Introduction

Afterpay is a popular buy-now-pay-later service that has gained significant traction in the retail industry. It offers consumers the opportunity to purchase products and services upfront and pay for them in installments, without the need for traditional credit checks or interest charges. This convenient payment method has proven to be a win-win for both customers and retailers, driving sales and boosting customer loyalty.

However, while Afterpay may be an attractive option for consumers, retailers need to understand the costs and fees associated with using this service. It is crucial for retailers to have a clear understanding of Afterpay’s fees and charges, as they can impact the profitability of their business and overall financial health.

In this article, we will explore the fees and charges that Afterpay imposes on retailers, providing insights into the various costs and considerations involved when integrating this payment option into your business.

By the end of this article, you will have a comprehensive understanding of Afterpay’s fees, ensuring that you can make informed decisions about whether Afterpay is the right choice for your business.

How does Afterpay work?

Before diving into the fees and charges that Afterpay imposes on retailers, let’s first understand how this buy-now-pay-later service actually works.

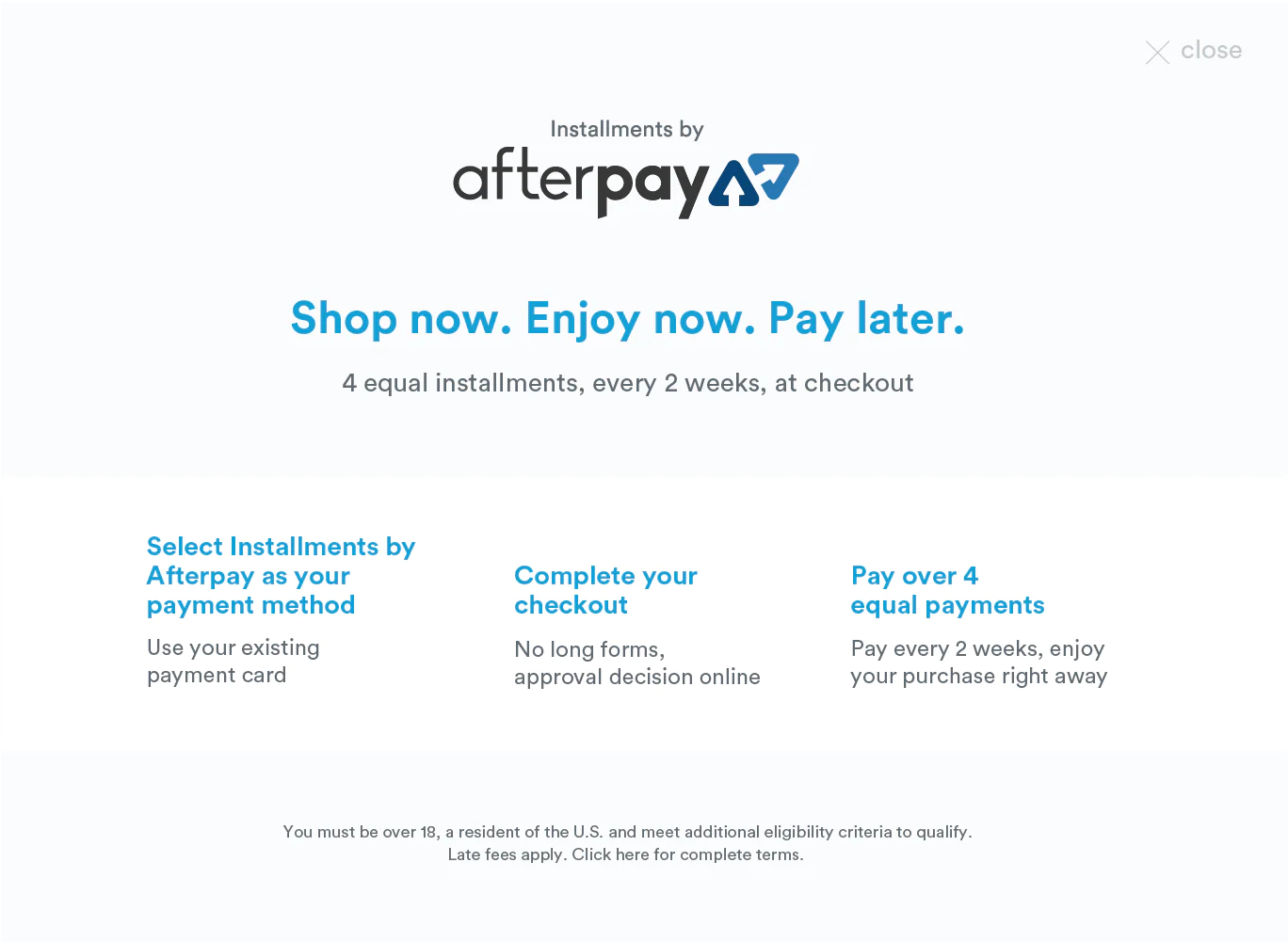

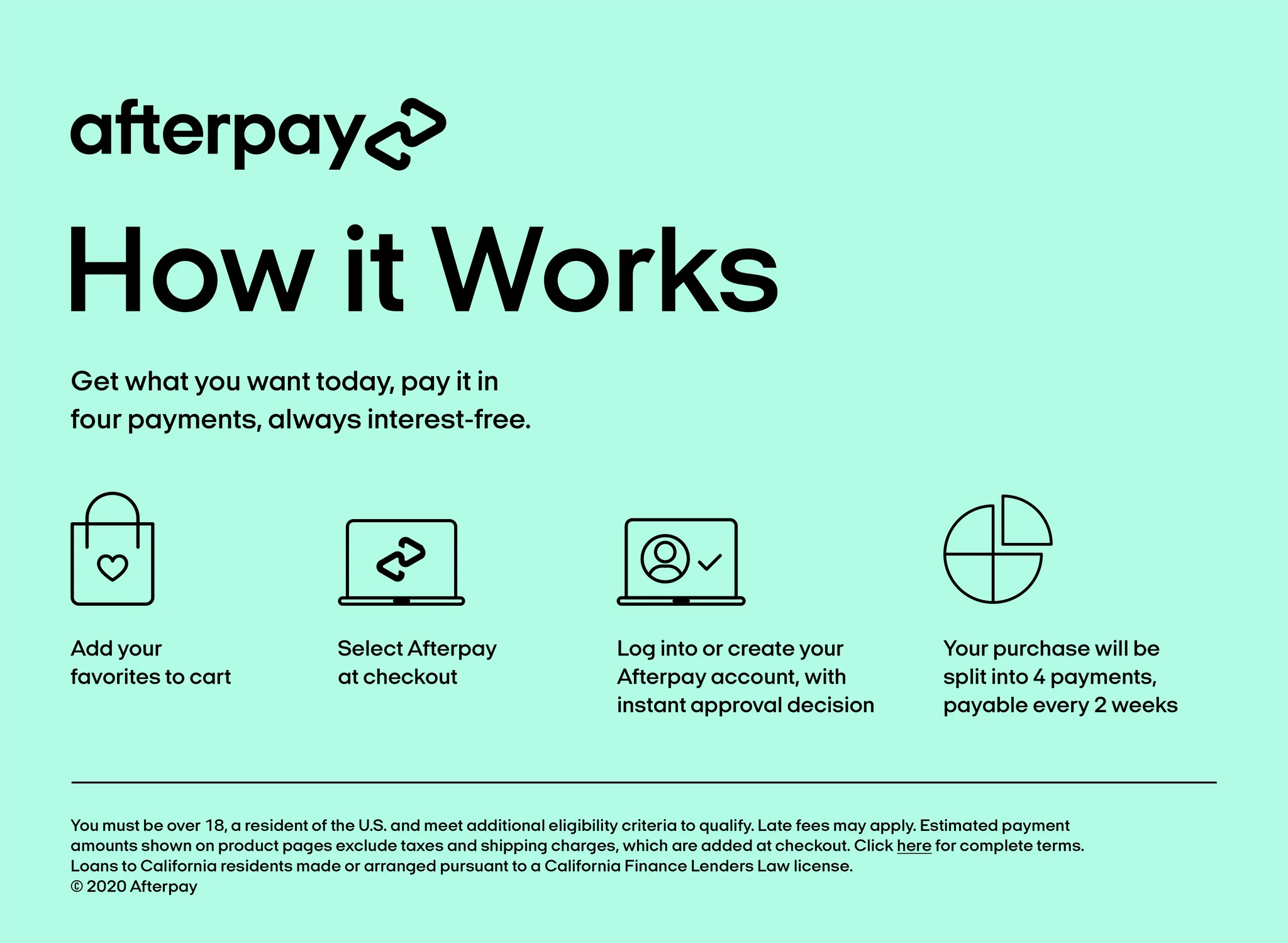

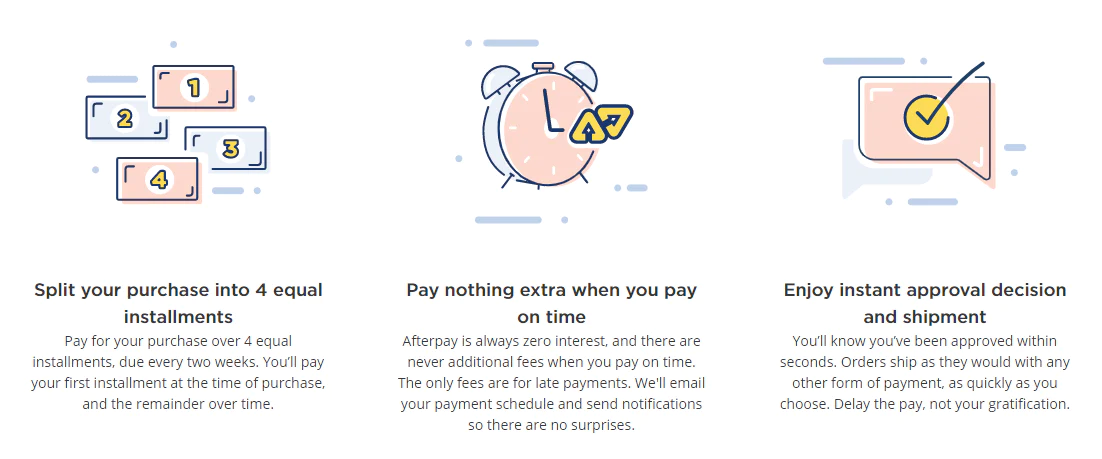

Afterpay allows customers to make purchases from participating retailers and pay for them in four equal installments over a six-week period. The process is seamless and straightforward, making it an appealing option for consumers looking for flexible payment options.

Here’s a step-by-step breakdown of how Afterpay works:

- Customer selects Afterpay at checkout: When shopping online or in-store, customers have the option to select Afterpay as their payment method during the checkout process. This option is usually displayed alongside other payment methods, such as credit cards or PayPal.

- Account creation or login: New customers are required to create an Afterpay account, providing their personal and payment information. Returning customers can simply log in to their existing accounts.

- Payment authorization: Afterpay performs a quick credit check to determine the customer’s eligibility. This process does not involve a hard inquiry that affects the customer’s credit score, making it an attractive feature for many.

- First installment payment: At the time of purchase, the customer is required to pay the first installment, which is typically a quarter of the total purchase amount. This payment can be made using a debit or credit card.

- Remaining installments: Over the next six weeks, the customer will be automatically charged in three additional installments, each two weeks apart. The remaining installments are also a quarter of the total purchase amount.

- Automatic payments: Afterpay securely stores the customer’s payment information and initiates the subsequent installment payments automatically. Customers are notified in advance of the payment dates and can manage their payments through the Afterpay mobile app or website.

It’s important to note that Afterpay assumes the risk of any unpaid installments, taking on the responsibility of collecting payment from the customer. This allows retailers to receive the full purchase amount upfront, minus any applicable fees.

Now that we have a clear understanding of how Afterpay works, let’s explore the fees and charges that retailers should be aware of when using this service.

Afterpay’s fees and charges for retailers

While Afterpay can be a convenient payment option for customers, it’s essential for retailers to understand the fees and charges associated with using this service. Let’s take a closer look at the costs involved:

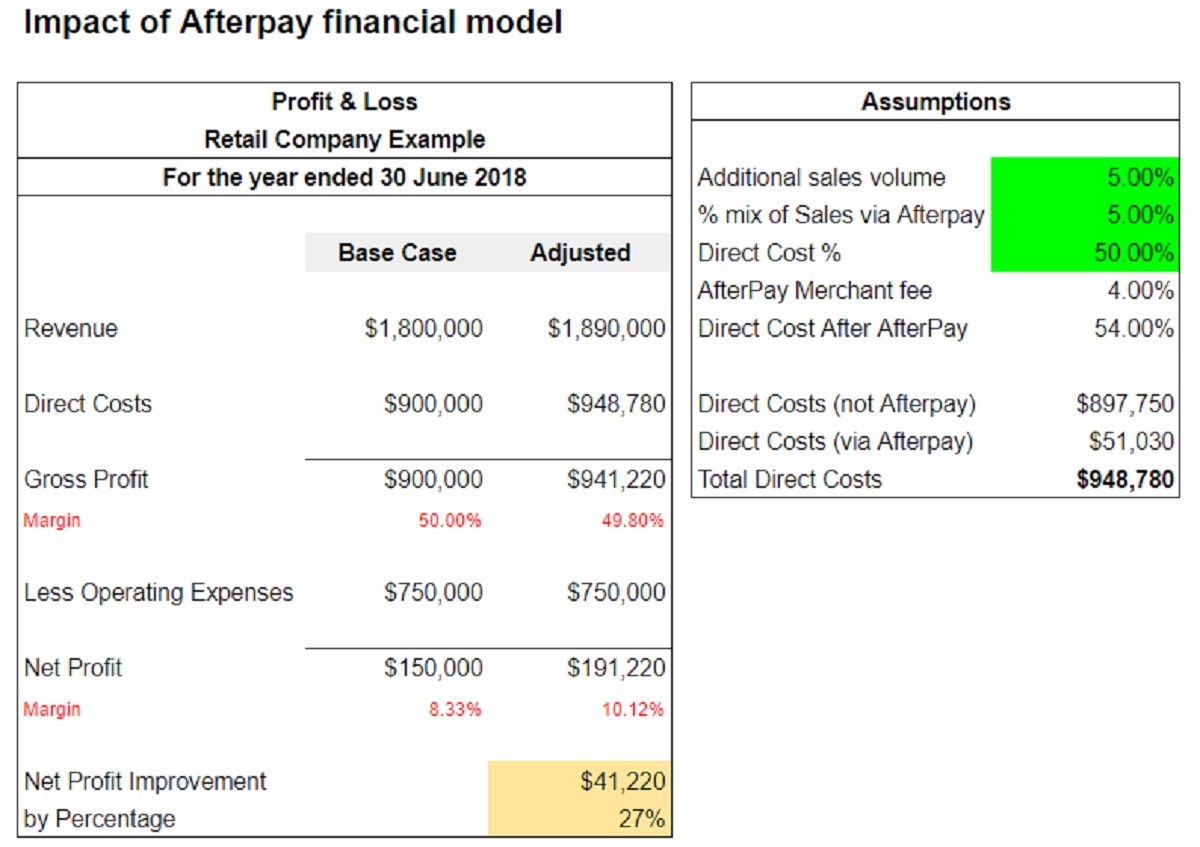

1. Merchant service fees: Afterpay charges retailers a merchant service fee, which is a percentage of the total transaction value. This fee covers the cost of processing payments and managing the Afterpay platform. The exact percentage varies depending on the retailer’s agreement with Afterpay. It’s important to factor in this fee when determining the profitability of each sale.

2. Late payment fees: If customers fail to make their installment payments on time, Afterpay may impose late payment fees. These fees are not directly charged to retailers; however, they can indirectly impact the retailer if customers encounter financial difficulties and struggle to make timely payments. It’s crucial for retailers to communicate Afterpay’s terms and conditions clearly to customers to minimize the risk of late payments.

3. Risk and fraud management fees: To protect against fraudulent transactions, Afterpay employs risk and fraud management systems. As part of these measures, retailers may incur risk and fraud management fees. These fees cover the costs associated with monitoring and preventing fraudulent activities. While these fees may seem like an added expense, they help safeguard retailers from potential losses due to fraudulent transactions.

4. Additional charges and costs: In addition to the fees mentioned above, retailers should also consider any additional charges and costs that may arise from using Afterpay. These can include fees for chargebacks, refunds, and disputes. It is crucial for retailers to carefully review the terms and conditions set by Afterpay and assess the potential impact on their business operations and finances.

By understanding and accounting for these fees and charges, retailers can make informed decisions about whether integrating Afterpay into their payment options aligns with their business goals and financial capabilities. It’s essential to evaluate the potential benefits of increased sales and customer satisfaction against the costs incurred.

Now that we’ve discussed Afterpay’s fees and charges for retailers, let’s explore some additional considerations that retailers should keep in mind when using this service.

Merchant service fees

One of the key fees that retailers need to consider when partnering with Afterpay is the merchant service fee. This fee is charged by Afterpay for the use of their payment platform and services. Here’s everything you need to know about merchant service fees:

Percentage-based fee: The merchant service fee charged by Afterpay is typically a percentage of the total transaction value. The exact percentage may vary depending on factors such as industry, sales volume, and agreement terms between the retailer and Afterpay. It’s important to carefully review the terms of the agreement to have a clear understanding of the applicable percentage for your business.

Transaction value impact: The merchant service fee directly affects the profitability of each sale made through Afterpay. As the fee is based on the transaction value, higher-priced items will incur higher fees, while lower-priced items will have lower fees. Retailers should carefully evaluate how this fee impacts their pricing strategy and sales margins.

Integration and maintenance costs: In addition to the percentage-based fee, retailers may also need to consider any integration or maintenance costs associated with Afterpay. Implementing Afterpay into an online store may require technical setup and ongoing maintenance, which could incur additional expenses. It’s important to factor in these costs when evaluating the overall financial impact of the merchant service fee.

Fee negotiation: Depending on the retailer’s size, industry, and sales volume, there may be room for negotiation with Afterpay regarding the merchant service fee. Large retailers with substantial sales volumes may be able to negotiate more favorable fee structures. It’s worth exploring the possibility of negotiating the fee to optimize the costs associated with using Afterpay.

Comparing fees with other payment options: As a retailer, it’s essential to compare the merchant service fees charged by Afterpay with other available payment options. Consider the fees associated with traditional credit card processing or other buy-now-pay-later services. By comparing these fees, you can assess which payment method offers the most cost-effective solution for your business.

Understanding the merchant service fees imposed by Afterpay is crucial when deciding whether to integrate their payment platform into your business. By carefully evaluating these fees and considering their impact on your profitability, you can make an informed decision that aligns with your financial goals.

Now that we’ve explored merchant service fees, let’s continue with other important considerations for retailers using Afterpay.

Late payment fees

While Afterpay provides a convenient payment option for customers, there is a risk of late payments. Late payment fees are one of the important considerations for retailers when partnering with Afterpay. Here’s what you need to know:

Customer responsibility: Afterpay expects customers to make their installment payments on time. However, in some cases, customers may encounter financial difficulties or forget to make a payment within the specified timeframe.

Impacts on retailers: Late payment fees are not directly charged to retailers. However, if customers fail to make timely payments, it can indirectly affect the retailer’s cash flow and profitability. Retailers rely on receiving the full purchase amount upfront, which may be jeopardized if payments are delayed or missed.

Risk mitigation: To mitigate the risk of late payments, it’s crucial for retailers to clearly communicate Afterpay’s terms and conditions to customers. This includes highlighting the consequences of late payments, such as the potential for additional fees. By educating customers about their payment obligations, retailers can minimize the occurrence of late payments and associated risks.

Customer support: Afterpay provides customer support services to help customers understand their payment obligations and assist with any payment-related issues. Encouraging customers to reach out to Afterpay’s customer support can help resolve payment difficulties and reduce the number of late payments.

Mitigating impact on retailers: Retailers can take proactive steps to mitigate the impact of late payments. This can include setting up automated reminders for customers to make their payments, offering flexible payment options for customers experiencing financial difficulties, or implementing stricter eligibility criteria to ensure customers have the means to make timely payments.

Customer communication: Open and transparent communication is key when it comes to managing late payment situations. Retailers should clearly outline their expectations regarding payment deadlines and consequences in their terms and conditions. Timely communication with customers can help address late payment issues and maintain a good relationship with customers.

While Afterpay does not charge retailers late payment fees directly, it’s important to consider the potential impact of late payments on your business. By implementing strategies to encourage timely payments and actively managing late payment situations, retailers can minimize any adverse effects on cash flow and profitability.

Now that we’ve discussed late payment fees, let’s move on to explore the risk and fraud management fees imposed by Afterpay.

Risk and fraud management fees

As with any payment system, Afterpay implements measures to protect retailers and customers from potential risk and fraud. To cover the costs associated with these risk management measures, Afterpay may charge retailers risk and fraud management fees. Here’s what you need to know about these fees:

Protecting against fraudulent transactions: Afterpay invests in robust systems and technologies to identify and prevent fraudulent transactions. These measures help safeguard both retailers and customers from financial losses caused by fraudulent activities.

Fee structure: The risk and fraud management fees charged by Afterpay may be a flat fee per transaction or a percentage of the transaction value. The exact fee structure may vary based on factors such as industry, sales volume, and agreement terms with Afterpay.

Covering the costs of risk management: The risk and fraud management fees are designed to cover the costs associated with monitoring and preventing fraudulent activities. Afterpay’s investment in risk management systems helps protect retailers from potential losses due to fraudulent transactions.

Shared responsibility: While Afterpay takes on the responsibility of detecting and preventing fraud, retailers also play a role in minimizing risks. Retailers should implement their own security measures, such as verifying customer information and setting up order validation processes, to further mitigate the risk of fraudulent transactions.

Transparent reporting: Afterpay provides retailers with transparent reporting on risk and fraud-related matters. Retailers can access reports and analytics to gain insight into the potential risks associated with their Afterpay transactions. This information can help retailers make informed decisions and take appropriate actions to reduce the risk of fraud.

Collaboration with Afterpay: In the case of suspicious or fraudulent activities, retailers can collaborate with Afterpay to address and resolve any issues. Open communication and collaboration are vital in maintaining a secure payment environment and protecting both retailers and customers.

While risk and fraud management fees may be an additional cost for retailers, they contribute to the overall security and trustworthiness of the Afterpay platform. By investing in risk management measures, Afterpay aims to provide a safe and secure payment experience for retailers and their customers.

Now that we’ve explored risk and fraud management fees, let’s discuss any additional charges and costs that retailers should be aware of when using Afterpay.

Additional charges and costs

In addition to merchant service fees, late payment fees, and risk management fees, there are other potential charges and costs that retailers should consider when using Afterpay as a payment option. These additional charges can impact a retailer’s financials and should not be overlooked. Here are some important factors to keep in mind:

Chargeback fees: Chargebacks occur when a customer disputes a transaction and requests a refund through their credit card issuer. If a chargeback is filed for an Afterpay transaction, the retailer may incur chargeback fees, which can vary in amount. It’s crucial for retailers to have clear policies regarding returns and refunds to minimize the occurrence of chargebacks.

Refund fees: When a customer returns a product and receives a refund, retailers may be responsible for associated refund fees. Afterpay may charge a fee for processing the refund within their system. Retailers should factor in these fees when assessing the financial implications of offering refunds for Afterpay purchases.

Dispute resolution costs: In the event of a dispute or disagreement between a retailer and a customer, Afterpay may charge fees for dispute resolution services. These fees cover the costs incurred by Afterpay to investigate and resolve the dispute. Retailers should carefully review the terms and conditions provided by Afterpay regarding dispute resolution and associated costs.

Customization and integration expenses: While not directly imposed by Afterpay, retailers may need to invest in the customization and integration of Afterpay into their e-commerce platforms or POS systems. These expenses can include development costs, technical support, and ongoing maintenance. Retailers should consider the investment required for seamless integration and evaluate the potential ROI of offering Afterpay as a payment option.

Marketing and promotion: To leverage the benefits of Afterpay fully, retailers may need to allocate resources for marketing and promotion. Successfully promoting Afterpay as a payment option can attract new customers and increase sales, but it may also require additional advertising and promotional expenses.

Considering these additional charges and costs is vital for retailers to make informed decisions about integrating Afterpay into their business operations. It’s recommended to carefully review the terms and conditions provided by Afterpay and assess how these charges may impact the overall profitability and financial health of the business.

Now that we’ve covered the various fees and charges associated with Afterpay, let’s move on to discuss other important considerations that retailers should keep in mind when using this payment option.

Other considerations for retailers

While understanding the fees and charges associated with Afterpay is crucial, there are other important considerations that retailers should keep in mind when deciding whether to integrate Afterpay into their business. Here are some key factors to consider:

Customer demand: Assessing customer demand for alternative payment options like Afterpay is essential. Research customer preferences and buying behaviors to determine whether offering Afterpay aligns with your target audience’s needs. This will help ensure that you’re providing a payment method that resonates with your customers and drives sales.

Integration and compatibility: Retailers need to evaluate the compatibility of Afterpay with their existing payment infrastructure. Determine whether Afterpay integrates seamlessly with your e-commerce platform or point-of-sale system. Proper integration is essential to ensure a smooth checkout process for customers and accurate transaction tracking for retailers.

Customer experience: Consider the impact of offering Afterpay on the overall customer experience. By adding Afterpay as a payment option, retailers can enhance convenience and flexibility for customers. However, it’s important to ensure that the integration of Afterpay doesn’t negatively affect other aspects of the customer journey, such as shipping, returns, or customer support.

Financial implications: Evaluate the financial implications of using Afterpay for your business. Consider the potential increase in sales volume and average order value that Afterpay can generate. Compare this with the fees and costs associated with using Afterpay to determine the overall impact on your bottom line.

Competitive advantage: Determine if offering Afterpay gives your business a competitive advantage in your industry. Research your competitors to understand whether they already offer Afterpay or similar buy-now-pay-later options. Assessing your competitive landscape will help you make an informed decision about integrating Afterpay into your business strategy.

Brand reputation: Consider how offering Afterpay may impact your brand reputation. Afterpay is associated with convenience and flexibility, and incorporating it into your payment options can enhance your brand image. However, ensure that the terms and conditions of Afterpay align with your brand values and don’t compromise your customer relationships.

By considering these factors, retailers can make well-informed decisions about incorporating Afterpay into their business. It’s important to weigh the benefits and costs, analyze market demand, and align the integration with your overall business strategy.

Now that we’ve explored the various considerations for retailers, let’s wrap up our discussion.

Conclusion

Afterpay offers a convenient payment option for customers, allowing them to make purchases and pay in installments without traditional credit checks or interest charges. However, retailers need to carefully consider the fees and charges associated with using Afterpay to ensure it aligns with their financial goals and profitability.

We discussed the various fees retailers may encounter when utilizing Afterpay. Merchant service fees, late payment fees, and risk management fees are important factors to evaluate, as they directly impact the profitability of each sale. Retailers should also be aware of additional charges like chargeback fees, refund fees, dispute resolution costs, and customization expenses.

Considering these fees and costs is crucial, but it’s equally important to assess other factors. Retailers should evaluate customer demand, integration compatibility, customer experience, financial implications, competitive advantage, and brand reputation when deciding whether to integrate Afterpay into their business operations.

By thoroughly understanding the fees and considering these factors, retailers can make informed decisions on whether Afterpay is the right choice for their business. While Afterpay can increase sales and customer loyalty, it’s crucial to weigh the costs involved against the potential benefits.

It’s recommended that retailers carefully review the terms and conditions provided by Afterpay and determine the feasibility and impact on their business before proceeding with integration. By examining all aspects and making strategic decisions, retailers can leverage Afterpay as a valuable payment option that enhances customer experiences and drives business growth.