Buy Now, Pay Later (BNPL) has been making waves in the world of consumer finance, offering an alternative way to make purchases without upfront payment. But is it simply another form of debt in disguise?

Key Takeaway

Buy Now, Pay Later (BNPL) has emerged as a popular payment option, offering consumers a flexible and convenient way to make purchases. However, it’s essential to approach BNPL with caution and ensure responsible borrowing practices to avoid falling into a debt trap. Regulators and businesses alike must find a balance between innovation and safeguarding consumer interests to ensure the sustainability of BNPL as a payment solution.

Exploring the Phenomenon of BNPL

BNPL has gained popularity among consumers, particularly millennials, who are looking for flexible payment options. The concept is simple: customers can buy a product now and pay for it in installments over a set period of time. This eliminates the need for credit cards or traditional loans and offers more convenience and flexibility in managing one’s finances.

With a rise in BNPL providers such as Afterpay, Klarna, and Affirm, it’s evident that the demand for this payment method is strong. These companies partner with retailers to offer BNPL as a checkout option, making it an attractive and accessible choice for consumers.

Is BNPL Just Another Form of Debt?

While BNPL presents itself as a convenient and interest-free payment solution, critics argue that it could lead individuals into a debt trap. The allure of deferred payments may entice consumers to overspend or overlook their budgeting capabilities. In this way, BNPL can be seen as a new avenue for accumulating debt.

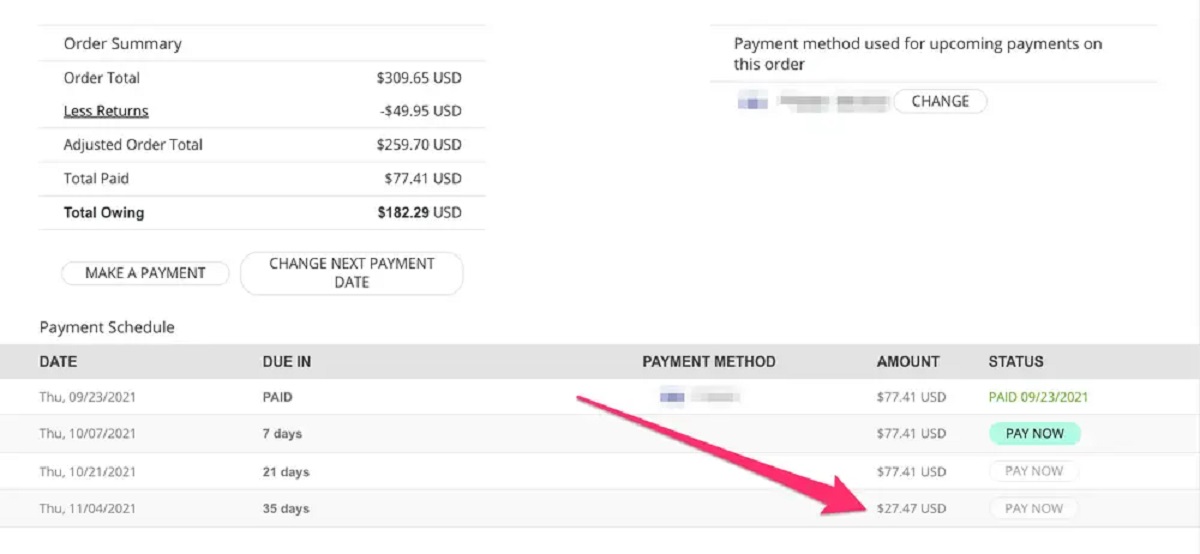

With BNPL, the repayment process is simplified, often requiring only a few clicks during the checkout process. However, borrowers must be cautious about the terms and conditions associated with BNPL services. Late payments or missed installments could result in interest charges or penalties, adding to the overall owed amount.

It’s important for consumers to take a disciplined approach when it comes to utilizing BNPL services. Understanding the impact on one’s financial wellbeing and ensuring the ability to repay on time is crucial to avoid falling into a debt cycle.

The Future of BNPL

Despite the concerns surrounding BNPL, it has undoubtedly reshaped the way people make purchases. Retailers are embracing this trend, recognizing the potential to attract customers and boost sales. The convenience and flexibility that BNPL offers make it an appealing option for both consumers and businesses.

Regulators are beginning to take notice of the growing popularity of BNPL and are considering introducing guidelines to protect consumers. Striking a balance between innovation and consumer protection will be crucial to ensure the long-term viability of this payment method.