Introduction

The emergence of blockchain technology has revolutionized various industries, especially the financial sector. At the heart of this groundbreaking technology are miners, who play a crucial role in maintaining the integrity and security of the blockchain network. In this article, we will explore the intricacies of miners in a blockchain and understand their significance in the underlying technology.

In a decentralized blockchain ecosystem, miners are responsible for validating and recording transactions. They ensure that each transaction is genuine, accurate, and adheres to the protocol’s rules. Through their computational power, miners compete to solve complex mathematical problems, ultimately adding new blocks to the blockchain.

The concept of mining in a blockchain draws inspiration from traditional mining practices. Similar to miners who dig deep into the Earth to extract valuable resources, blockchain miners rely on computational power to extract “digital gold” in the form of cryptocurrencies like Bitcoin or Ethereum. The mining process involves expending significant computational resources to solve cryptographic puzzles, which provides an added layer of security to the blockchain network.

Additionally, miners form an integral part of the consensus mechanism employed by most blockchains, known as Proof of Work (PoW). This consensus algorithm ensures the immutability and trustlessness of the blockchain by requiring miners to show proof of their computational efforts. This means that miners must expend computational power to find a solution to a mathematical problem, which can take a considerable amount of time and energy.

As a reward for their efforts, successful miners are incentivized with cryptocurrency rewards, typically in the form of newly minted coins and transaction fees. The mining process not only enables the creation of new units of digital currency but also facilitates the smooth functioning and security of the blockchain network.

What is a Miner?

In the context of blockchain technology, a miner is an individual or a group of individuals who use specialized computer hardware to validate and verify transactions on the blockchain network. Miners play a crucial role in maintaining the integrity and security of the blockchain by ensuring that all transactions are legitimate and adhering to the network’s rules and protocols.

Miners are essentially the backbone of the blockchain network, as they are responsible for processing and adding new transactions to the blockchain’s ledger. They achieve this by solving complex mathematical problems, known as cryptographic puzzles, using their computational power. These puzzles require miners to find a specific hash value that satisfies certain conditions, which can only be achieved through extensive computational efforts.

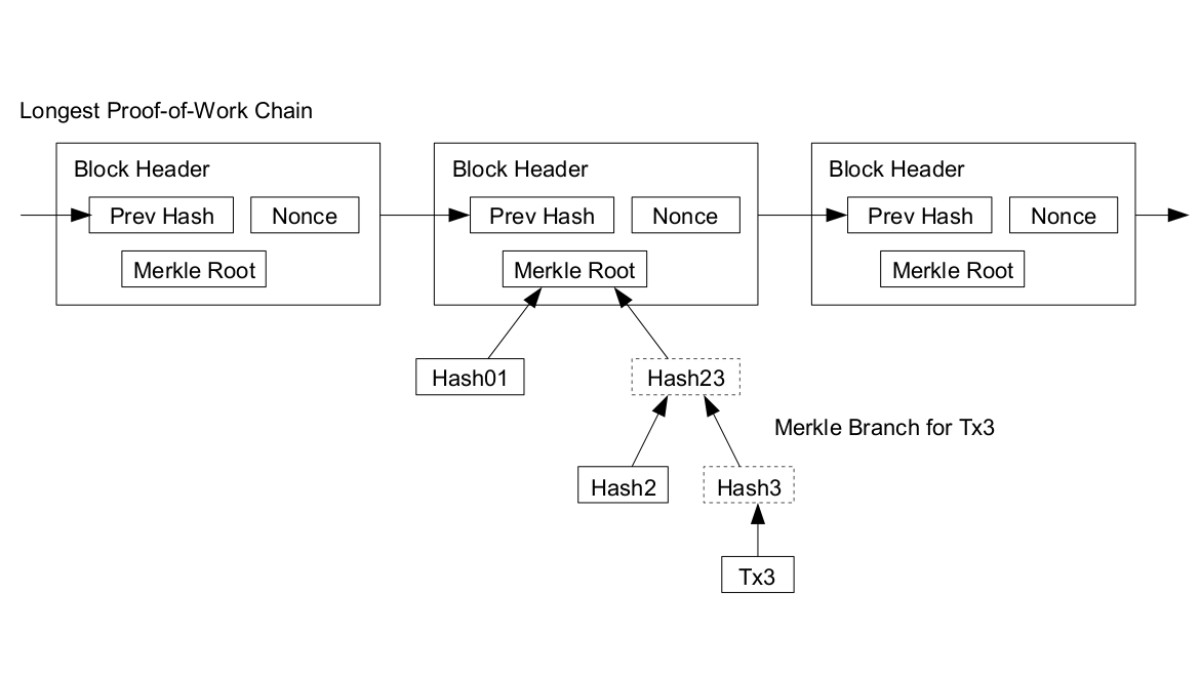

The mining process involves a series of steps. Firstly, miners collect unconfirmed transactions from the network and compile them into a block. This block contains a list of transactions along with a header that includes the previous block’s hash value and other metadata. Once the block is constructed, miners attempt to solve the cryptographic puzzle by repeatedly changing a nonce (a random value) in the block’s header and calculating its hash value. The goal is to find a hash value that meets the predetermined criteria set by the network’s difficulty level.

Mining is a highly competitive process, with miners competing against each other to find the correct nonce and solve the cryptographic puzzle. The first miner to successfully solve the puzzle and find the correct hash value gets to add the new block to the blockchain. This process requires significant computational power and energy consumption, as miners must perform numerous calculations until they find the solution.

Once the cryptographic puzzle is solved, the miner broadcasts the new block to the network, and other participants in the blockchain network verify the validity of the solution. If the majority of the network participants agree that the solution is valid, the block is added to the blockchain, and the miner receives a reward for their work. This reward typically consists of newly minted cryptocurrencies and transaction fees associated with the transactions included in the block.

In summary, miners are essential participants in a blockchain network. They are responsible for validating and verifying transactions, maintaining the security and integrity of the blockchain, and adding new blocks to the chain through the solving of complex mathematical puzzles. Their computational power and efforts ensure the smooth functioning of the blockchain ecosystem and enable the creation of new digital assets.

How does Mining Work?

Mining in a blockchain involves a complex process that relies on computational power and cryptographic algorithms. Let’s delve into the inner workings of mining and understand how this process facilitates the validation and addition of new blocks to the blockchain network.

The mining process begins with miners collecting a batch of unconfirmed transactions from the network. These transactions are then grouped together into a block, which serves as a container for storing the transactions until they are added to the blockchain. Each block also contains a unique identification number called a “hash” and the hash of the previous block, forming a chain of blocks.

To solve the cryptographic puzzle, miners utilize their computer hardware, specifically designed for mining operations. These hardware devices, called mining rigs, are equipped with high-performance processors, known as ASICs (Application-Specific Integrated Circuits), or powerful graphic cards (GPUs). The computational power of these devices allows miners to perform a large number of calculations in a short period.

The mining process involves repeatedly changing a small piece of data within the block, known as the “nonce,” and calculating the hash value of the block’s header. Miners aim to find a hash value that meets the specific criteria set by the network’s difficulty level. This criteria typically involves the hash value having a certain number of leading zeros.

Since the hash function used in the cryptographic puzzle is irreversible, miners have to rely on a trial-and-error approach. They change the nonce value and calculate the hash repeatedly until they find a hash value that meets the required criteria. This process is resource-intensive and requires substantial computational power and energy consumption.

The mining competition is fierce, with numerous miners in the network attempting to solve the puzzle simultaneously. The first miner to find the correct solution announces it to the network, validating the block. Other participants in the network then verify the solution and the validity of the block. If the network reaches a consensus that the solution is correct, the block is added to the blockchain, and the miner who found the solution is rewarded.

The complexity of the cryptographic puzzle is dynamically adjusted by the network to maintain a consistent block generation time. This adjustment ensures that new blocks are added to the blockchain at a predefined rate, regardless of changes in the computational power of the network.

Additionally, mining also contributes to the security of the blockchain network. As miners compete to find the correct solution, it becomes increasingly difficult for any individual or group to control the majority of computational power. This decentralization strengthens the security and immutability of the blockchain, making it highly resistant to fraudulent activities and attacks.

In summary, mining in a blockchain involves the use of specialized hardware and computational power to solve complex mathematical puzzles. Miners collect batches of unconfirmed transactions, construct new blocks, and compete to find the correct solution. Through this process, new blocks are added to the blockchain, and miners are rewarded for their efforts. Mining ensures the security, integrity, and decentralization of the blockchain network.

Proof of Work

Proof of Work (PoW) is a consensus mechanism used in many blockchain networks to ensure the security and immutability of the blockchain. It is a fundamental component of the mining process, providing a way to validate transactions and add new blocks to the blockchain. Let’s explore how Proof of Work works and its significance in maintaining the integrity of the blockchain network.

In a blockchain network that utilizes PoW, miners compete against each other to solve complex mathematical problems. These problems are designed to be computationally expensive, requiring a significant amount of computational power to find a solution. The goal is to demonstrate proof that a certain amount of computational work has been performed, hence the term “Proof of Work.”

The PoW algorithm sets a target difficulty level for miners to meet. This difficulty level determines the number of zeros required at the beginning of the hash value of the block. Miners must repeatedly change a nonce value within the block until they find a hash value that meets the difficulty criteria.

Once a miner finds a solution, they announce it to the network, along with the block and the specific nonce value used. Network nodes then verify the solution by independently running the same calculations. If the majority of nodes agree that the solution is valid, the block is added to the blockchain, and the miner is rewarded.

One of the main advantages of PoW is its ability to prevent double spending and malicious activities. Since each block is linked to the previous block through its hash value, tampering with any transaction within the chain would require recalculating the hashes for all subsequent blocks. This would require an enormous amount of computational power, making it virtually impossible to alter the blockchain’s history without detection.

Another benefit of PoW is its ability to create a decentralized and secure network. The competition among miners ensures that no single entity can gain control of the majority of computational power in the network. This makes the blockchain resistant to attacks and manipulation, as an attacker would need to overcome the combined computational power of all the honest miners in the network.

However, PoW also has some drawbacks. The computational power required for mining is energy-intensive, contributing to high energy consumption and environmental concerns. Additionally, the competitive nature of mining can lead to centralization, as larger and more powerful mining pools may dominate the network. This concentration of computational power can diminish the decentralization aspect of blockchain networks.

To address these concerns, alternative consensus mechanisms, such as Proof of Stake (PoS), have emerged. PoS aims to reduce energy consumption by selecting validators based on the stake they hold in the network, rather than their computational power. These alternative mechanisms provide different trade-offs in terms of scalability, energy efficiency, and security.

In summary, Proof of Work is a consensus mechanism utilized in blockchain networks to validate transactions and add new blocks to the blockchain. It involves miners competing to solve complex mathematical problems, providing proof of their computational efforts. PoW ensures the security, immutability, and decentralization of the blockchain network, although it also has associated energy consumption and centralization concerns.

Mining Rewards

In the world of blockchain, mining is not only essential for transaction validation and network security but also provides miners with lucrative rewards. These rewards act as an incentive for miners to dedicate their computational power and resources to the network. Let’s explore the various types of rewards that miners can receive for their mining efforts.

One of the primary rewards for miners is the creation of new digital assets or cryptocurrencies. In most blockchain networks, such as Bitcoin and Ethereum, miners are responsible for minting new coins into circulation. When a miner successfully mines a new block, they are rewarded with a predetermined number of newly minted coins. These coins are added to the miner’s wallet and can be traded or held as a form of investment.

In addition to newly minted coins, miners also receive transaction fees as part of their rewards. Whenever a user initiates a transaction on the blockchain network, they have the option to include a fee to incentivize miners to prioritize their transaction for inclusion in the block. These transaction fees are collected by the miner who successfully adds the block to the blockchain.

The transaction fees serve multiple purposes. They ensure that miners are compensated for the resources they dedicate to validating transactions and maintaining the blockchain network. Transaction fees also act as a mechanism to control the spamming of the network. By requiring users to pay a fee, it discourages malicious actors from flooding the network with unnecessary or low-value transactions.

The value of mining rewards can vary depending on the cryptocurrency and the network’s specific parameters. In the case of Bitcoin, for example, the mining rewards are halved approximately every four years through an event called the “Halvening.” This reduction in block rewards aims to maintain the scarcity of the cryptocurrency and control its inflation rate as the network matures.

Mining rewards are crucial for the sustainability and decentralization of blockchain networks. They incentivize miners to continuously dedicate their computational power, energy, and resources to secure the network. Without these rewards, the network would be vulnerable to attacks and would lack the necessary security and computational power to function effectively.

It’s important to note that mining rewards can be affected by several factors. The overall network difficulty, which adjusts based on the total computational power in the network, can impact the frequency with which miners successfully mine a block. Additionally, changes in the value of the cryptocurrency or the transaction volume on the network can influence the overall profitability of mining.

As blockchain technology continues to evolve, new consensus mechanisms and reward structures are being introduced. Proof of Stake (PoS) and other alternative mechanisms reward miners based on the amount of cryptocurrency they hold or stake in the network, rather than their computational power. These mechanisms aim to address the energy consumption concerns associated with Proof of Work and promote a more environmentally friendly approach to securing the blockchain.

In summary, mining rewards are a vital aspect of the blockchain ecosystem. They provide an incentive for miners to validate transactions and dedicate their computational power to secure the network. These rewards include newly minted coins and transaction fees, which can vary depending on the cryptocurrency and network parameters. Mining rewards ensure the sustainability and decentralization of the blockchain network while influencing miners’ profitability and the overall security of the network.

Mining Pools

Mining has evolved significantly since the early days of blockchain, and one of the developments that have emerged is the concept of mining pools. A mining pool is a collaborative effort where multiple miners combine their computational power to mine blocks and share the rewards. Let’s explore the concept of mining pools and understand their significance in the world of cryptocurrency mining.

In a mining pool, individual miners contribute their computing resources to a collective pool. This collective power enables the pool to solve complex mathematical problems and mine new blocks more efficiently and frequently. By pooling their resources, miners have a higher chance of successfully mining a block and receiving a share of the rewards based on their contribution.

The primary motivation behind joining a mining pool is to increase the chances of earning a steady stream of rewards. When mining individually, smaller miners face a higher level of uncertainty due to the significant computational power required to mine a block successfully. By combining their resources in a pool, miners can have more consistent and predictable earnings, even if it means sharing the rewards with other participants.

Mining pools usually employ a reward distribution system based on a proportional or a pay-per-share (PPS) model. In the proportional model, miners receive a share of the reward based on the computational power they contribute to the pool. For example, if a miner contributes 10% of the total hash rate of the pool, they will receive 10% of the rewards. The PPS model, on the other hand, guarantees miners a fixed payout for every share of work they contribute, regardless of whether the pool successfully mines a block or not.

Joining a mining pool also offers operational benefits. Miners no longer need to invest in expensive hardware and bear the maintenance costs associated with running a mining rig. Instead, they can connect their mining equipment to the pool’s infrastructure and start mining immediately. Mining pools also provide a more stable and reliable connection to the blockchain network, reducing the chances of downtime or connection issues.

However, mining pools are not without their drawbacks. By nature, mining pools centralize the control of computational power in a few entities, potentially leading to a concentration of power. If a single mining pool or a coalition of pools controls more than 50% of the network’s hash rate, they can potentially manipulate the blockchain’s operations or undermine its security. Therefore, it is crucial to have a diverse range of mining pools to maintain decentralization and security.

Additionally, mining pool participants often have to pay a fee to cover the pool’s operational costs and ensure its sustainability. These fees are typically deducted from the earned rewards before distribution. Depending on the pool’s reputation, features, and services provided, the fee structure can vary. Miners should carefully research and choose a mining pool that offers a fair fee structure and is trusted in the community.

In summary, mining pools provide a way for individual miners to combine their computational power and increase their chances of earning rewards in a more consistent and predictable manner. By pooling resources, miners can overcome the challenges of mining individually and benefit from a higher probability of successfully mining blocks. However, the concentration of computational power in a few entities and the payment of pool fees are factors to consider when deciding to join a mining pool. Overall, mining pools are a significant part of the mining ecosystem, fostering collaboration, and allowing more participants to engage in the mining process.

Significance of Miners in a Blockchain

Miners play a vital role in the functioning and security of blockchain networks. They contribute their computational power and resources to validate transactions, maintain the integrity of the blockchain, and ensure the overall security of the network. Let’s explore the significance of miners in a blockchain ecosystem and how their efforts contribute to the success of the technology.

One of the primary roles of miners is to validate and verify transactions on the blockchain network. By solving complex mathematical problems, miners confirm the authenticity and accuracy of each transaction, ensuring that only legitimate transactions are added to the blockchain. This validation process acts as a safeguard against fraudulent activities and maintains the integrity of the network.

Moreover, miners are responsible for the creation of new blocks in the blockchain. Through their computational efforts, they solve mathematical puzzles to add new blocks that contain verified transactions to the chain. This continuous block creation process ensures the smooth operation of the blockchain network, enabling participants to interact with the technology, perform transactions, and access decentralized applications (dApps).

In addition to transaction validation and block creation, miners provide the network with a critical layer of security. The decentralized nature of blockchain means that consensus among participants is essential to prevent malicious attacks and ensure the immutability of the ledger. Miners contribute their computational power to solve cryptographic puzzles and demonstrate proof of work, making it extremely difficult for individuals or groups to manipulate the blockchain’s history or tamper with transactions.

The computational power and electricity expended by miners act as a deterrent for malicious actors attempting to undermine the network. To successfully modify a transaction or introduce fraudulent activities, an attacker would need to control a significant portion of the network’s computational power, which becomes increasingly challenging as the network grows and more miners join.

Furthermore, miners play a significant role in maintaining the decentralization of the blockchain network. The distribution of mining power among various participants prevents any single entity from gaining control over the majority of computational resources. This decentralization of power ensures the democratic and transparent nature of blockchain, creating a level playing field for participants and reducing the risk of censorship or manipulation.

The contributions of miners also extend beyond their primary responsibilities. They help to propagate and transmit transactions across the network, ensuring that transactions reach all participants efficiently. By participating in the mining process, miners help to maintain and reinforce the network’s overall health and stability.

In summary, miners hold immense significance in blockchain networks. Their computational power, validation efforts, and contribution to block creation provide the foundation for the secure and decentralized nature of the technology. Miners ensure the authenticity and accuracy of transactions, maintain the integrity of the blockchain, and enhance the overall security of the network. Their role is instrumental in harnessing the full potential of blockchain technology and driving its adoption in various industries.

Conclusion

Miners play a crucial and multifaceted role in the world of blockchain technology. They validate transactions, add new blocks to the blockchain, ensure the security and integrity of the network, and contribute to its decentralization. Their computational power and efforts are essential in maintaining the smooth functioning and trustworthiness of blockchain networks.

Through the process of mining, which involves solving complex mathematical problems, miners validate the authenticity of transactions and add them to the blockchain. This validation process prevents fraudulent activities and ensures that only legitimate transactions are recorded on the decentralized ledger.

Miners also create new blocks, which enable the continuous operation of the blockchain network by facilitating transactions and the execution of decentralized applications. Their computational power and contributions to block creation are fundamental to the functioning of the technology.

The security provided by miners is a cornerstone of blockchain networks. Their involvement in solving cryptographic puzzles and demonstrating proof of work makes the blockchain highly resistant to attacks and tampering. The decentralized distribution of mining power ensures the democratic and transparent nature of the network, making it difficult for any single entity to manipulate the blockchain’s history.

Additionally, mining rewards incentivize miners to actively participate in the network. The creation of new digital assets and transaction fees provide a motivation for miners to contribute their computational power and resources, ensuring the sustainability and growth of the blockchain ecosystem.

While mining pools enable individual miners to collaborate and improve their chances of earning rewards, the concentration of mining power remains a concern. The blockchain community must strive to maintain a diverse range of mining pools to preserve decentralization and mitigate the risk of centralization.

In conclusion, miners are the backbone of blockchain technology. Their validation of transactions, creation of new blocks, provision of security, and contributions to decentralization are key to the success and adoption of blockchain networks. Their role is vital in ensuring the trust, transparency, and efficiency that blockchain technology promises, driving innovation and transforming industries across the globe.