Introduction

An e-wallet, also known as an electronic wallet or digital wallet, has become an increasingly popular and convenient method of payment in today’s digital age. With the rise of mobile technology and the evolution of online commerce, e-wallets offer a seamless and secure way to make transactions, manage finances, and store personal information. As traditional payment methods continue to be replaced by digital alternatives, understanding the concept of e-wallets and their limits is essential for both consumers and businesses.

So, what exactly is an e-wallet? Simply put, it is a virtual container that securely stores a user’s payment information, such as credit card details, bank account numbers, and even cryptocurrencies. This information is encrypted and can be accessed via a mobile application or website.

E-wallets work by establishing a secure connection between a user’s device, often a smartphone, and a payment gateway. When making a transaction, the e-wallet securely transfers the necessary payment details, allowing for a smooth and convenient payment process.

There are different types of e-wallets available, ranging from those provided by financial institutions to third-party platforms. Some e-wallets are single-purpose, designed for specific types of transactions, such as transit passes or gift cards. Others are multi-purpose, offering a wide range of capabilities, from making online purchases to sending money to friends or family.

The use of e-wallets brings several benefits to consumers. Firstly, they offer convenience, allowing users to make payments anytime, anywhere, with just a few taps on their smartphones. E-wallets also provide enhanced security, with encryption and authentication measures in place to protect sensitive information. Additionally, e-wallets often offer rewards programs and discounts, providing users with incentives to use them.

However, like any financial product, e-wallets have certain limits that users should be aware of. These limits can vary depending on factors such as the type of e-wallet, the user’s verification level, and local regulations. Understanding these limits is crucial to ensure a smooth and hassle-free transaction experience.

In the following sections, we will delve into the specifics of e-wallet limits, exploring factors that influence them, common types of limits, and how to increase them when needed.

What is an E-wallet?

An e-wallet, also known as an electronic wallet or digital wallet, is a digital version of a physical wallet that allows users to store and manage their payment information securely. It acts as a virtual container that holds various payment methods, such as credit cards, debit cards, bank account details, and even cryptocurrencies like Bitcoin.

With an e-wallet, users can make payments, send and receive money, and perform financial transactions seamlessly through a mobile application or website. The rise of e-commerce and mobile technology has made e-wallets increasingly popular, offering a convenient way to shop online and make in-person transactions without the need for physical cash or cards.

E-wallets work by securely storing users’ payment information and establishing a connection between the user’s device and a payment gateway. When making a purchase, the e-wallet securely transfers the necessary payment details, ensuring a smooth and secure transaction process.

There are different types of e-wallets available, catering to various needs and preferences. Some e-wallets are provided by financial institutions, such as banks or credit card companies, while others are offered by third-party payment platforms. These platforms often work across different devices, including smartphones, tablets, and computers, providing flexibility and accessibility to users.

One of the key advantages of using an e-wallet is the convenience it offers. Users can store multiple payment methods in one place, eliminating the need to carry physical cards or cash. This makes it easier to make purchases, especially when shopping online or in situations where carrying physical cards may be inconvenient.

Another benefit of e-wallets is enhanced security. E-wallets employ encryption and authentication measures to protect users’ payment information, reducing the risk of fraud or unauthorized access. Additionally, many e-wallet providers offer additional security features, such as biometric authentication or two-factor authentication, adding an extra layer of protection.

In summary, an e-wallet is a digital wallet that allows users to store and manage their payment information securely. It provides a convenient and secure way to make payments and perform financial transactions, eliminating the need for physical cash or cards. With the rise of e-commerce and mobile technology, e-wallets are becoming an integral part of the digital payment landscape.

How does an E-wallet work?

Understanding how an e-wallet works is essential to grasp the mechanics behind this digital payment solution. An e-wallet, also known as a digital wallet or electronic wallet, acts as a secure virtual container that stores and manages a user’s payment information, allowing for convenient and hassle-free transactions.

The functioning of an e-wallet can be broken down into a few key steps:

- Registration and Setup: The user typically downloads an e-wallet application onto their mobile device or accesses it through a website. They then proceed to create an account by providing the necessary personal and payment information. This information may include credit or debit card details, bank account information, or even digital currency addresses.

- Adding Payment Methods: Once the account is created, the user has the option to add multiple payment methods to their e-wallet. This could include linking credit or debit cards, bank accounts, or even virtual currencies like Bitcoin. The e-wallet securely stores this information and associates it with the user’s account.

- Making Transactions: When making a purchase or financial transaction, the user can select their desired payment method from the ones stored in their e-wallet. Depending on the transaction method, the e-wallet may prompt the user to confirm the payment using authentication measures such as a PIN code, biometrics, or a one-time password.

- Sending and Receiving Money: E-wallets also enable users to send and receive money from other e-wallet users or make peer-to-peer transfers. This functionality allows for convenient split payments, shared expenses, or quick money transfers between friends and family.

- Security Measures: E-wallets prioritize security to ensure the protection of users’ sensitive payment information. Encryption techniques are employed to safeguard data during transmission and storage. Additionally, many e-wallets offer additional security features, including biometric authentication, device linking, or two-factor authentication, to mitigate the risk of unauthorized access.

It’s important to note that each e-wallet service may have slightly different features and processes, depending on the provider and the specific application or platform. However, the underlying concept of securely storing and managing payment information remains consistent.

In summary, an e-wallet works by securely storing a user’s payment information, allowing them to make transactions, send and receive money, and manage their finances conveniently. By streamlining the payment process and providing enhanced security measures, e-wallets have become a popular choice for digital payments in today’s increasingly cashless world.

Types of E-wallets

E-wallets come in various forms, catering to different needs and preferences. Understanding the different types of e-wallets can help users choose the one that suits their requirements and aligns with their payment habits. Here are some of the most common types of e-wallets:

- Bank E-wallets: These e-wallets are provided by banks and are often linked to the user’s existing bank accounts. Users can access their e-wallets through dedicated banking applications or internet banking platforms. Bank e-wallets offer a wide range of functionalities, including making payments, transferring funds, and managing personal finances.

- Third-Party E-wallets: These e-wallets are offered by third-party payment service providers that are not affiliated with a specific bank. Examples include PayPal, Venmo, and Google Pay. Third-party e-wallets allow users to link various payment methods, make purchases, send money to other users, and even store loyalty cards.

- Mobile Network Operator E-wallets: These e-wallets are provided by mobile network operators and integrated with the user’s mobile subscription. Users can make payments, top-up mobile credit, and access exclusive promotions and discounts. Examples of mobile network operator e-wallets include M-Pesa and Airtel Money.

- Merchant E-wallets: Some businesses or merchants offer their own e-wallets to facilitate transactions within their ecosystem. These e-wallets are typically designed for use within a specific merchant’s network and may offer additional features such as loyalty rewards or exclusive discounts.

- Cryptocurrency E-wallets: As the popularity of cryptocurrencies like Bitcoin continues to grow, dedicated e-wallets for storing and managing digital currencies have emerged. These e-wallets provide a secure way to store and transact with cryptocurrencies, allowing users to send and receive digital assets easily.

- Transit E-wallets: Certain cities or regions have implemented e-wallet systems for public transportation. Users can load funds onto their e-wallets and use them to pay for fares on buses, trains, or other forms of public transport.

Each type of e-wallet has its own unique features and advantages, so users should consider their specific needs and the availability of e-wallet services in their region when choosing which e-wallet to use. Many e-wallets offer interoperability with multiple merchants and payment networks, providing users with flexibility and convenience.

It’s worth noting that the availability and functionality of e-wallets may vary across different countries and regions due to regulatory, technological, and market factors. Users should check the local offerings and capabilities of e-wallets when considering their options.

In summary, there are various types of e-wallets available to users, ranging from bank e-wallets and third-party providers to cryptocurrency wallets and transit e-wallets. Each type offers specific features and benefits, so users should choose the e-wallet that aligns with their needs and preferences.

Benefits of using an E-wallet

E-wallets offer numerous benefits that make them a popular choice for digital payments. As the world continues to shift towards a cashless society, understanding the advantages of using an e-wallet can help users make informed decisions about their payment methods. Here are some key benefits of using an e-wallet:

- Convenience: One of the main advantages of using an e-wallet is the convenience it offers. With an e-wallet, users can make payments anytime, anywhere, with just a few taps on their smartphones. Whether it’s making online purchases or paying for goods and services at physical stores, e-wallets streamline the payment process, eliminating the need to carry physical cash or search for credit cards.

- Security: E-wallets prioritize security to protect users’ payment information. They use encryption techniques to safeguard data during transmission and storage, reducing the risk of fraud or unauthorized access. Additionally, many e-wallets offer additional security features such as biometric authentication or two-factor authentication, providing an extra layer of protection.

- Rewards and Incentives: E-wallets often come with rewards programs and incentives, making them attractive to users. These rewards can range from cashback on purchases to loyalty points or exclusive discounts. By using an e-wallet for transactions, users can earn benefits and enjoy savings, enhancing their overall shopping experience.

- Expense Tracking and Budgeting: E-wallets often provide features that help users track their expenses and manage their budgets. With transaction history and spending analytics available at their fingertips, users can gain better insights into their spending habits and make informed financial decisions.

- International Transactions: For users who frequently make international transactions, e-wallets can be a convenient option. Some e-wallets offer the ability to hold and convert multiple currencies, allowing for seamless international payments without the need for currency exchange.

- Contactless Payments: E-wallets support contactless payment methods, enabling users to make transactions without physically handing over their cards. This feature is especially relevant in today’s world, where contactless payments have become more important due to health and safety concerns.

- Environmental Impact: By reducing the reliance on physical cash and paper receipts, e-wallets contribute to a more sustainable environment. They help to minimize the production and disposal of paper products, leading to reduced carbon footprint and waste.

The benefits of using an e-wallet extend beyond convenience and security. They provide users with opportunities to save money, track their expenses, and contribute to a more eco-friendly world. As e-wallet technology continues to advance, it is expected that more features and benefits will be offered to further enhance the user experience.

In summary, some benefits of using an e-wallet include convenience, enhanced security, reward programs, expense tracking, international transaction capabilities, contactless payments, and environmental sustainability. By embracing the use of e-wallets, users can enjoy a seamless and rewarding payment experience in the digital era.

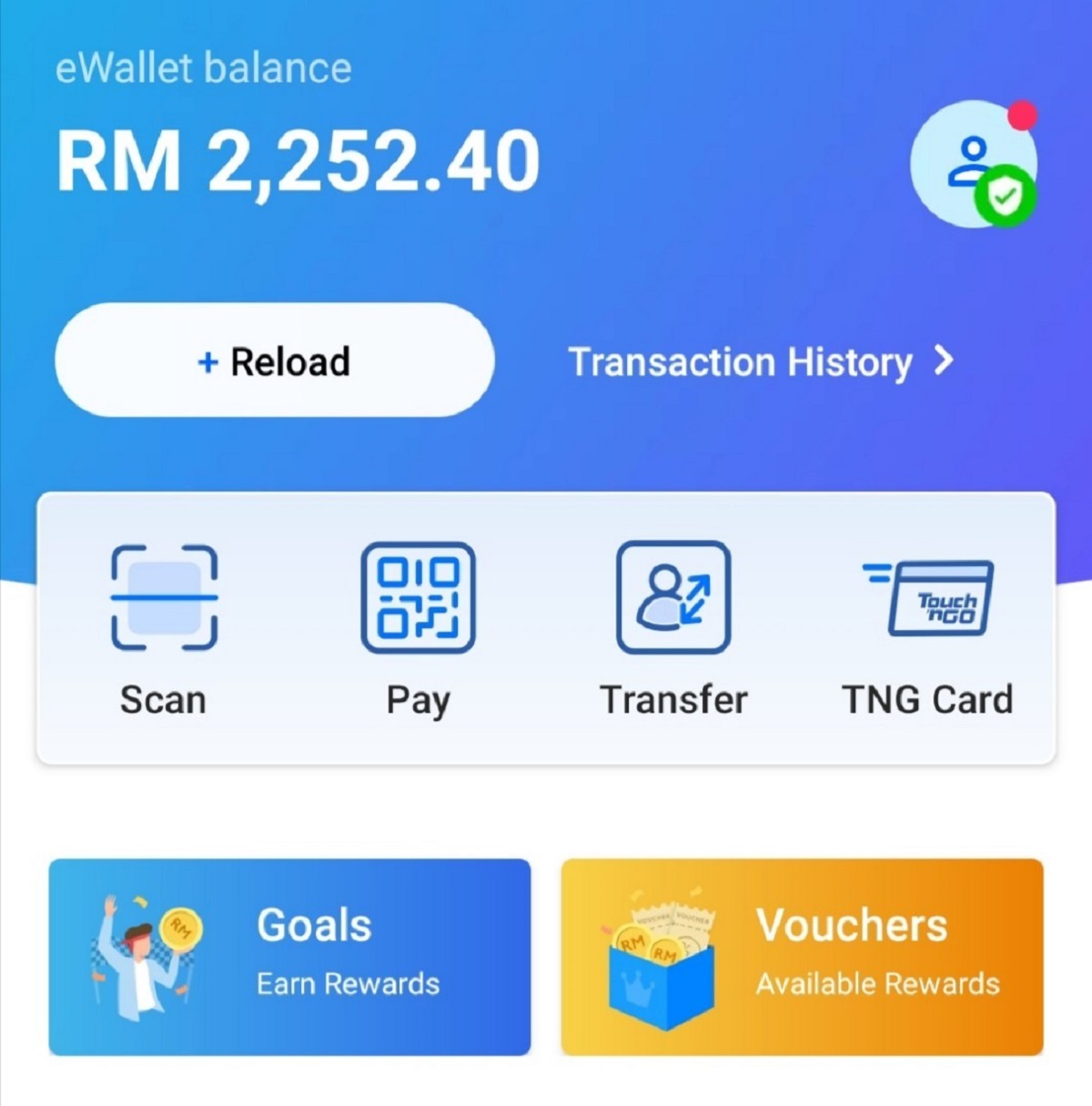

E-wallet Limits Explained

When using an e-wallet, it’s important to understand that there are certain limits in place that dictate the maximum and minimum amounts you can transact or store in your e-wallet account. These limits are set by the e-wallet provider and may vary depending on factors such as regulations, verification levels, and the type of e-wallet you are using.

There are generally two types of e-wallet limits:

- Transaction Limits: Transaction limits refer to the maximum amount of money you can send or receive in a single transaction. This limit is set to ensure security and prevent unauthorized or fraudulent transactions. Transaction limits may vary depending on the e-wallet provider, the account verification status, and local regulations. It’s important to note that transaction limits may also apply to specific types of transactions, such as those involving international transfers or high-value purchases.

- Account Limits: Account limits refer to the overall accumulated balance or maximum amount of funds that can be stored in your e-wallet account. Similar to transaction limits, account limits are in place to ensure security and compliance with regulations. The specific account limit will depend on the e-wallet provider and the type of account you have. Some e-wallets may offer different levels of account verification, such as basic, intermediate, or fully verified, with higher verification levels typically associated with higher account limits.

E-wallet limits play a crucial role in mitigating risks associated with fraud and money laundering. By imposing transaction and account limits, e-wallet providers can monitor and regulate the flow of money within their platforms, enhancing security and compliance.

It’s important to be aware of the specific limits imposed by your e-wallet provider. These limits can usually be found in the terms and conditions or the help section of the e-wallet application or website. By understanding the limits, you can ensure that your transactions fall within the allowable range, avoiding any disruptions or issues when using your e-wallet.

Additionally, it’s worth noting that e-wallet limits can sometimes be adjusted or increased. E-wallet providers may offer methods to increase limits, such as providing additional identification documents, linking a bank account, or upgrading to a higher account verification level. If you require higher transaction or account limits, it’s advisable to contact your e-wallet provider and inquire about the process for increasing your limits.

In summary, e-wallet limits refer to the maximum and minimum amounts set by e-wallet providers for transactions and account balances. These limits ensure security and compliance with regulations. Being aware of the specific limits and understanding how to potentially increase them can help you make the most of your e-wallet experience.

Factors influencing E-wallet limits

The limits imposed on e-wallet transactions and account balances can vary based on several factors. E-wallet providers take into consideration various elements when determining these limits, aiming to strike a balance between user convenience, security, and regulatory compliance. Here are some key factors that influence e-wallet limits:

- Regulations and Compliance: E-wallet limits are often influenced by local regulations and compliance requirements. Governments and financial authorities may impose certain restrictions on e-wallet providers to ensure transparency, prevent money laundering, and protect users. These regulations may differ from one country to another, resulting in varying limits applied by e-wallet providers in different jurisdictions.

- Account Verification: The level of account verification completed by a user can impact e-wallet limits. E-wallet providers typically offer different verification levels, such as basic, intermediate, or fully verified. Higher verification levels often come with increased limits on transactions and account balances. Users may need to provide additional identification documents or undergo a more rigorous verification process to unlock higher limits.

- Security Measures: E-wallet limits are designed to ensure the security of user funds. Providers consider factors such as authentication measures, encryption protocols, and risk management strategies when determining limits. The limits are set to prevent unauthorized access and mitigate the potential impact of fraudulent activities.

- User History and Behavior: E-wallet providers may consider a user’s transaction history and behavior when setting limits. Users who have a longer history of using the e-wallet service responsibly and have a positive track record may be granted higher limits. On the other hand, users with a history of suspicious or risky behavior may have lower limits imposed to minimize potential risks.

- Type of E-wallet: The type of e-wallet being used can also influence the limits. Different e-wallet categories, such as bank e-wallets, third-party e-wallets, or cryptocurrency wallets, may have varying limit structures. Some types of e-wallets may have higher limits due to stricter regulatory requirements or added security measures.

- Market Competition: Competition among e-wallet providers can influence the limits they set for their services. Providers may adjust their limits to remain competitive in the market and attract new users. This can lead to variations in limits between different providers, giving users the opportunity to choose a provider that offers limits that align with their needs.

It’s important for e-wallet users to be aware of these factors that influence e-wallet limits. Understanding the underlying considerations can help users manage their expectations and make informed decisions about their e-wallet usage.

If users require higher transaction or account limits, they should check with their e-wallet provider for any available options to increase their limits. This may involve providing additional documentation or fulfilling specific requirements outlined by the provider.

In summary, e-wallet limits are influenced by a variety of factors, including regulations, account verification, security measures, user history and behavior, the type of e-wallet, and market competition. Understanding these factors can help users better understand and navigate the limits set by their e-wallet providers.

Common E-wallet limits

E-wallets typically impose certain limits on transactions and account balances to ensure security, comply with regulations, and mitigate risks. The specific limits set by e-wallet providers can vary, but there are some common types of e-wallet limits that users may encounter. Understanding these limits can help users manage their e-wallet usage effectively. Here are some common e-wallet limits:

1. Transaction Limits: E-wallet providers often set limits on the maximum amount that can be sent or received in a single transaction. These limits can vary depending on the type of transaction, such as domestic or international transfers, online or in-store purchases. For example, a provider may set a transaction limit of $1,000 for online purchases and $500 for in-store transactions.

2. Daily, Weekly, and Monthly Limits: E-wallets may also enforce limits on the total amount that can be transacted within a specific time frame. These limits are typically set on a daily, weekly, or monthly basis. For instance, a user may have a daily transaction limit of $2,000, a weekly limit of $5,000, and a monthly limit of $10,000.

3. Account Balance Limits: E-wallets often have limits on the maximum account balance a user can maintain. This limit varies depending on factors such as the user’s verification level, regulations, and the e-wallet provider’s policies. For instance, a user may have a maximum account balance limit of $10,000 for a basic account, whereas a fully verified account may have a limit of $50,000.

4. Withdrawal Limits: Some e-wallets allow users to withdraw funds from their e-wallet accounts. These withdrawals may have separate limits, which can be daily, weekly, or monthly. For example, a user may have a daily withdrawal limit of $500 and a monthly withdrawal limit of $2,000.

5. Top-Up Limits: E-wallets often allow users to top up or load funds into their accounts. These top-up limits control the maximum amount that can be deposited into the e-wallet account. The limits can vary depending on factors such as the user’s verification level, source of funds, and regulatory requirements.

It’s important to note that these limits can be subject to change based on factors such as user activity, account history, or changes in regulations. Users should regularly review the terms and conditions of their e-wallet provider to stay updated on any limit changes.

Each e-wallet provider may have different limits, so it’s essential to familiarize yourself with the specific limits of the e-wallet you are using. If you require higher limits to suit your needs, you may need to undergo additional verification processes or contact your e-wallet provider for possible options to increase your limits.

In summary, common e-wallet limits include transaction limits, daily, weekly, and monthly limits, account balance limits, withdrawal limits, and top-up limits. These limits are in place to ensure security, regulatory compliance, and risk mitigation within the e-wallet ecosystem.

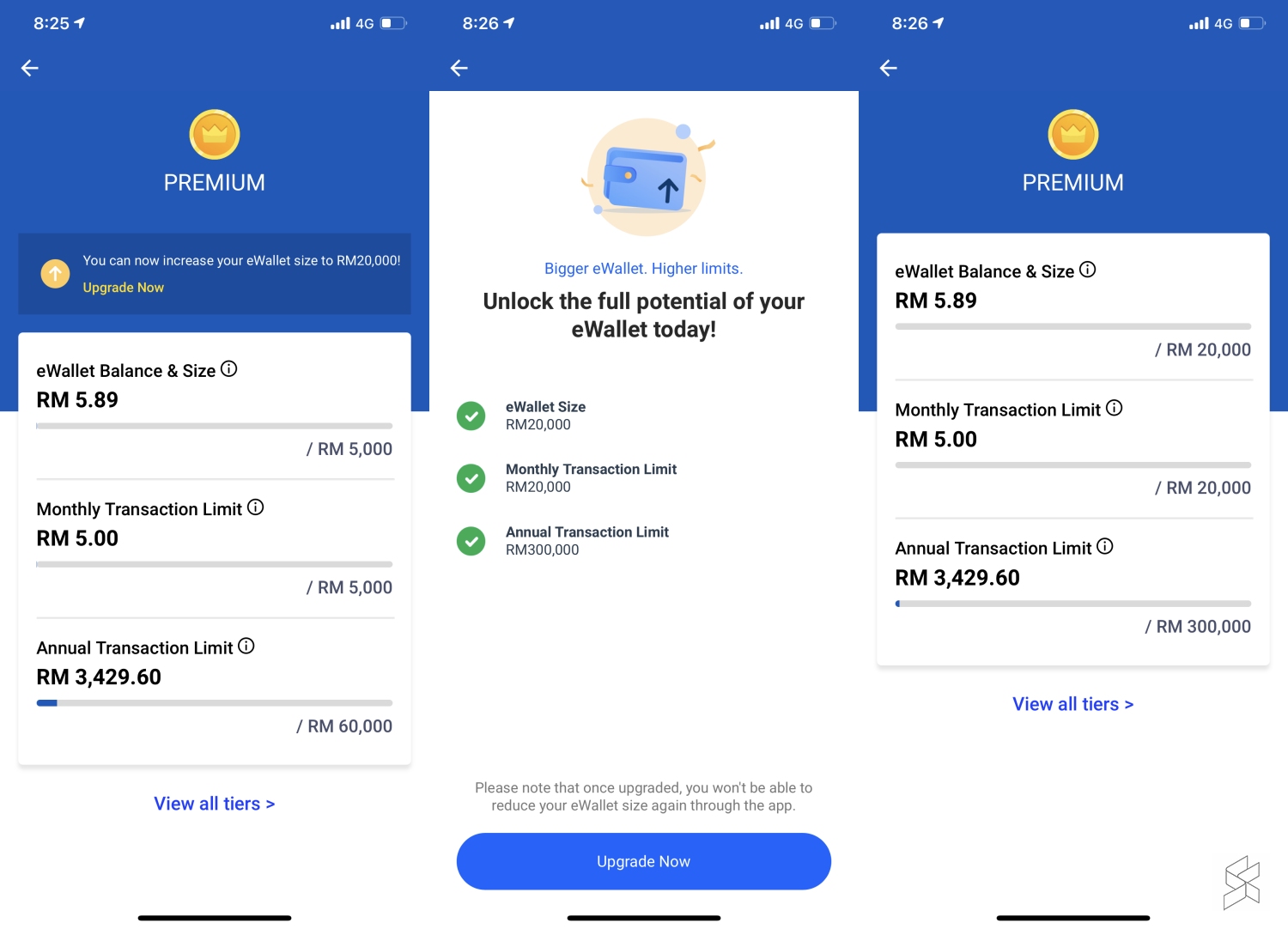

Increasing E-wallet limits

If you find that the limits imposed by your e-wallet provider are restrictive for your needs, you may have the option to increase your e-wallet limits. While the specific process may vary depending on the provider, here are some common methods that users can explore to increase their e-wallet limits:

- Complete Verification: E-wallet providers often offer different levels of account verification. By completing a higher level of verification, such as providing additional identification documents or linking a bank account, you may be able to increase your limits. This is because higher verification levels provide added security and compliance, giving e-wallet providers confidence in expanding user limits.

- Upgrade to Premium: Some e-wallet providers offer premium or upgraded account options that come with higher transaction and account limits. These premium accounts may require a monthly or annual fee, but they often come with additional features and benefits, such as priority customer support or access to exclusive rewards.

- Contact Customer Support: If you require higher limits and the above options are not available, it may be worth reaching out to your e-wallet provider’s customer support team. Explain your specific needs and inquire about the possibility of temporarily or permanently increasing your limits. They may require additional information or assess your account activity to determine if an increase in limits is warranted.

- Gradual Usage and Positive History: Building a positive track record with your e-wallet provider through consistent and responsible usage can also increase your chances of obtaining higher limits. By gradually increasing your transaction volume, maintaining a positive balance, and demonstrating responsible financial behavior, you may gain the trust of your e-wallet provider and be considered for limit increases over time.

- Consider Alternative E-wallet Providers: If your current e-wallet provider does not offer options to increase limits that meet your requirements, you can explore alternative e-wallet providers. Different providers may have different limit structures and verification processes, so switching to a new provider could provide higher limits that align with your needs.

Remember that the availability and suitability of these methods may vary depending on the e-wallet provider and local regulations. It’s recommended to review the specific guidelines and requirements provided by your e-wallet provider and follow their instructions to increase your limits.

Lastly, it’s important to consider that e-wallet providers impose limits to ensure security, regulatory compliance, and risk mitigation. While it may be possible to increase your limits, it’s crucial to keep your own financial needs and the overall security of your e-wallet in mind.

In summary, increasing e-wallet limits may involve completing higher levels of verification, upgrading to premium accounts, contacting customer support, building a positive usage history, or considering alternative e-wallet providers. Users should review their e-wallet provider’s guidelines and follow the appropriate steps to explore options for increasing their limits.

Conclusion

E-wallets have become an integral part of the modern digital payment landscape, offering users a convenient, secure, and efficient way to manage their finances. Understanding the concept of e-wallets, their functionality, limits, and ways to increase those limits can help users make the most of this digital payment solution.

We explored the different types of e-wallets available, such as bank e-wallets, third-party e-wallets, mobile network operator e-wallets, merchant e-wallets, and cryptocurrency e-wallets. Each type offers its own features and benefits, catering to specific needs and preferences.

Using an e-wallet provides several advantages, including convenience, enhanced security, rewards and incentives, expense tracking, and international transaction capabilities. E-wallets also have certain limits in place to ensure security, regulatory compliance, and risk mitigation. Users should be aware of factors that influence these limits, such as regulations, account verification, security measures, user history, the type of e-wallet used, and market competition.

While e-wallet limits are set to provide a secure and compliant environment, users may have the opportunity to increase these limits. Methods to increase e-wallet limits can involve completing higher levels of verification, upgrading to premium accounts, contacting customer support, building a positive usage history, or considering alternative e-wallet providers that offer higher limits.

In conclusion, e-wallets offer a practical solution for digital payments, delivering convenience, security, and a range of features to enhance financial management. By understanding e-wallet limits and exploring options to increase those limits, users can fully leverage the benefits of e-wallets and enjoy a seamless and flexible payment experience in the digital era.