Introduction

Welcome to the digital age, where technology has revolutionized the way we live and do business. With advancements in connectivity and data exchange, businesses are increasingly vulnerable to cyber threats. From data breaches to ransomware attacks, the risk of cyberattacks is a real and constant concern for organizations of all sizes.

As a result, the need for cybersecurity measures has become paramount. However, despite investing in robust security systems and protocols, no company is immune to the ever-evolving nature of cyber threats. That is where cybersecurity insurance comes into play.

Cybersecurity insurance, also known as cyber insurance or cyber risk insurance, is a specialized type of insurance that provides financial protection to businesses in the event of a cyber incident. It is designed to help companies manage the costs associated with a data breach, cyber extortion, network damage, and other cyber-related losses.

Throughout this article, we will explore the world of cybersecurity insurance and why it has become an essential component of every company’s risk management strategy.

With the increasing frequency and sophistication of cyber attacks, organizations must be proactive in mitigating their potential impact. While preventive measures such as firewalls, encryption, and employee training are crucial, they are not foolproof. Cybersecurity insurance acts as a safety net, offering financial resources to cover the costs of recovery, legal expenses, public relations, and business interruption. It can assist businesses in minimizing the financial and reputational damage that can result from a cyber incident.

Whether your business is a small startup or a large enterprise, cybersecurity insurance should be on your radar. In the next sections, we will delve deeper into the different types of cybersecurity insurance coverage, how it works, factors to consider when purchasing a policy, and the benefits it can provide to your organization.

What is Cybersecurity Insurance?

Cybersecurity insurance is a specialized type of insurance designed to protect businesses from the financial consequences of cyber threats and attacks. It provides coverage against various cyber risks, including but not limited to data breaches, theft of sensitive information, ransomware attacks, business interruption, and liability arising from a cyber incident.

Unlike traditional insurance policies that focus on physical risks such as property damage or bodily injury, cybersecurity insurance addresses the unique risks associated with digital assets and information. It acknowledges the growing prevalence of cyberattacks and the potentially devastating impact they can have on businesses.

Cybersecurity insurance policies typically offer a range of coverage options tailored to the specific needs of businesses. Common coverage elements include:

- Data breach response: This coverage helps businesses navigate the aftermath of a data breach, including forensic investigations, legal assistance, public relations support, and credit monitoring services for affected individuals.

- Business interruption: If a cyberattack disrupts your operations, this coverage can provide financial compensation for lost revenue, extra expenses incurred as a result of the incident, and ongoing expenses during the recovery period.

- Network security liability: This coverage protects your organization against claims of third-party damages resulting from a security breach or privacy violation.

- Cyber extortion: If your business becomes a victim of ransomware or cyber extortion, this coverage can help cover the costs associated with negotiating and paying the ransom, as well as the expenses to restore your systems.

- Errors and omissions: This coverage protects businesses that provide technology services or handle sensitive data from allegations of negligence or failure to provide adequate security.

It is important to note that cybersecurity insurance does not replace the need for implementing strong cybersecurity measures. It should be considered as part of a comprehensive cybersecurity strategy that includes preventive measures such as firewalls, strong access controls, regular data backups, and employee training on cybersecurity best practices. Insurance acts as a safety net to help businesses recover and minimize financial losses when preventive measures fall short.

Next, we will explore why businesses need cybersecurity insurance and the potential benefits it can provide.

Why Businesses Need Cybersecurity Insurance

In today’s digital landscape, cyber threats pose significant risks to businesses of all sizes and industries. To understand how organizations can safeguard themselves financially against online threats, exploring what cybersecurity liability becomes a pivotal aspect of modern risk management strategies. The consequences of a successful cyberattack can be devastating, ranging from financial losses to reputational damage and legal liabilities. Here are several reasons why businesses need cybersecurity insurance:

1. Financial Protection:

Cybersecurity incidents can result in substantial financial burdens for businesses. Data breaches can lead to costs associated with notifying affected individuals, providing credit monitoring services, conducting forensic investigations, and implementing security measures to prevent future incidents. Cybersecurity insurance offers financial protection by covering these costs, helping businesses to mitigate the financial impact of a cyber incident.

2. Business Continuity:

Cyberattacks can disrupt business operations, leading to revenue loss and reputational damage. With cybersecurity insurance, businesses can access coverage for business interruption, which provides compensation for the income lost during the time it takes to recover from a cyber incident. This financial support enables organizations to maintain their operations and ensure continuity while dealing with the aftermath of an attack.

3. Legal Liabilities:

A cyber incident can result in legal consequences, such as lawsuits from affected customers or regulatory fines for non-compliance with data protection regulations. Cybersecurity insurance includes liability coverage, which helps businesses address legal costs and damages arising from third-party claims related to a cyber incident. This coverage provides peace of mind and protects businesses from the potential financial ruin that legal liabilities can bring.

4. Reputation Management:

The damage to a company’s reputation following a cyber incident can be long-lasting and difficult to recover from. Cybersecurity insurance can cover the costs associated with reputation management efforts, including public relations services, crisis communication, and advertising campaigns to restore trust and demonstrate commitment to cybersecurity. Having this coverage allows businesses to proactively manage their reputation and rebuild customer confidence.

5. Compliance Requirements:

Many industries have strict regulatory requirements regarding data protection and cybersecurity. Cybersecurity insurance can help businesses meet these compliance obligations by providing coverage for expenses related to compliance audits, security improvements, and incident response plans. This coverage ensures that businesses can meet regulatory requirements and avoid penalties or other legal consequences.

By investing in cybersecurity insurance, businesses can protect themselves from the financial and operational impact of cyberattacks. However, it is essential to carefully assess policy terms, coverage limits, and exclusions to ensure that the insurance aligns with the specific needs and risks of your organization.

In the next section, we will explore the types of cybersecurity insurance coverage available to businesses.

Types of Cybersecurity Insurance Coverage

Cybersecurity insurance policies offer various types of coverage designed to address the specific risks and needs of businesses in the face of cyber threats. Here are the primary types of cybersecurity insurance coverage:

1. First-party Coverage:

This type of coverage is focused on protecting the insured business itself. It includes coverage for expenses incurred as a result of a cyber incident, such as:

- Data breach response: This coverage helps businesses manage the costs associated with investigating and responding to a data breach, including legal assistance, forensic investigations, notifying affected individuals, credit monitoring services, and public relations efforts.

- Business interruption: Business interruption coverage compensates for the financial losses resulting from the disruption of normal business operations due to a cyber incident.

- Cyber extortion: This coverage protects against the costs associated with responding to cyber extortion, including ransom payments, expenses related to negotiating with attackers, and investigation costs.

2. Third-party Coverage:

This type of coverage is designed to protect businesses from liabilities arising from a cyber incident. It includes coverage for claims made by third parties, including:

- Network security liability: This coverage protects against claims for third-party damages resulting from a security breach or privacy violation.

- Media liability: Media liability coverage applies to claims related to defamation, infringement of intellectual property, or plagiarism that occurs online.

- Errors and omissions: This coverage protects businesses that provide technology services or handle sensitive data from claims of negligence, errors, or omissions in delivering these services.

3. Cyber Crime Coverage:

Cyber crime coverage focuses on protection against financial losses resulting from criminal activities, such as:

- Fraud and social engineering: This coverage protects against losses resulting from fraud or social engineering schemes, where cybercriminals deceive employees into transferring funds or disclosing sensitive information.

- Electronic transfer fraud: This coverage applies to losses resulting from unauthorized electronic transfers of funds.

- Identity theft: Identity theft coverage protects against losses resulting from the theft or misuse of personal information.

It’s important for businesses to carefully review and understand the coverage options provided by different cybersecurity insurance policies. Examining the specific risks and needs of your organization can help you determine the appropriate combination of coverage types. Consulting with an insurance professional or cybersecurity expert can further assist you in selecting the right coverage for your business.

Next, we will explore how cybersecurity insurance works and the factors to consider when purchasing a policy.

How Cybersecurity Insurance Works

Cybersecurity insurance works similarly to other types of insurance policies. Here are the key aspects of how cybersecurity insurance operates:

1. Policy Purchase:

Businesses start by identifying their cybersecurity risks and determining the coverage they need. They then reach out to insurance providers specializing in cybersecurity insurance to receive policy quotes. After comparing different offers, businesses select the most suitable policy and purchase it.

2. Premium Payment:

Once the policy is purchased, the business pays a premium to the insurance provider. The premium amount is determined based on various factors, including the business’s industry, size, security measures in place, and the level of coverage required.

3. Risk Assessment:

During the underwriting process, the insurance provider conducts a risk assessment to evaluate the business’s cybersecurity posture. This assessment helps determine the level of risk the business faces, ensuring that the coverage and premium are appropriate.

4. Incident Response:

In the event of a cyber incident, the business must promptly notify the insurance provider and activate the incident response process outlined in the policy. This typically includes contacting the insurer’s designated cybersecurity incident response team and following specific procedures to mitigate the damage and address the situation.

5. Claims Submission:

After addressing the immediate impact of the cyber incident, the business submits a claim to the insurance provider. The claim includes documentation of the incident, such as incident reports, legal and forensic investigation reports, and evidence of financial loss or liability.

6. Claims Evaluation and Settlement:

The insurance provider evaluates the submitted claim and verifies its validity against the terms and conditions of the policy. Once the claim is approved, the insurance provider compensates the business for the covered losses or liabilities according to the policy’s limits and deductibles.

7. Risk Management Support:

Cybersecurity insurance providers often offer risk management support to their policyholders. This may include assistance in implementing effective security measures, employee training programs, and access to resources and expertise aimed at reducing the risk of future cyber incidents.

It is crucial for businesses to thoroughly review the policy terms and conditions, including coverage limits, deductibles, exclusions, and waiting periods, before purchasing cybersecurity insurance. It is also important to regularly review and update the policy as the business evolves and cyber threats evolve.

Next, we will discuss the key factors businesses should consider when purchasing cybersecurity insurance.

Factors to Consider When Purchasing Cybersecurity Insurance

When purchasing cybersecurity insurance, businesses need to carefully consider several factors to ensure they select the right policy that adequately addresses their specific needs and risks. Here are the key factors to consider:

1. Coverage Options:

Evaluate the coverage options offered by different insurance providers. Assess whether the policy covers the specific cyber risks that your business is most likely to face, such as data breaches, business interruption, or cyber extortion. Customizable coverage options allow businesses to tailor the policy to their specific needs.

2. Policy Limits:

Review the coverage limits of the policy, which determine the maximum amount the insurance provider will pay out in the event of a cyber incident. Ensure that the policy limits align with the potential financial losses your business could incur to adequately cover the costs of recovery, legal expenses, and other associated damages.

3. Deductibles:

Consider the deductibles associated with the policy. Deductibles are the amount the business must pay out of pocket before the insurance coverage kicks in. Evaluate the deductible amounts and determine if they are reasonable and affordable for your business.

4. Exclusions:

Read the policy exclusions carefully to understand what is not covered by the insurance. Exclusions can vary between policies and may include specific types of cyber incidents or situations. Ensure that the policy does not have broad exclusions that leave your business vulnerable to significant risks.

5. Claims Process:

Research the claims process of the insurance provider. Understand the timeline and requirements for submitting a claim and how the provider handles the claims evaluation and settlement process. A smooth and efficient claims process is crucial when you need the insurance coverage the most.

6. Risk Management Support:

Consider whether the insurance provider offers additional risk management support and resources. Some insurers provide access to cybersecurity experts, training programs, and best practices to help businesses proactively manage their cyber risks. This support can be valuable in strengthening your security efforts and reducing the likelihood of cyber incidents.

7. Reputation and Financial Stability:

Research the reputation and financial stability of the insurance provider. Look for established insurers with a track record of reliability and prompt payment of claims. Assess their financial strength ratings to ensure they have the financial capability to meet their obligations in the event of a large-scale cyber incident.

8. Cost and Value:

Consider the cost of the insurance policy in relation to the coverage and benefits offered. Compare the premiums of different insurers while evaluating the value provided by each policy. Remember that the cheapest policy may not always provide the comprehensive coverage your business needs, so strike a balance between cost and value.

It is advisable to consult with an insurance professional familiar with cybersecurity insurance to navigate the complexities of policy terms and evaluate the best options for your business. By carefully considering these factors, you can make an informed decision and choose a cybersecurity insurance policy that aligns with your risk management strategy.

Next, we will explore the benefits that businesses can derive from having cybersecurity insurance.

Benefits of Cybersecurity Insurance

Cybersecurity insurance offers numerous benefits to businesses in today’s digital landscape, where the risk of cyber threats and attacks is prevalent. Here are some key benefits of having cybersecurity insurance:

1. Financial Protection:

Cybersecurity insurance provides financial protection to businesses in the face of cyber incidents. It covers the costs associated with data breaches, business interruption, legal liabilities, forensic investigations, credit monitoring services, and other related expenses. This financial support helps businesses recover and minimize the financial impact of a cyberattack.

2. Risk Mitigation:

Having cybersecurity insurance incentivizes businesses to implement robust cybersecurity measures. Insurers often require policyholders to maintain certain security standards and procedures. By meeting these requirements, businesses can reduce their vulnerability to cyber threats, making it harder for attackers to breach their systems.

3. Business Continuity:

Cyberattacks can disrupt business operations for an extended period, leading to revenue loss and damage to reputation. Cybersecurity insurance with business interruption coverage helps businesses maintain their operations during the recovery phase. Financial compensation for the income lost and additional expenses incurred allows businesses to continue providing services and minimize the impact on customers and stakeholders.

4. Reputational Management:

The reputational damage caused by a cyber incident can have long-term consequences for a business. Cybersecurity insurance often covers the costs of reputational management efforts, such as public relations services, crisis communication, and advertising campaigns. These activities help rebuild trust, demonstrate transparency, and protect the company’s brand and reputation.

5. Legal Support:

Cybersecurity insurance includes liability coverage, which addresses legal liabilities arising from a cyber incident. The insurance provider can assist with legal counsel, legal defense costs, and settlements or judgments resulting from third-party claims. This support helps businesses navigate the legal complexities and potentially avoid severe financial consequences.

6. Compliance Assistance:

Many industries have specific data protection and cybersecurity regulations that businesses must comply with. Cybersecurity insurance can help in meeting these compliance requirements by covering expenses related to compliance audits, security improvements, and incident response planning. It ensures that businesses can meet their legal obligations and avoid penalties or reputational damage resulting from non-compliance.

7. Peace of Mind:

Having cybersecurity insurance provides peace of mind to businesses and their stakeholders. Knowing that financial protection and support are in place in the event of a cyber incident allows businesses to focus on their operations and growth, rather than constantly worrying about the potential financial and reputational risks associated with cyber threats.

While cybersecurity insurance is not a substitute for robust cybersecurity practices, it complements preventive measures by providing a safety net against the evolving threat landscape. It allows businesses to proactively manage their risks and respond effectively to cyber incidents when they occur.

In the next section, we will explore the cost considerations associated with cybersecurity insurance.

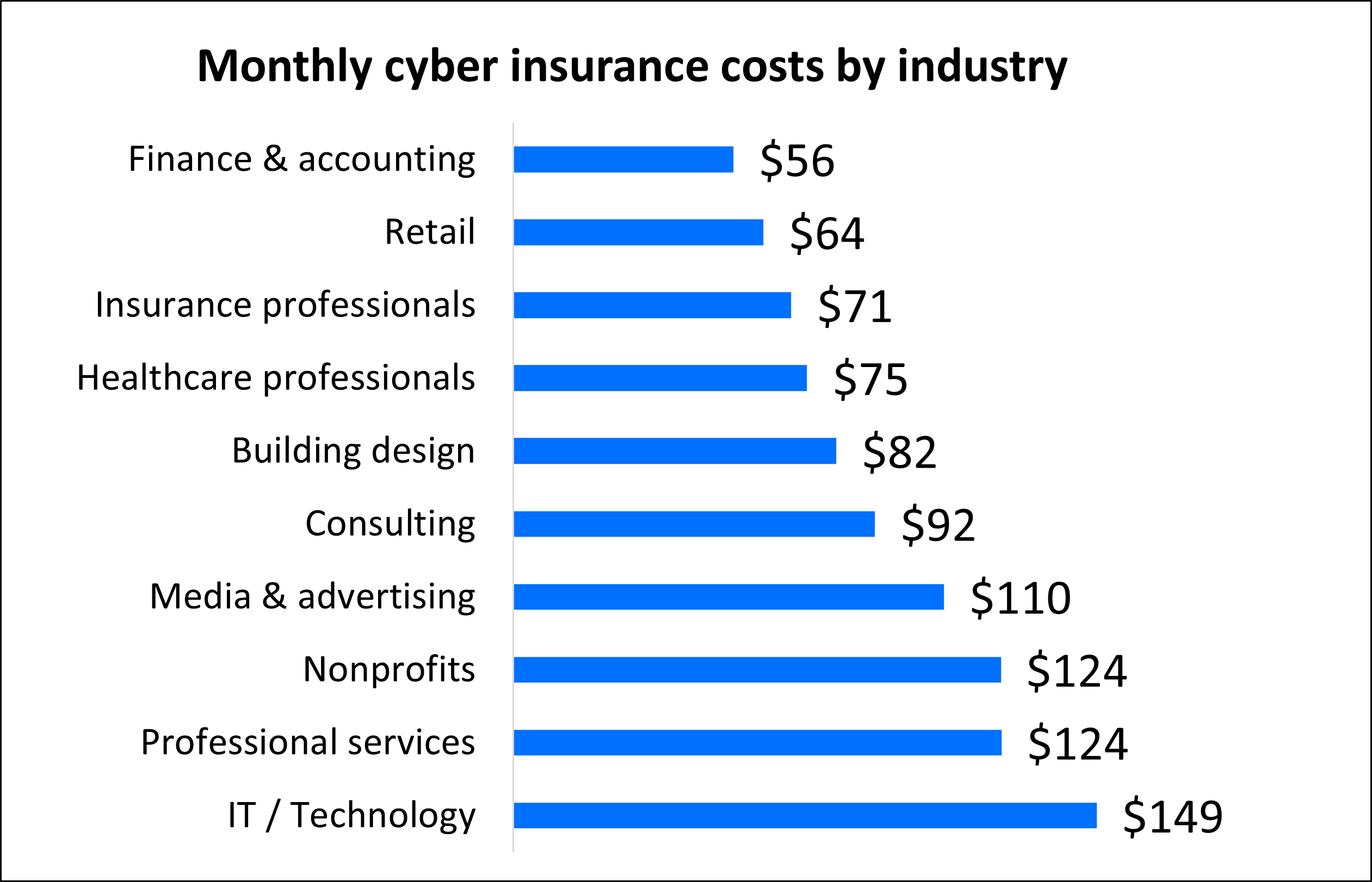

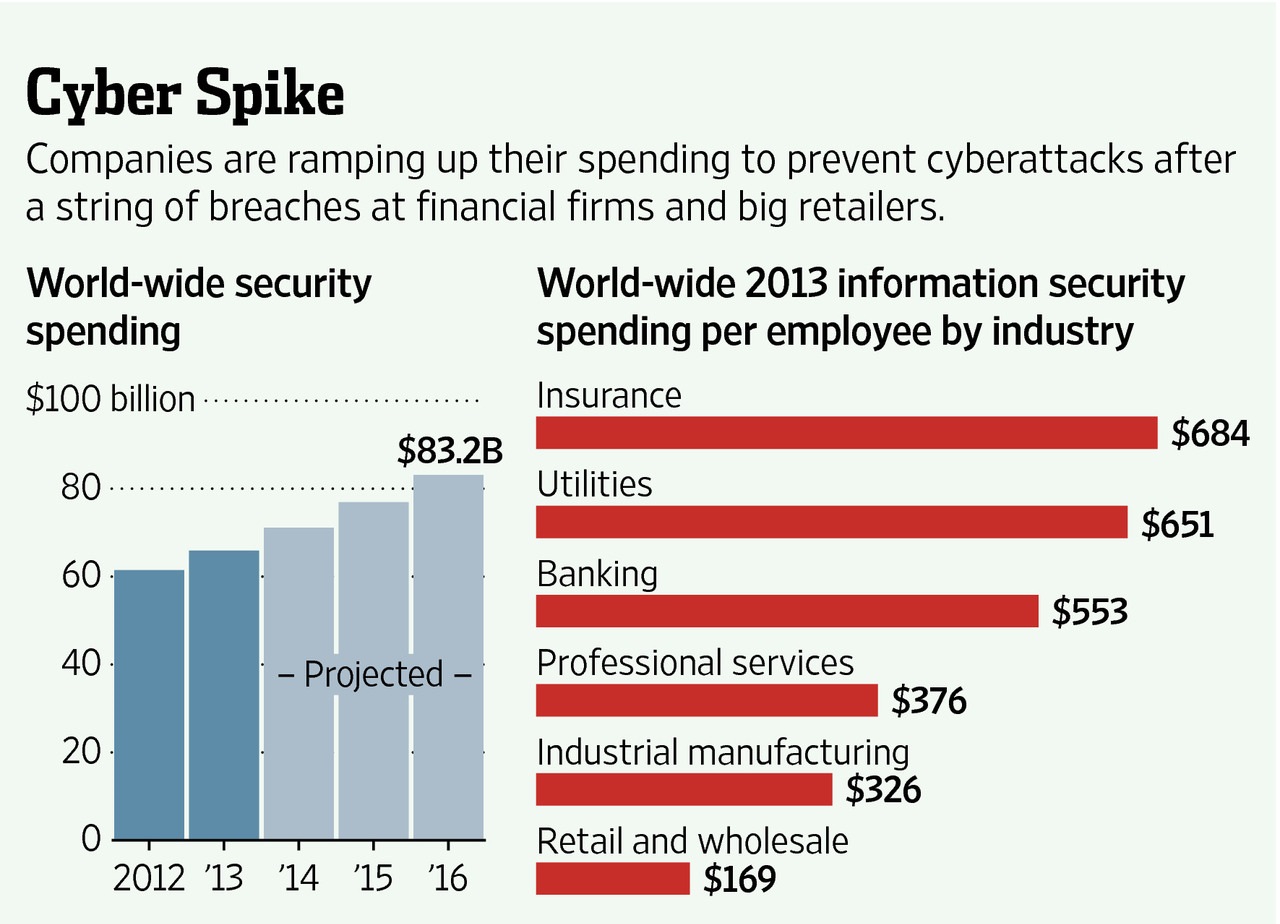

The Cost of Cybersecurity Insurance

When considering cybersecurity insurance, businesses need to understand the factors that determine the cost of coverage. Here are some key factors that influence the cost of cybersecurity insurance:

1. Business Size and Industry:

The size and industry of a business play a significant role in determining the cost of cybersecurity insurance. Large organizations or those operating in industries where cyber risks are more prevalent, such as healthcare or finance, may face higher premiums due to the increased likelihood and potential impact of cyber incidents.

2. Risk Profile:

The risk profile of a business is a critical factor in determining the cost of cybersecurity insurance. Insurers assess various aspects, including the company’s cybersecurity measures, data protection practices, incident response capabilities, and history of past cyber incidents. Businesses with comprehensive security measures in place may benefit from lower premiums compared to higher-risk organizations.

3. Security Controls:

The strength and effectiveness of a business’s security controls also impact the cost of cybersecurity insurance. Insurers evaluate the implemented security measures, such as firewalls, intrusion detection systems, encryption, and employee training programs. Businesses with robust security controls in place may demonstrate a lower risk profile and potentially qualify for more favorable premiums.

4. Coverage Limits and Deductibles:

The coverage limits and deductibles chosen by a business influence the cost of cybersecurity insurance. Higher coverage limits and lower deductibles generally result in higher premiums. It is essential to strike a balance between adequate coverage and manageable costs based on the specific needs and risk tolerance of the business.

5. Claims History:

A business’s claims history can impact the cost of cybersecurity insurance. Previous claims or a history of multiple cyber incidents may lead to higher premiums as insurers perceive a higher level of risk. Conversely, organizations without a significant claims history may be eligible for lower premiums.

6. Additional Risk Factors:

Other risk factors specific to the business, such as its use of cloud services, the type and volume of sensitive data stored, and its reliance on third-party vendors, can influence the cost of cybersecurity insurance. Insurers evaluate these factors to assess the potential vulnerabilities and exposures faced by the business.

It is important to note that the cost of cybersecurity insurance is an essential consideration, but businesses should also evaluate the value and coverage provided by the policy. Obtaining multiple quotes from different insurers and discussing specific needs and risk factors with insurance professionals can help businesses understand the potential costs and benefits associated with cybersecurity insurance.

Remember, the cost of cybersecurity insurance should be viewed as an investment in protecting the business against potential financial losses and reputational damage resulting from cyber incidents. It is crucial to assess the trade-off between the cost of coverage and the potential financial impact of an incident when deciding on the appropriate level of cybersecurity insurance for your business.

In the next section, we will discuss how businesses can select the right cybersecurity insurance provider.

How to Select the Right Cybersecurity Insurance Provider

Choosing the right cybersecurity insurance provider is crucial to ensure that your business receives comprehensive coverage and reliable support in the event of a cyber incident. Here are key factors to consider when selecting a cybersecurity insurance provider:

1. Reputation and Track Record:

Research the reputation and track record of potential insurance providers. Look for established insurers with a positive reputation for claim handling and prompt payment. Reading reviews, seeking referrals, and checking industry ratings can provide insights into the insurer’s reliability and customer satisfaction.

2. Industry Expertise:

Consider insurers that specialize in cybersecurity insurance or have extensive experience in the field. An insurer with industry expertise has a better understanding of the unique cyber risks businesses face in your specific industry. They can tailor policies and provide more targeted risk management support for your organization.

3. Financial Strength:

Evaluate the financial strength and stability of the insurer. Verify their financial ratings from reputable rating agencies to ensure they have the necessary resources to fulfill claims and provide the financial support your business needs in the event of a significant cyber incident.

4. Available Coverage Options:

Review the coverage options offered by each insurer. Assess whether the policies align with your business’s specific needs and risk profile. Look for flexibility in coverage options that allow customization to address the unique risks your organization faces. Ensure the policies cover common cyber risks such as data breaches, business interruption, and liability claims.

5. Claims Handling Process:

Consider the claims handling process of the insurer. Understand how they handle claims submission, evaluation, and settlement. Prompt and efficient claims handling is crucial in the event of a cyber incident, as delays can impact your business’s ability to recover and mitigate the financial impact of the incident.

6. Risk Management Support:

Evaluate the additional risk management support provided by the insurer. A good cybersecurity insurance provider will offer resources, tools, and guidance to help businesses strengthen their cybersecurity posture. This may include access to cybersecurity experts, training programs, and incident response planning assistance.

7. Cost and Value:

Consider the cost of the insurance policies relative to the coverage and benefits they offer. While cost is an important factor, it should not be the sole determining factor. Evaluate the value provided by each insurance provider, considering their coverage limits, deductibles, exclusions, and additional services. Seek a balance between affordability and comprehensive coverage.

8. Policy Terms and Conditions:

Thoroughly review the policy terms and conditions of each insurer. Understand the coverage limits, deductibles, exclusions, waiting periods, and any other specific policy requirements. Ensure that the policy aligns with your business’s risk profile and adequately addresses your most significant cyber risks.

Consulting with insurance professionals familiar with cybersecurity insurance can provide valuable guidance when evaluating different insurance providers. They can assist in assessing specific risks, understanding policy terms, and selecting a provider that meets your business’s unique needs.

Taking the time to research and carefully select a reliable and reputable cybersecurity insurance provider is crucial in securing the financial protection and support your business needs to navigate the complex landscape of cyber threats.

In the final section, we will summarize the key points and benefits of cybersecurity insurance.

Conclusion

In today’s digital age, cybersecurity threats are a constant concern for businesses of all sizes and industries. Cybersecurity insurance has emerged as a critical tool for organizations to manage the financial risks associated with cyber incidents. By providing financial protection, business continuity support, and risk management assistance, cybersecurity insurance helps businesses navigate the complex landscape of cyber threats.

When considering cybersecurity insurance, businesses should carefully evaluate their specific needs, risks, and budget. Factors such as coverage options, policy limits, deductibles, and exclusions play a crucial role in selecting the right insurance provider. It is essential to choose a reputable insurer with industry expertise, a strong track record, and the financial capability to meet their obligations.

While cybersecurity insurance provides important financial safeguards, it is crucial to remember that it is not a substitute for implementing robust cybersecurity measures. Businesses should prioritize proactive security measures, employee education, and incident response preparedness. Cybersecurity insurance should be seen as a complementary element of a comprehensive cybersecurity strategy.

By investing in cybersecurity insurance, businesses gain financial protection against the potential damages of cyber incidents, including data breaches, ransomware attacks, and business interruption. It also helps protect businesses from legal liabilities and supports reputational management efforts in the aftermath of a cyber incident.

When selecting a cybersecurity insurance provider, businesses should carefully assess their reputation, financial stability, available coverage options, claims handling process, risk management support, and overall value. By partnering with the right insurer, businesses can gain peace of mind and confidence in their ability to handle cyber risks.

Remember, cyber threats continue to evolve, and businesses must stay vigilant and proactive in their cybersecurity efforts. Regularly reviewing and updating cybersecurity insurance policies, along with ongoing risk assessments and security enhancements, will help businesses adapt and protect themselves against emerging cyber threats.

Cybersecurity insurance is an essential component of a comprehensive risk management strategy in today’s digital landscape. It enables businesses to mitigate financial losses, maintain business continuity, respond effectively to cyber incidents, and safeguard their reputation. By understanding their risks, selecting the right insurance provider, and implementing robust cybersecurity measures, businesses can confidently navigate the digital landscape and protect themselves against the ever-evolving cyber threats.