What is Zelle?

Zelle is a popular, user-friendly digital payment platform that allows individuals to send and receive money directly from their bank accounts. It was launched in 2017 as a joint venture among major U.S. banks with the aim of providing a convenient and secure way to transfer funds between friends, family, and acquaintances. With Zelle, you can quickly and easily send money without the need for cash or checks.

One of the key advantages of using Zelle is that it eliminates the hassle of dealing with third-party payment services or waiting for checks to clear. The funds are typically transferred instantaneously, making it an ideal solution for splitting bills, paying rent, reimbursing friends, or even making small business payments.

Zelle is accessible through participating banks’ mobile banking apps, making it incredibly convenient for users who already have an account with a participating bank. It allows you to send money using just the recipient’s email address or mobile phone number, skipping the need to input complicated bank account details.

Another noteworthy feature of Zelle is that it is free to use for most transactions, making it an economical choice for sending money. However, it is important to note that some banks may charge fees for certain types of transfers, so it is always best to review your bank’s policies before initiating a transaction.

Overall, Zelle offers a secure, convenient, and cost-effective way to transfer funds digitally. Its integration with major banks and ease of use have made it a popular option for individuals seeking to streamline their payment experiences.

How does Zelle work?

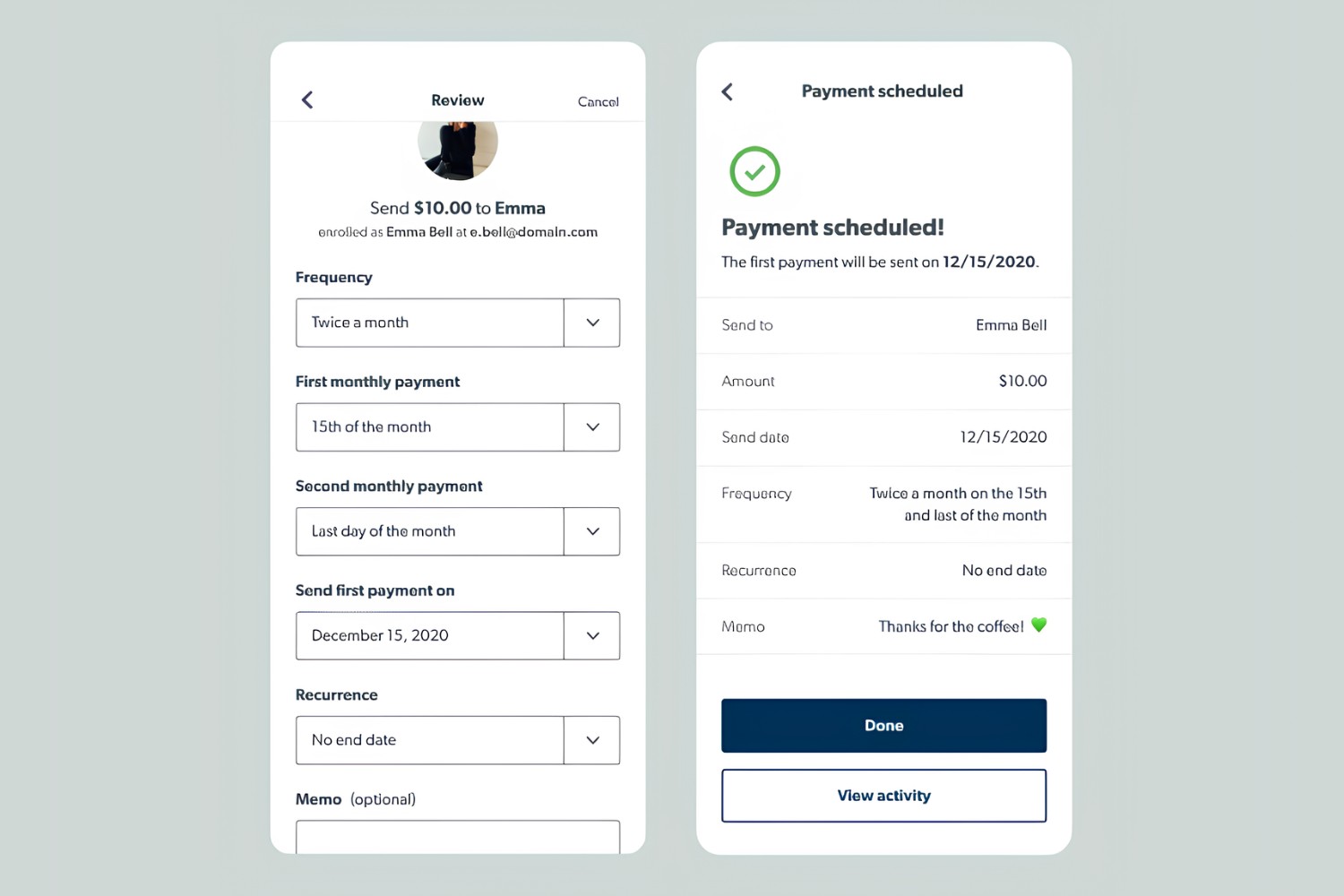

Zelle works by leveraging the existing infrastructure of participating banks to facilitate fast and secure money transfers. Here’s a step-by-step breakdown of how Zelle operates:

- Enrollment: To use Zelle, you first need to enroll in the service through your bank’s mobile banking app or website. Most major banks in the United States offer Zelle as a feature, so chances are your bank is already a participant.

- Sending money: Once enrolled, you can initiate a payment by opening your bank’s mobile app or visiting their website. Look for the option to send money with Zelle, usually located in the payments or transfers section.

- Recipient verification: To send money, you’ll need to provide the email address or mobile phone number of the person you want to send funds to. Zelle will verify whether the recipient is already enrolled in the service. If not, they will receive an invitation to enroll in order to receive the funds.

- Amount and memo: After verifying the recipient, you’ll specify the amount you want to send and have the option to include a memo to provide additional context for the transaction.

- Confirmation: Review the transaction details for accuracy and submit the payment. Zelle will confirm the transaction and send a notification to both the sender and recipient that the transfer is in progress.

- Receipt of funds: The recipient will receive a notification that they have received funds through Zelle. They can then access these funds directly in their bank account associated with their Zelle enrollment.

It’s important to note that both the sender and recipient need to have accounts with participating banks in order to use Zelle. If the recipient is not enrolled, they will have a limited time to enroll and claim the funds before the transaction is voided.

Additionally, Zelle transactions are typically processed instantaneously, allowing the recipient to access the funds quickly. The speed and efficiency of Zelle make it a convenient option for sending money in real-time.

Overall, Zelle simplifies the process of sending money by leveraging the infrastructure of participating banks. Its integration with existing banking platforms provides a seamless experience for users looking to transfer funds securely and efficiently.

Zelle daily limits

When using Zelle, it is important to be aware of the daily limits that are imposed on transactions. These limits are put in place to ensure security and mitigate potential fraudulent activity. The specific limits can vary depending on your bank and account type.

The majority of banks set a standard daily limit for Zelle transfers, typically ranging from $500 to $2,500. This means that you cannot exceed the specified dollar amount in total transactions for a given day.

It’s important to note that the daily limit applies to both incoming and outgoing transactions. For example, if your daily limit is set at $1,000 and you receive $600 from someone, you will only be able to send $400 to another person on the same day.

Keep in mind that these limits are not set by Zelle themselves but rather by the individual banks. Some banks may offer the option to increase the daily limit by contacting their customer service or visiting a branch in person.

Additionally, it’s worth noting that banks may also impose limits on the number of transactions you can make in a day. For example, you may be restricted to a maximum of 10 transactions per day, regardless of the total dollar amount.

If you anticipate needing to exceed the daily limits set by your bank, it may be necessary to explore alternative methods or contact your bank for potential solutions. Fortunately, there are options available to increase your Zelle limit, which we will discuss in more detail in the following section.

Remember, it’s always a good practice to review and understand your bank’s specific limits and policies concerning Zelle transactions to avoid any surprises or inconveniences when using the service.

How much can you Zelle in a day?

The amount you can Zelle in a day will depend on the daily limits set by your bank. As mentioned earlier, the daily limits can vary from bank to bank and can range from $500 to $2,500. It’s important to check with your specific bank to determine the exact limit applicable to your account.

These limits are put in place by banks to ensure the security of transactions and to prevent fraudulent activity. By setting a daily limit, banks can monitor and flag any suspicious or unusual transactions, protecting both the account holders and the overall integrity of the Zelle system.

It’s worth noting that the daily limit is for the total sum of transactions made in a day, both incoming and outgoing. For example, if your daily limit is set at $1,000 and you receive $400 from one person, you will only be able to send $600 to others on the same day.

While some individuals or businesses may find the daily limits to be sufficient for their needs, others may require higher transaction limits. If you anticipate needing to exceed the daily limits set by your bank, it’s advisable to explore alternative methods or contact your bank to inquire about potential solutions.

Some banks may offer the option to increase your daily limit by contacting their customer service or visiting a branch in person. They may require additional information or justification for the request, as they need to ensure the legitimacy and security of the transactions.

It’s important to remember that the Zelle daily limits are not set by Zelle itself, but rather by the participating banks. Therefore, the limits can vary depending on the bank you are associated with.

Before initiating any transactions, it is always a good practice to review the daily limits set by your bank. Understanding these limits will help you plan and manage your transactions effectively, ensuring a smooth and hassle-free experience when using Zelle.

Factors that can affect your Zelle limit

While Zelle daily limits are primarily determined by individual banks, there are several factors that can influence the specific limit applied to your account. Understanding these factors can help you navigate any limitations and potentially increase your Zelle limit, if necessary.

1. Bank policy: Each bank has its own policies and guidelines when it comes to setting Zelle limits. These policies may take into account factors such as account type, customer history, and risk assessment. Some banks may have more lenient limits for certain account types, such as premium or high-net-worth accounts.

2. Customer relationship: The duration and strength of your relationship with the bank can also play a role in determining your Zelle limit. Long-standing customers with a proven track record of responsible account management may be granted higher limits, as there is a level of trust established between the customer and the bank.

3. Account verification: Banks may have specific requirements for account verification in order to increase Zelle limits. This can include providing additional identifying information, such as government-issued IDs or proof of address. Verifying your account can help establish credibility and reduce the risk of fraudulent activity.

4. Transaction history: Your transaction history with Zelle can also impact your limit. Banks may review your past Zelle transactions, including the amount and frequency of transfers, to assess your eligibility for a higher limit. Consistently engaging in responsible and legitimate transfers may demonstrate your ability to handle larger amounts, potentially leading to an increased limit.

5. Risk assessment: Banks employ risk assessment techniques to identify and prevent potential fraudulent activity. Factors such as the recipient’s history, the frequency of transactions, and the transfer amount may be evaluated to determine risk. If a transfer is flagged as high-risk, it can lead to a lower limit being imposed on your account.

6. Customization options: Some banks offer customization options for Zelle limits. This allows customers to request higher limits based on their specific needs, such as businesses that require larger daily transfers. Contacting your bank’s customer service and discussing your requirements can help uncover potential customization options.

It’s important to note that while these factors can influence your Zelle limit, banks ultimately have the final say in setting the limits. They prioritize security and risk management to protect both their customers and the integrity of the Zelle platform.

If you find that your current Zelle limit is insufficient for your needs, it’s recommended to reach out to your bank’s customer service or visit a branch to inquire about potential options for increasing your limit. They may require additional information or authentication to support the request.

Understanding the factors that can affect your Zelle limit empowers you to navigate any limitations and explore opportunities for increasing your transaction capabilities.

How to increase your Zelle limit

If you find that your current Zelle limit is not meeting your transaction needs, there are several steps you can take to potentially increase your limit. While the specific options and requirements may vary depending on your bank, here are some common methods to consider:

1. Contact your bank: Reach out to your bank’s customer service or visit a branch to inquire about increasing your Zelle limit. They can provide information on the process and any necessary requirements. Be prepared to provide additional documentation, such as proof of income or business-related information, to support your request.

2. Provide additional verification: Banks may require additional account verification to increase your Zelle limit. This can involve submitting additional identifying information, such as government-issued IDs, proof of address, or verification of employment or business ownership. Follow your bank’s instructions and provide the necessary documentation promptly.

3. Demonstrate responsible usage: Consistently engage in responsible and legitimate Zelle transactions to build a positive transaction history. Banks may consider your past Zelle activity, such as the frequency and amount of transfers, when evaluating your eligibility for a higher limit. Show that you can handle larger amounts responsibly to increase the likelihood of a limit increase.

4. Upgrade your account: Some banks offer different types of accounts or banking packages that come with higher Zelle limits. If your current account has a lower limit, consider upgrading to a premium or higher-tier account that offers increased transaction capabilities. Explore the account options provided by your bank to find one that aligns with your needs.

5. Request customization options: Certain banks offer customization options for Zelle limits, allowing customers to have limits tailored to their specific requirements. Contact your bank and inquire about any customization options that they may offer. Be prepared to provide details on why you need a higher limit and any supporting documentation, such as business invoices or proof of transaction volumes.

It’s important to note that while these methods can potentially increase your Zelle limit, the final decision lies with your bank. Banks have their own policies and protocols in place to assess risk, ensure security, and prevent fraudulent activity. They will evaluate your request based on their internal guidelines and make a determination accordingly.

Be sure to follow your bank’s instructions and provide accurate and up-to-date information when seeking a limit increase. Understand that granting a higher limit is at the discretion of the bank and they may have specific requirements or restrictions.

By taking these steps and actively engaging with your bank, you can explore options to potentially increase your Zelle limit and accommodate your transaction needs more effectively.

Zelle transaction fees

One of the advantages of using Zelle is that, in most cases, it is free to use for personal transactions. This means that you can send money to friends, family, or acquaintances without incurring any transaction fees. However, it’s important to note that while Zelle itself does not charge fees, your bank may have its own fee structure in place for certain types of transfers.

When using Zelle to send money, you can typically do so without any additional cost. This is because Zelle operates through participating banks’ mobile banking apps or websites, utilizing the existing infrastructure of these banks. As a result, the transaction is conducted within the bank’s system rather than through a separate payment service provider.

However, it’s crucial to review your specific bank’s policies, as some banks may charge fees for specific types of transfers, such as international transfers or expedited transfers. These fees typically vary depending on your bank and the specific circumstances of the transaction.

It’s also important to note that some third-party banks may charge a fee to receive funds through Zelle. While sending money with Zelle is typically free, the recipient’s bank may have their own policies in place that incur a fee for accepting Zelle transfers. It’s advisable for the sender and recipient to be aware of any potential fees before initiating a transaction.

Should you have any concerns or questions regarding transaction fees, it is recommended to consult with your bank’s customer service or refer to the fee schedule provided by your bank. They can provide you with accurate and up-to-date information about any fees associated with Zelle transactions.

Overall, Zelle offers a cost-effective solution for sending money digitally, as it is typically free for personal transactions. However, it is essential to be aware of any potential fees imposed by your bank or the recipient’s bank to ensure a transparent and informed transaction process.

Zelle’s security measures

Zelle places a strong emphasis on security to ensure that your transactions are conducted in a safe and protected manner. Here are some of the security measures that Zelle has implemented:

1. Encryption: Zelle uses industry-standard encryption protocols to protect your personal and financial information during transmission. This encryption helps safeguard your data from unauthorized access and ensures its integrity during transit.

2. Authentication: Zelle incorporates multi-factor authentication to verify users’ identities and prevent unauthorized access to accounts. This typically involves a combination of something you know (such as a password), something you have (such as a registered device), and something you are (such as biometric verification).

3. Account monitoring: Zelle continuously monitors account activity for any suspicious or unusual transactions. This includes analyzing patterns, transaction amounts, and recipient information. If any potential threats or fraudulent activities are detected, Zelle will take appropriate actions to protect users and their accounts.

4. Fraud protection: Zelle offers fraud protection measures to help mitigate the risk of unauthorized transactions. They work closely with participating banks to promptly identify and address any fraudulent activity, providing customers with peace of mind when using the service.

5. Dispute resolution: In the event that a dispute arises regarding a Zelle transaction, Zelle provides a dispute resolution process. This allows users to report and resolve issues promptly and efficiently, ensuring a fair and transparent resolution.

6. Privacy controls: Zelle respects and protects the privacy of its users. They have implemented strict privacy controls to ensure that your personal information is handled securely and in accordance with applicable data protection laws.

It’s important to note that while Zelle has implemented robust security measures, users also have a responsibility to protect their own accounts. This includes keeping login credentials confidential, ensuring that devices used for Zelle transactions are secure and up-to-date, and practicing safe online habits, such as only conducting transactions on trusted networks.

If you have any concerns or suspect any suspicious activity related to your Zelle account, it is recommended to contact Zelle or your bank’s customer service immediately. They can provide guidance and assistance in addressing any security-related issues.

In summary, Zelle prioritizes the security of its users’ transactions through the implementation of encryption, multi-factor authentication, account monitoring, fraud protection, privacy controls, and dispute resolution. By combining these security measures with responsible user practices, Zelle aims to provide a safe and secure platform for digital transactions.

Alternatives to Zelle for larger transactions

While Zelle is a convenient and popular option for sending money, it does have certain limitations when it comes to larger transactions. If you find yourself needing to transfer larger sums of money, here are some alternatives to consider:

1. Wire transfers: Wire transfers are a common alternative for larger transactions. They involve directly transferring funds from one bank account to another, usually with the assistance of a banking professional. Wire transfers offer a secure and reliable method for sending larger amounts of money, but they often come with higher fees compared to other options.

2. Automated Clearing House (ACH) transfers: ACH transfers allow you to transfer funds electronically between bank accounts. They are typically used for one-time or recurring payments and are commonly used for transactions such as direct deposits and bill payments. While ACH transfers are generally slower than wire transfers, they are cost-effective and can be suitable for larger transactions.

3. PayPal: As a widely recognized online payment platform, PayPal offers the ability to send and receive money globally. While PayPal is often associated with smaller transactions, it also provides options for larger amounts. Keep in mind that PayPal may charge fees for certain types of transactions, especially for international transfers.

4. Cashier’s checks or money orders: Cashier’s checks and money orders are payment methods that are widely accepted and can be used for larger transactions. These instruments provide a secure and traceable way to transfer funds, but they typically require in-person visits to a bank or financial institution to obtain and deposit them.

5. Peer-to-peer (P2P) payment apps: P2P payment apps such as Venmo, Cash App, and Google Pay can be alternative options for larger transactions. These apps allow you to link your bank account or debit card and send money to other users. It’s important to check the transaction limits and any associated fees when using these apps for larger transfers.

6. Bank transfers: Traditional bank transfers refer to the process of initiating a transfer between different bank accounts. Most banks offer this service through their online or mobile banking platforms. Bank transfers are suitable for larger transactions as they typically have higher limits compared to P2P payment platforms.

When considering these alternatives, it’s important to assess the specific requirements, fees, and limitations associated with each option. Some methods may be more suitable for domestic transfers, while others may provide a better solution for international transactions.

It’s also worth noting that the availability of these alternatives may vary depending on the location and banking systems in your country. It’s advisable to consult with your bank or financial institution to understand the specifics and to choose the option that best fits your needs for larger transactions.

Conclusion

Zelle is a popular digital payment platform that offers a convenient and secure way to send and receive money directly from your bank account. With its user-friendly interface and integration with major banks, Zelle has become a go-to option for individuals looking to transfer funds easily and quickly.

We explored the features and functionalities of Zelle, including how it works and the daily limits imposed on transactions. By understanding these limits and the factors that can influence them, users can navigate them effectively and explore options for increasing their Zelle limit if necessary.

Additionally, we discussed Zelle’s commitment to security, outlining the encryption, authentication, account monitoring, and fraud protection measures it employs to ensure the safety of transactions. It’s important for users to also take responsibility for protecting their accounts and practicing safe online habits.

Furthermore, we considered alternative options for larger transactions, such as wire transfers, ACH transfers, PayPal, cashier’s checks, money orders, P2P payment apps, and traditional bank transfers. These alternatives provide users with flexibility based on their specific requirements and transaction needs.

In conclusion, Zelle offers a convenient and efficient way to transfer money digitally, especially for smaller transactions. Its integration with participating banks and emphasis on security make it a reliable option for individuals seeking a user-friendly and secure payment platform. However, for larger transactions, it’s important to explore alternative options that better suit your needs.

Remember to review the policies and fees associated with your specific bank and transaction type to ensure a seamless and cost-effective experience when using Zelle or any other payment method.