Introduction

Welcome to the world of accounting, where financial transactions are accurately recorded and reported. In the realm of accounting, short-term investments play a crucial role in managing a company’s financial resources. These investments are a key component in a company’s overall investment portfolio and are typically held for a short period of time, usually less than one year.

Short-term investments serve a variety of purposes, ranging from generating additional income to managing cash flows and taking advantage of investment opportunities. In this article, we will delve into the definition, purpose, types, characteristics, accounting treatment, valuation, risks, and examples of short-term investments in the accounting world.

Understanding the concept of short-term investments is essential for businesses and individuals alike. By gaining insights into these investments, companies can optimize their financial strategies and individuals can make informed decisions about their personal finances. So, let’s dive into the fascinating world of short-term investments and uncover the valuable insights they provide!

Definition of Short-Term Investments

Short-term investments, also known as marketable securities, are financial instruments that are easily convertible into cash within a short period of time, usually one year or less. These investments are typically made with the intention of earning a return on excess funds that are not immediately needed for day-to-day operations.

Short-term investments can take various forms, including Treasury bills, certificates of deposit (CDs), commercial paper, money market funds, and short-term corporate bonds. What distinguishes these investments from long-term investments is their short maturity period. Unlike long-term investments, which are held for an extended period, short-term investments provide liquidity and flexibility to investors, ensuring that funds are readily available when needed.

One key aspect of short-term investments is their low level of risk compared to long-term investments. While the potential returns may be lower, they offer greater stability and protection of capital. In uncertain economic times, many investors turn to short-term investments as a safe haven for their funds, allowing them to preserve capital while earning a modest return.

Short-term investments are often used as a means of temporarily parking excess cash. For businesses, this can arise from seasonal fluctuations in cash flow or from the need to set aside funds for upcoming expenses. Similarly, individuals may choose to invest their excess savings in short-term instruments to earn a higher return compared to traditional savings accounts.

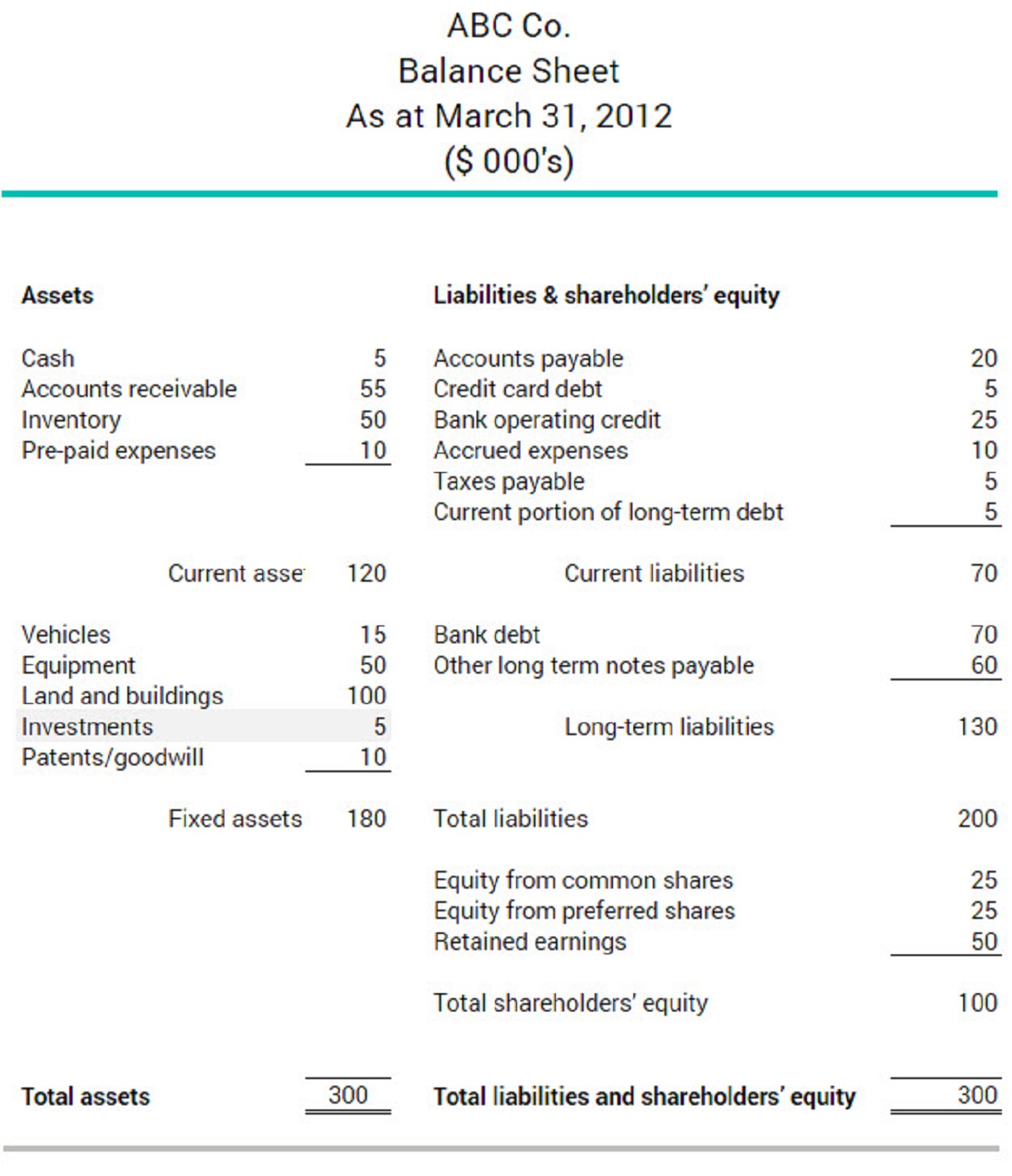

These investments are classified as current assets on a company’s balance sheet, as they are expected to be converted into cash within the next operating cycle. This classification allows investors and stakeholders to assess a company’s short-term liquidity position and its ability to meet its financial obligations.

Now that we have a clear understanding of the definition and purpose of short-term investments, let’s explore the different types of investments that fall under this category.

Purpose of Short-Term Investments

Short-term investments serve various purposes for businesses and individuals. Understanding these purposes can help investors make informed decisions about allocating their funds and managing their financial goals. Let’s explore some of the key purposes of short-term investments:

1. Generating Income: One of the primary purposes of short-term investments is to earn additional income. These investments are typically designed to generate a return on the excess funds that are not immediately needed for day-to-day operations. By investing in short-term instruments, individuals and businesses can earn interest or dividends, thereby increasing their overall income. This additional income can be reinvested or used to meet short-term financial obligations.

2. Managing Cash Flow: Short-term investments play a vital role in managing cash flow for businesses. There are times when businesses experience fluctuations in their cash flow due to seasonal demand, delayed payments from customers, or unforeseen expenses. During periods of excess cash, businesses can invest in short-term instruments to maximize returns. Conversely, during times of cash shortage, these investments can be easily liquidated to cover immediate expenses.

3. Preserving Capital: Short-term investments are often considered a safe haven for preserving capital. While they may offer lower potential returns compared to long-term investments, these investments have a lower level of risk. By investing in short-term instruments, individuals and businesses can protect their capital from market volatility and economic uncertainties.

4. Taking Advantage of Investment Opportunities: Short-term investments provide the flexibility to quickly take advantage of investment opportunities. When attractive investment options arise, investors can liquidate their short-term investments to capture those opportunities. This agility allows individuals and businesses to capitalize on potential gains and optimize their overall investment strategy.

5. Diversification: Short-term investments also serve as a means of diversifying an investment portfolio. By allocating funds to various short-term instruments with different risk profiles, investors can reduce their overall investment risk. This diversification can help protect against potential losses and provides a balanced approach to managing investments.

Understanding the purposes of short-term investments is essential for effectively managing financial resources. By aligning short-term investment strategies with specific goals, investors can achieve their desired outcomes while maintaining adequate liquidity and minimizing risk. Now that we have explored the purposes of short-term investments, let’s delve into the different types of investments that fall into this category.

Types of Short-Term Investments

Short-term investments encompass a wide range of financial instruments that offer liquidity and a relatively short maturity period. Let’s explore some of the common types of short-term investments:

1. Treasury Bills: Treasury bills, also known as T-bills, are short-term debt securities issued by governments to raise funds. They typically have a maturity period of less than one year, such as 3 months, 6 months, or 12 months. Treasury bills are considered highly secure investments as they are backed by the government, and the interest earned is exempt from state and local taxes.

2. Certificates of Deposit (CDs): CDs are time deposits offered by banks and financial institutions to investors. They have a fixed term, ranging from a few weeks to several years, and offer a fixed interest rate. CDs are low-risk investments, and the longer the term, the higher the interest rate. However, early withdrawal may incur penalties.

3. Commercial Paper: Commercial paper represents short-term unsecured promissory notes issued by corporations. These notes are typically issued to meet short-term funding needs and are backed by the issuing company’s creditworthiness. Commercial paper is considered relatively safe, but riskier than government-backed securities.

4. Money Market Funds: Money market funds are mutual funds that invest in short-term debt securities, such as Treasury bills, certificates of deposit, and commercial paper. These funds aim to maintain a stable net asset value (NAV) per share of $1. Money market funds provide liquidity, diversification, and typically offer higher yields than traditional savings accounts.

5. Short-Term Corporate Bonds: Short-term corporate bonds are debt securities issued by companies with a maturity period of one year or less. These bonds pay a fixed interest rate and offer higher yields than Treasury bills. However, they carry a slightly higher level of risk as they depend on the creditworthiness of the issuing company.

6. Savings Accounts: While not technically an investment, savings accounts allow individuals to deposit their excess funds in a bank, earning interest on their balance. Savings accounts offer a high level of liquidity and are considered a safe option for short-term investments. However, the interest rates are relatively low compared to other short-term investment options.

These are just a few examples of short-term investments available in the market. It’s important to consider the risk profile, expected return, and liquidity of each investment option before making a decision. Now that we have explored the types of short-term investments, let’s move on to understanding the key characteristics of these investments.

Characteristics of Short-Term Investments

Short-term investments possess certain characteristics that set them apart from other investment options. Understanding these key characteristics is essential for investors to make informed decisions and effectively manage their financial portfolios. Let’s explore the notable characteristics of short-term investments:

1. Liquidity: Short-term investments offer high liquidity, meaning they can be easily converted into cash without incurring significant losses. This characteristic allows investors to access their funds quickly, providing flexibility in managing cash flow and taking advantage of investment opportunities.

2. Low Risk: Compared to long-term investments, short-term investments generally carry lower levels of risk. Government-backed securities, such as Treasury bills, are considered to have the lowest risk as they are backed by the creditworthiness of the government. Short-term investments diversify risk by providing a stable and secure avenue for preserving capital.

3. Short Maturity Period: As the name suggests, short-term investments have relatively short maturity periods. Typically, these investments have a maturity of one year or less, providing investors with quick access to their funds. The short-term nature of these investments allows investors to adjust their investment strategy based on market conditions and changing financial goals.

4. Income Generation: Short-term investments are designed to generate income for investors through interest payments, dividends, or capital gains. While the potential returns may be lower compared to long-term investments, the focus is on preserving capital and generating a consistent income stream.

5. Preservation of Capital: Preserving capital is an essential characteristic of short-term investments. These investments aim to protect the initial investment amount by minimizing the risk of loss. The focus is on maintaining the principal amount while earning a reasonable return within a short period.

6. Minimal Price Volatility: Short-term investments generally exhibit minimal price volatility compared to long-term investments. This is due to their shorter duration and lower exposure to potential market fluctuations. The stability of short-term investments provides a sense of security to investors seeking to preserve their capital.

7. Diversification: Short-term investments offer diversification benefits to investors. By allocating funds across various short-term instruments, investors can mitigate risk and reduce dependence on a single investment. Diversification helps to enhance overall portfolio stability and potentially increase returns.

8. Regulatory Oversight: Short-term investments are subject to regulatory oversight, particularly in the case of money market funds. Regulatory bodies monitor the operations and investments of these funds to ensure compliance and safeguard investor interests.

Understanding the characteristics of short-term investments allows investors to align their investment strategies with their financial goals and risk tolerance. Now that we have explored the key characteristics of short-term investments, let’s move on to understanding how these investments are treated in accounting.

Accounting Treatment of Short-Term Investments

The accounting treatment of short-term investments is essential for accurately reporting a company’s financial position and performance. These investments are classified as current assets on the balance sheet, as they are expected to be converted into cash within the next operating cycle. Let’s delve into the accounting treatment of short-term investments:

1. Initial Recognition: When a company acquires a short-term investment, it is initially recorded at its cost, which includes the acquisition price and any transaction costs incurred.

2. Valuation: Short-term investments are subsequently measured at fair value on the balance sheet. Fair value represents the amount that would be received if the investment were to be sold in an orderly transaction between market participants on the measurement date.

3. Unrealized Gains and Losses: Changes in the fair value of short-term investments are recognized as unrealized gains or losses in the income statement. For available-for-sale investments, these unrealized gains or losses are reported as a separate component of equity, known as other comprehensive income.

4. Interest and Dividend Income: Any interest or dividend income earned from short-term investments is recognized in the income statement as revenue. This income is reported in the period in which it is earned, regardless of when it is received.

5. Impairment: If there is an indication that the value of a short-term investment has become impaired, a company is required to assess whether there has been a significant decline in the investment’s fair value. If the decline is deemed significant and is expected to be prolonged, an impairment loss is recognized.

6. Disclosure: Companies are required to disclose relevant information about their short-term investments in the financial statements. This includes the nature and terms of the investments, fair value measurements, and any significant concentration of risk associated with the investments.

It is important for companies to carefully evaluate and monitor their short-term investments to ensure accurate and transparent reporting. By adhering to the appropriate accounting standards and guidelines, companies can provide stakeholders with meaningful information about their investment activities and their impact on financial performance.

Now that we have examined the accounting treatment of short-term investments, let’s move on to the valuation methods used to determine their fair value.

Valuation of Short-Term Investments

The valuation of short-term investments is crucial for determining their fair value and assessing their financial impact on a company’s balance sheet. Fair value represents the price that would be received if the investment were to be sold in an orderly transaction between market participants. Let’s explore the common valuation methods used for short-term investments:

1. Market Price: The market price is the most straightforward method of valuing short-term investments that are actively traded in a financial market. It represents the actual price at which the investment is bought or sold in the open market. Market prices provide real-time and reliable information on the current value of the investment.

2. Net Realizable Value: Net realizable value is a valuation method used when the market price is not readily available or when the investment is impaired. It represents the estimated amount that would be realized from selling the investment, net of any selling costs. Net realizable value takes into account factors such as market conditions, liquidity, and other relevant factors affecting the investment’s saleability.

3. Amortized Cost: The amortized cost method is used for short-term investments that have a fixed maturity and are held to maturity. These investments are initially recognized at cost and subsequently measured at their amortized cost, taking into consideration any premium or discount from the initial investment amount. This method assumes that the investment will be held until maturity and calculates the yield to maturity.

4. Appraised Value: In some cases, short-term investments may be valued by an independent appraiser. This method is usually employed for complex or illiquid investments that do not have readily available market prices. The appraiser assesses the investment’s value based on various factors such as cash flow projections, market conditions, and industry trends.

5. Binomial Model: For certain short-term investments with embedded options or complex features, a binomial model may be used for valuation. This model takes into account various factors such as the probability of different outcomes and their corresponding values to calculate the investment’s fair value.

It is important for companies to use consistent and appropriate valuation methods for short-term investments to ensure accuracy and comparability in financial reporting. Regular assessment and monitoring of these investments are necessary to reflect their fair value in the financial statements. Additionally, companies must disclose the valuation methods used and any significant assumptions or estimates made in determining the fair value of their short-term investments.

Now that we have explored the valuation methods used for short-term investments, let’s move on to understanding the risks associated with these investments.

Risks Associated with Short-Term Investments

While short-term investments are generally considered less risky than long-term investments, they are not entirely devoid of risks. It is important for investors to be aware of these risks and factor them into their decision-making process. Let’s explore some of the common risks associated with short-term investments:

1. Interest Rate Risk: Short-term investments are influenced by changes in interest rates. When interest rates rise, the value of existing fixed-income investments may decline. This is because newly issued investments offer higher yields, making existing investments less attractive. Conversely, when interest rates fall, the value of fixed-income investments may rise. Therefore, investors need to consider the potential impact of interest rate movements on their short-term investments.

2. Credit Risk: Credit risk refers to the possibility of the issuer defaulting on interest or principal payments. While short-term investments are generally considered low risk, there is still the potential for an issuer to default on its obligations. Investing in short-term instruments issued by reputable entities and conducting thorough credit analysis can help manage credit risk.

3. Market Risk: Short-term investments can be affected by market volatility and fluctuations. External factors such as economic conditions, political events, or market sentiment can impact the value of these investments. It is important to be aware of market risk and diversify investments to mitigate the potential impact of adverse market movements.

4. Liquidity Risk: Although short-term investments are generally liquid, there can be instances where selling these investments may be challenging. Illiquid markets or specific investment characteristics may limit the ability to convert the investment into cash quickly. Investors should consider the liquidity profile of their short-term investments and the potential impact on their ability to access funds when needed.

5. Inflation Risk: Inflation can erode the purchasing power of investment returns. If the rate of inflation exceeds the rate of return on short-term investments, the investor may experience a loss in real terms. It is important to consider inflation risk and seek investments that offer returns that outpace inflation to maintain the value of investments over time.

6. Regulatory and Legislative Risk: Changes in laws and regulations can impact the value and performance of short-term investments. For example, changes in tax laws or regulations governing specific types of investments can affect the after-tax returns. Staying informed about regulatory changes and their potential impact is important for investors.

While short-term investments offer certain advantages, it is crucial to assess and manage the associated risks. Diversification, conducting thorough research, and staying informed about market conditions and economic trends can help mitigate these risks. Now that we have explored the risks associated with short-term investments, let’s move on to examining examples of commonly held short-term investment instruments.

Examples of Short-Term Investments

Short-term investments encompass a wide range of financial instruments that offer liquidity and a relatively short maturity period. Let’s take a look at some commonly held examples of short-term investments:

1. Treasury Bills (T-bills): Treasury bills are short-term debt securities issued by governments to raise funds. They are considered one of the safest investments as they are backed by the creditworthiness of the government. T-bills have a maturity period of less than one year, such as 3 months, 6 months, or 12 months, and offer competitive yields in relation to their low risk.

2. Certificates of Deposit (CDs): CDs are time deposits offered by banks and financial institutions. They have a fixed term, ranging from a few weeks to several years, and offer a fixed interest rate. CDs are generally considered low-risk investments. The longer the term, the higher the interest rate, providing investors with flexibility in choosing their investment horizon.

3. Money Market Funds: Money market funds are mutual funds that invest in short-term debt securities, such as Treasury bills, commercial paper, and certificates of deposit. These funds aim to maintain a stable net asset value (NAV) of $1 per share and are regulated to ensure liquidity and safety. Money market funds offer a convenient and diversified option for short-term investments.

4. Commercial Paper: Commercial paper represents short-term unsecured promissory notes issued by corporations. These notes have a maturity of typically 270 days or less and are used by companies to meet short-term funding needs. Commercial paper is generally issued by highly rated companies and offers competitive yields compared to other short-term investments.

5. Treasury Notes and Bonds: Treasury notes and bonds are longer-term debt securities issued by the government. While they are not classified as short-term investments, they can be purchased with shorter remaining maturities, such as less than one year. Treasury notes have maturities ranging from 2 to 10 years, while Treasury bonds have maturities exceeding 10 years. They offer fixed interest payments and are considered low-risk investments.

6. Savings Accounts: While not technically an investment, savings accounts offer a secure and easily accessible short-term parking option for excess funds. These accounts are typically offered by banks and credit unions and provide a modest interest rate with high liquidity. Savings accounts are suitable for individuals who prioritize liquidity and safety over higher returns.

These are just a few examples of short-term investments available to individuals and businesses. Each investment option varies in terms of risk, return, and liquidity. It is important to carefully consider individual financial goals, risk tolerance, and market conditions when selecting short-term investments.

Now that we have explored examples of short-term investments, let’s conclude our discussion by summarizing the key insights gained.

Conclusion

Short-term investments play a vital role in managing financial resources for both businesses and individuals. These investments offer liquidity, preservation of capital, and the potential for generating income over a short period. Through careful consideration of various factors such as risk tolerance, return expectations, and investment horizon, investors can optimize their short-term investment strategies.

In this article, we explored the definition of short-term investments, their purpose, types, characteristics, accounting treatment, valuation, risks, and examples. Short-term investments are easily convertible into cash within a year or less, and they serve purposes such as generating income, managing cash flow, preserving capital, and taking advantage of investment opportunities.

We discussed types of short-term investments, including Treasury bills, certificates of deposit, money market funds, commercial paper, and short-term corporate bonds. These investments offer diverse options with varying degrees of risk and return potential.

The characteristics of short-term investments, such as liquidity, low risk, short maturity period, income generation, and capital preservation, make them attractive investment options for individuals and businesses. It is crucial to understand these characteristics to align investment strategies with financial goals and risk appetite.

Accounting treatment of short-term investments involves initial recognition, valuation at fair value, recognition of unrealized gains and losses, and disclosure in financial statements. Accurate accounting ensures transparency and proper evaluation of a company’s financial position.

We also discussed the risks associated with short-term investments, including interest rate risk, credit risk, market risk, liquidity risk, inflation risk, and regulatory risk. Being aware of these risks is crucial for making informed investment decisions and implementing risk management strategies.

Lastly, we explored examples of short-term investments, such as Treasury bills, certificates of deposit, money market funds, commercial paper, and savings accounts. Each investment option presents unique characteristics and considerations for investors.

By understanding the various aspects of short-term investments, individuals and businesses can effectively manage their financial resources and make informed investment decisions to achieve their desired financial outcomes.