What is blockchain?

Blockchain is a revolutionary technology that has gained significant attention in recent years. It is a decentralized and distributed digital ledger that records and verifies transactions across multiple computers or nodes. Unlike traditional centralized systems, blockchain operates on a peer-to-peer network, where each participant has access to the same information.

The basic concept of blockchain can be likened to a digital spreadsheet, where each block represents a record of transactions, and these blocks are linked together in a chain. The information within each block is encrypted and secured using cryptographic algorithms, ensuring the integrity and immutability of the data.

One of the fundamental characteristics of blockchain is its transparency. Every transaction recorded on the blockchain is visible to all participants, creating a transparent and accountable ecosystem. This transparency eliminates the need for intermediaries, such as banks or financial institutions, as the technology itself verifies and validates the transactions.

Moreover, blockchain operates on a consensus mechanism, which means that before a new transaction can be added to the blockchain, it must be agreed upon by the majority of participants in the network. This consensus mechanism ensures the security and reliability of the blockchain, making it highly resistant to fraud and manipulation.

Blockchain technology has the potential to disrupt various industries, not just in finance but also in supply chain management, healthcare, voting systems, and more. Its decentralized nature provides a level of trust and security that traditional systems often lack.

In summary, blockchain is a decentralized and transparent digital ledger that records and verifies transactions. It operates on a peer-to-peer network, ensuring transparency, security, and reliability. Its potential applications are vast and its impact on various industries is expected to be transformative.

What is cryptocurrency?

Cryptocurrency is a form of digital or virtual currency that utilizes cryptography for secure financial transactions, control the creation of new units, and verify the transfer of assets. Unlike traditional currencies issued by governments, cryptocurrency operates on decentralized networks, such as blockchain, which are not controlled by any central authority.

The most well-known cryptocurrency is Bitcoin, introduced in 2009 by an anonymous person or group of people using the pseudonym Satoshi Nakamoto. Since then, thousands of cryptocurrencies have been created, each with its unique features and purposes.

One of the main characteristics of cryptocurrency is its cryptographic security. Transactions made with cryptocurrency are secured through complex mathematical algorithms that protect the integrity and confidentiality of the data. This security ensures that transactions cannot be altered or tampered with and allows for a higher level of trust and transparency.

Another important aspect of cryptocurrency is its decentralized nature. Instead of relying on a central authority like a bank or government, cryptocurrency transactions are verified and recorded by multiple participants on a distributed network. The use of blockchain technology ensures that no single entity has complete control over the currency, making it resistant to censorship and manipulation.

Cryptocurrency also provides benefits such as fast and low-cost transactions, particularly for cross-border payments. Traditional banking systems often involve intermediaries and lengthy processes, resulting in higher fees and slower transaction times. Cryptocurrencies eliminate these barriers, allowing for efficient and cost-effective transactions.

Furthermore, cryptocurrencies offer new opportunities for investment and financial inclusion. With the ability to buy, sell, and trade cryptocurrencies on various cryptocurrency exchanges, individuals can engage in a global market without significant barriers to entry.

In summary, cryptocurrency is a form of digital currency that utilizes cryptography and operates on decentralized networks. It provides secure transactions, decentralization, and financial inclusion. The rapid growth and adoption of cryptocurrencies indicate their potential to reshape the future of finance and revolutionize various industries.

How does blockchain work?

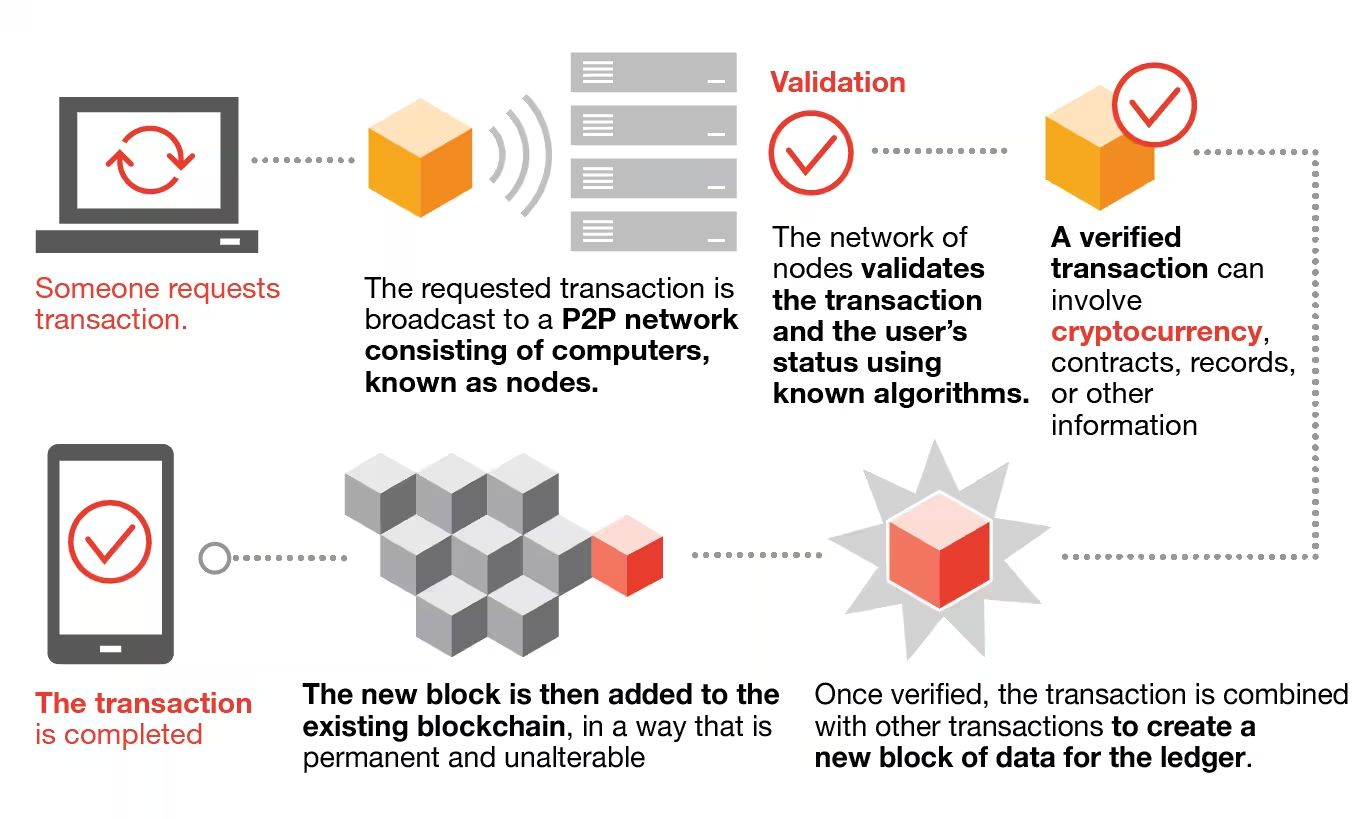

Blockchain technology operates on a decentralized and distributed network of computers or nodes. It works by creating a digital ledger that records and verifies transactions in a secure and transparent manner.

At its core, a blockchain consists of a series of blocks, each containing a set of transactions. The blocks are linked to each other using cryptographic hashes, creating a chain of blocks. This linkage ensures the immutability and integrity of the data within the blockchain.

When a new transaction occurs, it is grouped with other pending transactions and added to a block. Before the block can be added to the blockchain, it must go through a validation process called mining. Miners, specialized participants in the network, use powerful computers to solve complex mathematical puzzles, which requires a significant amount of computational power.

Once a miner solves the puzzle, they broadcast the solution to the network, allowing other miners to verify the correctness of the solution. This process, known as consensus, ensures that all participants in the network agree on the validity of the block and its transactions.

Once a block is verified, it is added to the blockchain, and the next block is created to continue the chain. The addition of a new block also requires referencing the previous block’s hash, further securing the integrity of the entire blockchain.

Each participant in the blockchain network has a copy of the entire ledger, making it decentralized and resistant to tampering. Any attempt to alter a previous block would require modifying all subsequent blocks, requiring an impractical amount of computational power and consensus from the majority of participants.

The transparency of the blockchain allows participants to view and audit all the transactions recorded on the network. However, the privacy of these transactions is maintained through the use of cryptographic techniques, ensuring that the identities of the participants remain anonymous while still providing the necessary security measures.

In summary, blockchain technology works by creating a decentralized and transparent digital ledger. It records and verifies transactions through a consensus mechanism, securing the data in blocks connected in a chain. This innovative technology offers security, transparency, and tamper resistance, presenting numerous opportunities across various industries.

How is blockchain related to cryptocurrency?

Blockchain and cryptocurrency are closely intertwined, with blockchain serving as the underlying technology that powers cryptocurrencies. While blockchain has a wide range of applications beyond cryptocurrencies, it is the foundation upon which cryptocurrencies like Bitcoin and Ethereum operate.

Blockchain technology enables the decentralized and secure nature of cryptocurrencies. Each transaction made with a cryptocurrency is recorded on a block within the blockchain. These blocks are linked together in a chain, creating a transparent and immutable ledger of all transactions.

One of the key benefits of blockchain in relation to cryptocurrencies is its ability to ensure trust and eliminate the need for intermediaries. Traditional financial transactions often rely on third-party institutions, such as banks, to verify and facilitate transactions. With blockchain, transactions can be verified and recorded by a decentralized network of participants, eliminating the need for intermediaries and reducing associated fees and delays.

Blockchain also enhances the security of cryptocurrencies. Each transaction made with a cryptocurrency is encrypted and linked to the previous transaction in the blockchain. This cryptographic security ensures the integrity and immutability of the transaction history, making it extremely difficult for fraudulent activities to take place.

Additionally, blockchain technology allows for the creation and management of new cryptocurrencies. Through the use of smart contracts, developers can build and deploy their own cryptocurrencies on blockchain platforms such as Ethereum. These cryptocurrencies can have various functionalities and use cases, ranging from decentralized finance (DeFi) to supply chain management.

The blockchain also plays a crucial role in ensuring the scarcity and value of cryptocurrencies. Through mechanisms such as proof-of-work or proof-of-stake, blockchain networks ensure that new units of cryptocurrencies are introduced according to predefined rules. This limited supply, combined with the decentralized nature of cryptocurrencies, contributes to their value and potential as stores of wealth.

Furthermore, blockchain technology enables the traceability and transparency of transactions within the cryptocurrency ecosystem. As every transaction is recorded on the blockchain, users can trace the flow of funds and verify the authenticity of transactions. This transparency can assist in addressing issues such as money laundering and fraud, making cryptocurrencies a more trusted and accountable form of digital currency.

In summary, blockchain technology is the underlying technology that powers cryptocurrencies. It enables the decentralized and secure nature of cryptocurrencies, eliminates the need for intermediaries, enhances security, facilitates the creation of new cryptocurrencies, and provides traceability and transparency within the cryptocurrency ecosystem.

Security in blockchain and cryptocurrency

Security is a crucial aspect of both blockchain technology and cryptocurrencies. The decentralized and cryptographic nature of blockchain provides a foundation for robust security measures, ensuring the integrity and protection of digital assets.

One key security feature of blockchain is immutability. Once a transaction is recorded on the blockchain, it becomes virtually impossible to alter or tamper with. Each block in the chain contains a unique cryptographic hash that is calculated based on the previous block’s data. Any modification made to a block would require recalculating the hash for that block and all subsequent blocks, which would be computationally infeasible. As a result, the blockchain provides a tamper-resistant ledger with a high level of data integrity.

Cryptocurrency transactions further enhance security through the use of cryptographic algorithms. Each transaction is securely encrypted, ensuring that the sender’s information, recipient’s address, and transaction details are protected from unauthorized access. This cryptographic security provides confidentiality and prevents fraud, making it extremely difficult for malicious actors to manipulate or forge transaction data.

Another important aspect of security in blockchain and cryptocurrency is the consensus mechanism. Consensus mechanisms, such as proof-of-work (PoW) or proof-of-stake (PoS), ensure that transactions are verified and added to the blockchain by a majority of participants in the network. By requiring a large number of participants to agree on the validity of transactions, these mechanisms make it difficult for a single entity to manipulate the blockchain. This decentralized consensus further strengthens the security and trustworthiness of the network.

Additionally, the use of public and private key cryptography provides strong authentication and authorization in the cryptocurrency ecosystem. Users hold a pair of cryptographic keys: a public key for communication and a private key for transaction signing. The private key is securely stored by the user, allowing them to authenticate and authorize transactions securely. This cryptographic key system ensures that only the rightful owner of the cryptocurrency can access and transfer their digital assets.

However, it is important to note that while blockchain and cryptocurrencies offer strong security measures, they are not without vulnerabilities. One potential vulnerability is the risk of private key compromise. If a user’s private key is stolen or accessed by unauthorized parties, it can result in the loss of their cryptocurrency holdings. Therefore, it is crucial for users to follow best practices for securing their private keys, such as using hardware wallets or secure storage solutions.

In summary, security is a paramount concern in blockchain and cryptocurrency. The immutable nature of blockchain, combined with cryptographic algorithms, consensus mechanisms, and public-private key cryptography, provides a robust security framework. However, users must remain vigilant in protecting their private keys to mitigate the risk of unauthorized access and potential loss of digital assets.

Advantages and disadvantages of blockchain in cryptocurrency

Blockchain technology offers several advantages in the realm of cryptocurrencies, revolutionizing the way financial transactions are conducted. However, it also presents certain drawbacks that need to be considered. Let’s explore the advantages and disadvantages of integrating blockchain with cryptocurrencies.

Advantages:

- Decentralization: Blockchain’s decentralized nature eliminates the need for intermediaries, such as banks or governments, in cryptocurrency transactions. This reduces costs, increases efficiency, and empowers individuals to have control over their financial transactions.

- Transparency: All transactions on the blockchain are transparent, visible to all participants. This transparency reduces the risk of fraud and promotes accountability within the cryptocurrency ecosystem.

- Security: The cryptographic security measures in blockchain protect cryptocurrency transactions from unauthorized access, ensuring the integrity and privacy of the data involved.

- Trustworthiness: Blockchain’s immutable nature and consensus mechanism provide a high level of trust among participants. Transactions recorded on the blockchain are tamper-resistant, making it difficult for malicious actors to manipulate or forge transaction data.

- Efficiency: Blockchain streamlines transaction processes, enabling faster and more efficient cross-border payments and reducing the need for manual reconciliation and verification.

Disadvantages:

- Scalability: Blockchain networks, especially public blockchains, can face scalability challenges when the number of transactions increases. The processing speed and capacity of the network may be limited, leading to potential delays and higher transaction fees.

- Energy Consumption: Mining, the process of validating transactions on many blockchain networks, consumes a significant amount of computational power and energy. This high energy consumption has raised concerns about the environmental impact of blockchain technology.

- Regulatory Challenges: The decentralized and borderless nature of cryptocurrencies can pose regulatory challenges for governments and financial institutions. The lack of centralized control and the potential for illicit activities raise questions about how to regulate and oversee the cryptocurrency ecosystem.

- User Responsibility: Cryptocurrency transactions rely on individuals securely managing their private keys. If a user loses or misplaces their private key, they may lose access to their digital assets permanently.

- Privacy Concerns: While blockchain offers transparency, some individuals may have concerns about their privacy in a system that records all transactions publicly. Although identities are often anonymized, it is still possible to trace transactions and link them to individuals in some cases.

It is essential to consider both the advantages and disadvantages of blockchain in relation to cryptocurrencies. While blockchain offers significant advantages, its drawbacks require careful consideration and ongoing innovation to address the challenges and maximize the potential of this transformative technology.

Future implications of blockchain in cryptocurrency

The future of blockchain technology in the realm of cryptocurrencies holds immense potential for transforming the financial landscape. As this technology continues to evolve, several implications can be anticipated.

1. Mainstream Adoption: Blockchain technology has the potential to bring cryptocurrencies into the mainstream. As blockchain solutions become more user-friendly, scalable, and accessible, adoption rates are expected to rise. This could lead to a shift in how individuals and businesses transact and manage their finances.

2. Financial Inclusion: Cryptocurrencies powered by blockchain can provide financial services to the unbanked and underbanked populations around the world. By reducing barriers to entry and eliminating the need for traditional banking requirements, blockchain-based cryptocurrencies can empower individuals who have been excluded from the traditional financial system.

3. Disintermediation: Blockchain technology eliminates the need for intermediaries in financial transactions. This disintermediation can significantly reduce transaction costs, increase efficiency, and disrupt traditional financial institutions, such as banks and payment processors.

4. Tokenization of Assets: Blockchain enables the tokenization of real-world assets, such as real estate, art, and intellectual property. This opens up new possibilities for fractional ownership, liquidity, and trading of traditionally illiquid assets. Through the use of smart contracts, the process of transferring and managing ownership can be automated and streamlined.

5. Smart Contracts: Smart contracts, self-executing programs built on blockchain, have the potential to revolutionize business processes and legal agreements. They can automate complex workflows, enforce predefined terms and conditions, and eliminate the need for intermediaries in contract execution. This can streamline various industries, such as supply chain management, insurance, and legal services.

6. Enhanced Privacy: As blockchain technology evolves, approaches to privacy are also developing. New solutions, such as zero-knowledge proofs and private transactions, allow for enhanced privacy in blockchain-based transactions. This can address concerns surrounding the public visibility of transactions while preserving the security and integrity provided by the blockchain.

7. Interoperability: The future of blockchain may involve increased interoperability, allowing different blockchain networks and cryptocurrencies to interact seamlessly. Interoperability would facilitate the transfer of assets and data across disparate blockchain platforms, leading to a more connected and efficient ecosystem.

8. Regulatory Frameworks: As blockchain and cryptocurrencies gain traction, governments around the world are developing regulatory frameworks to address the challenges and risks associated with this technology. Clear regulations can provide a sense of stability and legitimacy, fostering greater trust and confidence in the cryptocurrency space.

In summary, the future implications of blockchain in cryptocurrencies hold promise for mainstream adoption, financial inclusion, disintermediation, asset tokenization, smart contracts, enhanced privacy, interoperability, and regulatory frameworks. These advancements have the potential to reshape the financial landscape, empower individuals, and revolutionize various industries.