Introduction

Welcome to the digital age, where almost every aspect of our lives can be conveniently managed online. From shopping to communication, the internet has revolutionized the way we interact with the world. One of the most significant advancements in this digital landscape is the emergence of electronic commerce, or e-commerce. As technology continues to advance, e-commerce has become an integral part of our daily lives, providing us with a vast array of products and services available at our fingertips.

So, what exactly is e-commerce? In simple terms, e-commerce refers to the buying and selling of goods and services over the internet. It involves the use of various electronic platforms such as websites, mobile applications, and online marketplaces to facilitate transactions between buyers and sellers. With the power of e-commerce, consumers can conveniently browse and purchase products from the comfort of their own homes, while businesses can expand their reach and tap into global markets.

E-commerce can be classified into different types based on the nature of the transactions. These types include Business-to-Consumer (B2C), Business-to-Business (B2B), Consumer-to-Consumer (C2C), and Consumer-to-Business (C2B). Each type has its own unique characteristics and target audience. However, one specific type of e-commerce that has gained tremendous popularity in recent years is online banking.

Online banking, also known as electronic banking or internet banking, allows individuals to conduct financial transactions and manage their accounts through the internet. Gone are the days of waiting in long queues at the bank, as online banking provides a convenient and secure way to handle all your banking needs. With just a few clicks, you can transfer funds, pay bills, check account balances, and even apply for loans, all from the comfort of your own home or on-the-go through a mobile app.

As technology continues to advance, online banking has evolved to offer a wide range of features and services. The convenience, accessibility, and time-saving benefits of online banking make it a popular choice for individuals and businesses alike. In the following sections, we will explore the key features of online banking, the various types of transactions you can perform, the benefits it offers, and the security measures put in place to protect your financial information.

Definition of E-commerce

E-commerce, short for electronic commerce, is the buying and selling of goods and services over the internet. It involves the use of electronic platforms such as websites, mobile applications, and online marketplaces to facilitate transactions between buyers and sellers. With the advent of the internet and technological advancements, e-commerce has transformed the way businesses operate and consumers shop.

In e-commerce, transactions are conducted electronically, eliminating the need for physical presence or face-to-face interactions. This convenience has revolutionized the way people conduct business and has opened up opportunities for both small and large enterprises to reach a global customer base. E-commerce allows businesses to showcase their products or services online, provide detailed descriptions, images, and customer reviews, and offer secure payment gateways for seamless transactions.

E-commerce can be classified into different types based on the parties involved in the transactions. The most common types include:

- Business-to-Consumer (B2C): This refers to transactions between businesses and individual consumers. Online retail stores, such as Amazon and eBay, are prime examples of B2C e-commerce. Consumers can browse through a wide variety of products, compare prices, and make purchases directly from the business’s website.

- Business-to-Business (B2B): B2B e-commerce involves transactions between businesses. This type of e-commerce is commonly used for sourcing raw materials, components, or services required for business operations. Online marketplaces and platforms like Alibaba and ThomasNet serve as intermediaries connecting businesses with suppliers.

- Consumer-to-Consumer (C2C): C2C e-commerce enables consumers to sell products or services directly to other consumers. Popular platforms like Craigslist and eBay classifieds allow individuals to post listings and connect with potential buyers.

- Consumer-to-Business (C2B): In C2B e-commerce, consumers offer their products or services to businesses. This includes freelancers, influencers, or content creators who sell their skills or content to companies. Websites like Upwork and Fiverr act as intermediaries connecting individuals with businesses.

Overall, e-commerce has revolutionized the way we shop, connect, and conduct business. It offers convenience, accessibility, and a global reach for both buyers and sellers. With the continuous advancement of technology, e-commerce is expected to grow further, opening new opportunities for businesses and providing consumers with more choices and seamless shopping experiences.

Classification of E-commerce

E-commerce, or electronic commerce, can be classified into various types based on different factors. These classifications help in understanding the nature of transactions and the parties involved. Let’s explore the different classifications of e-commerce:

- Based on the parties involved:

- Business-to-Consumer (B2C): This type of e-commerce involves transactions between businesses and individual consumers. B2C e-commerce is commonly seen in online retail, where businesses sell products directly to consumers through their websites or online marketplaces. The rise of platforms like Amazon and eBay has massively contributed to the growth of B2C e-commerce.

- Business-to-Business (B2B): B2B e-commerce refers to transactions between businesses. In this type, companies purchase products or services from other companies to support their own operations. B2B e-commerce is often used for procurement of raw materials, components, or services required for manufacturing or other business processes.

- Consumer-to-Consumer (C2C): C2C e-commerce enables individuals to sell products or services to other individuals. Online marketplaces and classified platforms like eBay, Craigslist, and Facebook Marketplace facilitate C2C transactions. Here, individuals can list their items for sale, negotiate prices, and complete transactions directly with other consumers.

- Consumer-to-Business (C2B): In C2B e-commerce, consumers offer their products or services to businesses. This can include freelancers, influencers, or content creators who sell their skills or content to companies. C2B platforms like Upwork and Fiverr act as intermediaries, connecting individuals with businesses seeking their services.

- Based on the type of products or services:

- Physical goods: E-commerce allows businesses to sell physical products online, ranging from electronics, clothing, and home appliances to books, toys, and furniture. Customers can browse through product descriptions, images, and customer reviews before making a purchase.

- Digital goods: This category includes digital products like e-books, music, software, and video games that can be purchased and downloaded online. Digital goods are highly convenient as they can be instantly accessed and do not require physical shipping.

- Services: E-commerce has extended to the service industry, allowing customers to book services online. This includes travel bookings, hotel reservations, appointment scheduling for healthcare providers, and even online tutoring or consulting services.

- Based on the platform:

- Online marketplaces: These platforms bring together multiple sellers and buyers, facilitating transactions between them. Examples include Amazon, eBay, and Alibaba.

- Branded websites: Many businesses have their own websites to showcase and sell their products directly to consumers. These websites provide a personalized shopping experience and allow businesses to establish their brand identity.

- Mobile commerce: With the rise of smartphones and mobile apps, mobile commerce or m-commerce has gained popularity. Customers can make purchases, conduct transactions, and access online services through mobile applications.

These classifications provide a framework for understanding the different types and models of e-commerce. Each type has its own characteristics, target audience, and unique features, catering to the diverse needs and preferences of consumers and businesses. As technology continues to evolve, new forms of e-commerce are likely to emerge, offering more innovative ways to engage in online transactions.

Overview of Online Banking

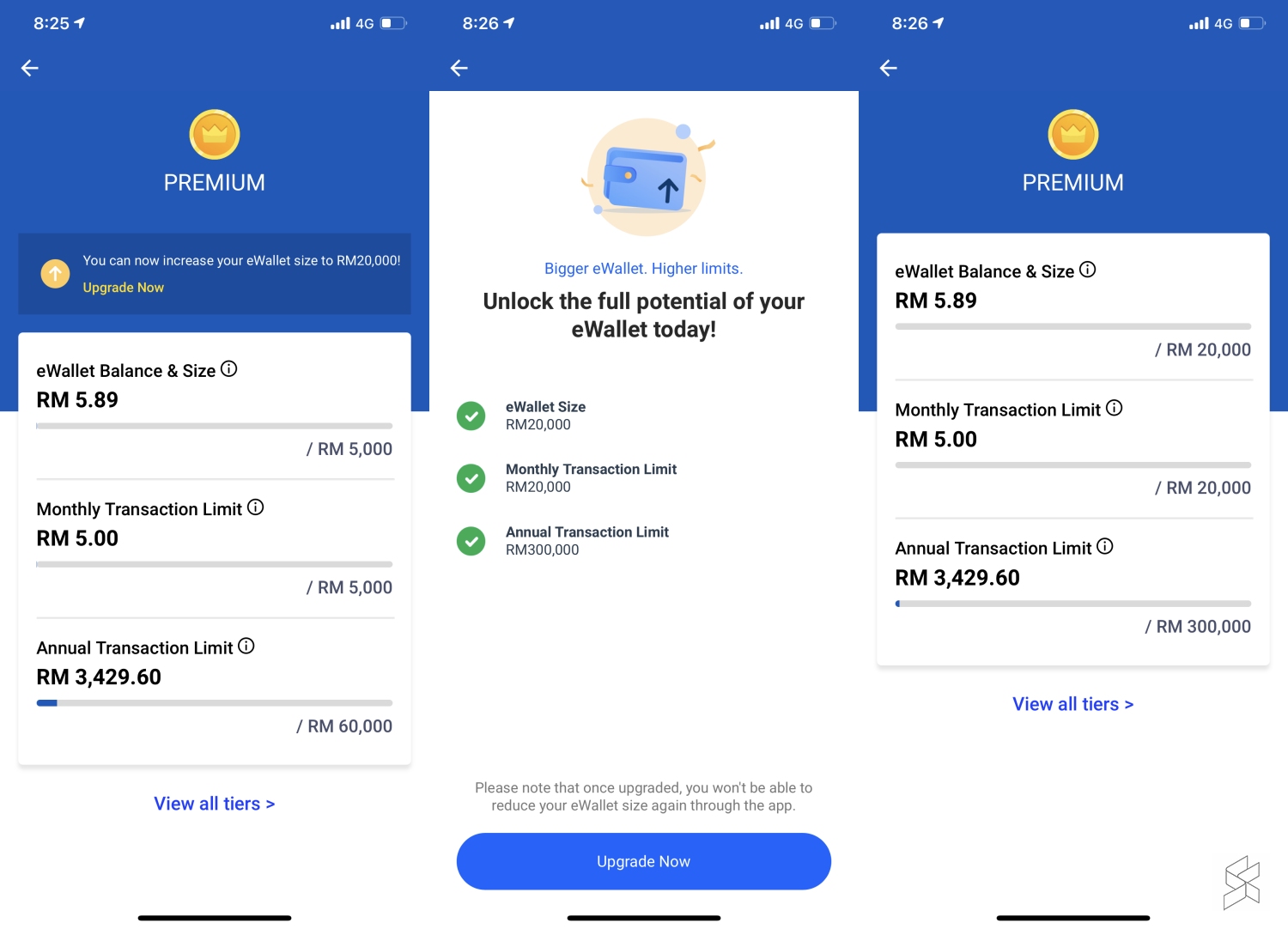

Online banking, also known as electronic banking or internet banking, has revolutionized the way we manage our finances. It provides individuals with the convenience and flexibility to access their bank accounts, conduct various financial transactions, and perform banking activities from the comfort of their own homes or on-the-go through a mobile app.

With online banking, customers can perform a wide range of banking activities without the need to visit a physical bank branch. These activities include checking account balances, viewing transaction history, transferring funds between accounts, paying bills, setting up automatic payments, and even applying for loans or opening new accounts. The ability to perform these tasks at any time and from anywhere in the world has made online banking increasingly popular and convenient.

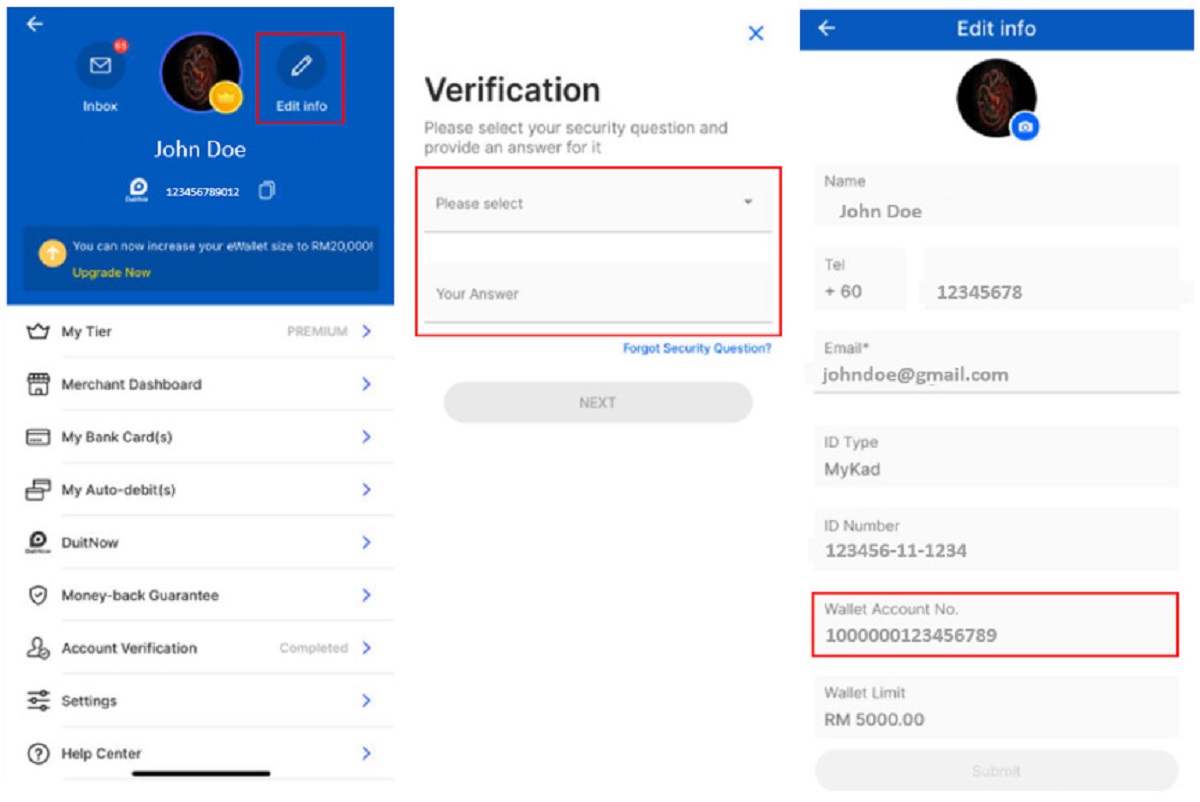

Most banks offer online banking services through their secure websites or dedicated mobile banking applications. Customers can access their accounts by logging in with their unique usernames and passwords. Some banks even provide additional security measures, such as two-factor authentication or biometric authentication, to ensure the safety of their customers’ financial information.

Online banking platforms provide a user-friendly interface that allows customers to navigate through different sections and perform their desired transactions with ease. Account summaries, transaction history, and account statements are readily available for customers to track their finances and monitor their spending. Many online banking platforms also offer personal financial management tools and budgeting features to help customers manage their money effectively.

Another significant feature of online banking is the ability to link external accounts. This allows customers to view their accounts from different banks or financial institutions in one place, providing a holistic view of their finances. Customers can also initiate transfers between these linked accounts, making it convenient to manage and move funds between different financial institutions.

Furthermore, online banking offers enhanced communication channels between customers and their banks. Customers can easily send messages, inquiries, or requests to their bank through secure messaging systems. The bank’s customer support team can then respond and address the queries promptly, providing efficient customer service.

In summary, online banking has transformed the way we interact with our banks and manage our finances. It eliminates the need for physical visits to bank branches, saving time and providing convenience. With features such as account management, transaction history, bill payment, and communication channels, online banking offers a comprehensive suite of services to empower customers and streamline their banking experience.

Key Features of Online Banking

Online banking offers a range of key features that enhance the convenience, accessibility, and efficiency of managing financial transactions. These features empower customers to take control of their finances and simplify the banking process. Let’s explore some of the key features of online banking:

- Account Access: Online banking provides customers with 24/7 access to their bank accounts. Customers can log in to their accounts at any time, view their balances, and check transaction history. This feature allows individuals to stay updated on their financial status and monitor their spending.

- Fund Transfers: Online banking enables customers to transfer funds between their own accounts or to other accounts within the same bank or different financial institutions. Customers can easily initiate transfers, set up recurring transfers, or schedule future-dated transfers, providing flexibility and convenience in managing their finances.

- Bill Payment: With online banking, customers can conveniently pay their bills online. This feature allows customers to set up one-time or recurring payments for utilities, credit cards, loans, and other expenses. It eliminates the need for writing checks or visiting physical locations to make payments, saving time and effort.

- Mobile Banking: Many banks offer dedicated mobile banking applications, allowing customers to access their accounts from their smartphones or tablets. Mobile banking offers all the features of online banking, but with the added convenience of accessing accounts on the go. Customers can perform transactions, monitor their accounts, and receive notifications directly on their mobile devices.

- Electronic Statements: Online banking provides customers with electronic statements, also known as e-statements or e-documents. Instead of receiving paper statements through traditional mail, customers can access their account statements electronically. E-statements are secure, easily accessible, and help reduce paper waste.

- Alerts and Notifications: Online banking allows customers to set up alerts and notifications for various account activities. Customers can receive notifications for account balance updates, transaction alerts, bill payment reminders, and more. These alerts help customers stay informed about their finances and prevent unauthorized transactions.

- Secure Messaging: Online banking platforms often include secure messaging systems that allow customers to communicate directly with their bank’s customer support team. Customers can send inquiries, report issues, or request assistance securely through these messaging systems. This feature ensures that customers can receive prompt and secure support for their banking needs.

- Account Aggregation: Many online banking platforms allow customers to link external accounts from different financial institutions. This aggregation feature provides a centralized view of all linked accounts, enabling customers to monitor and manage their finances from one place. It simplifies tracking balances, transactions, and helps with overall financial management.

These key features of online banking enhance the banking experience by offering flexibility, convenience, and real-time access to financial information. The ability to perform transactions, manage accounts, and communicate with the bank anytime and anywhere empowers customers to take control of their finances and streamline their banking activities.

Types of Transactions in Online Banking

Online banking provides customers with a wide range of transactions that can be conveniently performed through internet-based platforms or mobile banking applications. These transactions offer flexibility, efficiency, and accessibility to manage various financial activities. Let’s explore some of the common types of transactions in online banking:

- Balance Inquiry: Customers can check their account balances online, allowing them to monitor their available funds, savings, and investments. Online banking provides real-time balance updates, reducing the need to visit a bank branch or use an ATM.

- Money Transfers: Online banking offers the flexibility to transfer funds between accounts within the same bank or to accounts in other financial institutions. Customers can initiate one-time or recurring transfers, making it convenient to send money to family, friends, or pay bills. Online banking also allows customers to set up wire transfers for larger transactions.

- Bill Payments: With online banking, customers can easily pay bills electronically. They can set up automatic bill payments, schedule future-dated payments, or make one-time payments for utilities, credit cards, loans, and other recurring expenses. This feature eliminates the need for writing checks or visiting physical locations to make payments.

- Deposit and Withdrawal: Online banking enables customers to deposit checks remotely by taking a picture of the check and submitting it through the mobile banking app. Customers can also initiate electronic funds transfers to deposit money into their accounts. Similarly, customers can withdraw funds from their accounts through online banking, either by transferring to an external account or using an ATM card tied to the account.

- Loan Applications: Many online banking platforms allow customers to apply for loans online. Customers can fill out loan applications, submit supporting documents electronically, and track the progress of their applications. This feature streamlines the loan application process and reduces the time and effort required.

- Account Management: Online banking enables customers to manage their accounts efficiently. They can update contact information, request account statements, view transaction history, and download account activity reports. Customers can also set up alerts and notifications for various account activities, helping them stay informed about their finances.

- Investment and Wealth Management: Some online banking platforms provide investment and wealth management services. Customers can buy and sell stocks, mutual funds, and other investment products online. They can also access investment research and monitor the performance of their investment portfolios.

- Card Services: Online banking allows customers to manage their debit and credit cards. They can view transaction details, check available credit limits, pay credit card bills, and report lost or stolen cards. Some online banking platforms also offer the ability to customize card transaction alerts for added security.

- Account Closure and Updates: Customers can request to close their accounts or make updates to their account information through online banking. This includes changing personal details, updating mailing addresses, and managing account beneficiary information.

These types of transactions offered by online banking provide customers with the convenience and flexibility to manage their finances efficiently. Online banking eliminates the need for physical visits to bank branches, offers real-time access to financial information, and simplifies the process of conducting various financial activities from anytime and anywhere.

Benefits of Online Banking

Online banking offers numerous benefits that make managing finances easier, more convenient, and more efficient for customers. With the rise of digital technologies and the increasing demand for remote access to financial services, online banking has become an essential tool for individuals and businesses alike. Let’s explore some of the key benefits of online banking:

- Convenience: One of the biggest advantages of online banking is the convenience it offers. Customers can access their accounts 24/7 from anywhere, eliminating the need to visit a physical branch during regular banking hours. They can perform various transactions, check account balances, and manage their finances at their own convenience.

- Accessibility: Online banking provides unparalleled accessibility. Customers can access their accounts from any device with an internet connection, including computers, smartphones, and tablets. This accessibility allows customers to manage their finances on-the-go, whether they are at home, at work, or traveling.

- Time-saving: Online banking saves time by eliminating the need to physically visit a bank branch for routine transactions. Customers can quickly and easily check their balances, transfer funds, pay bills, and perform various other banking activities without the need for lengthy paperwork or waiting in long lines.

- Cost-effective: Online banking can be cost-effective for both banks and customers. Banks can reduce overhead costs associated with maintaining physical branches, which can result in lower fees or better interest rates for customers. Moreover, customers can save money on transportation costs and avoid paying fees for certain services, such as printing paper statements, by utilizing online banking options.

- Enhanced Security: Online banking platforms enforce robust security measures to protect customers’ financial information. These measures often include secure login procedures, encryption protocols, and advanced fraud detection systems. Moreover, customers can set up additional security features, such as two-factor authentication, to further safeguard their accounts from unauthorized access.

- Financial Monitoring and Control: Online banking provides customers with real-time access to their financial information. They can easily monitor their account balances, keep track of transactions, and receive alerts for account activities. This level of visibility and control allows customers to detect any suspicious transactions or unauthorized access to their accounts promptly.

- Environmental Considerations: Online banking is eco-friendly and promotes sustainability. By reducing the need for paper statements, checks, and other physical documents, online banking helps minimize paper waste and the carbon footprint associated with traditional banking methods.

- Additional Services: Online banking often comes with additional services and features that enhance the overall banking experience. These services may include personal financial management tools, budgeting features, access to investment accounts, and integration with external payment platforms.

Overall, online banking offers a wide range of benefits that improve the banking experience for customers. The convenience, accessibility, and time-saving features of online banking, combined with enhanced security and additional services, make it a preferred choice for individuals and businesses to manage their finances effectively.

Security Measures in Online Banking

Security is a top priority in online banking to protect customers’ sensitive financial information from unauthorized access and fraudulent activities. Online banking platforms implement a variety of security measures to ensure the safety and integrity of customer data. These security measures provide customers with peace of mind when conducting financial transactions online. Let’s explore some of the key security measures in online banking:

- Secure Socket Layer (SSL) Encryption: Online banking platforms typically use SSL encryption to secure the communication between the customer’s device and the bank’s servers. SSL encryption ensures that data transmitted between the customer and the bank remains confidential and cannot be intercepted or tampered with by malicious actors.

- Strong User Authentication: Online banking platforms enforce strong user authentication measures to ensure that only authorized individuals can access the accounts. This may include the use of complex passwords, two-factor authentication, or biometric authentication such as fingerprint or facial recognition. These authentication methods enhance the security of customer accounts by adding an extra layer of protection against unauthorized access.

- Fraud Monitoring and Detection: Banks implement sophisticated fraud detection systems to monitor customer transactions and detect any suspicious activities. These systems use algorithms and machine learning to identify patterns and anomalies that may indicate fraudulent behavior, such as unauthorized transactions or unusual spending patterns. When suspicious activities are identified, customers are typically alerted and additional security measures are put in place to prevent further fraudulent transactions.

- Secure Login Procedures: Online banking platforms employ secure login procedures to prevent unauthorized individuals from accessing customer accounts. This may include multi-factor authentication, CAPTCHA requirements, or one-time passwords sent via SMS or email. These login procedures help ensure that only authorized individuals can access the accounts and protect customers from unauthorized access.

- Account Activity Alerts: Online banking platforms allow customers to set up alerts for specific account activities. These alerts notify customers of any unusual or suspicious transactions, such as large withdrawals or changes to contact information. By monitoring these alerts, customers can quickly identify and report any fraudulent activities to their bank.

- Secure Communication Channels: Online banking platforms often provide secure messaging systems for customers to communicate with their banks. These systems use encryption to protect the confidentiality of customer messages and ensure that sensitive information is not compromised during communication. Customers can use these secure channels to report issues, ask questions, or provide additional authentication when needed.

- Data Privacy and Compliance: Banks follow strict data privacy regulations and compliance standards to protect customer data. They implement security protocols to ensure that customer information is collected, stored, and processed securely. Banks also adhere to legal requirements, such as the General Data Protection Regulation (GDPR) and the Gramm-Leach-Bliley Act (GLBA), to safeguard customer privacy.

These security measures work together to provide a secure online banking environment for customers. By implementing strong encryption protocols, robust authentication methods, and sophisticated fraud detection systems, online banking platforms strive to protect customer data and maintain the integrity of financial transactions. It is important for customers to stay vigilant, regularly review their account activities, and report any suspicious transactions to their bank to ensure continued account security.

Challenges in Online Banking

While online banking offers numerous benefits and conveniences, it is not without its challenges. These challenges pose potential risks and concerns for both customers and financial institutions. It is important to be aware of these challenges to ensure a safe and secure online banking experience. Let’s explore some of the key challenges in online banking:

- Security Risks: One of the primary challenges in online banking is the constant battle against cybersecurity threats. Cybercriminals are constantly evolving their tactics to exploit vulnerabilities in online banking systems and gain unauthorized access to sensitive customer information. Financial institutions must stay one step ahead by implementing robust security measures and regularly updating their systems to address emerging threats.

- Phishing and Identity Theft: Phishing attacks, where fraudulent actors impersonate legitimate institutions to trick customers into revealing their personal information, pose a significant threat in online banking. These attacks can lead to identity theft, unauthorized access to accounts, and financial loss. Customers must be vigilant about phishing attempts and verify the authenticity of the websites or emails they interact with to prevent falling victim to such scams.

- Technical Issues: Online banking heavily relies on technology, and technical issues can occur from time to time. System glitches, website outages, or slow response times can disrupt the banking experience and cause frustration for customers. Financial institutions need to ensure robust infrastructure and constant monitoring to minimize technical issues and promptly address any technological obstacles that may arise.

- User Error: Human error is another challenge in online banking. Customers may inadvertently disclose sensitive information, use weak passwords, or fall victim to social engineering tactics. Proper education and awareness campaigns can help customers understand the best practices for online security, but there is always a risk of human error. Banks must continuously educate customers and provide guidance to minimize such risks.

- Privacy Concerns: Online banking involves the collection and processing of personal data, raising concerns about privacy. Customers may worry about the security and confidentiality of their financial information, as well as the collection and use of their personal data for marketing or other purposes. Financial institutions must be transparent about their data practices and comply with data privacy regulations to address these concerns.

- Technological Advancement: The rapid pace of technological advancements poses both opportunities and challenges for online banking. New technologies such as artificial intelligence and biometrics offer enhanced security and convenience, but they also introduce new risks and complexities. Financial institutions must continually evaluate and adapt to emerging technologies to stay ahead of potential vulnerabilities and ensure a seamless user experience.

- Cybercrime Regulations: As cybersecurity threats continue to evolve, governments and regulatory bodies introduce new regulations to mitigate risks and protect consumers. Adhering to these regulations can be challenging for financial institutions, as compliance requires substantial investments in cybersecurity infrastructure and resources. Meeting regulatory standards is crucial to maintain customer trust and avoid penalties.

Although there are challenges in online banking, financial institutions are committed to addressing these concerns through constant innovation, robust security measures, and customer education. By staying informed, following best practices for online security, and reporting any suspicious activities, customers can mitigate risks and enjoy the benefits of online banking safely.

Conclusion

Online banking has transformed the way we manage our finances, offering convenience, accessibility, and a wide range of features and services. It has become an integral part of modern banking, allowing customers to access and control their accounts anytime and anywhere. The benefits of online banking, such as convenience, time-saving, enhanced security, and additional services, have made it increasingly popular among individuals and businesses.

However, it is important to be aware of the challenges that come with online banking. Security risks, phishing attacks, technical issues, user error, privacy concerns, and the constant evolution of cybercrime pose ongoing challenges for both customers and financial institutions. By staying vigilant, following best practices for online security, and actively engaging with their banks, customers can mitigate these risks and ensure a safe online banking experience.

Financial institutions play a crucial role in addressing these challenges. They must consistently invest in robust security measures, stay updated on emerging risks, and implement stringent protocols to protect customer data and financial transactions. Educating customers about online security and privacy practices is equally essential to empower them with the knowledge and awareness needed to safeguard their accounts.

As technology continues to evolve, online banking will continue to adapt and offer more innovative features and services. The seamless integration of emerging technologies, such as biometrics and artificial intelligence, will further enhance security and improve the user experience in online banking. Financial institutions and customers must embrace these advancements while remaining vigilant and proactive in ensuring the security of their financial information.

In conclusion, online banking has revolutionized the way we manage our finances, offering convenience, accessibility, and a wide range of features and services. By understanding the benefits and challenges of online banking and by practicing good online security habits, individuals can confidently embrace this digital banking revolution.