potential ramifications of failing to make a payment on time.

How does Afterpay work?

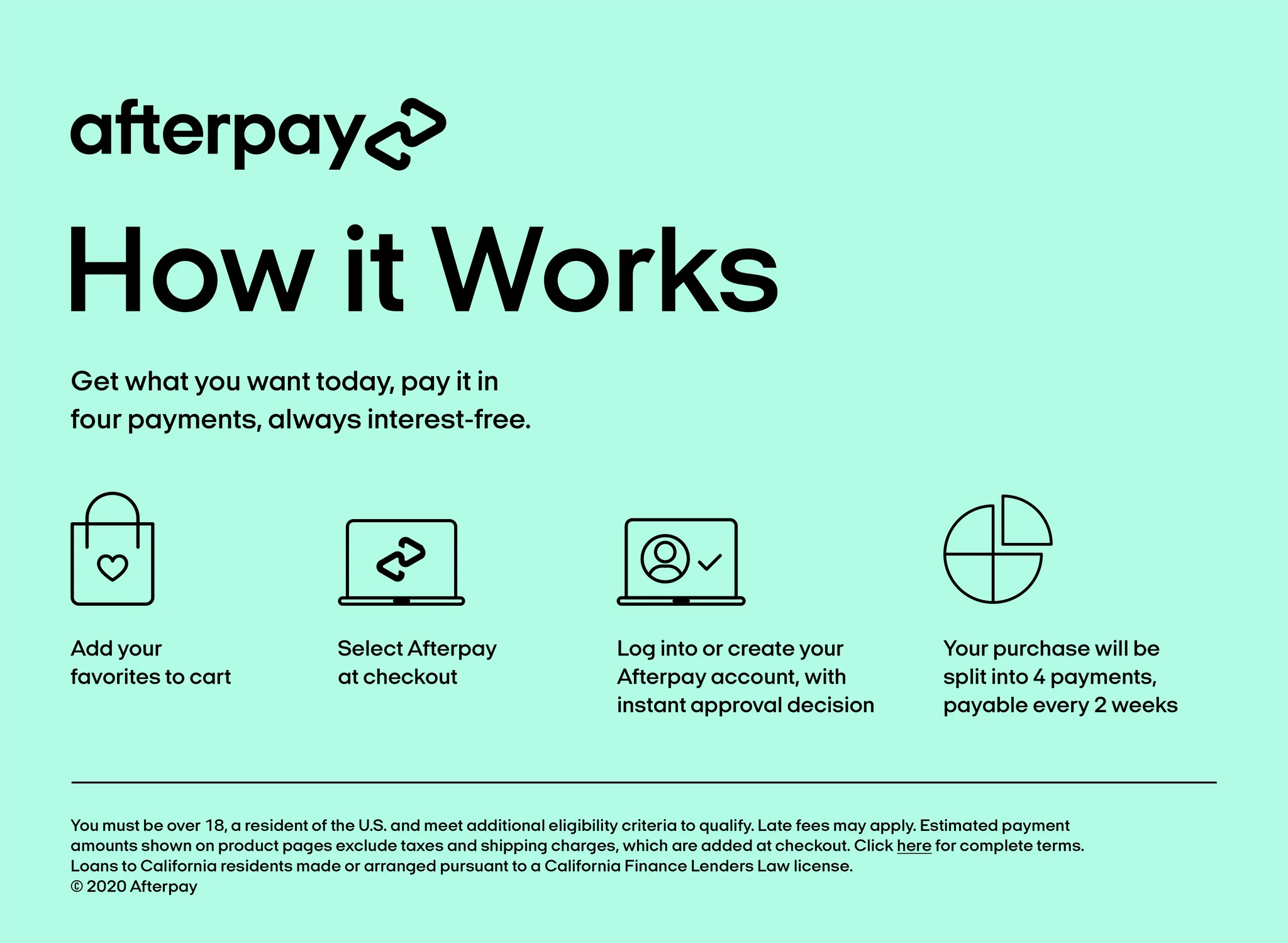

Afterpay operates on a “buy now, pay later” model, allowing customers to make purchases immediately and pay for them in installments. Here’s a step-by-step breakdown of how Afterpay works:

- Choose Afterpay as the payment method: When shopping online, select Afterpay as your payment option at the checkout. Afterpay is available on a wide range of websites and is indicated by the Afterpay logo.

- Sign up or log in to your Afterpay account: If you’re a first-time Afterpay user, you’ll need to create an account by providing some personal and financial details. Returning customers can simply log in to their existing Afterpay account.

- Complete your purchase: After selecting Afterpay as your payment method and logging in, proceed with the purchase as usual. The total amount will be split into four equal installments.

- Pay the first installment: At the time of purchase, you’ll be prompted to pay the first installment, which typically amounts to 25% of the total. This payment will be deducted immediately.

- Repay the remaining installments: The remaining installments will be automatically deducted from your linked debit or credit card every two weeks. You don’t need to manually make these payments, as Afterpay handles the process for you.

It’s important to note that Afterpay does not charge interest or fees if you make your payments on time. As long as you pay each installment by the due date, you can enjoy the convenience of spreading out your payments without incurring any additional costs.

Afterpay’s website and mobile app provide tools to help you manage your payments and keep track of your installment schedule. You can view upcoming payment dates, modify payment methods, and even make additional payments if desired. This level of transparency makes it easier to stay on top of your obligations and keep your Afterpay account in good standing.

By offering a flexible and interest-free payment option, Afterpay has gained popularity among shoppers who value convenience and budgeting control. However, it’s crucial to understand the implications of missing a payment. Let’s explore what happens when you don’t make your Afterpay payments on time.

What happens when you miss a payment?

Missing a payment with Afterpay can have several consequences that you should be aware of. While the exact policies may vary slightly depending on your location and the specific terms and conditions set by Afterpay, here are some general outcomes that can occur when you fail to make a payment on time:

- Late fees: Afterpay typically charges late fees if you miss a payment. These fees vary depending on the total purchase amount and can increase if you continue to miss subsequent payments. It’s important to note that these late fees can add up quickly and impact your overall repayment amount.

- Payment suspension: If you have missed a payment, Afterpay may suspend your account temporarily. This means you won’t be able to use Afterpay to make any further purchases until the missed payment and any associated fees are resolved.

- Communication from Afterpay: After a missed payment, Afterpay will usually reach out to you via email or SMS to inform you of the outstanding balance and any late fees incurred. It’s essential to be vigilant about checking your communication channels to ensure you stay informed about your payment obligations.

- Recurring payment attempts: Afterpay will attempt to deduct the outstanding payment and any applicable fees from your linked debit or credit card. They may continue to do so in subsequent payment cycles until the account is back in good standing. This can result in additional charges if your account lacks sufficient funds to cover the missed payment.

It’s crucial to address any missed payments with Afterpay as soon as possible to avoid further complications. Ignoring the issue may result in more significant consequences down the line, such as potential damage to your credit score or legal action.

Now that we’ve explored the potential outcomes of not paying Afterpay on time, let’s delve into some of the specific penalties and how they can affect your financial standing and creditworthiness.

Late fees and penalties

When you miss a payment with Afterpay, you can expect to incur late fees and penalties, which can quickly escalate if you continue to fall behind on your payments. Here are some important aspects to consider regarding late fees and penalties with Afterpay:

- Initial late fee: Afterpay typically charges an initial late fee if you miss a payment. This fee varies based on the amount of your purchase but is typically around $10 to $15. It’s important to note that this fee is usually added to your outstanding balance, increasing the overall amount you need to repay.

- Additional late fees: If you continue to miss payments, Afterpay may charge additional late fees for each subsequent missed payment. These fees may accumulate with each missed installment and can add up quickly. It’s crucial to stay on top of your payment schedule to avoid these additional charges.

- Penalties for non-payment: After repeated missed payments and failure to resolve your outstanding balance, Afterpay may take further action to collect the debt. This can include engaging debt collection agencies or pursuing legal action to recover the amount owed. These actions can have more severe consequences for your credit score and financial standing.

- Credit reporting: Afterpay has the ability to report your delinquent payments to credit bureaus, which can have a negative impact on your credit score. A lower credit score can make it more challenging to obtain credit or favorable loan terms in the future.

It’s important to note that the specific late fees and penalties may vary depending on your location and the terms and conditions set by Afterpay. It is advisable to review the specific details in your Afterpay agreement to understand the exact consequences of missing payments.

To mitigate the impact of late fees and penalties, it is crucial to communicate with Afterpay as soon as you realize you’ll miss a payment. They may be able to provide options for repayment plans or offer guidance on resolving the outstanding balance. Being proactive and transparent about your situation can help you navigate the potential financial implications of missing a payment with Afterpay.

Now that we’ve explored the late fees and penalties that can arise from not paying Afterpay on time, let’s examine how missing payments can affect your credit score and financial future.

Impact on credit score

Missing payments with Afterpay can have a significant impact on your credit score. While Afterpay itself does not directly report to credit bureaus, they have the option to do so if you fail to resolve your outstanding balance. Here’s how missing payments with Afterpay can affect your credit score:

- Credit reporting: Afterpay has the ability to report late or missed payments to credit bureaus, such as Equifax or Experian, depending on your location. Once reported, this negative information can remain on your credit report for up to seven years, potentially lowering your credit score.

- Credit score impact: Missed payments and delinquent accounts can have a significant negative impact on your credit score. Your credit score is a numerical representation of your creditworthiness, and a lower score can make it more difficult to obtain credit in the future or may result in higher interest rates on loans.

- Limited credit access: If your credit score decreases due to missed Afterpay payments, it can become more challenging to secure loans, credit cards, or favorable terms for financial products. Lenders may view you as a higher risk borrower and may be hesitant to offer credit to individuals with a history of late payments.

- Future financial implications: A negative credit history can have long-term consequences. It can impact your ability to rent an apartment, get approved for a mortgage, or even secure employment in certain industries that conduct credit checks.

It’s crucial to understand that your credit score is influenced by various factors, and missing payments with Afterpay is just one piece of the puzzle. However, it’s essential to be proactive in resolving any outstanding balances and communicating with Afterpay to avoid potential credit score damage.

If you do find yourself in a situation where you’ve missed payments and have negative information on your credit report, it is not the end of the road. Taking steps to improve your credit habits, such as making timely payments and reducing your overall debt, can help rebuild your creditworthiness over time.

Now that we’ve explored the impact of missed payments on your credit score, let’s discuss the potential debt collection and legal consequences of not paying Afterpay.

Debt collection and legal consequences

When you fail to make payments with Afterpay, it can lead to debt collection efforts and potential legal consequences. While Afterpay generally tries to work with customers to resolve outstanding balances, repeated missed payments can result in more severe actions being taken. Here’s what you need to know about debt collection and legal consequences related to not paying Afterpay:

- Debt collection agencies: After a certain period of non-payment, Afterpay may engage a debt collection agency to recover the outstanding balance. Debt collectors are experienced in recouping debts and may use various methods to collect the money owed, including phone calls, letters, and even legal action.

- Legal action: If efforts to collect the debt through a collection agency are unsuccessful, Afterpay may decide to pursue legal action against you. This can result in a court judgment against you, potentially leading to wage garnishment, asset seizure, or liens on your property.

- Additional costs: If legal action is taken, you may be responsible for the costs associated with the legal proceedings. This can include attorney fees, court fees, and other expenses incurred during the collection process.

- Impact on future credit: A judgment or legal action resulting from non-payment can have a significant negative impact on your credit score. It can further hinder your ability to secure credit in the future, as lenders may view you as a higher risk borrower.

It’s important to address any delinquencies as early as possible to avoid escalating the situation. If you are experiencing financial difficulties, it’s recommended to reach out to Afterpay and discuss your situation. They may be willing to work out a repayment plan or alternative solution that can help you avoid debt collection and legal consequences.

Remember, avoiding or ignoring the issue will not make it go away. It’s crucial to take proactive steps to address any missed payments and communicate openly with Afterpay to find a resolution that works for both parties.

Now that we’ve explored the potential debt collection and legal consequences of not paying Afterpay, let’s discuss the options available to resolve delinquency and avoid further complications.

Options for resolving delinquency

If you find yourself in a situation where you have missed payments with Afterpay, it’s important to take proactive steps to resolve the delinquency. Here are some options for addressing the outstanding balance and avoiding further complications:

- Contact Afterpay: The first step is to reach out to Afterpay as soon as you realize you’ve missed a payment. Explain your situation honestly and ask for guidance on how to resolve the outstanding balance. Afterpay may be willing to work with you to create a repayment plan that suits your financial circumstances.

- Create a budget: Assess your financial situation and create a budget to manage your expenses. By allocating funds specifically for your Afterpay payments, you can ensure that you meet your obligations going forward. Adjusting your spending habits and cutting back on non-essential expenses can also free up money for repayment.

- Consider payment assistance programs: Some countries and organizations offer payment assistance programs for individuals facing financial hardship. These programs can provide temporary relief by reducing or suspending payments for a certain period. Research if such programs are available in your area and if you qualify for assistance.

- Explore debt consolidation: If you have multiple debts, including Afterpay, consolidating your debts into one manageable payment can simplify your financial situation. This can be done through a personal loan or a debt consolidation program. However, it’s important to carefully consider the terms, interest rates, and any fees associated with consolidation.

- Seek professional advice: If you are facing significant financial difficulties and are unsure how to proceed, it may be beneficial to consult with a financial advisor or credit counselor. They can provide personalized guidance and assist in creating a repayment plan that aligns with your financial goals.

Remember, taking action and addressing the delinquency promptly is crucial to avoiding further consequences. Ignoring the issue will only exacerbate the situation and potentially lead to debt collection efforts or legal action.

By proactively communicating with Afterpay, creating a plan to manage your payments, and exploring available options, you can work towards resolving the delinquency and improving your financial standing. It’s important to learn from this experience and develop healthy financial habits to avoid similar situations in the future.

Now that we’ve explored the various options for resolving delinquency, let’s wrap up the article and summarize the main points discussed.

Conclusion

Afterpay offers a convenient “buy now, pay later” option for online shoppers, allowing them to split their purchases into manageable installments. However, failing to make payments on time can lead to a cascade of consequences that can impact your financial well-being. It’s crucial to understand the potential ramifications of missing Afterpay payments and take proactive steps to address any delinquency.

Late fees and penalties are common when payments are missed with Afterpay. These fees can accumulate quickly, increasing the overall amount you owe. Additionally, repeated missed payments can result in the suspension of your Afterpay account and communication from debt collection agencies. There is also the possibility of legal action being taken against you, which can have significant financial and credit-related implications.

Missing Afterpay payments can also have a negative impact on your credit score, potentially making it harder to obtain credit in the future. Furthermore, it is important to promptly address any delinquency to avoid further complications and explore options for resolution.

By contacting Afterpay, creating a budget, exploring payment assistance programs, considering debt consolidation, or seeking professional advice, you can take the necessary steps to resolve the delinquency and improve your financial standing. It is important to develop healthy financial habits to avoid similar situations in the future.

Remember, staying informed about your payment obligations, maintaining open communication with Afterpay, and being proactive in resolving any missed payments are key to avoiding potential negative consequences. By taking responsibility for your financial commitments, you can navigate the world of Afterpay more effectively and make the most of its convenient payment options.