Introduction

Blockchain technology has gained immense popularity in recent years, with its potential to revolutionize various industries through its decentralized and transparent nature. It is most commonly associated with cryptocurrencies like Bitcoin and Ethereum, but its applications extend far beyond the realm of digital currencies. However, like any emerging technology, blockchain also comes with its disadvantages and challenges.

In this article, we explore some of the key disadvantages of blockchain and discuss the implications they may have on its widespread adoption. While the advantages of blockchain are undeniable, it is essential to consider the limitations and risks associated with this technology as well.

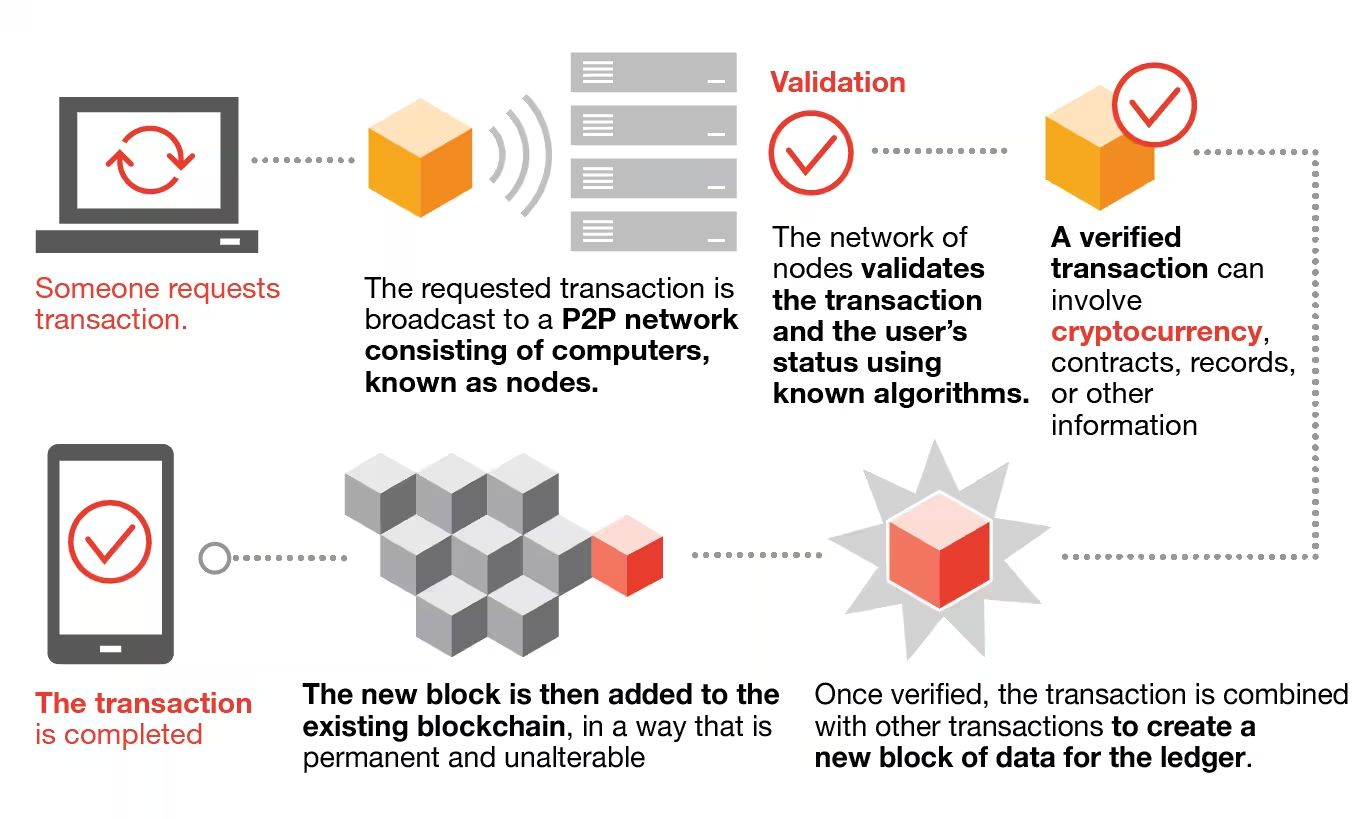

Blockchain operates on a distributed ledger system, where multiple computers or nodes participate in the verification and validation of transactions. While this decentralized nature offers numerous benefits, it also presents several challenges that need to be addressed.

In the following sections, we will explore the potential disadvantages of blockchain technology, including scalability issues, energy consumption, vulnerability to hacking, lack of regulation, slow transaction speeds, immutability of transactions, dependence on internet connectivity, and limited adoption.

By gaining an understanding of these challenges, we can explore possible solutions and advancements needed to overcome them. This will not only help in harnessing the benefits of blockchain technology but also in mitigating the risks associated with its implementation.

Now, let’s delve deeper into the specific disadvantages of blockchain and explore their implications in today’s digital landscape.

Lack of Scalability

One of the primary disadvantages of blockchain technology is its inherent scalability challenge. Blockchain networks are designed to store and validate every transaction across all nodes in the network. As the number of transactions increases, so does the size of the blockchain, resulting in potential performance issues.

Traditional financial networks can process thousands of transactions per second, while most blockchain networks are limited to a fraction of that capacity. Bitcoin, for example, can handle around 7 transactions per second, while Ethereum can process approximately 15 transactions per second. This limitation hampers the scalability of blockchain, especially when it comes to large-scale applications that demand high transaction volumes.

The scalability issue arises due to the consensus mechanism employed by blockchain networks. Most blockchains use a proof-of-work (PoW) or proof-of-stake (PoS) consensus algorithm, which requires significant computational resources and time to validate transactions and add them to the blockchain.

Efforts are being made to address this scalability challenge. Layer 2 solutions, such as the Lightning Network for Bitcoin and state channels for Ethereum, aim to offload a large number of transactions from the main chain, thereby increasing throughput. Additionally, various blockchain projects are exploring alternative consensus algorithms and sharding techniques to enhance scalability without compromising network security.

Despite these efforts, achieving significant scalability improvements remains an ongoing challenge for blockchain technology. As more industries and applications seek to leverage the potential of blockchain, scalability will continue to be a crucial concern that needs to be resolved.

Energy Consumption

Another significant disadvantage of blockchain technology is its high energy consumption. The process of validating and adding transactions to the blockchain requires substantial computational power, which in turn requires a significant amount of electricity.

Bitcoin, the most well-known blockchain network, relies on the proof-of-work (PoW) consensus algorithm, which involves “miners” competing to solve complex mathematical puzzles to add new blocks to the blockchain. This process requires intensive computational calculations, consuming substantial amounts of electricity. In fact, according to the Cambridge Centre for Alternative Finance, Bitcoin mining consumes more energy than some countries, such as Argentina and Sweden.

While some argue that the energy consumption is justified due to the security and decentralization provided by PoW, others see it as an unsustainable ecological impact. The high energy consumption of blockchain networks has drawn criticism for its carbon footprint and contribution to climate change.

Efforts are being made to address the energy consumption issue. Some blockchain networks are exploring alternative consensus algorithms, such as proof-of-stake (PoS), which requires validators to hold a certain amount of cryptocurrency instead of performing resource-intensive calculations. PoS can significantly reduce energy consumption while maintaining the security and decentralization of the blockchain.

Additionally, there are initiatives to incorporate renewable energy sources into the mining process to reduce the environmental impact. By using renewable energy to power blockchain networks, the carbon footprint can be minimized, making the technology more sustainable.

It is crucial for the blockchain community to continue exploring energy-efficient solutions to mitigate the environmental impact of this technology. Balancing the benefits and drawbacks of blockchain technology, including its energy consumption, is essential to pursue sustainable and responsible adoption.

Vulnerability to Hacking and Security Breaches

While blockchain technology is often touted for its security features, it is not immune to vulnerabilities and hacking. Although blockchain is designed to be tamper-resistant, it is still subject to certain security risks that need to be addressed.

One potential vulnerability is the 51% attack, where a malicious actor or group of actors gains control of more than 50% of the network’s computing power. This allows them to manipulate the blockchain’s consensus protocol and potentially double-spend or reverse transactions. However, pulling off a 51% attack in a well-established blockchain network like Bitcoin is highly unlikely due to the massive computational power required.

Another concern is the vulnerability of individual wallets and exchanges. While the blockchain itself may be secure, the weak point lies in the storage and management of private keys. If a user’s private key is compromised or a centralized exchange is hacked, it can lead to the loss of funds stored in the associated wallet. Over the years, there have been several high-profile hacking incidents and thefts from exchanges, highlighting the need for robust security measures.

Smart contract vulnerabilities are yet another area of concern. Smart contracts, which are self-executing contracts with predefined conditions, are deployed on blockchain networks like Ethereum. However, if not properly audited or written with secure coding practices, smart contracts can contain bugs or loopholes that can be exploited by hackers. Instances of such vulnerabilities have led to significant losses for individuals and organizations.

To address these security concerns, the blockchain community emphasizes the importance of rigorous security audits and code reviews. Regular vulnerability assessments and penetration testing can help identify and mitigate potential weaknesses. Additionally, implementing multi-factor authentication, cold storage for private keys, and secure hardware wallets can enhance user-level security.

As the adoption of blockchain technology grows, it is crucial for developers, businesses, and users to stay vigilant and implement robust security measures to safeguard against hacking and security breaches. Constant innovation and collaboration within the blockchain community are essential to ensure the continuous improvement of security practices.

Lack of Regulation and Legal Frameworks

One of the challenges faced by blockchain technology is the lack of adequate regulation and legal frameworks. As a relatively new and rapidly evolving technology, blockchain operates in a regulatory grey area in many jurisdictions.

The decentralized and borderless nature of blockchain poses challenges for traditional regulatory frameworks, which were primarily designed for centralized systems. This lack of clear regulations and guidelines can create uncertainty for businesses and individuals looking to adopt blockchain technology.

Several areas require regulatory clarity, such as cryptocurrencies, initial coin offerings (ICOs), security token offerings (STOs), and decentralized finance (DeFi) platforms. The legality and classification of these digital assets and activities vary greatly across different jurisdictions, leading to a lack of consistency and potential legal risks.

Furthermore, due to the anonymous and pseudonymous nature of blockchain, illegal activities such as money laundering, fraud, and illicit transactions can occur. The absence of clear regulations can hinder the ability of law enforcement agencies to effectively address these issues.

However, it is important to strike a balance between regulation and innovation. Excessive regulation can stifle the potential of blockchain technology and impede its development. Blockchain-friendly jurisdictions, such as Switzerland and Singapore, have taken proactive steps to provide a conducive regulatory environment for blockchain projects, promoting innovation while ensuring consumer protection and security.

Efforts are underway globally to establish regulatory frameworks and guidelines for blockchain and cryptocurrencies. Regulatory bodies are working towards providing clarity to ensure compliance and protect the interests of both businesses and consumers. Collaboration between the blockchain industry and regulators is crucial to strike the right balance and foster a favorable environment for blockchain adoption.

With time and continued dialogue between the blockchain community and regulators, it is expected that the legal landscape will evolve to accommodate and regulate the various aspects of blockchain technology, ensuring its responsible and secure integration into existing systems.

Slow Transaction Speeds

An inherent limitation of many blockchain networks is their slow transaction speeds. When compared to traditional electronic payment systems, blockchain transactions can take significantly longer to confirm and settle.

The verification and validation process in blockchain networks typically involves multiple nodes reaching a consensus on the validity of each transaction. This decentralized process, while ensuring transparency and security, also introduces time delays. Bitcoin, for example, has an average block time of around 10 minutes, meaning that transactions may take at least 10 minutes to be included in a block and confirmed.

The slow transaction speeds are particularly problematic when it comes to scalability and mass adoption. With increasing transaction volumes, the backlog of unconfirmed transactions can grow, leading to longer confirmation times and potential congestion on the network.

Several solutions are being explored to address this challenge. Layer 2 scaling solutions, such as the Lightning Network for Bitcoin and state channels for Ethereum, aim to enable off-chain transactions that can improve transaction speeds and reduce fees. By moving a significant portion of transactions off the main chain, these solutions can alleviate congestion and enhance the overall scalability of the network.

Furthermore, advancements in consensus algorithms, such as proof-of-stake (PoS) and delegated proof-of-stake (DPoS), offer the potential for faster transaction speeds. These consensus algorithms rely on a smaller group of validators or nodes to validate transactions, reducing the time required for reaching consensus.

However, it is essential to strike a balance between transaction speed and network security. Faster transaction speeds may come at the expense of decentralization and security, as compromising on consensus mechanisms can increase the vulnerability to attacks and manipulation.

As the blockchain ecosystem continues to evolve and mature, it is expected that advancements in technology, such as the implementation of scaling solutions and improved consensus algorithms, will help address the issue of slow transaction speeds. These developments will be crucial for facilitating the mainstream adoption of blockchain technology for real-time applications, such as payments and financial transactions.

Immutability and Irreversibility of Transactions

One of the fundamental characteristics of blockchain technology is the immutability and irreversibility of transactions. Once a transaction is recorded and confirmed on the blockchain, it becomes extremely difficult, if not impossible, to alter or reverse it.

While this feature provides transparency, security, and trust in the blockchain ecosystem, it can also present challenges in certain situations. In traditional centralized systems, transactions can be reversed, corrected, or disputed through intermediaries or legal mechanisms. However, on a blockchain, these options are limited due to the decentralized and trustless nature of the technology.

This immutability and irreversibility can be problematic in cases of accidental transactions, erroneous data entry, or fraudulent activities. If a user sends funds to the wrong address or falls victim to a scam, recovering those funds becomes challenging as there is no central authority to reverse the transaction.

Disputes and errors in smart contracts can also have significant consequences due to their immutability. Once a smart contract is deployed on the blockchain, it executes automatically according to predefined conditions, without the need for human intervention. If there’s a bug or a mistake in the code, it can lead to financial losses, and rectifying it requires a complex and time-consuming process.

To mitigate the risks associated with the immutability and irreversibility of transactions, it is crucial to exercise caution and due diligence. Double-checking transaction details, verifying smart contract code, and using reputable platforms and wallets can help minimize the chances of errors or fraudulent activities.

Furthermore, the blockchain community is exploring solutions to address these concerns. Some projects are developing decentralized dispute resolution mechanisms, where disputes can be settled through community consensus or specialized arbitration protocols. While these solutions are in their early stages, they have the potential to introduce a layer of flexibility to transactions on the blockchain without compromising its core principles.

It is important for users and businesses to be aware of the immutability and irreversibility of transactions on the blockchain. Proper education, scrutiny, and proactive measures can minimize the risks associated with this unique characteristic of blockchain technology.

Dependence on Internet Connectivity

One of the limitations of blockchain technology is its dependence on internet connectivity. Blockchain networks rely on a distributed network of nodes to validate and confirm transactions. These nodes communicate with each other through the internet, enabling the decentralized nature of blockchain. However, this reliance on internet connectivity poses challenges in certain scenarios.

In regions with limited or unreliable internet infrastructure, accessing and participating in blockchain networks can be difficult. Lack of internet connectivity can prevent individuals and businesses from utilizing blockchain-based services or participating in blockchain networks. This can create a digital divide, where certain populations or areas are unable to leverage the benefits of blockchain technology.

Furthermore, the dependence on internet connectivity introduces a potential point of failure. If there are disruptions in internet service or network failures, it can impact the availability and reliability of blockchain networks. Transactions may be delayed, and the network may experience temporary downtime, leading to inconvenience and potential financial losses.

However, it is worth mentioning that blockchain technology is evolving, and efforts are being made to address these challenges. Several projects are exploring offline transaction capabilities, where transactions can be conducted and validated even without a consistent internet connection. These solutions aim to enhance the accessibility of blockchain technology and reduce the reliance on continuous internet connectivity.

In addition, as internet infrastructure continues to improve globally, it is expected that the dependence on internet connectivity for blockchain operations will become less of a hindrance. The expansion of internet access, including initiatives such as satellite-based internet connectivity, can contribute to overcoming this limitation.

Nevertheless, it is important for users and businesses to be aware of the dependence on internet connectivity when engaging with blockchain networks. Having contingency plans, such as backup internet connections or utilizing offline transaction solutions when necessary, can help mitigate potential disruptions.

Overall, while dependence on internet connectivity is a current limitation of blockchain technology, ongoing developments and improvements in internet infrastructure and offline transaction capabilities aim to address this concern and make blockchain more accessible and robust.

Limited Adoption and Awareness

Despite the growing popularity and potential of blockchain technology, there still exists limited adoption and awareness in many industries and among the general public. Blockchain adoption faces several barriers that hinder its widespread implementation and understanding.

One of the primary challenges is the lack of awareness and understanding of blockchain technology. Many individuals and businesses are still unfamiliar with the concepts and applications of blockchain. This lack of knowledge can create skepticism and reluctance to explore and adopt blockchain solutions.

Additionally, the complexity of blockchain technology can be a barrier to adoption. Understanding the intricacies of distributed ledgers, consensus algorithms, and cryptographic protocols requires technical expertise, which may not be readily available to all. The perceived complexity can deter organizations from exploring the potential benefits of blockchain and hinder its integration into existing systems.

Moreover, the limited number of real-world use cases and successful implementations can impede widespread adoption. While blockchain has shown promise in certain areas like finance, supply chain, and healthcare, many industries have yet to fully embrace and utilize this technology. The lack of compelling case studies and success stories can make it challenging for businesses to justify the investment and effort required for blockchain integration.

Another hindrance to adoption is the interoperability challenge. Multiple blockchain platforms and protocols exist, each with its own set of features and limitations. Integrating different blockchains and ensuring seamless interaction between them can be complex. Lack of standardized protocols and interoperability frameworks can slow down the adoption of blockchain in multi-platform scenarios.

However, efforts are being made to address these challenges and promote wider adoption. Industry collaborations, blockchain consortia, and standardization initiatives are working towards creating frameworks and guidelines to facilitate seamless integration and interoperability. Education and awareness campaigns are also helping to spread understanding and knowledge about blockchain technology.

As more organizations recognize the potential benefits and understand the intricacies of blockchain technology, adoption is expected to increase. Continued research and development, along with proactive efforts to address adoption barriers, will play a crucial role in driving the widespread adoption of blockchain in various sectors.

In summary, limited adoption and awareness of blockchain technology persist due to factors such as lack of understanding, complexity, limited use cases, and interoperability challenges. Nonetheless, ongoing initiatives are working towards overcoming these barriers and promoting the broader adoption of blockchain, contributing to its continued growth and development.

Conclusion

Blockchain technology holds great promise in revolutionizing various industries with its decentralized and transparent nature. However, it is essential to recognize and address the disadvantages and challenges that come with its implementation.

The lack of scalability, high energy consumption, vulnerability to hacking, lack of regulation, slow transaction speeds, immutability of transactions, dependence on internet connectivity, and limited adoption are some of the key drawbacks associated with blockchain.

While these challenges exist, it is important to approach them as opportunities for improvement rather than insurmountable obstacles. The blockchain community is actively working on solutions to enhance scalability, improve energy efficiency, strengthen security, develop regulatory frameworks, increase transaction speeds, explore offline capabilities, and foster wider adoption.

As technology evolves, it is expected that these challenges will be gradually overcome. Blockchain will continue to mature, and its adoption will grow as businesses and individuals become more aware of its benefits and potential applications.

Ultimately, the success of blockchain technology relies on collaboration, education, innovation, and the development and implementation of robust solutions. By addressing the disadvantages and actively working towards solutions, we can harness the transformative power of blockchain while navigating the complexities and risks associated with its implementation.

As we move forward, it is crucial to strike a balance between innovation and regulation, ensuring that blockchain technology is harnessed responsibly and ethically. Through ongoing efforts and continuous improvement, blockchain has the potential to revolutionize industries, enhance transparency, streamline processes, and foster a more connected, secure, and efficient digital future.