Introduction

Welcome to the world of Ripple, a revolutionary technology that is transforming cross-border payments. In today’s globalized economy, traditional payment methods often fall short, causing delays, high fees, and inefficiencies. Ripple offers a solution to these problems through its innovative software and XRP cryptocurrency.

Ripple was created in 2012 and has quickly gained attention and adoption in the financial industry. With its cutting-edge technology, Ripple aims to revolutionize international transfers, making them faster, more affordable, and more secure.

This article will provide an overview of Ripple, explain how it addresses the problems with traditional cross-border payments, discuss the value of Ripple’s XRP cryptocurrency, explore its use cases and partnerships, and analyze its impact on the financial industry. We will also delve into the criticisms and challenges faced by Ripple as it strives to disrupt the traditional banking system.

Before we dive into the details, it’s important to note that Ripple is not just another cryptocurrency. While it is often associated with XRP, Ripple’s underlying technology, known as the RippleNet, is its true innovation. This decentralized global network enables financial institutions to connect and transact with each other seamlessly.

Now, let’s explore how Ripple tackles the issues with traditional cross-border payments and why it has the potential to reshape the financial landscape.

Ripple: An Overview

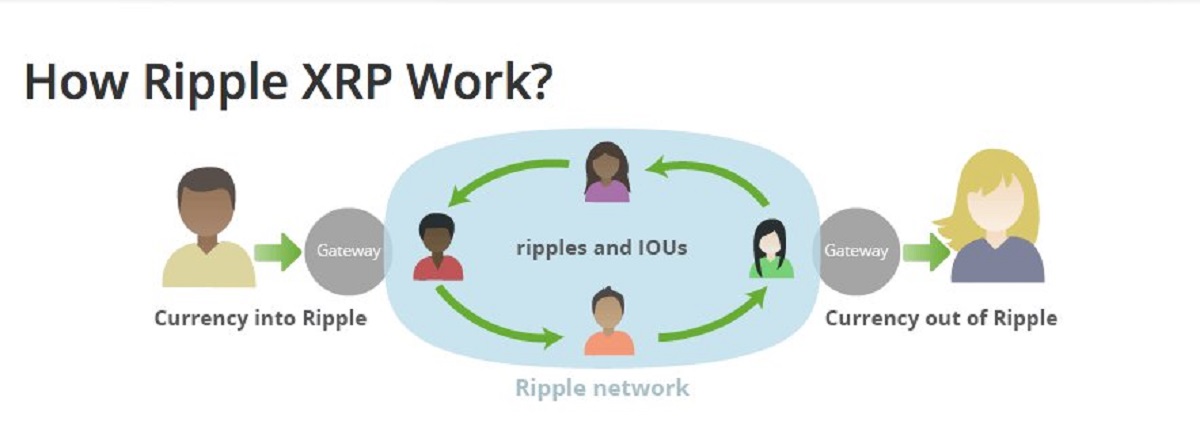

Ripple is not just a cryptocurrency; it is an entire ecosystem designed to facilitate fast, secure, and cost-effective cross-border transactions. It operates on the premise that money should be able to move as quickly as information does in the digital age.

Ripple’s main innovation is its decentralized global network, RippleNet. RippleNet connects banks, payment providers, and digital asset exchanges, enabling them to transfer funds seamlessly and efficiently. The network uses a consensus algorithm and a distributed ledger to validate and settle transactions within seconds.

At the heart of RippleNet is the XRP Ledger, a digital ledger that serves as the backbone of Ripple’s ecosystem. The XRP Ledger is open-source and decentralized, meaning no single entity has control over it. This ensures transparency, security, and trust among participants in the network.

Ripple aims to bridge the gap between traditional banking systems and the world of cryptocurrencies. Unlike Bitcoin and other cryptocurrencies, which operate outside the traditional financial system, Ripple collaborates with banks and financial institutions. This strategy has helped Ripple gain widespread acceptance and adoption in the financial industry.

One of the key features of RippleNet is its ability to facilitate real-time gross settlement (RTGS) of funds. This means that transactions can be settled instantly, eliminating the need for intermediaries and resulting in faster and more efficient cross-border payments.

Furthermore, Ripple offers an alternative to the outdated SWIFT (Society for Worldwide Interbank Financial Telecommunication) system, which is commonly used for international transfers. SWIFT transfers can take several days to complete and often come with high fees. In contrast, Ripple’s technology allows for near-instantaneous transfers at a fraction of the cost.

Overall, Ripple’s mission is to revolutionize the way money is moved globally. By harnessing the power of blockchain technology and leveraging its partnerships with financial institutions, Ripple has positioned itself as a major player in the fintech industry.

The Problem with Traditional Cross-Border Payments

Traditional cross-border payments have long been plagued by inefficiencies, high fees, and slow transaction times. This has become increasingly problematic in today’s globalized economy, where businesses and individuals rely on seamless and timely international transactions.

One of the major issues with traditional cross-border payments is the reliance on a complex web of intermediaries. When a payment is made from one country to another, it typically goes through multiple banks, each of which may charge fees and take time to process the transaction. This results in delays and added costs, making international transfers slow and expensive.

Another problem is the lack of transparency in the traditional system. When a payment is sent overseas, it can be difficult for both the sender and the recipient to track the progress of the transaction. This lack of visibility leaves room for errors and disputes, further complicating the cross-border payment process.

The outdated technology used by banks and other financial institutions is yet another challenge. Many traditional payment systems rely on legacy infrastructure, making them slow and prone to errors. This not only hampers the speed of transactions but also increases the risk of fraud and cyberattacks.

Furthermore, traditional cross-border payments are subject to varying regulatory frameworks and compliance requirements in different countries. This adds complexity to the process and increases the chances of delays and errors due to manual intervention.

Lastly, the high cost of cross-border payments is a significant barrier. Traditional methods often involve hefty fees, including foreign exchange fees and intermediary fees, which can eat into the amount being transferred and affect the overall profitability of international transactions.

These challenges have created a strong demand for a solution that can streamline cross-border payments, reduce costs, enhance transparency, and improve the speed of transactions. This is where Ripple comes into play.

How Ripple Addresses the Problem

Ripple addresses the challenges of traditional cross-border payments through its innovative technology and collaborative approach with financial institutions. Here’s how Ripple tackles each of the problems:

1. Intermediary Elimination: Ripple’s technology allows for direct transfers between financial institutions, eliminating the need for multiple intermediaries. This streamlines the payment process, reduces costs, and improves the speed of transactions.

2. Transparency: Ripple provides real-time tracking and visibility of transactions through its decentralized ledger, the XRP Ledger. This ensures transparency and accountability, allowing both senders and recipients to monitor the progress of their payments.

3. Modern Technology: Ripple’s technology is built on blockchain, a secure and decentralized system that minimizes the risk of fraud and cyberattacks. By leveraging this modern technology, Ripple improves the security and reliability of cross-border payments.

4. Regulatory Compliance: Ripple works closely with regulatory authorities and financial institutions to ensure compliance with local regulations. This helps to streamline the cross-border payment process and reduce the chances of delays or errors due to compliance issues.

5. Lower Costs: Ripple’s technology significantly reduces the cost of cross-border payments compared to traditional methods. By eliminating intermediaries, optimizing liquidity, and using the XRP cryptocurrency as a bridge currency, Ripple enables cost-effective international transfers.

6. Speed and Efficiency: Ripple’s technology enables near-instantaneous settlement of cross-border payments. This eliminates the days or even weeks of waiting time that are typically associated with traditional transfers, providing businesses and individuals with faster and more efficient transactions.

Ripple’s approach of collaborating with financial institutions sets it apart from other cryptocurrencies. By partnering and integrating with banks, Ripple has gained widespread acceptance and has the potential to transform the global payments landscape.

By addressing these pain points, Ripple offers a compelling solution to the challenges faced by traditional cross-border payments, empowering businesses and individuals to send and receive money across borders in a faster, more affordable, and more secure manner.

The Value of Ripple’s XRP Cryptocurrency

Ripple’s XRP cryptocurrency plays a crucial role in its ecosystem, serving as a bridge currency and enhancing the efficiency of cross-border payments. XRP offers several key benefits and value propositions:

1. Liquidity

XRP serves as a source of liquidity in Ripple’s network. It allows financial institutions to facilitate instant transfers between different fiat currencies, minimizing the need for pre-funded nostro and vostro accounts. This reduces capital requirements and frees up liquidity for financial institutions, making cross-border payments more efficient and cost-effective.

2. Speed

Utilizing XRP as a bridge currency enables rapid settlement of cross-border transactions. Compared to traditional methods, which require multiple intermediary banks and can take days to complete, XRP transactions settle within seconds. This speed revolutionizes the cross-border payment industry, providing businesses and individuals with near-instantaneous fund transfers.

3. Cost Savings

Using XRP for cross-border payments can yield significant cost savings. The speed of transactions reduces the need for costly intermediaries, lowering fees and associated foreign exchange costs. Additionally, the efficiency of Ripple’s network, combined with low transaction fees for XRP, results in cost-effective cross-border payments compared to traditional banking methods.

4. Stability

XRP has earned a reputation for its stability, making it an attractive asset for financial institutions and individual investors alike. With a finite maximum supply of 100 billion coins, XRP offers a level of predictability and control, mitigating the volatility often associated with other cryptocurrencies.

5. Integration

XRP’s integration into Ripple’s ecosystem and partnerships with banks and financial institutions worldwide provide it with substantial utility and potential for adoption. As more institutions join the RippleNet network, the demand for XRP as a bridge currency increases, driving its value proposition and utility in the cross-border payment space.

6. Global Accessibility

XRP facilitates seamless cross-border transactions, making it accessible to individuals and businesses around the world. Through its ecosystem, Ripple aims to democratize access to financial services, bridging the gap between traditional banking systems and emerging economies.

Overall, the value of Ripple’s XRP cryptocurrency extends beyond speculation and trading. Its integration into Ripple’s network and its role as a bridge currency have the potential to revolutionize cross-border payments, delivering benefits such as liquidity, speed, cost savings, stability, integration, and global accessibility.

Ripple’s Use Cases and Partnerships

Ripple’s technology has found application in various industries beyond cross-border payments. Its use cases and partnerships demonstrate the versatility and potential of Ripple’s solutions:

1. Cross-Border Payments

The primary use case for Ripple’s technology is facilitating fast, secure, and cost-effective cross-border payments. By connecting financial institutions through its RippleNet network, Ripple enables seamless and near-instantaneous transfers of funds across different currencies, eliminating intermediaries and reducing costs.

2. Remittances

Ripple’s technology has proven particularly valuable in the remittance market, where migrants send money back to their home countries. By leveraging RippleNet and XRP, remittance service providers can offer faster and more affordable transfers, benefiting both senders and recipients.

3. Money Transfers for Businesses

Ripple’s technology is also being adopted by businesses for international money transfers. By utilizing Ripple’s network, companies can streamline their payment processes, reduce fees, and improve cash flow management, enhancing their global business operations.

4. Financial Institutions

Ripple has established partnerships with numerous financial institutions worldwide, including banks, payment providers, and remittance companies. These partnerships enable institutions to leverage Ripple’s technology and expand their cross-border payment capabilities, offering improved services to their customers.

5. Central Banks and Digital Currencies

Ripple is actively exploring partnerships with central banks to help them develop and pilot central bank digital currencies (CBDCs). By leveraging Ripple’s technology, central banks have the opportunity to introduce digital currencies that can enhance payment systems and financial inclusion.

6. Real Estate and Supply Chain

Ripple’s technology has potential applications beyond finance. It can be integrated into real estate transactions, enabling fast and transparent property transfers. Additionally, Ripple’s distributed ledger technology can provide visibility and efficiency in supply chain management, facilitating secure and reliable tracking of goods.

Ripple’s growing list of partnerships reflects the industry’s recognition of its technology’s potential. Notable partnerships include collaborations with global financial institutions such as American Express, Santander, and Standard Chartered. These partnerships demonstrate Ripple’s ability to gain the trust and adoption of established players in the financial sector.

As Ripple continues to expand its network and forge new partnerships, its use cases will likely diversify and grow. By leveraging advanced technology and collaboration with industry leaders, Ripple aims to revolutionize not only cross-border payments but also various other sectors, driving innovation and efficiency in global transactions.

Ripple’s Impact on the Financial Industry

Ripple’s emergence has had a profound impact on the financial industry, revolutionizing cross-border payments and challenging traditional banking systems. Here are some of the key ways in which Ripple has influenced the financial landscape:

1. Enhanced Efficiency

Ripple’s technology has significantly improved the efficiency of cross-border payments. By reducing the number of intermediaries and facilitating near-instantaneous transactions, Ripple has eliminated the delays and high costs associated with traditional methods. This has made international transfers faster, more affordable, and more accessible to businesses and individuals worldwide.

2. Increased Competition

Ripple’s entry into the financial industry has created healthy competition, challenging the monopoly of traditional payment systems, such as SWIFT. Financial institutions now have alternative options for cross-border payments, forcing them to improve their services to remain competitive. This has ultimately led to better customer experiences and more innovative solutions in the global payments space.

3. Improved Financial Inclusion

One of Ripple’s goals is to enhance financial inclusion by providing access to global payment networks for underserved populations. Through partnerships with financial institutions and remittance service providers, Ripple has facilitated affordable international transfers for individuals in emerging economies, allowing them to participate in the global economy and access essential financial services.

4. Adoption of Blockchain Technology

Ripple’s success has brought greater attention and adoption of blockchain technology within the financial industry. Financial institutions are now exploring the benefits of distributed ledger technology for various use cases beyond cross-border payments. This adoption has the potential to transform multiple aspects of the financial sector, including settlements, identity verification, and trade finance.

5. Ripple’s Influence on Regulations

Ripple’s growth and partnerships have driven discussions and regulatory developments around digital assets and cryptocurrencies. Regulators have recognized the potential benefits and risks associated with these technologies, prompting the establishment of guidelines and frameworks to ensure consumer protection and market stability. Ripple’s influence has played a role in shaping the evolving regulatory landscape.

6. Collaboration with Financial Institutions

Ripple’s collaborative approach with financial institutions has reshaped the relationship between traditional banks and cryptocurrencies. The partnerships forged by Ripple demonstrate the industry’s acceptance of blockchain technology as a viable solution for financial transactions. This collaboration has positioned Ripple as a respected player in the financial ecosystem, bridging the gap between traditional banking systems and cutting-edge fintech innovations.

In summary, Ripple’s impact on the financial industry cannot be understated. Its technology has brought efficiency, competition, and financial inclusion to cross-border payments. Ripple’s success has also increased adoption of blockchain technology and influenced regulatory developments. Collaboration with financial institutions and partnerships with industry leaders have solidified Ripple’s role as a key player in reshaping the future of global financial transactions.

Criticisms and Challenges Faced by Ripple

While Ripple has made significant strides in revolutionizing cross-border payments, it has also faced criticisms and encountered challenges along the way. It is important to examine these criticisms to gain a comprehensive understanding of Ripple’s position in the financial industry:

1. Centralization Concerns

One of the main criticisms leveled against Ripple is its perceived centralization. As the majority of XRP tokens are held by Ripple Labs, some argue that this concentration of ownership undermines the decentralization ethos of cryptocurrencies. Ripple has taken steps to address these concerns, such as establishing escrow accounts for the release of XRP, but the centralization debate continues.

2. XRP Token Utility

Another criticism revolves around the utility of XRP as a token within Ripple’s ecosystem. While Ripple has successfully partnered with many financial institutions, the use of XRP within these partnerships varies. Some institutions choose to integrate Ripple’s technology without necessarily utilizing XRP, leading to questions about the long-term demand and value of the token.

3. Regulatory Environment

The regulatory landscape surrounding cryptocurrencies remains uncertain and evolving. Ripple has faced legal challenges and scrutiny regarding the classification of XRP as a security. Regulatory clarity is essential for Ripple’s widespread adoption and acceptance by financial institutions, and ongoing legal proceedings add a layer of uncertainty to its future prospects.

4. Competing Technologies

Ripple operates in a competitive landscape with other blockchain-based solutions, such as SWIFT’s Global Payments Innovation (gpi) and other payment providers exploring the use of digital assets for cross-border payments. These competing technologies pose challenges for Ripple’s market share and require constant innovation to maintain its position as a leader in the field.

5. Resistance from Incumbents

The traditional banking sector is known for its resistance to change, and ripple’s disruptive technology may face pushback from incumbents. Established financial institutions may be hesitant to fully embrace Ripple’s technology due to concerns over security, regulatory compliance, and potential disruption to their existing systems.

6. Volatility and Perception

The volatility and speculative nature commonly associated with cryptocurrencies can create challenges for Ripple’s reputation and adoption. The perception of XRP as a speculative investment rather than a utility token for cross-border payments may lead to skepticism from potential institutional partners or users looking for stability in their financial transactions.

It is important to note that despite these challenges and criticisms, Ripple has made significant progress in reshaping the financial industry. It continues to forge partnerships with financial institutions, address centralization concerns, and navigate the evolving regulatory landscape. As it overcomes these obstacles, Ripple has the potential to solidify its position as a leading player in the global payments ecosystem.

Conclusion

Ripple has emerged as a game-changer in the financial industry, revolutionizing cross-border payments and challenging traditional banking systems. By leveraging its innovative technology and collaborative approach with financial institutions, Ripple has addressed the longstanding problems of inefficiencies, high costs, and delays associated with traditional methods of international transfers.

Ripple’s decentralized global network, RippleNet, has enabled financial institutions to connect and conduct seamless transactions with one another, eliminating the need for multiple intermediaries. Through the use of its native cryptocurrency, XRP, Ripple has provided liquidity, speed, and cost savings to cross-border payments, propelling it to become a viable alternative to traditional banking systems.

Furthermore, Ripple’s impact extends beyond cross-border payments, with its technology finding applications in remittances, business money transfers, and even real estate and supply chain management. Its partnerships with financial institutions and exploration of central bank digital currencies demonstrate Ripple’s influence and potential to reshape the financial industry.

Despite its success, Ripple has faced criticism and challenges. Concerns about centralization, the utility of XRP, regulatory uncertainties, and competition from other technologies pose hurdles to its widespread adoption. However, Ripple has consistently worked to address these issues and adapt to the evolving landscape of the financial sector.

As Ripple continues to innovate and expand its network, its impact on the financial industry is undeniable. It has brought efficiency, competition, and financial inclusion to cross-border payments, spurring the adoption of blockchain technology and influencing regulatory developments. Collaboration with financial institutions and partnerships with industry leaders have solidified Ripple’s position as a key player in reshaping the future of global financial transactions.

In conclusion, Ripple’s disruptive technology, collaborative approach, and focus on solving real-world problems make it a significant player in the ongoing evolution of the financial industry. As it navigates the challenges, Ripple has the potential to further transform cross-border payments and drive innovation, paving the way for a more efficient and inclusive global financial system.