Introduction

Welcome to the world of banking, where there are various tools and services available to manage your finances effectively. One such tool is a standing order, which can be a convenient and hassle-free way to handle your regular payments. Whether you’re paying your rent, utility bills, or making charitable donations, understanding what a standing order is and how it works can enable you to streamline your financial obligations.

A standing order is a payment instruction that you give to your bank, directing them to make regular, fixed payments from your account to another person or organization. This payment can be scheduled to occur at specific intervals, such as daily, weekly, monthly, or annually. Once set up, a standing order automatically transfers the specified amount on the designated date, eliminating the need for manual payments or remembering due dates.

Standing orders provide a level of convenience and control over your regular payments. They help ensure that your essential expenses are promptly paid, avoiding any potential late fees or missed payments. By automating these payments, you can free up valuable time and mental energy that would otherwise be spent on remembering due dates and manually initiating payments.

However, it’s important to note that standing orders are different from direct debits, although they both involve automatic payments. With a standing order, you are in control of initiating and setting up the payment instruction. In contrast, with a direct debit, the recipient of the funds, such as a utility company or subscription service provider, initiates the payment from your account on your behalf.

In this article, we will explore the ins and outs of standing orders in banking. We will delve into how they work, the benefits they offer, and the differences between standing orders and direct debits. Additionally, we will provide a step-by-step guide on how to set up a standing order and offer examples of common uses for this payment method. By the end, you will have a comprehensive understanding of standing orders and be equipped to make informed decisions regarding your financial transactions.

Definition of a Standing Order

A standing order is a financial arrangement between a bank account holder and their bank. It is an instruction given by the account holder to the bank, authorizing the bank to make regular payments from the account to a specific recipient on specified dates or at fixed intervals.

Unlike direct debits, where the recipient initiates the payment, standing orders are initiated by the account holder. This means that you have full control over when and how much money is transferred from your account to the designated recipient. It is a predetermined arrangement, ensuring that the payments are made automatically without the need for manual intervention.

The amount transferred through a standing order can be a fixed amount, such as a monthly rent payment, or a variable amount based on factors like usage or bills. The frequency of the payment can be daily, weekly, monthly, quarterly, or annually, depending on the agreement between the account holder and the recipient.

Standing orders are commonly used for various purposes, including paying rent or mortgage, utility bills, loan repayments, subscription services, charitable donations, and regular savings. They provide a convenient way to ensure that essential payments are made on time and eliminate the risk of forgetting or missing a payment deadline.

It’s important to note that standing orders are usually set up for an indefinite period, but they can be canceled or amended by the account holder at any time. This flexibility allows you to adjust the payment amount or frequency based on your changing needs or financial circumstances.

Overall, a standing order is a simple yet effective tool for managing regular payments. By automating these payments, you can maintain control over your finances, avoid late fees, and ensure that your financial obligations are met consistently and efficiently.

How Does a Standing Order Work?

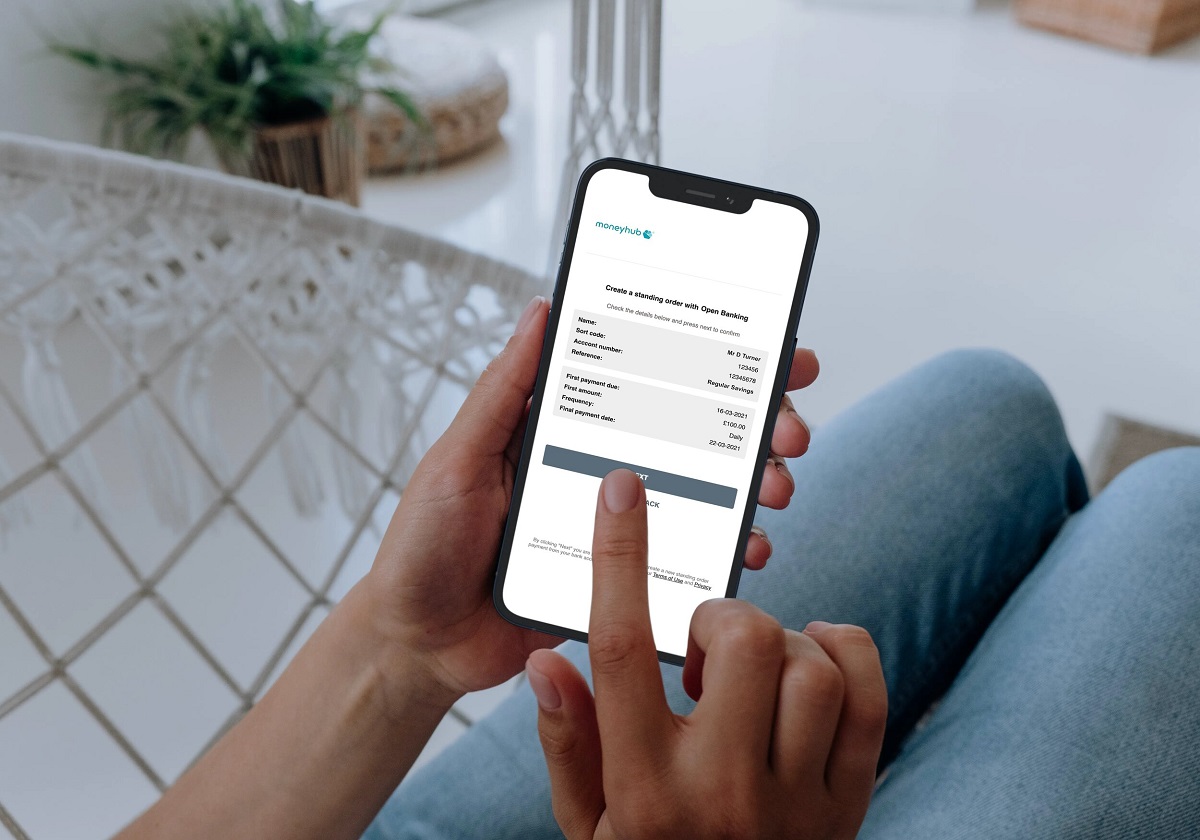

Setting up a standing order involves a straightforward process. First, you need to provide your bank with the necessary details, such as the recipient’s name, account number, and the amount and frequency of the payments. You will also need to specify the date or day of the month on which the payments should be made. Once the standing order is set up, the bank will automatically transfer the specified amount from your account to the recipient’s account on the scheduled dates or at the designated intervals.

Here’s a step-by-step breakdown of how a standing order works:

- You initiate the standing order by contacting your bank and providing them with the necessary information.

- The bank sets up the standing order in your account based on the details you provided.

- On the specified date, the bank deducts the specified amount from your account.

- The bank transfers the deducted amount to the recipient’s account.

- This process repeats automatically on the scheduled dates or at the defined intervals, according to your instructions.

It’s important to ensure that you have sufficient funds in your account to cover the standing order payments. If there are insufficient funds, the payment may not be successfully processed, leading to potential fees or penalties. Some banks may also offer the option to set up alerts or notifications to remind you of upcoming standing order payments or low account balances.

If you need to make changes to an existing standing order, such as modifying the payment amount or the payment frequency, you can do so by contacting your bank. They will assist you in updating the details accordingly.

Keep in mind that standing orders are ongoing payment instructions, typically until you decide to cancel or amend them. Therefore, it is essential to review your standing orders periodically to ensure they still align with your financial needs and obligations.

By understanding how standing orders work and effectively managing them, you can enjoy the convenience of automated payments while maintaining control over your finances.

Benefits of Using Standing Orders

Using standing orders for your regular payments offers several advantages that can simplify your financial management and provide peace of mind. Let’s explore some of the key benefits:

- Convenience and Time-Saving: Setting up a standing order allows you to automate your regular payments. This eliminates the need to manually initiate payments or remember due dates, saving you time and effort.

- Prompt and Timely Payments: Standing orders ensure that your payments are made on time, every time. By automating the process, you minimize the risk of forgetting or missing a payment deadline, avoiding late fees or penalties.

- Control over Payments: Unlike direct debits, where the recipient initiates the payment, standing orders give you full control over when and how much money is transferred from your account. You decide the amount and frequency of the payments, allowing you to tailor them to your specific needs.

- Budgeting and Financial Planning: With standing orders, you can accurately predict your cash outflows and incorporate them into your budget. This helps you plan your finances more effectively and ensures that you allocate sufficient funds for your regular payments.

- Flexibility to Modify or Cancel: Standing orders can be modified or canceled at any time, giving you the flexibility to adjust the payment amount or frequency based on your changing needs or financial circumstances. This allows you to maintain control over your financial obligations.

- Security and Reliability: When you set up a standing order, the payment is initiated by your bank using secure and reliable banking systems. This reduces the risk of fraud or unauthorized access to your funds.

- Efficient Money Management: By automating your regular payments, you can keep track of your expenses more efficiently. This enables you to monitor your cash flow, identify any discrepancies, and maintain a clear record of your financial transactions.

Whether you’re paying your rent, utility bills, loan repayments, or making charitable donations, using standing orders provides a convenient and hassle-free way to handle your regular payments. The benefits they offer help simplify your financial obligations, increase your control over payments, and enhance your overall financial management.

Differences Between Standing Orders and Direct Debits

While both standing orders and direct debits involve automatic payments, there are significant differences between the two payment methods. Understanding these differences can help you decide which option is best suited for your specific financial needs. Let’s explore the contrasts between standing orders and direct debits:

- Initiation: One of the key differences is the party who initiates the payment. With a standing order, you, as the account holder, initiate the payment by providing the bank with the necessary instructions. In contrast, with a direct debit, the recipient of the funds, such as a utility company or subscription service provider, initiates the payment from your account on your behalf.

- Payment Flexibility: Standing orders offer more control and flexibility over payments. You can specify the exact payment amount, the payment frequency, and the payment dates. The amount and timing remain consistent unless you choose to modify them. In contrast, direct debits vary in amount and may fluctuate from one payment period to another, depending on the bill or service usage.

- Cancellation and Amendments: Cancelling or amending a standing order is relatively straightforward. You can contact your bank and make the necessary changes as per your requirements. On the other hand, cancelling or amending a direct debit usually involves contacting the recipient (e.g., the utility company) to make the changes, often with specific notice periods required.

- Payment Guarantee: Direct debits come with a payment guarantee known as the Direct Debit Guarantee. This guarantee ensures that if an error occurs, such as an incorrect or unauthorized payment, you have the right to request a refund from your bank. Standing orders do not offer this guarantee, as the payment initiation and control rest with the account holder.

- Transaction Processing: Standing orders are generally processed during the working hours of the bank, and the funds are transferred directly from your account to the recipient’s account. In contrast, direct debits are usually processed by the recipient’s bank and may take place outside of regular banking hours.

- Payment Protection: With a standing order, it is crucial to ensure that you have sufficient funds in your account to cover the payments. If there are insufficient funds, the payment may not be processed, potentially leading to fees or penalties. With a direct debit, there is often a grace period for payment, and the recipient may attempt to collect the payment multiple times before considering it as a failed payment.

Understanding the differences between standing orders and direct debits can help you choose the payment method that aligns with your preferences and financial requirements. Both options provide automation and convenience, but their nuances make them suitable for different types of payments.

How to Set Up a Standing Order

Setting up a standing order is a straightforward process that can be done through your bank’s online banking platform, mobile app, or by visiting a branch in person. Follow the steps below to set up a standing order:

- Choose the Recipient: Determine the individual or organization you want to make regular payments to. Ensure you have their correct name, account number, and any other necessary details.

- Gather the Payment Information: Collect the required payment information, such as the payment amount, payment frequency (e.g., monthly, weekly), and the start date for the standing order.

- Access Your Banking Platform: Log in to your online banking account or open your bank’s mobile app.

- Navigate to the Standing Order Section: Locate the section of your online banking platform or app where you can set up standing orders. This may be under the “Payments,” “Transfers,” or similar options.

- Enter the Recipient Details: Provide the recipient’s name, account number, and any additional required information as prompted by your banking platform.

- Select the Payment Amount and Frequency: Specify the exact payment amount and the frequency at which the payments should be made (e.g., monthly, weekly).

- Set the Start Date: Choose the start date for the standing order. This is typically the date you want the first payment to be made.

- Verify and Submit: Review all the entered information to ensure accuracy. Once you are satisfied, submit the standing order request.

- Confirmation: You will receive a confirmation message or email from your bank indicating that the standing order has been set up successfully.

It’s important to monitor your account after setting up a standing order to ensure that the payments are being made as expected. Check that the correct amount is being deducted from your account on the scheduled dates or at the defined intervals.

If you need to make changes to an existing standing order, such as modifying the payment amount or the payment frequency, you can do so through your online banking platform, mobile app, or by contacting your bank directly. They will guide you through the process of updating the standing order details.

By following these steps, you can set up a standing order and enjoy the convenience of automated regular payments, ensuring timely and hassle-free transactions.

Examples of Common Uses for Standing Orders

Standing orders can be used for a variety of purposes and are particularly useful for making regular payments. Let’s explore some common examples of how standing orders are commonly used:

- Rent or Mortgage Payments: Many tenants and homeowners set up standing orders to pay their monthly rent or mortgage. This ensures that these critical payments are made on time consistently.

- Utility Bills: Standing orders are commonly used to pay utility bills, such as electricity, gas, and water. By automating these payments, you can avoid any interruption in service and ensure that your bills are paid promptly.

- Loan Repayments: If you have a loan or a financial arrangement that requires regular repayments, setting up a standing order can streamline the repayment process. It helps you stay on track with your loan obligations and prevents any missed or late payments.

- Subscription Services: Many subscription services, such as streaming platforms, gym memberships, and magazine subscriptions, can be paid through standing orders. This ensures that your subscription is consistently renewed, and you can continue enjoying the services without interruption.

- Charitable Donations: For individuals who make regular charitable donations, setting up a standing order can simplify the donation process. It allows you to contribute to your chosen charities on a predetermined schedule without having to remember to make manual donations.

- Regular Savings: Standing orders can also be used to facilitate regular savings. By automating the transfer of funds from your current account to a savings account, you can build your savings consistently and effortlessly.

- Loan or Credit Card Repayments: If you have outstanding credit card bills or loan repayments, setting up a standing order ensures that the required minimum payments are made on time. This helps avoid any late payment fees or penalties.

These are just a few examples of the many potential uses for standing orders. The flexibility of this payment method allows individuals to set up regular payments for a wide range of financial obligations, making it a convenient and efficient way to manage regular expenses.

Things to Consider When Using Standing Orders

While standing orders offer convenience and automation for regular payments, there are a few important factors to consider when using this payment method. Taking these into account can help you make the most of standing orders while ensuring effective financial management. Here are some key considerations:

- Sufficient Account Balance: It is essential to have sufficient funds in your account to cover the standing order payments. Ensure that you maintain a balance that can accommodate the regular payments to avoid any potential fees or penalties.

- Payment Amounts and Dates: Double-check the payment amounts and scheduled dates to ensure accuracy. Any errors in these details can lead to incorrect payments or missed payments.

- Regular Account Monitoring: It’s important to regularly review your bank account statements to ensure that the standing order payments are being processed correctly. Monitor for any discrepancies or unusual transactions.

- Changes in Payment Requirements: If there are any changes in the payment amount or frequency, it’s crucial to update the standing order details promptly. Failure to adjust the standing order to reflect the new requirements can lead to incorrect payments or missed payments.

- Financial Planning: Incorporate your standing order payments into your budget and financial planning. Ensure that you allocate sufficient funds for your regular payments, considering other financial obligations and expenses.

- Reviewing Standing Orders Periodically: Regularly review your standing orders to assess whether they still align with your financial needs and obligations. Cancel or amend standing orders that are no longer necessary or require modification.

- Communication with Recipients: If there are any changes to the standing order details, such as payment amounts or dates, notify the recipients in advance to ensure a smooth transition and avoid any confusion or disruptions in services.

- Banking Platform Security: Use secure and reputable banking platforms for setting up and managing your standing orders. Safeguard your login credentials and be cautious in accessing your online banking or mobile banking facilities on public or unsecured networks.

Considering these factors when using standing orders can help you make informed decisions, maintain control over your payments, and ensure effective financial management. Regular monitoring and communication with your bank and payment recipients will help address any issues promptly, providing you with peace of mind.

Conclusion

Standing orders are a valuable tool for managing regular payments and streamlining your financial obligations. By automating your payments, you can ensure timely transactions, avoid late fees, and have greater control over your finances. Whether you’re paying rent, utility bills, loan repayments, or making charitable donations, setting up a standing order can simplify the process and provide peace of mind.

In this article, we explored the definition of a standing order and how it differs from direct debits. We discussed the benefits of using standing orders, such as convenience, timely payments, and financial planning. We also provided a step-by-step guide on how to set up a standing order and highlighted common use cases for this payment method.

However, it’s important to consider a few things when using standing orders. Ensuring sufficient account balance, monitoring payments, reviewing and updating standing orders periodically, and maintaining communication with recipients are vital for effective usage of this payment method.

Overall, standing orders offer an efficient and hassle-free solution for managing your regular payments. By leveraging this financial tool, you can automate your financial responsibilities, freeing up time and mental energy to focus on other aspects of your life. Take advantage of standing orders to simplify your financial management and enjoy the convenience of automated payments.