Introduction

Welcome to the digital age, where technological advancements continue to reshape various aspects of our lives. One area that has witnessed significant transformation is the world of payments. Traditional methods of conducting transactions, such as cash and physical cards, are gradually being replaced by digital payments. As this shift occurs, a new challenger has emerged: blockchain technology.

The payments industry has long been plagued by various challenges, including security concerns, high transaction costs, and slow processing times. However, with the advent of blockchain, these issues have the potential to be addressed and overcome. Blockchain, most commonly associated with cryptocurrencies like Bitcoin, is a decentralized ledger that records transactions across multiple computers, ensuring transparency, security, and immutability.

In this article, we will explore the role of blockchain in solving the payments riddle. By leveraging the unique features and capabilities of blockchain technology, we can expect to witness a revolution in the way we conduct financial transactions. From enhanced security and fraud prevention to faster, cheaper, and more efficient transactions, blockchain has the potential to reshape the landscape of payments as we know it.

Throughout this article, we will delve into the various aspects of blockchain technology that make it an ideal solution for the challenges faced by the payments industry. We will also discuss the limitations and potential barriers to adoption that need to be addressed for widespread implementation.

So, fasten your seatbelts as we embark on a journey through the fascinating world of blockchain and its potential to revolutionize the way we make payments.

Understanding the Payments Riddle

The payments riddle refers to the complex challenges that exist within the payments industry. Traditional methods of making payments often involve lengthy processes, high fees, and security vulnerabilities. These issues have been a hindrance to seamless transactions and have created opportunities for fraud and inefficiency.

One of the main challenges is the lack of secure and transparent payment systems. Traditional methods rely on centralized authorities, such as banks, to process and verify transactions. This centralized approach leaves room for security breaches and unauthorized access to sensitive financial information.

Moreover, the costs associated with traditional payment methods can be exorbitant. Transaction fees, foreign exchange rates, and intermediary charges can significantly impact the overall cost of a transaction, especially for cross-border payments.

Additionally, the speed of traditional payment systems often falls short of consumer expectations. Waiting times for transactions to be processed and settled can be time-consuming, particularly for international payments that may take several days to complete.

Furthermore, the accessibility of financial services remains a challenge for many individuals and businesses, especially in developing countries. Limited access to banking infrastructure and the need for a physical presence to conduct financial transactions hinder financial inclusion.

These challenges collectively form the payments riddle, where traditional payment methods struggle to provide secure, efficient, and accessible solutions for individuals and businesses alike.

Fortunately, blockchain technology has the potential to solve this riddle by introducing a new paradigm for payments. By leveraging the features of blockchain, such as decentralization, security, and immutability, we can address the shortcomings of traditional payment systems and unlock a world of possibilities.

In the following sections, we will explore how blockchain works and its role in solving the payments riddle. We will examine its impact on security and fraud prevention, transaction speed and efficiency, international payments, decentralized verification, smart contracts, and financial inclusion.

What is Blockchain?

Before diving into the role of blockchain in solving the payments riddle, it is crucial to understand what blockchain is and how it works. Developed as a foundational technology for cryptocurrencies like Bitcoin, blockchain is a decentralized and distributed ledger that records transactions across multiple computers.

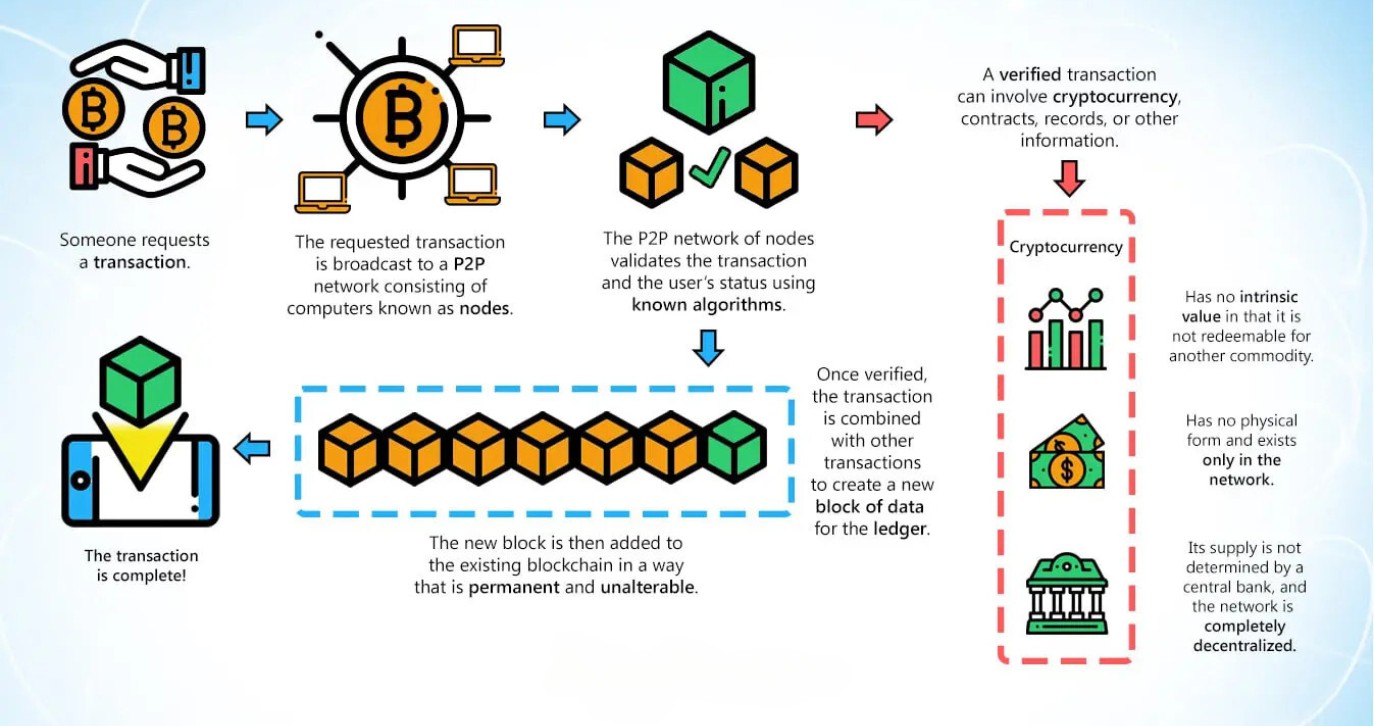

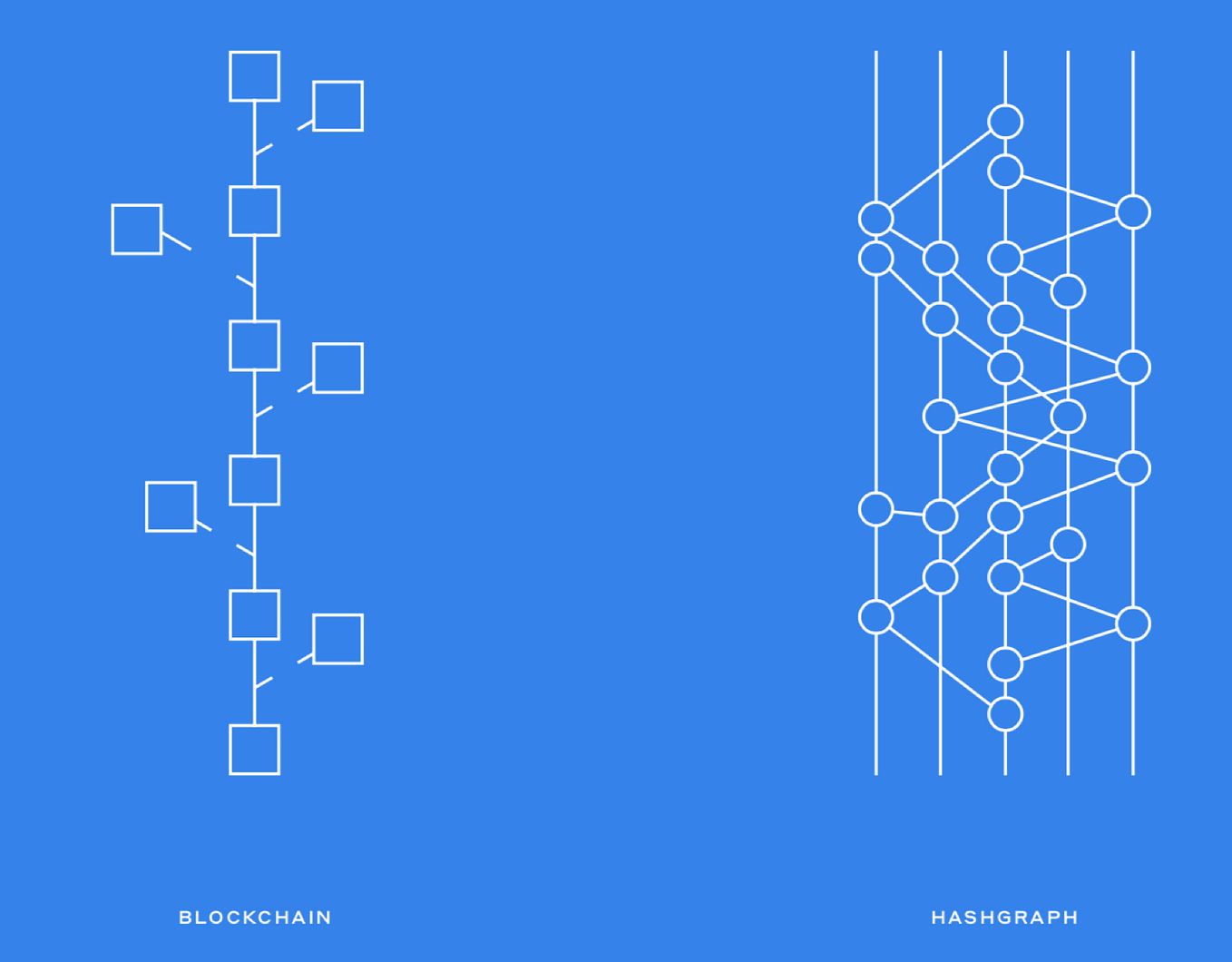

At its core, a blockchain is a series of blocks, where each block contains a list of transactions. These blocks are linked together using cryptographic hashes, creating an immutable chain of information. This decentralized nature of blockchain eliminates the need for a central authority, such as a bank, to validate and process transactions.

So, how does blockchain ensure security and trust in transactions? One key feature is the consensus mechanism, where a network of computers, also known as nodes, collectively agrees on the validity of a transaction. This consensus mechanism, often achieved through techniques like proof-of-work or proof-of-stake, eliminates the need for intermediaries and reduces the risk of fraud.

Another vital aspect of blockchain is its transparency. Once a transaction is added to a block and confirmed by the network, it becomes visible to all participants in the blockchain network. This transparency ensures accountability and helps in the prevention of fraud and manipulation.

Blockchain technology also provides immutability, meaning that once a transaction is recorded on the blockchain, it is nearly impossible to alter. Each block in the chain contains a unique hash that is calculated based on the transactions within the block. Any attempt to modify the data in a block would require changing the hash, which would in turn affect the subsequent blocks in the chain. This makes blockchain tamper-resistant and enhances trust in the system.

Furthermore, blockchain has the potential to leverage smart contracts. Smart contracts are self-executing contracts with the terms of the agreement written into code. These contracts are stored and executed on the blockchain, eliminating the need for intermediaries and enabling automated and secure transaction processing.

Overall, blockchain is a revolutionary technology that offers a decentralized, secure, transparent, and immutable way of recording and verifying transactions. Its unique features and capabilities position blockchain as a promising solution to address the challenges faced by traditional payment systems.

Blockchain’s Role in Payments

The emergence of blockchain technology presents a significant opportunity to transform the world of payments. By leveraging the unique features of blockchain, we can overcome the challenges faced by traditional payment systems and unlock a more secure, efficient, and accessible payment ecosystem.

One of the key advantages of blockchain in payments is enhanced security and fraud prevention. Traditional payment systems rely on a central authority to verify and process transactions, making them susceptible to security breaches. In contrast, blockchain’s decentralized nature and cryptographic techniques ensure that transactions are securely recorded and verified by a network of participants. This reduces the risk of fraud and unauthorized access to sensitive financial information.

Blockchain technology also enables faster, cheaper, and more efficient transactions. Traditional payment systems often involve layers of intermediaries, leading to high transaction fees and processing delays. With blockchain, transactions can be directly executed peer-to-peer, eliminating the need for intermediaries and reducing associated costs. Additionally, the decentralized nature of blockchain allows for faster settlement times, enabling near-instantaneous transactions, particularly for cross-border payments.

Furthermore, blockchain has the potential to revolutionize international payments. Cross-border transactions are currently cumbersome and time-consuming, often involving intermediaries and multiple currencies. Blockchain’s ability to facilitate direct peer-to-peer transactions can streamline this process and reduce costs. The transparency of blockchain also enables real-time tracking and monitoring of international payments, enhancing visibility and accountability.

Decentralization and trustless verification are other key aspects of blockchain that contribute to its role in payments. The decentralized nature of blockchain eliminates the need for a central authority, providing a level playing field for participants. Transactions are validated and confirmed through consensus mechanisms, ensuring trust without the reliance on intermediaries. This trustless verification mechanism enhances transaction security and reduces the need for third-party involvement.

Moreover, blockchain enables the implementation of smart contracts, which automate and enforce the terms of agreements. Smart contracts facilitate seamless execution and settlement of payments, removing the need for manual intervention and reducing the potential for errors or disputes. This automated process improves efficiency and reduces administrative costs.

Finally, blockchain has the potential to promote financial inclusion and accessibility. Traditional payment systems often require a physical presence or extensive documentation, which may hinder individuals and businesses from accessing financial services. With blockchain, individuals can access financial services through mobile devices, enabling financial inclusion for the unbanked population.

In summary, blockchain technology presents a unique opportunity to revolutionize the payments industry. Its ability to enhance security, improve transaction speed and efficiency, facilitate international payments, decentralize verification, automate processes with smart contracts, and promote financial inclusion makes blockchain a powerful solution in solving the payments riddle.

Enhanced Security and Fraud Prevention

Security and fraud prevention are paramount in the world of payments. Traditional payment systems rely on centralized authorities to validate and process transactions, leaving them vulnerable to security breaches and unauthorized access. However, blockchain technology offers enhanced security measures and stronger fraud prevention mechanisms.

One of the key features of blockchain that enhances security is its decentralized nature. In traditional payment systems, a single point of failure can lead to catastrophic consequences. In contrast, blockchain operates on a distributed network of computers known as nodes. Each node maintains a copy of the blockchain, ensuring that no single entity has control over the entire system. This decentralized network makes it exceedingly difficult for hackers to manipulate or compromise the blockchain, providing a higher level of security.

Moreover, the transparency of blockchain contributes to security and fraud prevention. Once a transaction is recorded on the blockchain, it becomes visible to all participants in the network. This transparency ensures that transactions are open to scrutiny and can be verified by anyone on the network. Any attempt to alter or manipulate the transaction data would require consensus from the majority of nodes, making fraudulent activities and tampering highly unlikely.

In addition to decentralization and transparency, blockchain utilizes cryptographic techniques to secure transactions. Every transaction is encrypted and linked to the previous transaction through a unique hash. This cryptographic hash protects the integrity of the transaction data, ensuring that any modifications or tampering would be immediately detected. Furthermore, the use of public-private key cryptography offers secure user authentication and protects sensitive financial information.

Another significant aspect of blockchain security is the consensus mechanism that validates transactions. Consensus mechanisms, such as proof-of-work or proof-of-stake, require network participants to agree on the validity of transactions before they are added to the blockchain. This consensus process ensures that only legitimate transactions are accepted, preventing fraudulent or malicious activities.

Furthermore, the immutability of blockchain adds an additional layer of security. Once a transaction is recorded on the blockchain and confirmed by the network, it becomes nearly impossible to alter or delete. The blocks in the chain are interconnected through cryptographic hashes, with any modification in one block affecting the subsequent blocks, making it virtually impossible to tamper with past transactions.

With enhanced security measures and fraud prevention mechanisms, blockchain technology provides a robust solution for securing payments in various industries. Its decentralized nature, transparency, cryptographic techniques, consensus mechanisms, and immutability collectively contribute to a more secure payment ecosystem, reducing the risks associated with fraud and unauthorized access.

Faster, Cheaper, and More Efficient Transactions

The speed, cost, and efficiency of transactions have long been pain points in traditional payment systems. However, blockchain technology has the potential to revolutionize the way transactions are conducted by offering faster settlement times, reducing costs, and streamlining the overall payment process.

One of the primary advantages of blockchain in payments is the elimination of intermediaries. Traditional payment systems often involve multiple intermediaries, such as banks and payment processors, adding complexity and increasing transaction costs. With blockchain, transactions can be executed directly between two parties, removing the need for intermediaries and reducing associated fees.

Moreover, the decentralized nature of blockchain enables near-instantaneous transactions. In traditional payment systems, settlement times can be prolonged, particularly for cross-border transactions that require involvement from multiple intermediaries. Blockchain’s peer-to-peer model allows for direct transaction execution and immediate verification, resulting in significantly faster settlement times.

Reduced transaction costs are another significant advantage of blockchain in payments. Traditional payment systems often charge various fees, including transaction fees, currency conversion fees, and intermediary fees. These costs can add up, especially for international transactions. By eliminating intermediaries and streamlining the payment process, blockchain can significantly reduce transaction costs, making it a more cost-effective solution for individuals and businesses.

Furthermore, blockchain technology can enhance the overall efficiency of transactions. With the elimination of manual processes and paperwork, blockchain automates and streamlines transaction processing. By leveraging smart contracts, payment terms and conditions can be programmed into the blockchain, allowing for seamless and automated execution. This removes the need for manual intervention, reduces administrative overhead, and minimizes the potential for errors or disputes.

Blockchain’s ability to facilitate micropayments is another factor contributing to its efficiency. Micropayments, involving tiny amounts of money, have traditionally been difficult to execute due to high transaction fees. However, blockchain’s low transaction costs make micropayments more feasible and enable new business models in areas such as content monetization, online gaming, and pay-per-use services.

Furthermore, the transparency of blockchain enables improved auditing and reconciliation processes. All transactions recorded on the blockchain are visible to all participants, providing real-time access to transaction information. This transparency reduces the need for extensive manual reconciliation, as parties can independently verify and trace transactions on the blockchain, thereby improving operational efficiency.

In summary, blockchain technology offers faster, cheaper, and more efficient transactions compared to traditional payment systems. Through the elimination of intermediaries, near-instantaneous settlement times, reduced transaction costs, streamlined processes through smart contracts, facilitation of micropayments, and enhanced transparency for auditing and reconciliation, blockchain has the potential to revolutionize the speed and efficiency of transactions in the payment industry.

Improved International Payments

International payments have long been plagued by complexity, high fees, and slow processing times. However, blockchain technology offers a promising solution to address these challenges and significantly improve the efficiency and cost-effectiveness of international transactions.

One of the key advantages of blockchain in international payments is the elimination of intermediaries. Traditional cross-border transactions often involve multiple banks and financial institutions, each charging their own fees and requiring time for processing and verification. With blockchain, transactions can be conducted directly between parties, reducing the need for intermediaries and streamlining the payment process.

By removing intermediaries, blockchain bypasses the delays and costs associated with their involvement. Cross-border transactions require coordination between different banking systems and currencies, which can result in lengthy processing times. With blockchain, transactions are executed on a decentralized network, enabling near-instantaneous settlement and reducing the time required for cross-border payments.

Furthermore, traditional international transfers often involve currency conversions, leading to additional costs and potential losses due to unfavorable exchange rates. With blockchain, digital currencies that operate across borders, such as stablecoins, can be utilized to facilitate direct peer-to-peer payments without the need for currency conversion. This reduces exchange rate risks and minimizes associated fees.

In addition to speed and cost, blockchain technology brings greater transparency and traceability to international payments. Every transaction recorded on the blockchain is visible to all participants, creating a transparent audit trail. This transparency enhances accountability, as parties can independently verify the details and progress of the transaction. Furthermore, the immutability of blockchain ensures the integrity and authenticity of the transaction data, reducing the risk of fraud and providing a higher level of trust in cross-border transactions.

Blockchain’s ability to facilitate real-time tracking and monitoring of international payments is another significant advantage. Traditional payment systems often lack transparency in the status and location of funds during the transfer process. With blockchain, participants can track and trace the progress of their transactions, providing increased visibility and certainty.

Additionally, blockchain technology minimizes the reliance on correspondent banking relationships, which can be costly and time-consuming. Correspondent banking involves a series of relationships between banks that facilitate cross-border transfers. The use of blockchain reduces the need for these relationships, enabling direct interactions between parties and eliminating associated fees and delays.

Overall, blockchain technology has the potential to revolutionize international payments by offering faster, more cost-effective, and transparent transactions. Through the elimination of intermediaries, real-time tracking, reduced reliance on currency conversions, enhanced transparency and traceability, and the removal of correspondent banking relationships, blockchain can significantly improve the efficiency and accessibility of cross-border transactions.

Decentralization and Trustless Verification

Decentralization and trustless verification are two fundamental concepts that make blockchain technology a game-changer in the world of payments. These concepts reshape the traditional trust models and introduce a new paradigm that eliminates the need for intermediaries and enhances transaction security and transparency.

One of the key features of blockchain is its decentralized nature. Unlike traditional payment systems that rely on a central authority, such as a bank, to verify and process transactions, blockchain operates on a distributed network of computers known as nodes. Each node maintains a copy of the blockchain, ensuring that no single entity has control over the entire system.

This decentralized architecture offers numerous benefits for payments. By removing the reliance on a central authority, blockchain enhances the security of transactions. In traditional systems, a single point of failure can have catastrophic consequences, leaving transactions vulnerable to hacking and fraud. In contrast, blockchain’s decentralized network makes it exceedingly difficult for attackers to manipulate the system, ensuring a higher level of security.

Furthermore, decentralization increases the resilience and availability of the payment system. Traditional systems may experience downtime or disruptions, causing transaction delays and inconvenience for users. With blockchain, the distributed nature of the network ensures that even if some nodes go offline, the system continues to function, maintaining the availability of transactions.

Another significant aspect of blockchain is trustless verification. Traditional payment systems rely on trust in intermediaries to validate and process transactions. Blockchain, on the other hand, operates on a trustless model. Transactions on the blockchain are verified and confirmed by a network of participants, known as the consensus mechanism, without the need to trust a central authority.

This trustless verification mechanism is achieved through cryptographic techniques and consensus algorithms like proof-of-work or proof-of-stake. Network participants independently validate transactions and reach a consensus on their validity. As a result, blockchain transactions do not require trust in intermediaries or rely on a centralized authority, making the system more resilient to fraud and manipulation.

Furthermore, the transparency of blockchain complements trustless verification. Once a transaction is recorded on the blockchain, it becomes visible to all participants in the network. This transparency allows for independent auditability and verification, as anyone can review the transaction history and ensure its integrity. This increased transparency provides a higher level of trust in the payment system and reduces the risk of fraudulent activities.

In summary, decentralization and trustless verification are fundamental characteristics of blockchain technology that reshape the trust models in payments. By eliminating the need for intermediaries, blockchain enhances transaction security and reduces the risk of fraud. The trustless verification mechanism, along with the transparency of the blockchain, provides a new level of trust and assurance in the system, ensuring the integrity and authenticity of transactions without relying on a central authority.

Smart Contracts and Automation

Smart contracts and automation are two powerful features of blockchain technology that have the potential to revolutionize the payments industry. By enabling self-executing contracts and automating transaction processes, blockchain simplifies and streamlines payment operations, reducing the need for intermediaries and increasing efficiency.

At its core, a smart contract is a computer program that runs on a blockchain. These contracts are automatically executed once predefined conditions are met. Smart contracts eliminate the need for intermediaries to enforce contractual terms, as the code itself ensures that the agreed-upon conditions are fulfilled.

One of the main advantages of smart contracts is their ability to automate and simplify contractual processes. Traditional payment systems often involve manual interventions and complex workflows for contract execution and settlement. With smart contracts, payment terms and conditions are written into the code and automatically enforced, removing the need for manual intervention and reducing the potential for errors or disputes.

For example, in a supply chain scenario, a smart contract can be programmed to release payment automatically to the supplier once the delivery is confirmed by a trusted third party or when certain predefined criteria are met. This automation reduces administrative overhead, accelerates transaction processing, and minimizes the risk of payment delays or disputes.

Furthermore, smart contracts facilitate faster and more accurate settlement of payments. Traditional payment systems often involve multiple intermediaries who need to verify and settle transactions. These processes can be time-consuming and prone to errors. With smart contracts, payments can be settled in near real-time, as the terms of the contract are automatically executed once the agreed-upon conditions are met. This speed and accuracy not only streamline payment operations but also enhance user experience and customer satisfaction.

In addition to automation and efficiency, smart contracts offer increased transparency and accountability. Since the terms and conditions of the contract are encoded in the blockchain, they are visible to all participants. This transparency ensures that all parties have a clear understanding of the contractual obligations and can independently verify the execution of the contract. This visibility reduces the potential for fraud and builds trust among participants.

Moreover, the use of smart contracts can bring cost savings by eliminating the need for intermediaries and reducing administrative overhead. By automating processes, smart contracts streamline transaction operations, reducing the costs associated with manual interventions, paperwork handling, and reconciliation activities.

The potential applications of smart contracts in payments are vast and span various industries. From automated payment processing to conditional payments, escrow services, and revenue sharing agreements, smart contracts have the potential to transform the way payments are made and managed.

In summary, smart contracts and automation are powerful features of blockchain technology that simplify and streamline payment processes. By enabling self-executing contracts and automating transaction operations, blockchain eliminates the need for intermediaries, enhances efficiency, increases transparency, and reduces costs. The potential applications of smart contracts in the payments industry are broad, paving the way for more streamlined and secure payment transactions.

Financial Inclusion and Accessibility

Financial inclusion, the ability for individuals and businesses to access and participate in financial services, is a challenge faced by many around the world. Traditional payment systems often require a physical presence, extensive documentation, and access to banking infrastructure, making it difficult for certain populations to participate in the formal financial ecosystem. However, blockchain technology has the potential to promote financial inclusion and enhance accessibility by leveraging its unique features.

One of the key advantages of blockchain in promoting financial inclusion is its ability to offer digital wallets and digital currencies. With blockchain, individuals can access financial services through mobile devices, enabling them to send, receive, and store funds without the need for a traditional bank account. This lowers the barrier to entry and provides financial services to the unbanked population, who may lack access to banking infrastructure or face challenges in meeting traditional banking requirements.

Additionally, blockchain’s low-cost and efficient payment infrastructure allow for micropayments, which are small-value transactions often considered impractical by traditional payment systems due to high transaction costs. On the blockchain, micropayments can be executed economically, opening up new opportunities for businesses that rely on microtransactions, such as content creators, freelancers, and online gaming platforms. This allows individuals with limited financial resources to participate in the digital economy.

Moreover, blockchain’s borderless nature facilitates cross-border remittances. Remittances, often sent by foreign workers to their families in their home countries, can be expensive and time-consuming due to intermediary fees and currency conversion costs. Blockchain-based remittances offer a more affordable and efficient alternative by minimizing intermediaries, eliminating the need for currency conversions, and providing near-instantaneous settlement. This significantly benefits individuals in underserved regions who rely on remittances for their financial well-being.

Blockchain technology also offers a level of financial privacy and security, which can be especially valuable for individuals in countries with unstable political or economic environments. With blockchain, individuals can have control over their financial transactions and data, mitigating the risks of censorship, confiscation, or unauthorized access. This empowers individuals to take charge of their financial lives, fostering financial autonomy and inclusion.

Furthermore, blockchain can enable the creation of identity management systems, offering individuals without official identification documents the opportunity to establish their digital identities. This is particularly beneficial for refugees, migrants, and those living in remote areas who may lack traditional forms of identification. Digital identities based on blockchain can unlock access to financial services, healthcare, education, and other opportunities, enhancing social and economic inclusion.

By leveraging the unique features of blockchain technology, such as digital wallets, low-cost micropayments, efficient cross-border remittances, financial privacy, and identity management, we can empower individuals and businesses with greater financial inclusion and accessibility. Blockchain has the potential to bridge the gap between the unbanked population and formal financial systems, opening up doors for economic participation, empowerment, and growth.

Challenges and Limitations of Blockchain Payments

While blockchain technology holds immense potential to revolutionize the payments industry, it is not without its challenges and limitations. Understanding these obstacles is crucial for the successful adoption and implementation of blockchain payments.

One of the main challenges is scalability. Blockchain networks, such as Bitcoin and Ethereum, have faced scalability issues, limiting the number of transactions they can handle. The decentralized nature of blockchain requires all nodes to process and validate each transaction, resulting in slower transaction speeds and higher resource requirements. To overcome this challenge, various solutions are being explored, including layer two solutions, such as the Lightning Network, and the development of new consensus algorithms that enhance scalability.

Another challenge is regulatory uncertainty and compliance. As blockchain technology expands into the payments industry, regulators seek to establish guidelines and regulations to ensure security, consumer protection, and adherence to anti-money laundering (AML) and know-your-customer (KYC) regulations. The intersection of blockchain with traditional financial regulations presents challenges and requires coordination between technological advancements and regulatory frameworks.

Interoperability is another limitation of blockchain payments. With multiple blockchain platforms and cryptocurrencies in existence, the lack of standardization and interoperability between them can hinder the seamless exchange of value. Efforts are underway to develop interoperability protocols and frameworks that enable different blockchain networks to communicate and transact with one another, laying the foundation for widespread blockchain adoption in the payments industry.

Another limitation is the association of blockchain with cryptocurrencies. While cryptocurrencies have their merits, their volatility can pose challenges for daily transactions. The value of cryptocurrencies can fluctuate significantly, creating uncertainty and instability when conducting payments. Stablecoins, which are cryptocurrencies pegged to a stable value, have emerged as a potential solution to this challenge, providing a stable medium of exchange for blockchain payments.

Furthermore, the energy consumption of blockchain networks, particularly those using proof-of-work consensus algorithms, has raised concerns about its environmental impact. The computational power required to validate transactions consumes a significant amount of electricity. The development and adoption of more energy-efficient consensus algorithms, such as proof-of-stake, can address this limitation and reduce the ecological footprint of blockchain networks.

Privacy is another consideration in blockchain payments. While the transparency of blockchain enhances security and trust, it can also compromise user privacy. All transactions on a public blockchain are visible to all participants, potentially revealing sensitive financial information. Privacy-focused blockchain solutions, such as zero-knowledge proofs and confidential transactions, are being developed to address privacy concerns without compromising the overall security of the system.

Lastly, the human factor plays a role in the adoption of blockchain payments. Educating users about blockchain technology and its benefits, as well as providing user-friendly interfaces and seamless onboarding processes, is crucial to widespread adoption. Resistance to change and a lack of familiarity with the technology can pose challenges in convincing individuals and businesses to shift from traditional payment systems to blockchain-based solutions.

In summary, while blockchain payments offer numerous advantages, challenges and limitations exist. Scalability, regulatory compliance, interoperability, cryptocurrency volatility, energy consumption, privacy, and user adoption are among the hurdles that need to be addressed. By addressing these challenges, blockchain technology can unlock its full potential in revolutionizing the payments industry.

Conclusion

Blockchain technology has emerged as a powerful solution that has the potential to revolutionize the payments industry. By leveraging its unique features, such as enhanced security, faster and cheaper transactions, improved international payments, decentralization, trustless verification, smart contracts, and financial inclusion, blockchain addresses the challenges faced by traditional payment systems.

Through enhanced security measures and fraud prevention mechanisms, blockchain technology provides a more secure and transparent environment for transactions. The elimination of intermediaries, faster settlement times, and reduced transaction costs contribute to faster, cheaper, and more efficient transactions. Improved international payments are facilitated by bypassing the need for multiple intermediaries, enabling direct peer-to-peer transactions, and reducing currency conversion fees.

Decentralization and trustless verification reshape the trust models in payments by eliminating the need for intermediaries and enabling secure and transparent transactions. Smart contracts and automation streamline payment operations, reducing manual interventions, minimizing errors, and enhancing efficiency. Financial inclusion and accessibility are fostered through digital wallets, low-cost micropayments, efficient cross-border remittances, increased financial privacy, and the establishment of digital identities.

However, blockchain payments also face challenges and limitations. Scalability, regulatory compliance, interoperability, cryptocurrency volatility, energy consumption, privacy concerns, and user adoption pose hurdles that need to be addressed for widespread blockchain adoption. Overcoming these challenges requires continuous innovation, collaboration between stakeholders, and ongoing regulatory efforts.

In conclusion, blockchain technology has the transformative potential to reshape the payments industry. Its ability to provide enhanced security and efficiency, improve international payments, foster financial inclusion, and automate processes through smart contracts opens up new horizons for individuals and businesses. By addressing the challenges and limitations, blockchain can unlock its full potential and pave the way for a future where payments are secure, transparent, accessible, and efficient for all.