Introduction

The International Bank Account Number, commonly known as IBAN, is an internationally recognized system used in the banking industry to identify bank accounts during cross-border transactions. It provides a standardized format for account numbers, making it easier to process and track payments across different countries.

IBAN was introduced by the International Organization for Standardization (ISO) as a means to streamline and improve the efficiency of international payments. Prior to the implementation of IBAN, each country had its own unique account numbering system, which often caused confusion and delays when conducting transactions between banks located in different countries.

The purpose of IBAN is to ensure accuracy and eliminate errors when transferring funds between countries. By using a standardized format, financial institutions can easily validate the accuracy of an IBAN and reduce the risk of making erroneous payments. In addition, IBAN helps to facilitate automatic processing of transactions, reducing manual intervention and speeding up the transfer process.

In this article, we will explore the definition, structure, and benefits of IBAN, along with its application in international payments. We will also provide guidance on how to verify the validity of an IBAN and answer some frequently asked questions to enhance your understanding of this important banking concept.

Definition of IBAN

The International Bank Account Number (IBAN) is a unique alphanumeric code used to identify bank accounts in international transactions. It provides a standardized format for account numbers, allowing for seamless and accurate processing of payments across different countries. The IBAN acts as a passport for your bank account, making it easily identifiable by banks and financial institutions worldwide.

The structure of an IBAN varies depending on the country. However, it typically consists of two-letter country code, followed by two check digits, and then a combination of alphanumeric characters that represent the individual bank branch and account number. The length of the IBAN also varies by country.

IBANs were introduced to replace the complex and often confusing local bank account numbering systems that were used in each country. The goal was to create a unified and globally recognized system that would enhance the efficiency and accuracy of international payments.

By using IBAN, banks and financial institutions can easily identify the recipient’s bank and account details, reducing the risk of errors and ensuring that funds are transferred to the intended recipient. IBANs also facilitate the automation of payment processes, allowing for faster and more efficient cross-border transactions.

It is important to note that an IBAN does not replace the traditional bank account number; rather, it is an additional piece of information that is used to enhance the accuracy and reliability of international transactions.

Overall, the IBAN is a crucial component of the global banking system, enabling seamless communication between banks and ensuring the smooth processing of international payments. Its standardized format simplifies the identification and verification of bank accounts, leading to improved efficiency and security in cross-border transactions.

Purpose of IBAN

The International Bank Account Number (IBAN) serves several important purposes in the banking industry, all of which contribute to the smooth and secure processing of international payments.

One of the primary purposes of IBAN is to ensure accuracy and eliminate errors when transferring funds between different countries. Prior to the implementation of IBAN, there were instances where payments were mistakenly sent to the wrong bank or account due to inconsistencies in account numbering systems. With IBAN, the standardized format helps to reduce the risk of such errors by providing a unique identifier for each bank account.

IBAN also enables banks and financial institutions to automate the processing of international payments. By using the IBAN as a reference, banks can quickly identify the recipient’s bank and account details, reducing the need for manual intervention and increasing the efficiency of cross-border transactions. This automation leads to faster processing times, allowing businesses and individuals to receive funds in a timely manner.

Furthermore, IBAN plays a crucial role in fraud prevention and security. The unique structure of IBAN enables banks to validate the accuracy and authenticity of the provided account details. By verifying the correct IBAN, banks can ensure that the funds are being transferred to the intended recipient, reducing the risk of fraudulent activity and financial losses.

Another purpose of IBAN is to simplify the reconciliation process for both sending and receiving banks. With a standardized format, it becomes easier to match incoming payments to the correct accounts, reducing administrative errors and delays. This is particularly important in high-volume transactions, where efficient reconciliation is critical for maintaining accurate financial records.

IBAN also promotes transparency and standardization in international banking practices. By adopting a globally accepted format, financial institutions around the world can communicate and collaborate more effectively, facilitating smoother cross-border financial transactions. This standardization allows for better cooperation and coordination among banks, ultimately benefiting businesses and individuals engaging in international trade and commerce.

In summary, the purpose of IBAN is to enhance accuracy, efficiency, and security in international payments. It simplifies the identification and verification of bank accounts, automates payment processes, prevents fraud, and promotes global standardization. With the use of IBAN, the banking industry is better equipped to meet the demands of the globalized economy and ensure the seamless transfer of funds across borders.

Structure of IBAN

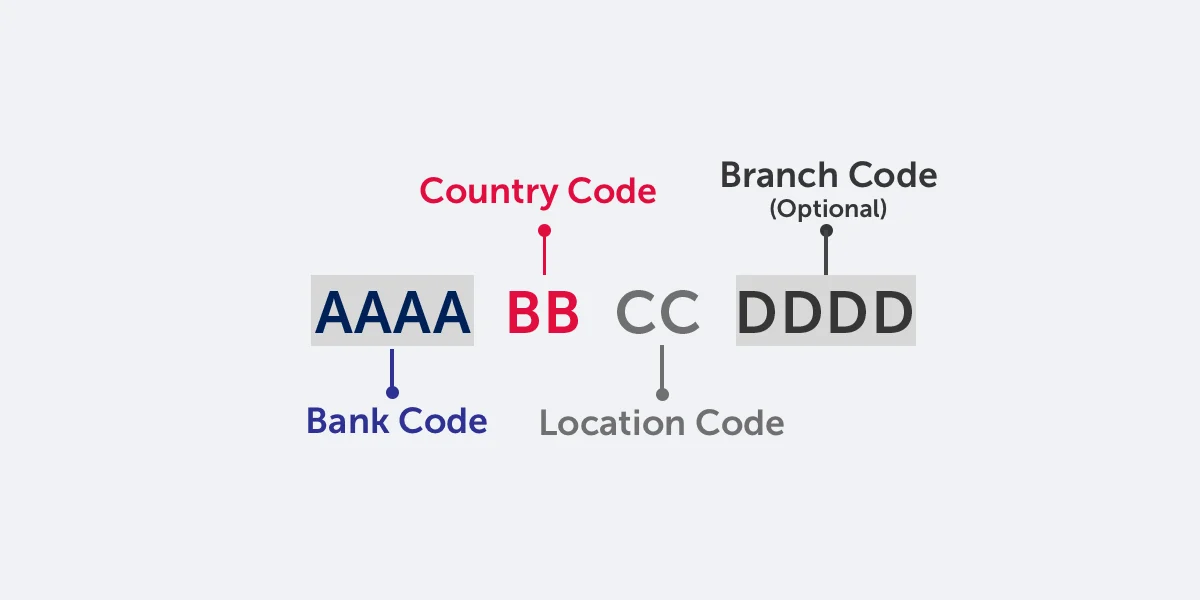

The International Bank Account Number (IBAN) has a specific structure that varies based on the country. However, the general framework of IBAN consists of a combination of alphanumeric characters that uniquely identify a bank account for international transactions.

The IBAN structure typically includes the following elements:

- Country Code: The first two characters of the IBAN represent the country code. These characters indicate the country in which the bank account is registered. For example, “US” represents the United States, “GB” represents the United Kingdom, and “DE” represents Germany.

- Check Digits: After the country code, two check digits follow. These digits are used to verify the accuracy and integrity of the IBAN. The combination of the country code and check digits helps ensure that the IBAN is valid and free from errors.

- Bank Identifier: Following the check digits, the IBAN contains a bank identifier. This alphanumeric code identifies the specific bank or branch where the account is held. It helps ensure that the funds are transferred to the correct banking institution.

- Account Number: The last part of the IBAN is the account number. This alphanumeric code uniquely identifies the individual bank account within the designated bank or branch. It allows for precise identification of the recipient’s account, ensuring that funds are credited accurately.

It is important to note that the length and format of each element can vary depending on the country’s specific IBAN requirements. Some countries may have fixed lengths for each component, while others may allow for variable lengths. Additionally, there may be certain country-specific rules regarding the inclusion of leading zeros or the use of specific characters.

Overall, the structure of the IBAN provides a standardized and internationally recognized format for identifying bank accounts in cross-border transactions. By following this prescribed structure, financial institutions can accurately interpret and process IBANs, ensuring that funds are correctly allocated to the intended recipients.

IBAN Format by Country

The format of the International Bank Account Number (IBAN) may vary from country to country, as each country has its own unique requirements and specifications. Here is an overview of the IBAN formats for some commonly used countries:

- United States (US): The IBAN format is not used in the United States. Instead, the country utilizes a different system for identifying bank accounts, such as the routing number and account number.

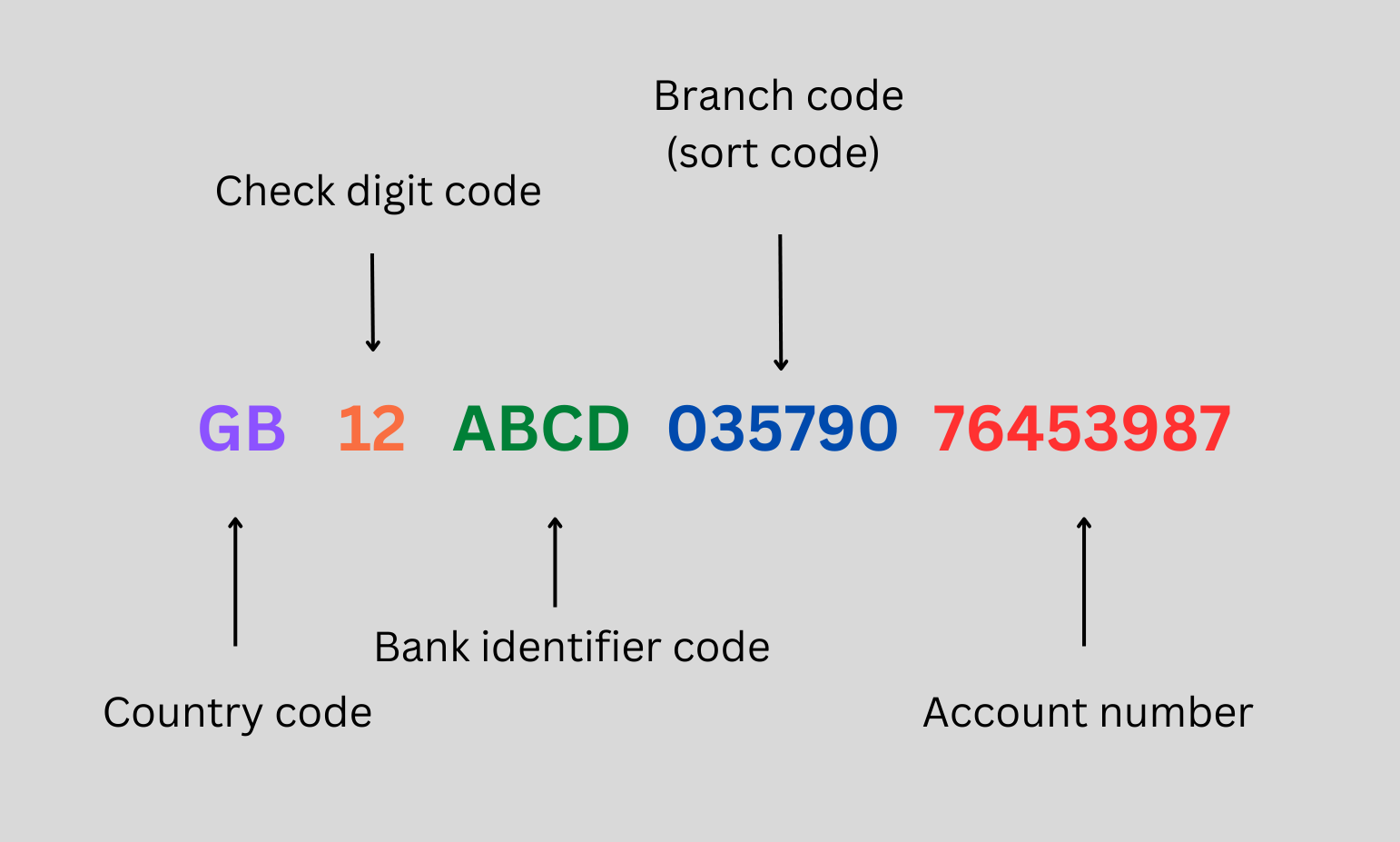

- United Kingdom (GB): In the United Kingdom, the IBAN consists of two letters representing the country code (GB), followed by a two-digit checksum, four letters representing the bank code, and an eight-digit account number.

- Australia (AU): The IBAN in Australia, also known as the Basic Bank Account Number (BBAN), consists of six digits representing the bank branch code, followed by a nine-digit account number and a three-digit bank code.

- Germany (DE): The German IBAN consists of two letters representing the country code (DE), followed by a two-digit checksum, an eight-digit bank code (Bankleitzahl), and a ten-digit account number.

- France (FR): In France, the IBAN starts with two letters representing the country code (FR), followed by a two-digit checksum, five digits representing the bank code, and eleven digits representing the account number.

- Canada (CA): Canada does not currently use IBAN. Instead, bank account identification is typically done using a combination of the bank number, branch number, and account number.

It is important to note that the length and structure of the IBAN can vary even within the same country, as different banks may have their own specific requirements. To obtain the correct IBAN for your bank account, it is recommended to consult your bank or use online IBAN generators that are specific to your country.

When conducting international transactions, it is crucial to ensure that the IBAN provided follows the correct format for the recipient’s country. Any discrepancies or errors in the IBAN format can result in failed or delayed transactions. Therefore, it is always advisable to double-check the IBAN details and validate its accuracy before initiating any cross-border payments.

In summary, the format of the IBAN varies by country, with each country having its own specific requirements. Understanding the correct format for the recipient’s country is essential to ensure accurate processing of international payments.

Advantages of IBAN

The International Bank Account Number (IBAN) offers several advantages that contribute to smoother and more efficient international transactions. Here are some key benefits of using IBAN:

- Standardization: IBAN provides a standardized format for bank account numbers across different countries. This uniformity simplifies the identification and processing of international payments, reducing errors and delays caused by discrepancies in local account numbering systems.

- Accuracy: The structure of IBAN includes check digits, which serve as a built-in validation mechanism. These digits help to verify the accuracy of the IBAN and reduce the risk of sending funds to the wrong recipient or account.

- Efficiency: By using IBAN, banks and financial institutions can automate the processing of international payments. The standardized format allows for faster validation and routing of transactions, resulting in quicker fund transfers and improved operational efficiency.

- Cost-Effectiveness: The automation enabled by IBAN reduces manual intervention and the need for manual data entry. This leads to cost savings for financial institutions, as fewer resources are required to process international transactions.

- Increased Security: IBAN helps to enhance security in international transactions. By validating the accuracy of the recipient’s bank account details, it reduces the risk of fraudulent activities, such as sending funds to incorrect or unauthorized accounts.

- Facilitates Compliance: IBAN plays a crucial role in complying with regulatory requirements, such as anti-money laundering (AML) and know your customer (KYC) regulations. It provides a standardized and reliable method for verifying bank account details, supporting institutions in meeting their compliance obligations.

Overall, the advantages of IBAN include increased efficiency, accuracy, cost-effectiveness, and security in international transactions. By adopting IBAN as the standard identification system for bank accounts, the banking industry can experience improved operational processes, reduced errors, and enhanced customer experiences when conducting cross-border payments.

Using IBAN for International Payments

The International Bank Account Number (IBAN) is widely used for facilitating international payments. By incorporating IBAN into the payment process, banks and financial institutions can ensure accurate and efficient fund transfers across borders. Here are some key aspects of using IBAN for international payments:

- Identifying the Recipient: When making an international payment, the IBAN serves as a crucial piece of information to identify the recipient’s bank account. It helps to ensure that the funds are credited to the correct account and reduces the risk of misdirected transactions. The IBAN provides a standardized and internationally recognized format for account identification.

- Transferring Funds: To initiate an international payment, the sender’s bank requires the IBAN of the recipient’s bank account. With the IBAN, the sender’s bank can accurately route the funds to the correct recipient’s account by referencing the specific bank and account details provided in the IBAN.

- Automated Processing: IBAN enables the automation of international payment processes. Financial institutions can utilize technology and systems to quickly validate and process IBANs, reducing the need for manual intervention. This automation leads to faster and more efficient fund transfers.

- Exchange Rate Conversion: When making international payments, IBAN does not directly handle currency conversion. The exchange rate conversion typically occurs through the sending bank or a third-party provider. However, IBAN facilitates the accurate transfer of funds to the intended recipient’s account, regardless of the currency being used.

- Payment Tracking: IBAN also enables tracking of international payments. Through the use of IBAN, banks and financial institutions can monitor the progress of transactions and provide updates to the sender and receiver regarding the status of the payment. This tracking feature helps improve transparency and provides peace of mind to both parties involved in the transaction.

It is important to note that while IBAN is widely used for international payments, some countries may have additional requirements or alternative systems in place. Therefore, it is essential to ensure that you have the correct and up-to-date IBAN for the recipient’s country before initiating an international payment.

In summary, IBAN is a vital component of international payments, enabling accurate identification of recipients’ bank accounts and facilitating efficient fund transfers. With the use of IBAN, banks and financial institutions can automate payment processes, track transactions, and ensure that funds are efficiently and securely transferred across borders.

Verifying the Validity of an IBAN

Verifying the validity of an International Bank Account Number (IBAN) is essential to ensure that the provided IBAN is accurate and can be used for international transactions. Although the structure of IBANs varies by country, there are several methods you can use to validate an IBAN:

- Use an IBAN Validation Tool: Many online tools and websites offer IBAN validation services. These tools allow you to input the IBAN and instantly check its validity. The tool will verify if the IBAN follows the correct structure and has the correct check digits, ensuring that it is a valid IBAN.

- Check with the Recipient’s Bank: If you are making a payment to a specific individual or organization, you can contact their bank directly to verify the IBAN. Provide the full details of the recipient, including the IBAN, and ask the bank to confirm if the provided IBAN is correct.

- Use Official Bank Websites: Access the official website of the recipient’s bank and look for their IBAN validation tool or service. Many banks provide an online platform where you can enter the IBAN and receive confirmation if it is a valid IBAN for their institution.

- Double-Check the IBAN Structure: Understand the correct IBAN structure for the recipient’s country. Each country has specific requirements for the length and format of the IBAN. By comparing the provided IBAN against the correct structure, you can identify any potential errors or discrepancies.

- Review the Check Digits: The check digits in an IBAN are crucial for validating its accuracy. These digits enable banks to verify the integrity of the IBAN. By calculating the check digits based on the specified algorithm for the country, you can compare them with the provided IBAN to ensure they match.

It is important to note that while these methods can help verify the validity of an IBAN, they do not guarantee the existence of the account or the accuracy of other details associated with the account. IBAN validation primarily confirms that the provided IBAN follows the correct structure and has the correct check digits.

By taking the necessary steps to verify the validity of an IBAN, you can ensure the accuracy of your payment details and reduce the risk of sending funds to the wrong recipient or account. It is crucial to be diligent and thorough in checking the IBAN before initiating any international transactions.

Frequently Asked Questions about IBAN

Here are some common questions that arise when discussing the International Bank Account Number (IBAN) and its usage in international transactions:

Q: Can I use IBAN for domestic transactions?

A: While IBAN was primarily introduced for international transactions, some countries have adopted the use of IBAN for domestic payments as well. It is important to check with your local banking authorities or consult your bank to determine if IBAN is required for domestic transfers in your country.

Q: Can an IBAN include special characters?

A: No, IBANs typically do not include special characters. They primarily consist of uppercase letters and digits. Certain countries may have specific rules regarding the inclusion of certain characters or leading zeros, so it is important to understand the IBAN format for the specific country in question.

Q: Can an IBAN be used for all types of transactions?

A: Yes, IBAN can be used for various types of transactions, including bank transfers, direct debits, and international payments. It serves as a standardized account identifier that ensures accurate routing and allocation of funds across borders.

Q: What happens if I provide an incorrect IBAN for a payment?

A: Providing an incorrect IBAN can result in failed or delayed transactions. It is crucial to double-check the accuracy of the provided IBAN before initiating any international payments. In case of an error, the funds may be returned to the sender, or they may need to contact the recipient or recipient’s bank to rectify the situation.

Q: How long is an IBAN valid?

A: An IBAN is typically valid as long as the associated bank account remains active. However, it is important to note that changes in personal or banking details may require updating the IBAN. If there are any changes in the account holder’s information, it is advisable to inform the relevant bank and update the IBAN accordingly.

Q: Do all countries use IBAN?

A: While IBAN is widely adopted across many countries, not all countries use IBAN. Some countries may have their own unique systems for identifying bank accounts in international transactions. It is important to confirm the specific requirements based on the countries involved in the transaction.

These are just a few of the most frequently asked questions about IBAN. If you have additional questions or concerns, it is recommended to consult your bank or financial institution for further guidance specific to your situation.

Conclusion

The International Bank Account Number (IBAN) has become an integral part of the global banking system, providing a standardized format for identifying bank accounts in international transactions. By adopting IBAN, financial institutions can enhance the accuracy, efficiency, and security of cross-border payments.

IBAN simplifies the identification and verification of bank accounts, reducing errors and delays caused by inconsistent local account numbering systems. Through its structure, which includes country codes, check digits, bank identifiers, and account numbers, IBAN allows for accurate routing and allocation of funds to the intended recipients.

With IBAN, the process of transferring funds across borders becomes more efficient. Banks and financial institutions can automate payment processes, reduce manual intervention, and provide faster processing times. This automation not only improves efficiency but also contributes to cost savings.

Moreover, IBAN plays a crucial role in enhancing security and fraud prevention. By validating the accuracy of the recipient’s account details, it reduces the risk of funds being sent to incorrect or unauthorized accounts. This increases the trust and reliability of international transactions.

It is important to note that each country may have its own IBAN format and additional requirements. Therefore, it is essential to ensure that the provided IBAN follows the correct structure for the recipient’s country. Validating the IBAN using online tools or confirming with the recipient’s bank helps ensure accurate information and successful transactions.

In conclusion, IBAN serves as a global standard for identifying bank accounts in international transactions. Its advantages include standardization, accuracy, efficiency, cost-effectiveness, security, and compliance facilitation. By leveraging IBAN, financial institutions and individuals can enjoy the benefits of streamlined and reliable cross-border payments, supporting global trade and facilitating economic growth.