Introduction

In the world of banking, technological advancements have revolutionized the way financial transactions are conducted. One such advancement is the Point of Sale (POS) system, which has become an integral part of the banking industry. POS systems enable seamless and secure transactions by allowing customers to make payments through credit or debit cards at merchant outlets.

In this article, we will explore what POS means in banking, its different types, the benefits it offers, and how it works. We will also delve into the common challenges and risks associated with POS systems in banking, as well as the security measures that are in place to ensure the safety of transactions. Lastly, we will touch upon the future of POS in the banking sector.

The introduction of POS systems in banking has brought about significant changes in the way customers make payments. It has eliminated the need for traditional cash-based transactions and has streamlined the process, making it more efficient and convenient. By understanding what POS means in banking and how it operates, we can gain valuable insights into the future of financial transactions.

Throughout this article, we will explore the intricacies of POS systems in banking and shed light on how they have transformed the way we handle financial transactions. So, let’s dive into the world of POS and uncover its impact on the banking industry!

Definition and Overview

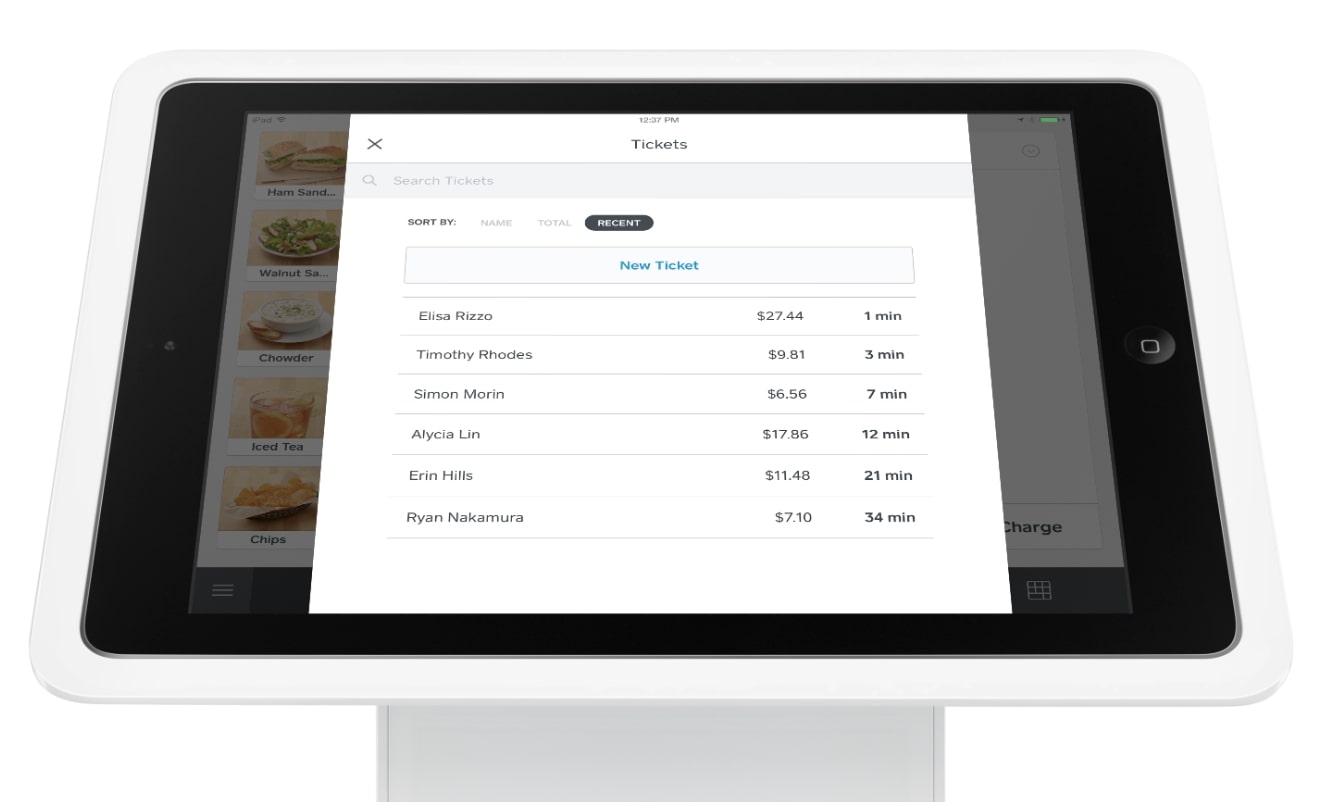

Before delving into the intricacies of POS systems in banking, it is essential to understand what POS means and its role in facilitating financial transactions. POS, short for Point of Sale, refers to the physical location where a customer makes a payment for goods or services. It is the final stage in the sales process where the customer’s payment is processed, and the transaction is completed.

In the banking industry, POS systems are electronic devices that enable customers to make payments using credit or debit cards. These systems are typically found in retail stores, restaurants, hotels, and other merchant outlets. When a customer wishes to make a purchase, they simply swipe or insert their card into the POS terminal, enter their PIN or sign the receipt, and the payment is processed instantaneously.

POS systems in banking offer a convenient and secure alternative to cash transactions. They provide customers with the flexibility to pay using their preferred payment method while also offering real-time transaction processing. This eliminates the need for customers to carry large amounts of cash and reduces the risk of theft or loss.

Moreover, POS systems offer businesses the opportunity to streamline their operations and improve efficiency. These systems provide accurate and detailed reports on sales, inventory, and customer behavior, allowing businesses to make informed decisions and optimize their processes. From a customer perspective, POS systems offer a seamless and hassle-free payment experience, enhancing overall satisfaction.

POS systems in banking have evolved over the years, transitioning from traditional card swipe machines to more sophisticated and versatile devices. Modern POS systems often include additional features such as touch screens, barcode scanners, and inventory management tools, further enhancing their functionality.

Overall, POS systems play a crucial role in the banking industry by facilitating secure and convenient payment transactions. They have become an indispensable tool for businesses and customers alike, embracing the digital transformation and reshaping the way we handle financial transactions.

Types of POS Systems in Banking

Within the banking industry, there are several types of POS systems available to cater to different needs and preferences. Let’s explore some of the common types:

- Traditional POS Systems: These are the conventional card swipe machines that have been in use for many years. They consist of a basic terminal that reads the magnetic strip on credit or debit cards. While these systems are simple and easy to use, they lack some of the advanced features found in more modern POS systems.

- Mobile POS Systems: With the advent of smartphones and tablets, mobile POS systems have gained popularity in recent years. These systems utilize mobile devices as terminals, enabling businesses to accept payments on the go. Mobile POS systems are especially useful for small businesses, pop-up shops, and vendors at events who require flexibility and mobility.

- Integrated POS Systems: Integrated POS systems are more advanced and comprehensive solutions that combine various functionalities into a single platform. These systems integrate with other business management tools such as inventory management, customer relationship management (CRM), and accounting software. They provide businesses with a holistic view of their operations and enable seamless data synchronization.

- Virtual POS Systems: Virtual POS systems, also known as online payment gateways, allow businesses to accept payments over the internet. These systems are typically used for e-commerce platforms, where customers make purchases online and complete their transactions using credit or debit cards. The payment process is secure and encrypted, ensuring the protection of sensitive customer information.

- Contactless POS Systems: Contactless POS systems utilize Near Field Communication (NFC) technology to enable quick and secure payments. Customers can simply tap their contactless-enabled cards or mobile devices on the POS terminal to complete the transaction. Contactless payments offer convenience and speed, reducing the need for physical contact between the customer and the terminal.

Each type of POS system has its own advantages and limitations, and businesses must choose the system that aligns with their specific requirements. Regardless of the type, POS systems in banking have revolutionized the way transactions are conducted, providing businesses and customers with flexibility, convenience, and security.

Benefits of POS in Banking

The adoption of POS systems in the banking industry comes with a multitude of benefits for both businesses and customers. Let’s explore some of the key advantages:

- Convenience: POS systems offer a convenient payment experience for customers. Instead of carrying cash, customers can simply use their credit or debit cards to make quick and hassle-free transactions. This eliminates the need for counting change, prevents the risk of counterfeit currency, and saves time for both customers and businesses.

- Efficiency: POS systems streamline the payment process, improving efficiency for businesses. The automation of transaction processing reduces the likelihood of human error and eliminates the need for manual paperwork. Additionally, integrated POS systems provide businesses with real-time sales data, helping them make informed decisions and optimize their operations.

- Increased Sales: Accepting card payments through POS systems can significantly boost sales for businesses. Studies show that customers tend to spend more when using cards instead of cash. POS systems also enable businesses to offer additional services such as loyalty programs and discounts, enhancing customer satisfaction and encouraging repeat business.

- Enhanced Security: POS systems in banking prioritize security to protect customer and business data. Encryption technology ensures that sensitive information is securely transmitted during transactions, safeguarding against unauthorized access. Additionally, with digital receipts, there is less risk of loss or theft compared to traditional paper receipts.

- Improved Record-Keeping: POS systems maintain accurate and detailed records of transactions, providing businesses with comprehensive financial reports. These reports help businesses track sales, inventory, and customer behavior, enabling them to make data-driven decisions and identify trends or areas for improvement.

The benefits of POS systems extend beyond the transactional aspects. They contribute to overall customer satisfaction, operational efficiency, and better financial management for businesses in the banking industry.

Both businesses and customers stand to gain from the adoption of POS systems, creating a win-win situation in the ever-evolving landscape of banking transactions.

How Does POS Work in Banking?

POS systems in banking are designed to facilitate seamless and secure transactions between customers and businesses. Here’s a simplified overview of how POS systems work:

- Customer Initiates Transaction: When a customer wishes to make a purchase, they present their credit or debit card to the merchant at the point of sale. The card contains the necessary information, such as the cardholder’s account details and a unique card number.

- Card Authentication: The merchant swipes or inserts the customer’s card into the POS terminal. The terminal then reads the card’s magnetic strip or chip, verifying the card’s authenticity and retrieving the necessary transaction information.

- Transaction Details: The customer is prompted to enter their PIN or sign the receipt, depending on the verification method used. This ensures that the cardholder authorizes the transaction and provides an additional layer of security.

- Processing the Payment: Once the customer completes the necessary verification steps, the POS terminal encrypts the transaction details and sends them to the acquiring bank or payment processor for authentication. The acquiring bank then communicates with the customer’s card issuer to confirm the availability of funds or credit limit.

- Transaction Approval: Upon receiving authorization from the card issuer, the acquiring bank or payment processor sends an approval message back to the POS terminal. This signals that the transaction has been successfully authorized, and the payment can be processed.

- Payment Confirmation: The merchant receives confirmation of the approved transaction on the POS terminal. A receipt, either in physical or electronic form, is then generated and provided to the customer as proof of payment.

- Settlement and Clearing: At the end of each business day, the merchant submits a batch of approved transactions to the acquiring bank for settlement. The acquiring bank transfers the funds from the cardholders’ accounts to the merchant’s account, completing the transaction.

It is important to note that the actual process may vary based on the specific POS system and the payment network involved. However, the underlying principles remain the same: authentication, verification, authorization, and settlement.

POS systems in banking ensure that transactions are processed efficiently, securely, and in real-time, offering a seamless payment experience for both customers and businesses.

Common Challenges and Risks of POS in Banking

While POS systems have revolutionized the way transactions are conducted in the banking industry, they also come with certain challenges and risks. Let’s explore some of the common challenges and risks associated with POS in banking:

- Data Breaches and Security Threats: Data breaches pose a significant risk to both businesses and customers. Malicious actors may attempt to gain unauthorized access to the sensitive information stored within POS systems, such as cardholder data and personal identification numbers (PINs). Implementing robust security measures like encryption and tokenization can mitigate these risks.

- Point of Sale Malware: Point of Sale malware is designed to gather payment card details from compromised POS systems. This malware can be introduced through various attack vectors, such as phishing emails or infected devices. Regular software updates and security patches, along with employee awareness training, can help in preventing such attacks.

- System Downtime: POS systems rely on technology, and like any other system, they can experience technical issues or downtime. This could disrupt business operations and lead to inconvenience for both businesses and customers. Regular maintenance and backup systems can help minimize the impact of system downtime.

- Transaction Errors: Human errors or technical glitches can result in inaccurate transactions. This may include erroneous charges, incorrect payment amounts, or failed transactions. Monitoring and reconciling transactions regularly can help identify and rectify any errors promptly.

- Compatibility and Integration Issues: Businesses often rely on various systems and software for their operations. Integrating POS systems with existing software, such as inventory management or accounting systems, can present challenges. Choosing compatible systems and working closely with experienced vendors can address these integration issues.

- Compliance and Regulatory Requirements: Banking transactions are subject to strict regulatory compliance standards, such as Payment Card Industry Data Security Standard (PCI DSS) and General Data Protection Regulation (GDPR). Failing to comply with these requirements can result in severe penalties and reputational damage. Businesses must stay updated with the latest regulations and ensure their POS systems meet the necessary compliance standards.

Addressing these challenges and mitigating associated risks is essential for businesses to maintain the security, integrity, and efficiency of POS systems in the banking industry.

Security Measures in POS Banking Transactions

Given the sensitive nature of banking transactions, ensuring the security of POS systems is of utmost importance. Various security measures are implemented to protect the integrity and confidentiality of data during POS banking transactions. Let’s explore some common security measures:

- Encryption: Encryption is a crucial security measure that converts sensitive data, such as cardholder information, into unreadable code. This ensures that even if the data is intercepted, it cannot be accessed without the proper decryption key. Implementing strong encryption protocols, such as Advanced Encryption Standard (AES), helps safeguard data during transmission and storage.

- Tokenization: Tokenization is the process of replacing sensitive data, such as credit card numbers, with unique identification symbols called tokens. These tokens are used in POS transactions instead of the actual card data, adding an extra layer of security. Even if the tokenized data is intercepted, it holds no value as it cannot be used outside the transaction context.

- Two-Factor Authentication (2FA): Implementing two-factor authentication adds an additional layer of security to POS transactions. This involves combining something the user knows (e.g., a password) with something the user possesses (e.g., a one-time password generated on a mobile device) or something biometric (e.g., a fingerprint). 2FA strengthens the authentication process and reduces the risk of unauthorized access.

- Regular Patching and Updates: POS systems should receive regular software updates and security patches to address any vulnerabilities or bugs. These updates not only improve the functionality of the system but also address any known security weaknesses. Businesses should establish a process to regularly monitor and apply these updates to keep their systems secure.

- Firewalls and Intrusion Detection Systems: Firewalls and intrusion detection systems play a crucial role in protecting POS systems from unauthorized network access. Firewalls act as a barrier between internal networks and external networks, allowing only authorized traffic to pass through. Intrusion detection systems monitor network activity and identify any suspicious or malicious behavior, alerting system administrators of potential security breaches.

- Employee Training and Awareness: Human error is a common cause of security breaches. Providing comprehensive training and raising awareness among employees about best security practices helps ensure secure POS transactions. Employees should be educated on identifying social engineering attacks, handling customer data securely, and following proper protocol when using POS systems.

By implementing these security measures, businesses can significantly reduce the risk of data breaches and unauthorized access to POS banking transactions. The protection of customer data and the integrity of financial transactions remain top priorities in the constantly evolving landscape of cybersecurity.

Future of POS in Banking

The future of POS systems in the banking industry holds exciting prospects as technology continues to evolve and customer expectations grow. Here are some glimpses into what the future may hold for POS in banking:

- Mobile Wallet Integration: With the rise of mobile payments and digital wallets, we can expect to see greater integration between POS systems and mobile devices. This will enable customers to make payments directly from their smartphones, eliminating the need for physical cards and enhancing convenience.

- Biometric Authentication: Biometric authentication, such as fingerprint or facial recognition, is gaining popularity as a secure method for identity verification. We can expect to see increased adoption of biometric authentication in POS systems, providing customers with a seamless and secure payment experience.

- Internet of Things (IoT) Integration: The integration of IoT devices with POS systems can provide new opportunities for personalized and contextualized customer experiences. IoT-enabled devices, such as smart shelves or wearables, can automatically detect and process purchases, making transactions even more seamless for customers.

- Artificial Intelligence (AI) and Machine Learning: AI and machine learning technologies have the potential to revolutionize POS systems. These technologies can analyze transaction data, customer behavior, and market trends to provide valuable insights for businesses. AI-powered chatbots can also enhance customer support and engagement at the point of sale.

- Enhanced Data Analytics: The future of POS in banking will involve advanced data analytics capabilities. POS systems will offer businesses deeper insights into customer preferences, buying patterns, and inventory management. This data will help businesses make data-driven decisions and optimize their operations for improved profitability.

- Blockchain Technology: Blockchain technology has the potential to revolutionize the security and transparency of transactions. In the future, we might see the integration of blockchain technology in POS systems for secure, decentralized transactions, reducing the risks associated with traditional centralized systems.

- Personalized Offers and Loyalty Programs: POS systems will continue to facilitate personalized offers and loyalty programs for customers. With the use of customer data and advanced analytics, businesses can offer targeted promotions, discounts, and rewards at the point of sale, enhancing customer engagement and loyalty.

The future of POS in banking is driven by innovation and customer-centric solutions. These advancements aim to create a seamless, secure, and personalized payment experience that meets the evolving needs and expectations of businesses and customers alike.

Conclusion

The adoption of Point of Sale (POS) systems in the banking industry has transformed the way financial transactions are conducted, offering numerous benefits for both businesses and customers. POS systems provide convenience, efficiency, increased sales, and enhanced security in the payment process. They have become an integral part of modern banking operations, revolutionizing the way businesses and customers interact at the point of sale.

With various types of POS systems available, businesses can choose the one that best suits their needs and integrates seamlessly with their existing infrastructure. Traditional, mobile, integrated, virtual, and contactless POS systems offer different functionalities and serve diverse business requirements.

While there are challenges and risks associated with POS systems, such as data breaches and system downtime, these can be mitigated through robust security measures, regular updates, and employee training. Encrypted data transmission, tokenization, two-factor authentication, and monitoring network activity help ensure the security and integrity of POS banking transactions.

The future of POS in banking holds exciting prospects. Mobile wallet integration, biometric authentication, IoT integration, AI and machine learning, enhanced data analytics, blockchain technology, and personalized offers and loyalty programs are shaping the future of POS systems. These advancements aim to create a seamless, secure, and personalized payment experience that meets the evolving needs of businesses and customers.

In conclusion, POS systems have revolutionized the banking industry, streamlining transactions, enhancing security, and improving operational efficiency. As technology continues to advance, the future of POS in banking looks promising, offering innovative solutions that enable businesses to thrive and provide customers with more convenient and personalized payment experiences.