Introduction

Blockchain technology has emerged as a game-changer in various industries, and banking is no exception. With its decentralized and transparent nature, blockchain has the potential to revolutionize traditional banking systems and introduce a new era of secure and efficient financial transactions.

At its core, blockchain is a distributed ledger that allows multiple parties to record and verify transactions without the need for intermediaries. It operates on a network of computers and uses advanced encryption techniques to ensure the integrity and security of data. This technology gained prominence with the introduction of cryptocurrency, but its applications extend far beyond digital currencies.

Blockchain banking, also known as decentralized finance or DeFi, refers to the integration of blockchain technology into traditional banking systems. It aims to address the limitations of traditional banking by offering improved security, transparency, and efficiency. By leveraging blockchain, banks can streamline processes, reduce costs, and provide better services to their customers.

Unlike traditional banking systems that rely heavily on intermediaries such as banks, clearinghouses, and payment processors, blockchain banking allows for peer-to-peer transactions. This means that individuals can send and receive funds directly without the need for a central authority to oversee the transaction.

One of the key characteristics of blockchain banking is the immutability of data. Once a transaction is recorded on the blockchain, it cannot be modified or tampered with. This ensures the integrity and transparency of financial transactions, reducing the risk of fraud and providing users with a high level of trust.

The rise of blockchain banking also comes at a time when cybersecurity threats are increasing. Traditional banking systems are vulnerable to hacking and data breaches, putting customer’s personal and financial information at risk. With blockchain, the use of advanced encryption techniques and decentralized networks make it highly resistant to cyber attacks.

Overall, blockchain banking has the potential to reshape the banking industry by offering a more transparent, secure, and efficient alternative to traditional banking. In the following sections, we will explore how blockchain banking works, the benefits it provides, and the challenges it faces.

What is Blockchain?

Blockchain is a decentralized and distributed ledger technology that enables the secure and transparent recording of transactions across multiple computers or nodes. It was originally developed as the underlying technology for cryptocurrencies such as Bitcoin but has since found applications in various industries, including finance, supply chain management, and healthcare.

At its core, a blockchain is a digital ledger that contains a sequential and unchangeable record of transactions. Instead of having a centralized authority, the transactions are verified and stored by a network of computers known as nodes. These nodes work together to maintain consensus on the validity of transactions and ensure the security of the blockchain.

Transactions in a blockchain are grouped into blocks, which are cryptographically linked to form a chain. Each block contains a unique identifier, a timestamp, and a list of transactions. When a new transaction occurs, it is broadcasted to the network and validated by the nodes using a consensus mechanism, such as Proof of Work or Proof of Stake. Once validated, the transaction is added to a new block, which is then added to the existing chain.

One of the fundamental characteristics of blockchain is its immutability. Once a transaction is recorded on the blockchain, it cannot be altered or deleted without the consensus of the network. This ensures the integrity and transparency of the data stored on the blockchain, making it highly secure and resistant to fraud.

Another important feature of blockchain is its transparency. The entire transaction history is available to all participants of the network, and any changes made to the blockchain are visible to everyone. This transparency enables trust and accountability, as all parties can verify the authenticity of transactions and the ownership of assets.

Blockchain technology also offers a high level of security. The decentralized nature of the network makes it difficult for malicious actors to manipulate the data or perform fraudulent activities. Additionally, the use of cryptographic algorithms ensures that the data on the blockchain is encrypted and protected from unauthorized access.

In summary, blockchain is a decentralized ledger technology that allows for secure, transparent, and immutable recording of transactions. Its innovative design has the potential to revolutionize various industries and create new opportunities for efficiency and trust.

What is Blockchain Banking?

Blockchain banking, also known as decentralized finance or DeFi, refers to the integration of blockchain technology into traditional banking systems. It aims to revolutionize the way financial transactions are conducted by providing secure, transparent, and efficient solutions.

In blockchain banking, traditional intermediaries such as banks, clearinghouses, and payment processors are replaced by decentralized networks. Transactions are recorded on a blockchain, which is a distributed ledger accessible to all participants. This eliminates the need for a central authority to validate and oversee transactions, resulting in faster and cheaper transactions.

One of the key advantages of blockchain banking is the removal of geographical barriers. Traditional banking systems can be cumbersome and time-consuming, especially for cross-border transactions. With blockchain banking, individuals can send and receive funds directly without the need for intermediaries. This not only speeds up the process but also reduces costs associated with currency conversion and international transfers.

Blockchain banking also provides increased transparency and security. Traditional banking systems are often opaque, making it difficult for customers to track their transactions or verify the accuracy of their account balances. In blockchain banking, all transactions are recorded on a public ledger, accessible to all participants. This level of transparency ensures that all transactions can be audited and verified, reducing the risk of fraud and providing customers with a high degree of trust.

Security is another significant benefit of blockchain banking. Traditional banking systems are susceptible to cyber attacks and data breaches, putting customer’s personal and financial information at risk. With blockchain, the use of advanced encryption techniques and the decentralized nature of the network make it highly resistant to hacking attempts. Additionally, the immutability of data recorded on the blockchain ensures that it cannot be altered or tampered with, further enhancing security.

Furthermore, blockchain banking opens up opportunities for financial inclusion. In many parts of the world, people still lack access to traditional banking services. Blockchain technology enables individuals to participate in the financial system without the need for a traditional bank account. This can empower the unbanked population and provide them with opportunities for financial growth and stability.

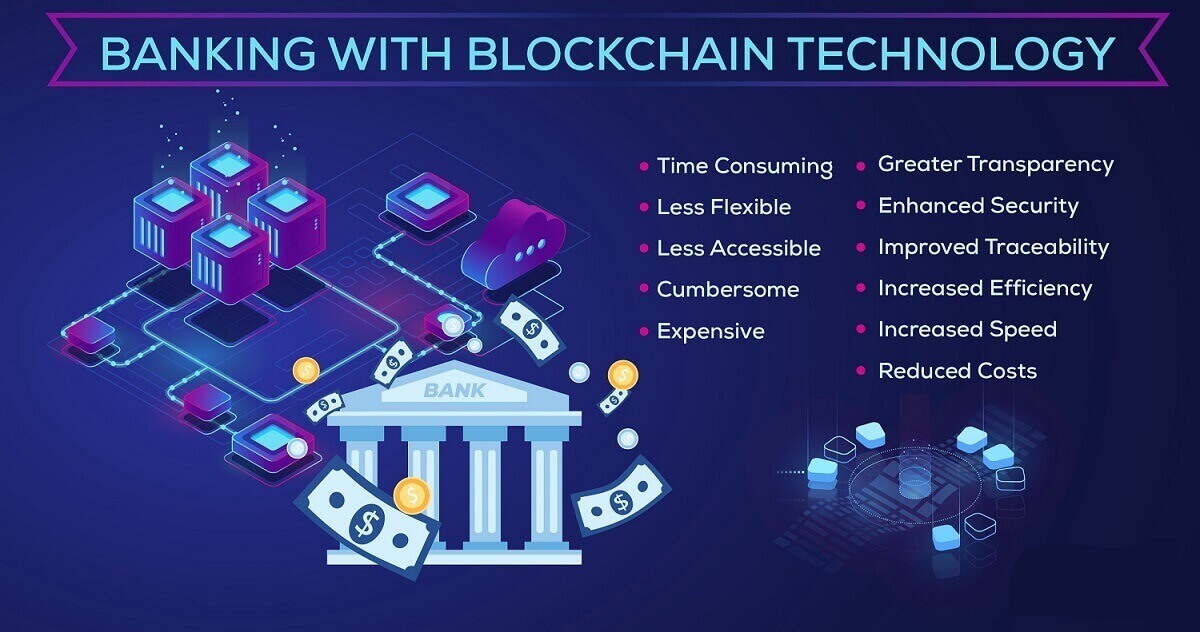

Overall, blockchain banking offers numerous benefits over traditional banking systems, including faster transactions, reduced costs, enhanced transparency, improved security, and increased financial inclusion. As the technology continues to evolve, we can expect to see more innovative solutions and applications in the financial sector.

How does Blockchain Banking work?

Blockchain banking operates on the principles of decentralization, transparency, and immutability. It leverages blockchain technology to facilitate secure and efficient financial transactions. Here’s a breakdown of how blockchain banking works:

1. Decentralization: In blockchain banking, there is no central authority or intermediary controlling the transactions. Instead, a network of computers, known as nodes, work together to validate and record transactions. This decentralized structure eliminates the need for intermediaries like banks, providing a peer-to-peer transaction environment.

2. Creating a transaction: To initiate a transaction, the sender creates a digital record known as a block. This block contains information such as the sender’s wallet address, the recipient’s wallet address, the transaction amount, and a unique identifier. The sender then digitally signs the block using cryptography to ensure the integrity and security of the transaction.

3. Verification and consensus: Once the block is created, it is broadcasted to all the nodes in the network. The nodes verify the validity of the transaction by checking if the sender has sufficient funds and if the transaction follows the rules of the blockchain protocol. This verification process ensures the consistency and accuracy of the transaction data.

4. Adding the block to the blockchain: After verification, the block is added to the blockchain. This is done by linking the new block to the previous block in the chain through a process called hashing. Hashing involves creating a unique digital fingerprint of the block using complex mathematical algorithms. This ensures the immutability of the blockchain, as any changes to a previous block would require altering all subsequent blocks in the chain, making it practically impossible to tamper with the transaction history.

5. Updating account balances: As transactions are added to the blockchain, the account balances of the sender and recipient are updated. Nodes maintain a copy of the blockchain and continuously synchronize their records with the network to reflect the most up-to-date account balances.

6. Transaction confirmation: Once a block is added to the blockchain, it is considered confirmed. The number of confirmations required for a transaction to be considered fully verified depends on the blockchain protocol. More confirmations increase the level of security and decrease the chances of a transaction being reversed or invalidated.

7. Accessing funds: Participants in the blockchain network can access their funds by using their unique cryptographic keys. Wallets, which can be hardware devices or software applications, store these keys and enable users to send and receive funds securely. These wallets interact with the blockchain and update the user’s account balance accordingly.

By leveraging the power of blockchain technology, blockchain banking provides a secure, transparent, and efficient way to conduct financial transactions. It eliminates the need for intermediaries, reduces transaction costs, and enables faster cross-border transfers, revolutionizing the traditional banking system.

Benefits of Blockchain Banking

Blockchain banking offers a wide range of benefits that have the potential to transform the traditional banking landscape. Here are some key advantages of adopting blockchain technology in the banking sector:

1. Enhanced Security: Blockchain technology provides a high level of security through its decentralized and immutable nature. The use of cryptographic algorithms and distributed consensus on the network minimizes the risk of fraud, hacking, and unauthorized access. Transactions recorded on the blockchain are transparent and tamper-proof, ensuring the integrity and confidentiality of financial data.

2. Increased Transparency: Traditional banking systems often lack transparency, making it difficult for customers to trust processes and verify the accuracy of their transactions. Blockchain banking, on the other hand, offers complete transparency by providing a transparent and verifiable record of all transactions on the blockchain. This transparency builds trust, reduces the risk of fraud, and enhances the overall credibility of the banking system.

3. Faster Transactions: Blockchain banking eliminates the need for intermediaries and manual verification processes, resulting in faster transaction settlements. With blockchain, transactions can be processed in real-time or near real-time, reducing the time and cost associated with traditional banking transactions that may involve multiple parties and lengthy reconciliation processes.

4. Cost Savings: Implementing blockchain technology in banking operations can lead to significant cost savings. By eliminating intermediaries and automating processes, blockchain banking reduces operational costs associated with manual reconciliation, paperwork, and third-party fees. Additionally, blockchain reduces the risk of fraud and lowers compliance costs by providing an auditable and transparent transaction history.

5. Simplified Cross-Border Payments: Traditional cross-border payments can be complex, time-consuming, and expensive, involving multiple intermediaries and currency conversions. Blockchain banking simplifies this process by enabling peer-to-peer international transactions without the need for intermediaries. By leveraging cryptocurrencies or stablecoins, cross-border payments can be conducted more efficiently, reducing fees and settlement times.

6. Financial Inclusion: Blockchain banking has the potential to promote financial inclusion by providing access to financial services to the unbanked and underbanked populations. With blockchain, individuals in remote areas can participate in the financial system, creating new opportunities for economic growth and empowerment.

7. Improved Auditing and Compliance: With all transactions recorded on the blockchain and accessible to all participants, auditing processes become more efficient and reliable. Regulatory compliance can be streamlined by automating compliance checks and ensuring better transparency into financial activities. This helps banks and regulatory bodies to monitor and investigate potential fraudulent activities more effectively.

These benefits of blockchain banking highlight its potential to create a more secure, transparent, efficient, and inclusive banking system. As the technology continues to evolve, we can expect to see further advancements and innovative use cases that will reshape the future of banking.

Challenges of Blockchain Banking

While blockchain banking offers numerous benefits, there are also several challenges that need to be addressed for wider adoption and integration. These challenges include:

1. Scalability: Blockchain technology faces scalability issues due to its consensus mechanism and the size of the blockchain. As the number of transactions increases, the processing time and resource requirements also increase. This can hinder the scalability of blockchain banking, especially in high-volume transaction environments, limiting its applicability in mainstream banking activities.

2. Regulatory and Legal Frameworks: Blockchain banking operates in a complex regulatory environment with varying laws and regulations across different countries. The lack of standardized regulations governing blockchain and cryptocurrencies can create legal challenges and uncertainty for banks and financial institutions. Developing robust regulatory frameworks that address issues such as data privacy, consumer protection, and anti-money laundering remains a significant challenge.

3. Interoperability: Blockchain networks often operate on different protocols and standards, making interoperability between different blockchain platforms a challenge. This can hinder seamless integration and communication between banks and other financial institutions, limiting the potential for widespread adoption of blockchain banking.

4. Security and Privacy Concerns: While blockchain technology enhances security through its cryptographic algorithms, there are still concerns regarding the security and privacy of sensitive financial data. Private keys, if compromised, can lead to unauthorized access to funds and personal information. Additionally, the public nature of certain blockchain networks can raise privacy concerns, as transaction information is accessible to all participants.

5. Energy Consumption: Some blockchain networks, particularly those using Proof of Work consensus algorithms, require significant computational power and energy consumption. This raises concerns about the environmental impact of blockchain technology and its sustainability in the long run. Addressing energy efficiency and exploring alternative consensus mechanisms can mitigate this challenge.

6. Adoption and User Experience: Wide-scale adoption of blockchain banking requires user-friendly interfaces and seamless integration with existing banking systems. Improving the user experience and educating users on the benefits and functionalities of blockchain technology is crucial for the successful integration and acceptance of blockchain banking solutions.

7. Governance and Standards: Blockchain networks lack unified governance structures and industry-wide standards. The absence of clear governance models can hinder decision-making, consensus building, and the resolution of disputes. Developing industry standards and establishing governance frameworks are essential for ensuring interoperability, compliance, and accountability in blockchain banking.

Addressing these challenges requires collaborative efforts from banks, regulators, technology providers, and industry stakeholders. Overcoming these hurdles will pave the way for the widespread adoption and integration of blockchain banking, unlocking its full potential in revolutionizing the financial sector.

Examples of Blockchain Banking

Blockchain banking has gained significant attention and adoption from various financial institutions around the world. Here are a few notable examples showcasing the application of blockchain technology in the banking sector:

1. JPMorgan Chase: JPMorgan Chase, one of the largest banks in the United States, has been actively exploring blockchain technology. They have developed Quorum, a blockchain platform built on the Ethereum network, to improve the efficiency and security of their banking operations. Quorum allows for faster and more secure payment transfers, smart contract automation, and enhanced data privacy.

2. Ripple: Ripple is a blockchain-based payment protocol and cryptocurrency designed to enable fast and low-cost international money transfers. Ripple’s blockchain technology has been adopted by various banks and financial institutions worldwide, including Santander, American Express, and Standard Chartered. Ripple’s network facilitates real-time settlement and offers a more efficient alternative to traditional cross-border payment systems.

3. DBS Bank: DBS Bank, based in Singapore, has embraced blockchain technology to enhance its trade finance operations. They have implemented a blockchain platform called DBS Blockchain Registry to digitize and streamline the trade finance process. This platform allows for secure and transparent trade document sharing among banks, reducing the risk of fraud and improving efficiency.

4. BBVA: BBVA, a Spanish multinational bank, has been actively exploring blockchain technology and its potential benefits. They have implemented blockchain-based solutions for various financial services, including international payments, supply chain finance, and trade finance. BBVA aims to enhance transaction speed, increase transparency, and reduce operational costs through their blockchain initiatives.

5. ING Group: ING Group, a Dutch multinational banking and financial services corporation, has made significant strides in blockchain banking. They have developed various blockchain applications, such as Easy Trading Connect, which simplifies the trading process for commodities and energy. ING has also partnered with various organizations to explore the use of blockchain in areas like identity management and digital asset custody.

These examples demonstrate the diverse applications of blockchain technology in the banking industry. Through these initiatives, financial institutions are leveraging blockchain to improve efficiency, enhance security, and create innovative solutions for their customers. As blockchain technology continues to evolve, we can expect to see even more advancements and adoptions in the field of blockchain banking.

Future of Blockchain Banking

The future of blockchain banking holds immense potential for transforming the traditional banking industry. As blockchain technology continues to evolve, we can expect to see the following developments and advancements:

1. Increased Adoption: With the growing awareness and understanding of blockchain technology, we can anticipate increased adoption of blockchain banking solutions by traditional financial institutions. Banks will be more inclined to leverage blockchain for faster, more secure, and cost-effective transactions, thereby moving towards a more decentralized and efficient banking system.

2. Interoperability and Standardization: Blockchain networks will likely become more interoperable, allowing for seamless integration and communication between different blockchain platforms. Industry-wide standards and governance frameworks are expected to emerge, ensuring compatibility and compliance among various blockchain-based banking systems.

3. Tokenization of Assets: The tokenization of real-world assets, such as stocks, bonds, real estate, and commodities, is expected to become more prevalent. Through blockchain technology, assets can be digitized and tokenized, allowing for fractional ownership, faster transactions, and increased liquidity in the market.

4. Smart Contracts and Automations: Smart contracts, self-executing agreements written on the blockchain, will play a significant role in streamlining banking processes. They will automate repetitive tasks, eliminate intermediaries, and facilitate secure and transparent transactions. Smart contracts have the potential to revolutionize areas such as loan origination, trade finance, and compliance monitoring.

5. Enhanced Security and Privacy: Blockchain technology will continue to enhance the security and privacy of banking transactions. Advancements in encryption and privacy protocols will provide individuals with greater control over their personal data, ensuring data protection while maintaining transparency and trust within the network.

6. Integration with Artificial Intelligence (AI) and Internet of Things (IoT): The integration of blockchain with AI and IoT technologies will create new possibilities in banking. AI algorithms can analyze blockchain data to provide personalized financial recommendations and prevent fraud. IoT devices can leverage blockchain for secure and automated financial transactions, such as smart payments between connected devices.

7. Central Bank Digital Currencies (CBDCs): Central banks worldwide are exploring the idea of issuing their own digital currencies using blockchain technology. CBDCs could potentially provide a more efficient and secure means of payment while enabling better monetary policy implementations and financial inclusion.

The future of blockchain banking is promising, with the potential to revolutionize the way we conduct financial transactions and interact with the banking system. As technology evolves and regulatory frameworks mature, blockchain banking will continue to offer innovative solutions, increased efficiency, and enhanced financial services for individuals and businesses alike.

Conclusion

Blockchain banking has emerged as a transformative force in the traditional banking industry. By leveraging decentralized networks, cryptographic algorithms, and transparent ledgers, blockchain technology offers numerous benefits such as enhanced security, increased transparency, faster transactions, and reduced costs.

Through the adoption of blockchain, financial institutions can streamline their processes, provide more efficient services to their customers, and promote financial inclusion by reaching the unbanked population. Moreover, blockchain banking has the potential to reshape cross-border payments, improve auditing and compliance procedures, and create new opportunities for tokenization of assets.

While blockchain banking presents significant opportunities, it also comes with challenges that need to be addressed. Scalability, regulatory frameworks, interoperability, security concerns, energy consumption, and user adoption are among the key challenges that need to be overcome for wider adoption and integration.

The future of blockchain banking holds great promise. Increased adoption, improved interoperability, and the integration of blockchain with AI, IoT, and CBDCs will further revolutionize the banking sector. As blockchain technology continues to evolve, financial institutions, regulators, and other stakeholders need to collaborate to address challenges, develop standards, and establish robust governance frameworks.

Overall, blockchain banking has the potential to create a more secure, transparent, efficient, and inclusive banking system. By embracing blockchain technology and harnessing its power, the future of banking can be reshaped, providing individuals and businesses with a more seamless, accessible, and secure financial ecosystem.