Introduction

Blockchain technology has emerged as a groundbreaking innovation with the potential to revolutionize various industries, including payments. As society becomes increasingly digitalized, traditional payment systems face challenges such as high transaction fees, slow processing times, and the need for intermediaries. Blockchain offers a promising solution by providing a decentralized, secure, and transparent platform for conducting financial transactions.

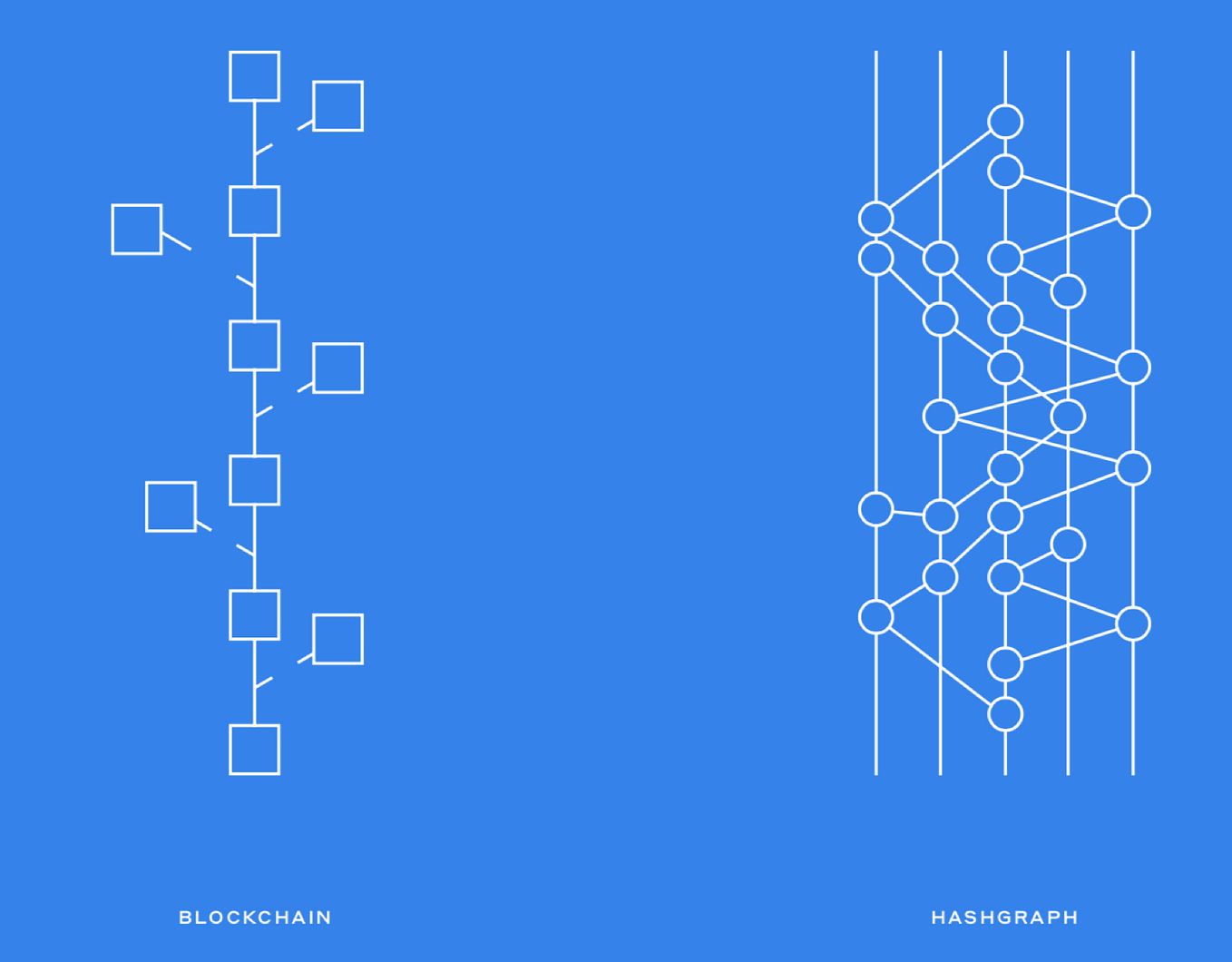

At its core, blockchain is a distributed ledger that records and verifies transactions across multiple computers or nodes. Each transaction is bundled into a block and linked to previous blocks, creating a chain of information. This decentralized structure eliminates the need for a central authority and provides inherent security through cryptography.

The benefits of using blockchain in payments go beyond just speed and cost efficiency. One of the key advantages is the inherent transparency it offers. Each transaction is recorded on the blockchain and can be viewed by all participants, ensuring trust and accountability.

Additionally, blockchain technology enables real-time settlement, eliminating the need for intermediaries and reducing the time and cost associated with traditional payment systems. This is particularly advantageous for cross-border transactions, which often suffer from lengthy processing times and high fees.

Furthermore, blockchain provides enhanced security by leveraging encryption algorithms to protect sensitive data. Transactions are immutable and tamper-proof, making them resistant to fraud and hacking attempts. This increased security and transparency can foster trust among users and help mitigate the risk of fraudulent activities.

Overall, the potential use cases of blockchain in payments are vast and continue to evolve. From remittances and peer-to-peer payments to supply chain financing and micropayments, blockchain technology has the potential to reshape the way we transact and interact financially.

In the following sections, we will explore the benefits of using blockchain in more detail, examine various use cases, and provide actionable steps for individuals and businesses to adopt this revolutionary technology in their payment processes.

What is blockchain and how does it work?

Blockchain is a decentralized and distributed ledger technology that allows for transparent and secure transactions. It operates on a peer-to-peer network where every participant, or node, has a copy of the entire ledger. This eliminates the need for a central authority to verify and authorize transactions.

At its core, a blockchain is composed of blocks, which contain records of transactions. Each block is linked to the previous block through a cryptographic hash function, creating a chain of information that is resistant to tampering and modification.

When a new transaction occurs, it is broadcasted to the network of nodes. These nodes verify the transaction using a consensus algorithm, such as Proof of Work (PoW) or Proof of Stake (PoS). Once the transaction is verified, it is bundled into a new block and added to the blockchain.

One of the key features of blockchain is its immutability. Once a block is added to the chain, it cannot be altered without the consensus of the majority of the network. This ensures that the transaction history remains transparent and tamper-proof.

Furthermore, blockchain utilizes cryptographic techniques to enhance security. Each transaction is encrypted and linked to its previous block, making it computationally impractical to alter or tamper with the data. Additionally, public and private key cryptography is used to authenticate transactions and ensure that only authorized parties can access and modify the data.

Blockchain technology also addresses the issue of trust through decentralization. Traditional payment systems rely on trusted intermediaries to facilitate transactions and validate the authenticity of parties involved. In contrast, blockchain removes the need for intermediaries by utilizing a network of nodes to collectively verify transactions. This decentralized structure increases trust among participants and reduces the risk of fraud and manipulation.

Overall, blockchain technology is transforming the way we conduct transactions by providing a secure, transparent, and efficient platform. Its decentralized nature and cryptographic techniques make it an ideal solution for various industries, particularly in the realm of payments.

Benefits of using blockchain in payments

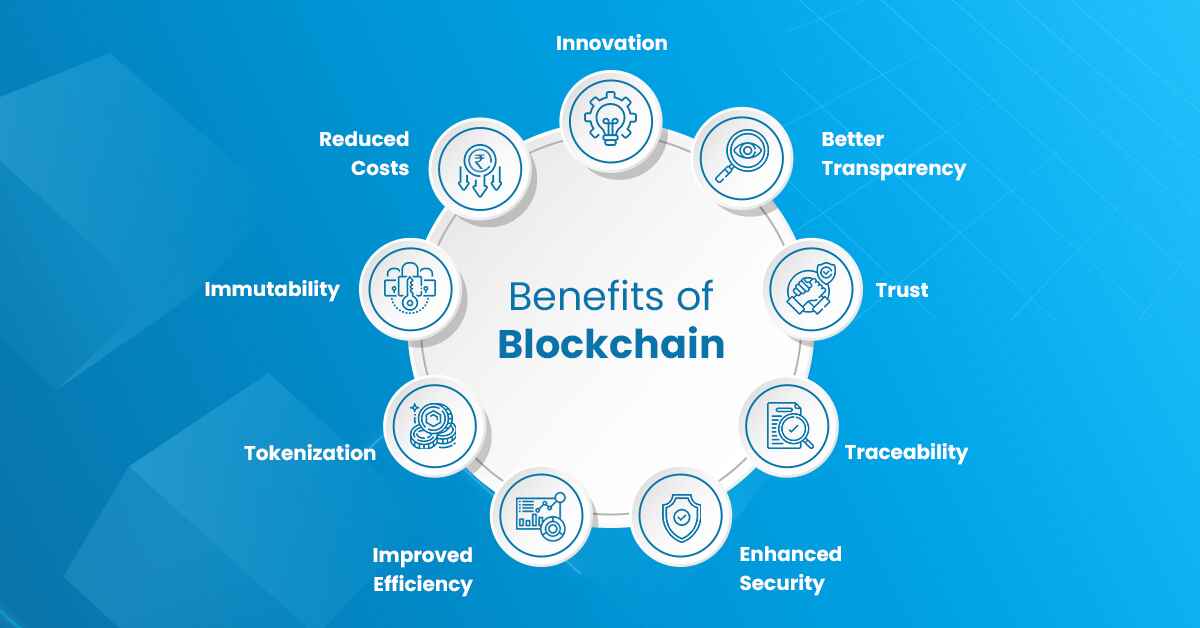

The use of blockchain technology in payments offers several significant benefits that can revolutionize the way we conduct financial transactions. Here are some key advantages:

- Transparency: Blockchain provides a transparent and auditable record of transactions. Every transaction is recorded on the blockchain and can be viewed by all participants. This transparency builds trust and accountability, as transactions can be easily verified and audited.

- Security: Blockchain technology enhances security in payments. Transactions are encrypted and linked to previous blocks, making it extremely difficult for fraudsters to alter or tamper with the data. The decentralized nature of the blockchain adds an extra layer of security, as there is no single point of failure.

- Efficiency: Traditional payment systems often involve multiple intermediaries, leading to delays and additional fees. With blockchain, transactions can be settled in real-time, removing the need for intermediaries and streamlining the payment process. This increased efficiency can significantly reduce costs and processing times.

- Cost savings: Blockchain eliminates the need for intermediaries, resulting in cost savings for businesses and individuals. By reducing transaction fees and eliminating the need for third-party payment processors, blockchain can make payments more affordable and accessible to a wider range of people.

- Global accessibility: Blockchain technology transcends geographic boundaries, allowing for seamless cross-border transactions. Traditional payment systems often face challenges when it comes to international transfers, such as high fees and slow processing times. Blockchain can facilitate faster, more cost-effective, and secure cross-border payments.

- Empowering financial inclusion: With blockchain, individuals who are currently unbanked or underbanked can have access to financial services. Blockchain-based payment systems can provide a secure and accessible platform for individuals in developing countries, enabling them to participate in the global economy.

These benefits highlight the potential of blockchain technology to transform payment systems and create more efficient, secure, and inclusive financial ecosystems. By leveraging blockchain in payments, businesses and individuals can streamline transactions, reduce costs, increase trust, and expand their reach on a global scale.

Use cases of blockchain in payments

Blockchain technology has a wide range of potential use cases in the payments industry. Here are some notable examples:

Remittances:

Blockchain can revolutionize the remittance industry by providing faster, cheaper, and more secure cross-border transactions. By eliminating the need for intermediaries and reducing fees, blockchain-based remittance platforms can enable immigrants and foreign workers to send money to their families in a more cost-effective and efficient manner.

Peer-to-peer payments:

Blockchain enables direct peer-to-peer payments without the need for traditional financial institutions. Individuals can send and receive payments directly, bypassing intermediaries and reducing transaction fees. This peer-to-peer payment system can empower individuals and businesses, particularly in underserved regions with limited access to traditional banking services.

Smart contracts:

Blockchain technology can facilitate automated payment processing through smart contracts. Smart contracts are self-executing agreements that automatically trigger transactions when predefined conditions are met. This technology streamlines payment processes, reduces administrative costs, and ensures that payments are executed securely and efficiently.

Cross-border payments:

Traditional cross-border payments often involve multiple intermediaries, resulting in high fees and slow processing times. Blockchain can simplify and accelerate cross-border payments by providing a decentralized platform for direct transactions. This eliminates the need for intermediaries, reduces costs, and increases the speed of settlement.

Supply chain financing:

Blockchain can enhance supply chain financing by providing a transparent and immutable record of transaction histories. Using blockchain, lenders can verify the authenticity of invoices and track the movement of goods throughout the supply chain. This enables faster and more secure financing for suppliers, reducing the risk of fraud and improving cash flow.

Micropayments:

Blockchain technology can facilitate microtransactions by reducing transaction costs and enabling seamless transfers of small amounts of value. This opens up new possibilities for monetizing digital content, such as news articles, music, and software, as blockchain-based micropayments allow users to pay small amounts for access to specific content without the need for a subscription or advertising-based revenue models.

These use cases are just a glimpse of the potential of blockchain technology in payments. As the technology continues to evolve and gain wider adoption, it is expected to unlock more innovative solutions and transform various aspects of the payments industry.

Steps to start using blockchain in payments

Integrating blockchain technology into payment processes requires careful planning and execution. Here are some important steps to consider when starting to use blockchain in payments:

Evaluate your payment needs:

Begin by assessing your specific payment requirements. Identify pain points and areas where blockchain can provide the most value. Determine if you need a public or private blockchain and consider factors such as transaction volume, speed, security, and scalability.

Choose a suitable blockchain platform:

Select a blockchain platform that aligns with your payment needs. Popular options include Bitcoin, Ethereum, and Ripple. Each platform has its own characteristics, so research and choose the one that best suits your requirements in terms of technology, consensus mechanism, ecosystem, and community support.

Develop or integrate a payment application:

Next, you’ll need to either develop a custom payment application on top of the chosen blockchain or integrate with existing blockchain-based payment solutions. This will involve working with developers or partnering with technology providers who specialize in blockchain development.

Ensure regulatory compliance:

Blockchain-based payment systems may be subject to regulatory requirements and compliance obligations, depending on your jurisdiction. Ensure that your solution adheres to relevant financial regulations, data protection laws, and anti-money laundering (AML) and Know Your Customer (KYC) requirements.

Establish partnerships and network connections:

Blockchain-based payment systems are most effective when they have a robust network of participants. Establish partnerships with banks, financial institutions, and other businesses to facilitate seamless interactions and expand your network. Collaborate with existing payment service providers to provide a bridge between blockchain and traditional payment systems.

Test and iterate:

Before launching a blockchain-based payment system, conduct thorough testing to ensure its functionality, security, and efficiency. Involve end-users and collect feedback to identify areas for improvement and iterate on the solution based on user needs and preferences.

Educate users and promote adoption:

Educate your users and stakeholders about the benefits of blockchain technology and its impact on payments. Promote adoption by demonstrating how blockchain-powered payments can be faster, cheaper, more secure, and transparent. Offer incentives, such as discounts or rewards, to encourage users to transact using the blockchain-based payment system.

By following these steps and carefully implementing blockchain technology in your payment processes, you can leverage the advantages of blockchain to enhance security, efficiency, and transparency in your payment ecosystem.

Challenges and considerations when using blockchain in payments

While blockchain technology offers numerous advantages for payments, there are also several challenges and considerations to keep in mind. Understanding these challenges is crucial to ensure successful implementation:

Scalability:

Blockchain scalability remains a significant challenge. As transaction volumes increase, public blockchains can become congested and experience slower transaction processing times. Addressing scalability requires implementing solutions such as off-chain transactions, sharding, or layer-two scaling solutions to handle a larger number of transactions efficiently.

Regulatory compliance:

The regulatory landscape surrounding blockchain is still evolving. Compliance with existing financial regulations, data protection laws, and anti-money laundering (AML) and Know Your Customer (KYC) requirements is essential. Adapting blockchain-based payment systems to meet regulatory standards while maintaining the technology’s core benefits can be complex and require ongoing monitoring and adjustment.

User education and adoption:

Blockchain technology is still relatively new to many users. Educating users about the benefits and functionality of blockchain-based payments is important for widespread adoption. Overcoming the learning curve and ensuring a seamless user experience will be critical to gaining acceptance and encouraging users to transition from traditional payment methods to blockchain-based solutions.

Interoperability:

Interoperability between different blockchain networks and traditional payment systems can be a challenge. Ensuring compatibility and seamless integration with existing infrastructure, such as legacy payment systems, is crucial to foster wide-scale adoption. Standardization efforts and collaboration between different blockchain platforms and payment service providers are necessary to overcome interoperability hurdles.

Security and privacy:

While blockchain technology is renowned for its security, vulnerabilities and privacy concerns can still arise. Implementing strong encryption, multi-factor authentication, and secure key management practices is crucial to protect against hacking and unauthorized access. Ensuring privacy for sensitive user data while maintaining the transparency benefits of blockchain requires careful consideration and appropriate privacy-enhancing measures.

Energy consumption:

Some blockchain networks, such as those that use the Proof of Work (PoW) consensus algorithm, consume significant amounts of energy. This can be a concern in terms of environmental impact and cost-efficiency. Exploring alternative consensus algorithms, such as Proof of Stake (PoS) or energy-efficient blockchain designs, can help mitigate these concerns and reduce the carbon footprint of blockchain-based payments.

Considering these challenges and taking appropriate measures to address them is vital to ensure the successful implementation and adoption of blockchain technology in the payments industry. By addressing these considerations, businesses and individuals can unlock the full potential of blockchain and harness its benefits while mitigating potential risks.

Conclusion

Blockchain technology holds immense potential to transform the way we conduct payments. By leveraging its decentralized, secure, and transparent nature, businesses and individuals can reap numerous benefits, including increased efficiency, reduced costs, enhanced security, and improved financial inclusion.

In this article, we explored the concept of blockchain and how it works. We delved into the benefits of using blockchain in payments, such as transparency, security, efficiency, cost savings, global accessibility, and financial empowerment. We also discussed various use cases, including remittances, peer-to-peer payments, smart contracts, cross-border transactions, supply chain financing, and micropayments.

To start using blockchain in payments, we outlined important steps, such as evaluating payment needs, selecting a suitable blockchain platform, developing or integrating a payment application, ensuring regulatory compliance, establishing partnerships and network connections, testing and iterating, and educating users to promote adoption.

We also highlighted the challenges and considerations associated with implementing blockchain in payments, including scalability, regulatory compliance, user education and adoption, interoperability, security and privacy, and energy consumption.

As blockchain continues to evolve and gain wider acceptance, it has the potential to reshape the payments landscape, ushering in a new era of efficiency, security, and financial empowerment. While there are challenges to overcome, the benefits outweigh the drawbacks, making blockchain a powerful tool to revolutionize the way we transact and interact financially.

By embracing blockchain technology and exploring its possibilities in payments, businesses and individuals can unlock new opportunities, streamline processes, and create a more inclusive and efficient financial ecosystem.