Introduction

Blockchain technology has emerged as a revolutionary solution with the potential to transform various industries and processes. Initially introduced as the underlying technology behind cryptocurrencies like Bitcoin, blockchain has evolved into a robust and versatile tool that offers numerous advantages in terms of security, transparency, efficiency, and more. This decentralized and distributed ledger system has gained widespread attention and adoption due to its ability to ensure trust, reduce intermediaries, and enhance overall data integrity.

By leveraging cryptographic algorithms and a network of computers (nodes), blockchain technology enables the secure storage and transfer of digital assets and information. Transactions recorded on a blockchain are permanent, tamper-proof, and transparent, making it an ideal solution for industries that rely heavily on secure and efficient data management.

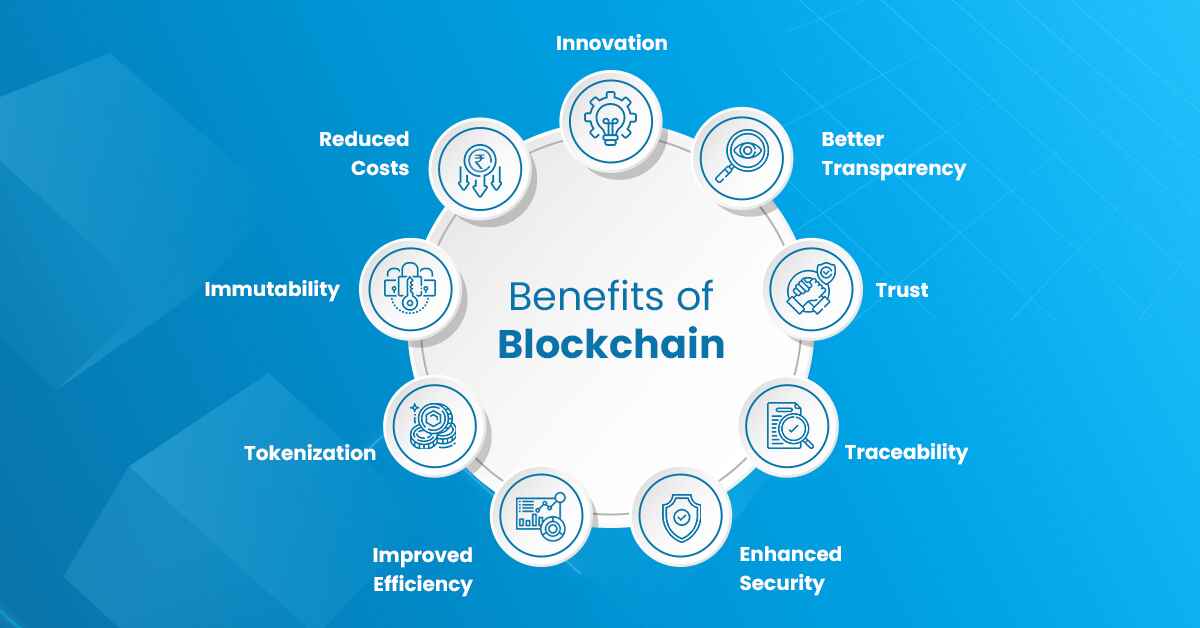

In this article, we will explore some of the key advantages of using blockchain technology across various sectors. From enhanced security and transparency to improved efficiency and cost reduction, blockchain has the potential to revolutionize the way we conduct business and exchange information.

Let’s dive deeper into the advantages of blockchain technology and how it is reshaping industries across the globe.

Increased Security

One of the primary advantages of using blockchain technology is the heightened level of security it offers. Traditional centralized systems store data in a single location, making them vulnerable to cyberattacks and unauthorized access. In contrast, blockchain utilizes a decentralized network of computers, eliminating the need for a central authority and significantly reducing the risk of a single point of failure.

The data stored on a blockchain is encrypted and distributed across multiple nodes, making it extremely difficult for hackers to compromise the system. Each transaction is verified by consensus among network participants, further ensuring the integrity of the data. Additionally, the use of cryptographic algorithms provides an added layer of security, making it nearly impossible to tamper with or alter the information recorded on the blockchain.

Furthermore, blockchain technology employs a transparent and auditable ledger system. Every transaction or data entry is recorded in a block and linked to the previous block, creating a chain of information. This immutability makes it easy to track and verify any changes or attempts at unauthorized access, providing a high level of accountability.

Industries such as financial services, healthcare, supply chain management, and government institutions can greatly benefit from the increased security offered by blockchain technology. For example, financial institutions can use blockchain to secure sensitive data like customer information, transaction records, and identity verification. Healthcare providers can store and share patient medical records securely while maintaining data privacy. By leveraging blockchain, supply chain stakeholders can ensure the authenticity and transparency of product information, preventing fraudulent activities.

With its robust security features and transparent nature, blockchain technology is revolutionizing data management and protection, providing organizations and individuals with peace of mind and confidence in the integrity of their digital assets.

Decentralization

Decentralization is a fundamental aspect of blockchain technology that sets it apart from traditional centralized systems. In a decentralized network, there is no single governing authority or central entity controlling the entire system. Instead, blockchain operates on a peer-to-peer network, where all participants have equal decision-making power.

This decentralized nature of blockchain brings several advantages. Firstly, it eliminates the need for intermediaries, such as banks or third-party payment processors, thereby reducing costs and increasing efficiency. Transactions can be conducted directly between parties, eliminating the delays, fees, and potential risks associated with intermediaries.

Furthermore, decentralization enhances the resilience and robustness of the blockchain network. Unlike centralized systems that are susceptible to a single point of failure, a decentralized blockchain network is distributed across a vast number of nodes. If one or more nodes fail or are compromised, the network can continue to function without interruption. This makes blockchain highly reliable and resistant to attacks.

Decentralization also enables greater transparency and trust. As every transaction is recorded on the blockchain and can be viewed by all network participants, it creates a transparent and auditable system. This transparency helps to foster trust between parties, as transactions and data entries cannot be easily manipulated or altered without consensus from the network. This is particularly crucial in industries where trust is paramount, such as supply chain management or public voting systems.

The decentralized nature of blockchain technology also empowers individuals by putting them in control of their own data and digital assets. Users have the ability to manage their private keys, granting them ownership and control over their information. This provides a level of autonomy and privacy that is often lacking in centralized systems where user data is stored and managed by third parties.

Overall, decentralization is a key advantage of blockchain technology as it empowers individuals, increases efficiency, enhances transparency, and provides a robust and secure framework for various applications across industries.

Improved Transparency

Blockchain technology brings unprecedented levels of transparency to various industries, revolutionizing the way data is recorded and shared. Unlike traditional systems where information is often siloed and controlled by a central authority, blockchain offers a transparent and auditable ledger system that is accessible to all network participants.

One of the key features of blockchain is its ability to provide a single source of truth. Every transaction recorded on the blockchain is time-stamped, verified, and stored permanently, creating an immutable record of events. This transparency ensures that all parties involved have access to the same information, eliminating any discrepancies or disputes that may arise due to data manipulation.

With blockchain, stakeholders can easily track and trace the origin and movement of assets, products, or funds. This is particularly valuable in industries such as supply chain management, where transparency and accountability are crucial. By recording every step of the supply chain on the blockchain, from raw material sourcing to manufacturing to distribution, organizations can ensure the authenticity, ethical sourcing, and quality of their products. Consumers, in turn, can verify the claims made by the manufacturer and make informed purchasing decisions.

Additionally, blockchain technology enables the creation of smart contracts, which are self-executing contracts with the terms and conditions directly written into code on the blockchain. Smart contracts automate the execution of agreements, ensuring transparency and removing the need for intermediaries. All parties involved can view the terms, conditions, and execution of the contract, eliminating the risk of fraud or manipulation.

Moreover, blockchain’s transparency extends to public accountability. In sectors like government and public administration, blockchain can facilitate transparent voting systems where every vote is recorded on the blockchain, ensuring a fair and tamper-proof electoral process. Similarly, blockchain-based identity management systems can provide individuals with control over their personal data, enabling them to choose what information to share and with whom.

Overall, improved transparency is a significant advantage of blockchain technology, enabling trust, accountability, and authenticity in various industries. By providing a verifiable and immutable record of transactions, blockchain enhances transparency and empowers stakeholders to make informed decisions based on accurate and trustworthy information.

Enhanced Efficiency and Cost Reduction

One of the most significant advantages of utilizing blockchain technology is the enhanced efficiency and cost reduction it offers across various industries. By streamlining processes and eliminating intermediaries, blockchain has the potential to revolutionize the way businesses operate.

Blockchain technology automates and digitizes processes, reducing the need for manual interventions and paperwork. For example, in supply chain management, blockchain can enable real-time tracking of goods, reducing the time and effort spent on manual inventory management. This automation not only saves time but also minimizes the risk of error and enhances overall efficiency.

Additionally, blockchain eliminates the need for intermediaries and reduces associated costs. In financial transactions, for instance, traditional methods involve multiple intermediaries, such as banks, payment processors, and clearinghouses, each charging fees. With blockchain, transactions can be conducted directly between parties, eliminating the need for these intermediaries and lowering costs.

Furthermore, blockchain technology can facilitate faster and more secure cross-border transactions. Traditional cross-border payments are often subjected to lengthy processing times, high fees, and currency conversion charges. Blockchain-based solutions, like cryptocurrencies, enable near-instantaneous and low-cost cross-border transactions, bypassing the need for multiple financial institutions to be involved in the process.

Moreover, the use of smart contracts on the blockchain can automate and streamline contract execution, reducing the time and resources required for contract management. Smart contracts automatically trigger actions based on predefined conditions, eliminating the need for manual intervention and potential human error. This automation improves efficiency, speeds up processes, and reduces costs associated with contract management.

Furthermore, blockchain’s decentralized nature eliminates the risk of a single point of failure, increasing system resilience and uptime. While centralized systems are vulnerable to network outages or hardware failures, blockchain networks function as a distributed network of nodes, ensuring continuous operation even in the face of individual node failures.

Overall, blockchain technology offers enhanced efficiency and cost reduction by automating processes, eliminating intermediaries, enabling faster cross-border transactions, and providing a robust and resilient infrastructure. By leveraging these advantages, businesses can streamline operations, reduce costs, and improve overall productivity.

Immutable and Tamper-Proof Records

One of the key advantages of utilizing blockchain technology is the ability to create immutable and tamper-proof records. Unlike traditional databases or record-keeping systems, blockchain provides a secure and transparent way to store and verify information.

When data is recorded on the blockchain, it becomes part of a series of blocks, each linked to the previous one through cryptographic hashes. This chain of blocks creates a permanent and unalterable record of transactions or data entries. Once a block is added to the blockchain, it is nearly impossible to modify or delete its contents without consensus from the entire network.

This immutability provides assurance and trust in the data stored on the blockchain, making it an ideal solution for critical information such as financial transactions, medical records, or legal contracts. The nature of blockchain ensures that records are tamper-proof, preventing fraudulent activities and unauthorized changes.

Additionally, the decentralized consensus mechanism employed by blockchain technology adds another layer of security and integrity to the records. Transactions or data entries recorded on the blockchain are validated and verified by multiple network participants, known as nodes, before being added to the chain. This consensus mechanism ensures that only valid and legitimate transactions are included, and any attempts to manipulate the data will be identified and rejected by the network.

The immutability and tamper-proof nature of blockchain records also have significant implications for auditing and compliance. With traditional systems, auditors often rely on sampling or trust the accuracy of the data provided by third parties. With blockchain, audit trails become more accurate and comprehensive. Every transaction is recorded, time-stamped, and linked to the previous block, creating a chronological and transparent record of events. This level of transparency and verifiability simplifies the auditing process, reduces the risk of fraud, and ensures compliance with regulations.

Industries such as finance, healthcare, supply chain management, and legal services greatly benefit from the immutability and tamper-proof nature of blockchain records. For example, in supply chain management, blockchain can be used to track the origin, authenticity, and quality of products, preventing counterfeit or substandard goods from entering the market. In healthcare, patient records stored on the blockchain ensure data integrity and privacy, while enabling trusted sharing among authorized healthcare providers.

In summary, leveraging blockchain technology for record-keeping ensures the immutability and tamper-proof nature of data, establishing trust, integrity, and accountability in various industries.

Elimination of Middlemen

One of the significant advantages that blockchain technology brings is the elimination of middlemen or intermediaries in various transactions and processes. Traditional centralized systems often require intermediaries such as banks, brokers, or lawyers to facilitate and validate transactions, adding complexity, cost, and potential delays to the process.

Blockchain technology allows peer-to-peer transactions, enabling parties to transact directly with each other without the need for intermediaries. By leveraging smart contracts, which are self-executing contracts with predefined terms and conditions, blockchain automates and enforces transactions based on the agreed-upon rules. This eliminates the need for intermediaries to oversee and validate the execution of contracts, reducing costs and speeding up the process.

This elimination of middlemen not only streamlines transactions but also reduces fees and commissions associated with their involvement. For example, in the financial industry, blockchain-based cryptocurrencies like Bitcoin enable direct peer-to-peer transactions without the need for banks or payment processors. This allows for lower transaction fees and faster settlement times, benefiting both consumers and businesses.

In supply chain management, blockchain eliminates the need for intermediaries in verifying the authenticity and provenance of products. By recording every step of the supply chain on the blockchain, including sourcing, manufacturing, distribution, and quality inspections, all participants can access and validate the information, ensuring transparency and trust. This reduces the reliance on intermediaries for verifying the integrity of products and mitigates the risks of counterfeit or substandard goods entering the market.

Additionally, in the real estate industry, blockchain can simplify the process of property ownership transfer by eliminating the need for title companies or lawyers to verify and record the transaction. By recording property ownership and transfers on the blockchain, the process becomes more efficient, transparent, and secure, reducing the time and cost involved in traditional property transactions.

The elimination of middlemen through blockchain technology also has implications for crowdfunding and fundraising. Blockchain-based crowdfunding platforms allow for direct peer-to-peer transactions between project creators and investors, bypassing traditional investment intermediaries. This opens up new opportunities for small businesses and startups to raise capital more efficiently and for investors to access a wider range of investment opportunities.

Overall, blockchain technology’s ability to facilitate peer-to-peer transactions through smart contracts enables the elimination of middlemen in various industries. This not only reduces costs and complexities but also improves efficiency and enhances the overall user experience.

Streamlined Supply Chain Management

Blockchain technology has the potential to revolutionize supply chain management by streamlining processes, increasing transparency, and enhancing efficiency. In traditional supply chains, the lack of transparency, data silos, and manual processes often lead to inefficiencies, delays, and increased costs. Blockchain offers a decentralized and transparent platform that can address these challenges and optimize supply chain operations.

By utilizing blockchain, supply chain stakeholders can track and verify the movement of goods from the point of origin to the final destination. Each transaction, such as the transfer of ownership, location, or condition of goods, can be recorded as a block on the blockchain. This creates an auditable and transparent supply chain where participants can trace the history and provenance of products, ensuring authenticity, quality, and compliance with regulations.

The transparency provided by blockchain technology also enables better visibility into inventory levels, production processes, and demand forecasting. Supply chain participants can access real-time data on inventory levels, allowing for accurate demand planning and optimization of production and logistics. This reduces the risk of overstocking or stockouts, minimizes waste, and optimizes inventory management, leading to cost savings and improved customer satisfaction.

Moreover, blockchain improves the efficiency of supply chain financing and payment processes. Traditional payment systems involve multiple intermediaries and lengthy settlement times. With blockchain-based smart contracts, payments can be automated and executed once predefined conditions are met, eliminating the need for intermediaries and reducing delays and costs associated with manual payment reconciliation.

Smart contracts on the blockchain can also automate compliance and quality assurance processes. By embedding predefined rules and conditions into the contract, compliance checks, certifications, and quality inspections can be automated and verified, reducing the need for manual interventions and ensuring compliance with regulatory standards and industry best practices.

In addition, blockchain technology allows for enhanced collaboration and trust among supply chain participants. With a shared and secure platform, all stakeholders, including suppliers, manufacturers, distributors, and customers, can access and contribute to the same data. This eliminates data discrepancies, improves communication, and enables more effective collaboration, leading to faster decision-making and improved overall supply chain performance.

Furthermore, blockchain can aid in the identification and mitigation of supply chain risks. By recording every transaction and data entry on the blockchain, potential issues and bottlenecks can be easily identified and addressed. This enables faster responses to disruptions, improves resilience, and enhances risk management in supply chains.

Overall, blockchain technology streamlines supply chain management by providing transparency, enhancing collaboration, automating processes, and improving overall efficiency. By optimizing supply chain operations, organizations can reduce costs, improve customer satisfaction, and gain a competitive edge in the market.

Enhanced Data Privacy and Control

Data privacy and control are crucial considerations in today’s digital world. Blockchain technology offers advanced solutions to enhance data privacy and give individuals more control over their personal information.

One of the key features of blockchain is its ability to provide secure and private transactions. When a transaction is recorded on the blockchain, it is encrypted and linked to the previous transactions through cryptographic hashes. This encryption ensures that only authorized participants can access the encrypted data, protecting sensitive information from unauthorized access.

Furthermore, blockchain allows individuals to have ownership and control over their personal data. Traditional systems often store individuals’ data in centralized databases controlled by third parties, leaving them vulnerable to data breaches or unauthorized sharing of personal information. With blockchain, users can store their data in a decentralized manner, where they hold the private keys that grant access to their information. This gives individuals greater control over who can access or use their data, reducing the risk of data abuse or privacy violations.

Blockchain-based identity management systems are emerging as a secure and efficient way to manage personal identities. By utilizing cryptographic techniques, individuals can prove their identity without revealing unnecessary personal information. This enhances privacy while enabling trusted interactions and transactions.

Moreover, blockchain provides a transparent and auditable system for data sharing. When data is shared on the blockchain, it can be accessed and verified by authorized parties, ensuring the accuracy and integrity of the shared information. This transparency builds trust among participants, promoting secure data exchanges while maintaining the privacy of sensitive information.

Blockchain technology also enables individuals to benefit from the use of their data. With traditional systems, individuals often have little control over how their data is used or monetized. Blockchain-based platforms can allow individuals to securely share their data with selected parties while retaining ownership and receiving compensation for its use. This empowers individuals to leverage their data as a valuable asset while maintaining control over its usage.

Additionally, blockchain’s immutability and tamper-proof nature provide an extra layer of security for sensitive information. Once data is recorded on the blockchain, it cannot be easily altered, ensuring the integrity and authenticity of the stored information. This makes blockchain an attractive solution for industries that deal with sensitive data, such as healthcare, finance, and legal services.

In summary, blockchain technology enhances data privacy and control by providing secure and private transactions, enabling individuals to own and control their personal data, offering transparency and auditability in data sharing, and facilitating secure and trusted exchanges of sensitive information. This empowers individuals to protect their privacy, retain ownership of their data, and participate in the digital economy on their own terms.

Simplified Cross-Border Payments

Cross-border payments have long been associated with challenges such as high fees, long transaction times, and currency exchange complexities. However, blockchain technology offers solutions that can simplify and streamline the process of cross-border payments.

Blockchain-based cryptocurrencies, such as Bitcoin and Ethereum, enable peer-to-peer transactions without the need for intermediaries like banks or payment processors. This eliminates the complexities and costs associated with traditional cross-border payment systems. With blockchain, individuals and businesses can send and receive payments directly, regardless of geographical boundaries.

One of the key advantages of blockchain technology in cross-border payments is the near-instantaneous transaction settlement. Traditional cross-border transactions often require multiple intermediaries, each adding their processing time. In contrast, blockchain transactions can be settled within minutes, reducing transaction times significantly.

Furthermore, blockchain eliminates the need for currency conversion during cross-border transactions. Cryptocurrencies operate on a universal medium of exchange, removing the need to convert currencies and reducing associated fees and exchange rate risks. This simplifies the payment process and makes it more cost-effective, especially when multiple currencies are involved.

Blockchain technology also enables greater transparency and traceability in cross-border payments. Every transaction recorded on the blockchain is time-stamped, verified, and publicly accessible, ensuring transparency and accountability. This transparency reduces the risk of fraud and increases trust between parties involved in the payment process.

Moreover, the use of smart contracts on the blockchain can automate and streamline cross-border payment workflows. Smart contracts can automatically execute payment instructions once predefined conditions are met, eliminating the need for manual interventions and reducing the chances of errors or delays. This automation improves efficiency and accelerates the settlement process.

For individuals and businesses in developing countries or regions with limited access to traditional banking services, blockchain-based cross-border payments provide an opportunity to participate in the global economy. By leveraging mobile devices and blockchain technology, individuals can access financial services and engage in cross-border transactions, enabling greater financial inclusion.

While there are still challenges to overcome, such as regulatory frameworks and scalability, blockchain technology has already demonstrated its potential in simplifying cross-border payments. As more organizations and financial institutions adopt blockchain-based solutions, the efficiency and accessibility of cross-border payments are expected to improve significantly, benefiting individuals, businesses, and the global economy at large.

Conclusion

Blockchain technology offers numerous advantages that have the potential to transform industries and processes across the globe. From increased security and decentralization to improved transparency and enhanced efficiency, the benefits of blockchain are far-reaching.

By leveraging blockchain technology, organizations can enhance the security of their data, ensuring that it remains tamper-proof and resistant to unauthorized access. The decentralized nature of blockchain eliminates the need for intermediaries, reducing costs, and increasing the efficiency of transactions. Blockchain’s transparent and auditable ledger system provides a single source of truth, enabling trust and accountability in various sectors.

Moreover, the immutability of records on the blockchain ensures that information cannot be easily altered or manipulated, strengthening the integrity of data. Blockchain technology empowers individuals by giving them greater control over their personal data and improving privacy. It simplifies cross-border payments, making them faster and more cost-effective, and streamlines supply chain management, optimizing processes and increasing supply chain visibility.

While blockchain technology is still maturing and faces challenges in terms of scalability, regulations, and adoption, its potential to revolutionize various industries is undeniable. As more organizations and individuals recognize the advantages of blockchain and embrace its implementation, the impact on the global economy and society as a whole will be significant.

In conclusion, blockchain technology holds immense promise in terms of security, transparency, efficiency, and control. As we embark on a future powered by blockchain, it is essential for businesses, policymakers, and individuals to embrace this transformative technology and explore its limitless possibilities.