What Is a NFC Payment?

NFC, which stands for Near Field Communication, is a technology that allows devices to communicate with each other wirelessly, simply by being in close proximity. NFC payments refer to the use of this technology to make contactless transactions, allowing consumers to make purchases by simply tapping their NFC-enabled smartphones or cards on a payment terminal.

NFC payments rely on a chip embedded in the device or card, which securely stores the user’s payment information. When the device or card is brought close to a payment terminal, the NFC chip communicates with the terminal, initiating the payment transaction.

This technology has gained popularity in recent years due to its convenience and speed. NFC payments eliminate the need to carry physical cash or swipe a card, making the checkout process seamless and efficient.

One of the key advantages of NFC payments is that they are contactless. Unlike traditional payment methods, which require physical contact with a card or terminal, NFC payments can be completed with a simple tap. This not only saves time but also reduces the risk of germs being spread, especially in the current era of heightened hygiene awareness.

NFC payments are also considered secure. The technology uses encryption and tokenization to protect the user’s sensitive information. Each transaction generates a unique code, ensuring that the user’s payment details remain safe and are not exposed to potential fraud. Additionally, NFC payments often require biometric authentication, such as a fingerprint or facial recognition, adding an extra layer of security.

As contactless payments continue to gain traction, NFC technology is expected to play a significant role in the future of digital transactions. Its versatility and simplicity make it an ideal solution for various payment scenarios, including in-store purchases, public transportation fares, and even peer-to-peer transfers.

How Does NFC Payment Work?

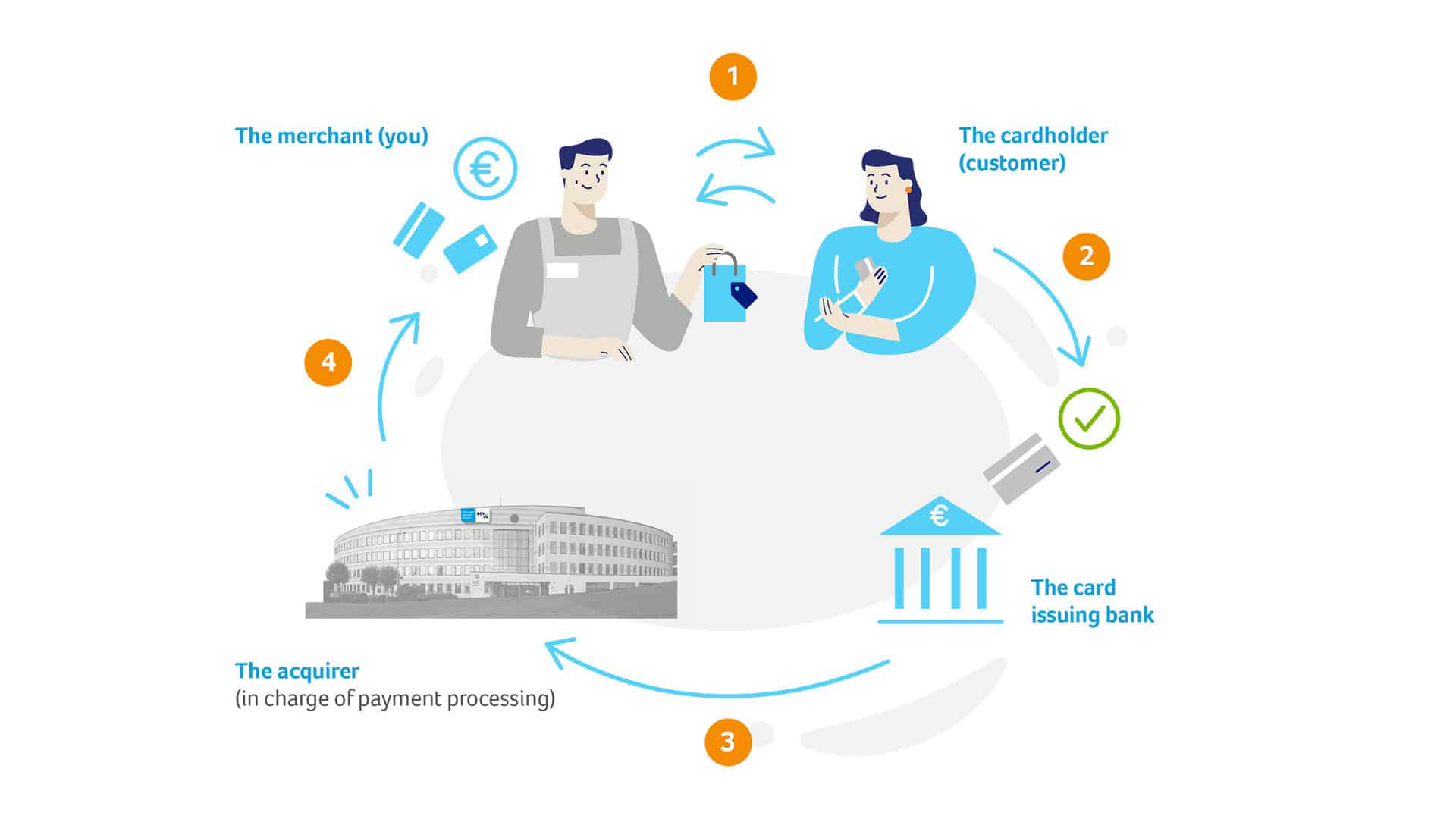

NFC payment works through a combination of hardware and software that enables secure communication between devices involved in a transaction. Here’s a step-by-step breakdown of how NFC payment typically works:

- Device Initialization: To initiate an NFC payment, both the sender’s and the recipient’s devices must have NFC capabilities and the appropriate payment app installed. The sender’s device is usually a smartphone or a contactless-enabled payment card.

- Transaction Setup: The sender opens the payment app and selects the payment method they want to use, such as a credit or debit card. They may also have the option to choose between different payment sources linked to their account.

- Device Proximity: The sender brings their NFC-enabled device close to the recipient’s payment terminal, which is equipped with an NFC reader. The devices need to be within a few centimeters of each other to establish a connection.

- Data Transfer: Once the connection is established, the sender’s device securely transfers the payment information to the recipient’s terminal using NFC communication. The details typically include the payment amount, the sender’s account information, and a transaction identifier.

- Authentication: The recipient’s payment terminal validates the received payment information and communicates with the respective payment network or service provider to verify the transaction. This step ensures that the payment request is legitimate and that the sender has sufficient funds or credit available for the transaction.

- Confirmation: If the transaction is approved, the recipient’s terminal sends a confirmation signal back to the sender’s device. The payment app on the sender’s device then displays a confirmation message, indicating that the transaction was successful.

- Transaction Record: Both parties involved in the transaction, the sender, and the recipient, receive a record of the transaction. The sender can view the transaction details in their payment app or account statement, while the recipient receives payment confirmation in their merchant portal or POS system.

NFC payment technology streamlines the payment process by eliminating the need for physical cards or cash. Its quick and secure nature makes it an attractive option for both consumers and businesses alike.

The Benefits of NFC Payment

NFC payment offers several benefits for both consumers and businesses. Let’s delve into some of the key advantages of using NFC technology for contactless transactions:

- Convenience: One of the primary benefits of NFC payment is its convenience. With just a simple tap, users can make payments quickly and effortlessly, eliminating the need to carry physical cash or search for cards in a wallet. This seamless and hassle-free experience saves time for both consumers and businesses.

- Speed: NFC payment transactions are lightning-fast. By leveraging the power of wireless communication, NFC-enabled devices can transmit payment data within milliseconds. Customers can breeze through checkout lines and complete transactions in seconds, resulting in improved customer satisfaction and shorter wait times.

- Enhanced Security: NFC payment technology incorporates robust security measures to protect users’ sensitive information. Transactions are encrypted and tokenized, ensuring that payment details remain secure throughout the process. Additionally, many NFC payment methods require biometric authentication, such as fingerprint or face recognition, adding an extra layer of security.

- Hygiene and Safety: In the wake of the COVID-19 pandemic, contactless payment methods have gained significant popularity due to their hygiene benefits. NFC payments eliminate the need for physical contact with payment terminals, reducing the risk of germ transmission. This touchless approach promotes a safer and more sanitary payment experience for both customers and employees.

- Versatility: NFC technology is not limited to traditional retail payments. It can be used for various applications such as public transportation fares, event ticketing, loyalty programs, and access control. This versatility makes NFC payments a convenient solution for a wide range of industries and scenarios.

- Reduced Cost: For businesses, NFC payment systems can lead to cost savings in the long run. By adopting contactless payment methods, companies can reduce the need for physical payment terminals or cash handling, lowering operational expenses and streamlining their financial processes.

Overall, NFC payment provides a convenient, secure, and efficient way to make transactions. Its widespread adoption and increasing availability make it an integral part of the evolving digital payment landscape.

Common Uses of NFC Payment

NFC payment technology has expanded beyond traditional retail transactions and has found its way into various industries and use cases. Let’s explore some of the common uses of NFC payment:

- Retail: NFC payments are widely used in brick-and-mortar stores, enabling customers to make quick and contactless payments at the point of sale. By simply tapping their NFC-enabled smartphones or cards on payment terminals, customers can complete transactions efficiently.

- Public Transportation: NFC technology is integrated into many transportation systems, allowing commuters to conveniently pay for bus, train, or subway rides. With a simple tap of their NFC-enabled devices or transit cards, passengers can access fares, eliminating the need for physical tickets or tokens.

- Access Control: NFC payment has become a popular solution for access control systems in offices, hotels, and events. NFC-enabled access cards or wristbands can be used to grant entry to authorized individuals, improving security and streamlining entry processes.

- Loyalty Programs: NFC payment is also utilized in loyalty programs. Customers can store their loyalty information or membership details on their NFC-enabled devices, making it convenient to collect and redeem rewards at participating businesses without the need for physical cards or key tags.

- Mobile Wallets: NFC payment is often integrated into mobile wallet applications. Mobile wallet platforms like Apple Pay, Google Pay, and Samsung Pay allow users to store their payment information securely on their smartphones and make contactless payments by tapping their devices on compatible payment terminals.

- Event Ticketing: NFC technology has revolutionized event ticketing by offering a secure and convenient ticketing solution. Event organizers can issue NFC-enabled tickets that attendees can easily tap on scanners for entry, eliminating the risk of counterfeit tickets.

These are just a few examples of how NFC payment is transforming various industries. As the technology continues to evolve, we can expect even more innovative applications and use cases to emerge.

NFC Payment Security

When it comes to any form of digital payment, security is of paramount importance. Fortunately, NFC payment technology incorporates several measures to ensure the security of transactions. Here are some key aspects of NFC payment security:

1. Encryption: NFC payment transactions are encrypted, which means that the payment data is encoded in a way that makes it unreadable to unauthorized parties. This encryption helps prevent eavesdropping and protects the privacy of the user’s payment information during wireless communication.

2. Tokenization: Tokenization is an additional layer of security used in NFC payment. Instead of transmitting actual payment details, such as credit card numbers, a unique token is generated for each transaction. This token acts as a representation of the payment information and is used to verify and authorize the transaction, reducing the risk of sensitive information from being intercepted or compromised.

3. Biometric Authentication: Many NFC payment methods incorporate biometric authentication, such as fingerprint or facial recognition, to ensure that only authorized users can initiate transactions. This adds an extra layer of protection by linking the payment process to the unique characteristics of the user, making it difficult for unauthorized individuals to access or misuse the user’s payment information.

4. Secure Element: NFC-enabled devices often have a dedicated hardware component called a Secure Element. This Secure Element stores sensitive payment information, such as card details or digital wallets, in an isolated and encrypted environment. It provides additional protection against unauthorized access to the payment data, even if the device itself is compromised.

5. Transaction Limits and Verification: NFC payment methods typically have transaction limits, ensuring that even if a device is lost or stolen, the potential financial loss is minimized. Additionally, some payment providers may require additional verification steps, such as a PIN or biometric authentication, for higher-value transactions, further securing the payment process.

It’s important to note that while NFC payment technology is generally considered secure, users should still follow best practices to protect their payment information. This includes keeping devices updated with the latest security patches, using strong passwords or biometric authentication methods, being cautious of phishing attempts, and regularly monitoring payment activity for any unauthorized transactions.

By incorporating encryption, tokenization, biometric authentication, and other security measures, NFC payment technology provides a secure platform for contactless transactions, giving users peace of mind when making payments with their NFC-enabled devices.

NFC Payment vs Other Payment Methods

When comparing NFC payment with other payment methods, several factors come into play, including convenience, security, acceptance, and user experience. Let’s take a look at how NFC payment stacks up against other popular payment methods:

Cash: NFC payment offers a significant advantage over cash in terms of convenience and speed. With NFC payment, there’s no need to carry physical cash or worry about making exact change. It also eliminates the hassle of counting and handling paper money and coins. Additionally, NFC payment provides a more hygienic option, especially in light of the current COVID-19 pandemic, as it reduces the need for physical contact.

Credit and Debit Cards: NFC payment provides similar convenience to traditional card payments but adds an extra layer of speed and simplicity. With NFC payment, users can tap their cards on the payment terminal instead of having to insert or swipe them. This saves time and makes the checkout process more efficient. NFC payment also offers the advantage of being contactless, reducing the risk of card skimming or stolen card information.

Mobile Wallets: NFC payment is an integral part of mobile wallet applications, such as Apple Pay, Google Pay, and Samsung Pay. These mobile wallets allow users to store their payment information securely on their smartphones and make contactless payments by simply tapping their devices on compatible payment terminals. Mobile wallets also offer additional features like loyalty program integration and in-app payments.

Online Payments: While NFC payment is primarily used for in-person transactions, online payments can also be made using NFC-enabled devices. This is typically done by tapping the device on an NFC reader or scanning an NFC tag to initiate the payment. However, for online payments, options like digital wallets or card payments are more commonly used.

QR Code Payments: QR code payments have gained popularity in recent years, especially in certain regions. While both NFC and QR code payments offer contactless transactions, NFC payment tends to be more seamless and quicker. With NFC, users simply tap their devices, whereas QR code payments require scanning a code, which can be more time-consuming and prone to errors.

Peer-to-Peer Payments: NFC payment can also be utilized for peer-to-peer transactions. Some mobile wallet apps enable users to make quick payments to friends, family, or acquaintances by tapping their devices together. This provides a convenient and secure way to transfer funds without the need for cash or physical card exchange.

In summary, NFC payment offers advantages in terms of speed, convenience, and hygiene compared to cash and traditional card payments. While other payment methods like mobile wallets, online payments, QR code payments, and peer-to-peer transfers have their own benefits, NFC payment stands out for its seamless and contactless nature, making it an increasingly popular choice for modern-day transactions.

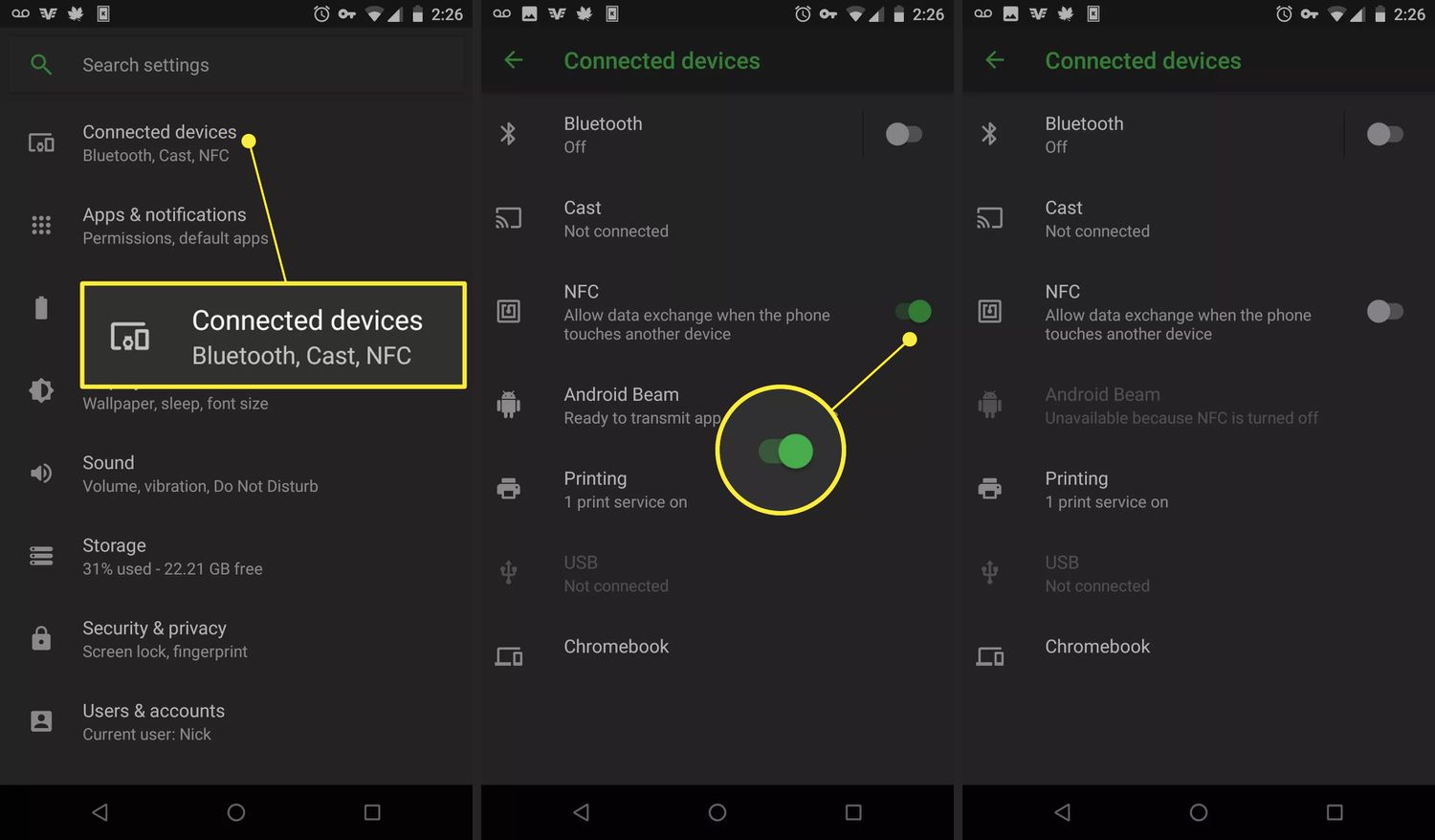

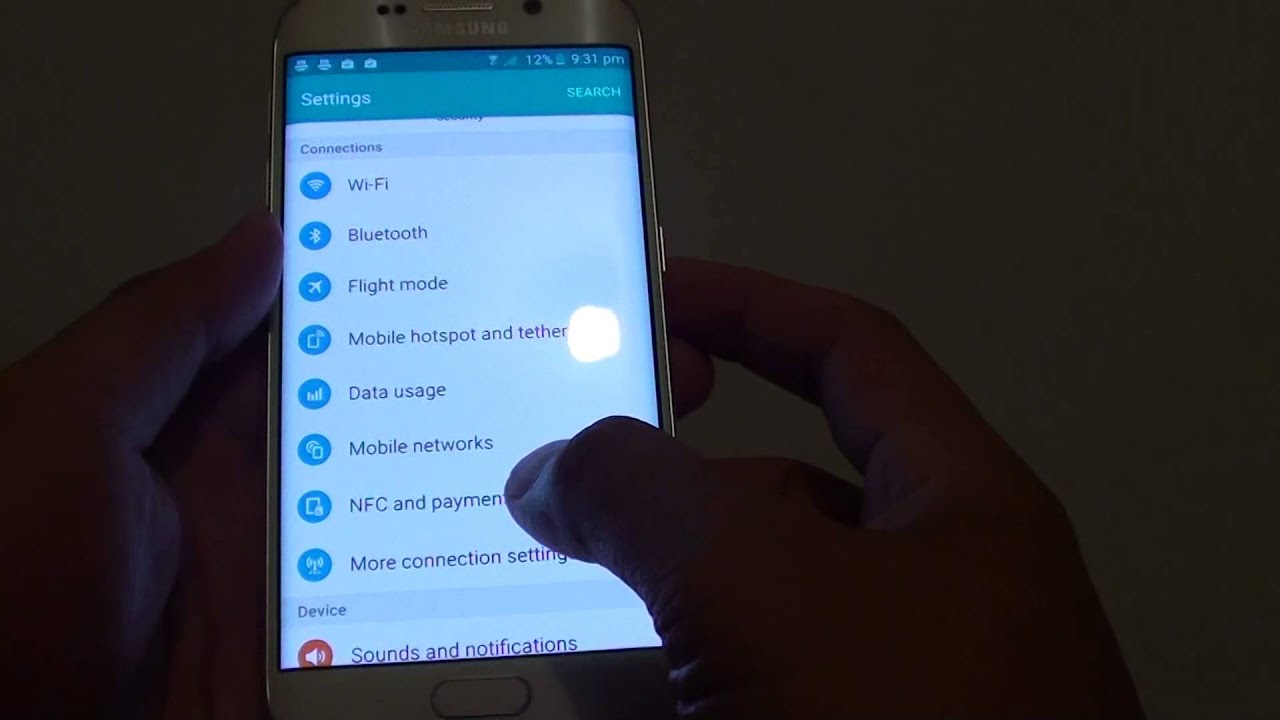

How to Set Up NFC Payment on Your Device

Setting up NFC payment on your device is a straightforward process that allows you to make contactless payments with ease. While the specific steps can vary based on your device and operating system, here are general guidelines to help you get started:

- Ensure Device Compatibility: Check if your device is NFC-enabled. Most modern smartphones and wearable devices support NFC, but it’s important to verify this capability before proceeding.

- Update your Operating System: Make sure your device’s operating system is up to date. NFC payment functionality is often included in software updates, so installing the latest version will ensure you have the necessary features and security patches.

- Find NFC Payment Apps: Identify the NFC payment apps available for your device. Depending on your region, popular options include Apple Pay, Google Pay, Samsung Pay, or specific banking apps that support NFC payments. Visit the app store on your device and search for the relevant app.

- Download and Install the App: Once you’ve found the suitable NFC payment app, download and install it on your device. Follow the on-screen instructions to set up the app, including linking it to your preferred payment method, such as a credit or debit card.

- Add Your Payment Details: Within the NFC payment app, you’ll be prompted to add your payment details. This typically involves entering your card information, such as the card number, expiration date, and security code. Some apps may allow you to scan your card using the device’s camera to expedite this process.

- Verify Your Payment Method: Depending on the app and your bank’s requirements, you may need to verify your payment method. This is usually done through a verification code sent via SMS, email, or a phone call. Follow the provided instructions to complete the verification process.

- Set Up Security Features: Take advantage of the security features offered by the NFC payment app. Enable biometric authentication, such as fingerprint or facial recognition, to add an extra layer of protection to your transactions. Set a strong PIN or passcode to secure your payment app and device.

- Ready to Pay: Once your NFC payment app is all set up, you can start using it to make contactless payments. Ensure that NFC is enabled on your device by going to the settings menu and toggling the NFC option. When making a purchase at a contactless payment terminal, simply unlock your device, hold it near the terminal, and follow the on-screen instructions on the device and terminal.

Remember to keep your device protected and refrain from sharing your payment app credentials or PIN with anyone. Regularly monitor your payment activity and report any suspicious transactions immediately to your bank or payment app provider.

By following these steps, you can easily set up NFC payment on your device and enjoy the convenience of making quick and secure contactless transactions.

Popular NFC Payment Apps

Several popular NFC payment apps offer a convenient and secure way to make contactless payments using your NFC-enabled devices. Let’s explore some of the most widely used NFC payment apps available:

1. Apple Pay: Apple Pay is a widely recognized NFC payment app available on iPhones, iPads, and Apple Watches. It allows users to store their credit or debit cards securely and make payments by holding their devices near NFC-enabled payment terminals. Apple Pay also supports in-app and online purchases, making it versatile across various payment scenarios.

2. Google Pay: Google Pay is a popular NFC payment app available for Android devices. It enables users to add their credit and debit cards, loyalty cards, and even transit cards to the app. Google Pay allows contactless payments using NFC technology and supports online and in-app payments. It also offers features like peer-to-peer payments and rewards integration.

3. Samsung Pay: Samsung Pay is an NFC payment app offered by Samsung for their smartphones and smartwatches. What sets Samsung Pay apart is its compatibility with traditional magnetic stripe card readers, which expands acceptance beyond NFC-enabled terminals. Users can make payments by tapping their devices or by swiping their devices on magnetic stripe card readers. Samsung Pay supports online and in-app payments as well.

4. PayPal: PayPal, a leading online payment platform, also offers NFC payment functionality. Users can link their PayPal accounts to their NFC-enabled devices and make contactless payments by tapping their devices on supported payment terminals. PayPal’s NFC payment feature, known as “Pay with Venmo” or “Pay in Person,” can be used for in-store purchases.

5. Bank Mobile Apps: Many banks provide their own dedicated NFC payment apps, allowing customers to make payments using their accounts. Examples include Chase Pay, Wells Fargo Mobile Wallet, and Bank of America Mobile Banking. These apps often support both NFC payments and online banking services, providing a comprehensive payment solution.

6. Transportation Apps: Some cities have dedicated NFC payment apps for public transportation, allowing users to pay for fares by tapping their devices. Examples include Transport for London’s “TfL Pay” app or Chicago Transit Authority’s “Ventra” app. These apps offer convenient and quick payment options for commuters.

Remember to check the availability and compatibility of these NFC payment apps in your region and with your specific device. Each app may have additional features, loyalty program integrations, and security measures to enhance the overall payment experience.

Whether you choose one of the popular NFC payment apps or a specific app offered by your bank, these options provide a convenient and secure way to make contactless payments using your NFC-enabled device.

NFC Payment Limitations

While NFC payment offers numerous benefits, it’s important to be aware of its limitations. Understanding these limitations can help users make informed decisions regarding their payment methods. Here are some key NFC payment limitations to consider:

1. Device Compatibility: NFC payment requires an NFC-enabled device, such as a smartphone or wearable. Older devices may not support NFC functionality, limiting the availability of NFC payment options. It’s essential to ensure that your device is compatible before expecting to use NFC payment.

2. Merchant Acceptance: Although NFC payment is becoming more widespread, not all merchants have upgraded their payment terminals to support contactless payments. Users may encounter situations where NFC payment is not accepted, requiring them to use alternative payment methods.

3. Reliance on Internet Connection: NFC payment typically requires an internet connection for transaction verification and authorization. In situations where internet connectivity is weak or unavailable, NFC payment may not be possible, hindering the user’s ability to make contactless transactions.

4. Transaction Limits: Some NFC payment methods may have transaction limits in place, restricting the maximum amount that can be spent in a single transaction. These limits vary depending on the payment provider and may not be suitable for high-value purchases.

5. Device Battery Life: Using NFC payment requires the device to have sufficient battery life. If a device’s battery is critically low, NFC payment may not be accessible. Users need to ensure that their devices are adequately charged before relying on NFC payment.

6. Security Considerations: While NFC payment technology incorporates security measures, users should remain vigilant. The risk of fraudulent transactions or unauthorized access to NFC-enabled devices exists, especially if precautions such as device passcodes and biometric authentication are not implemented. Users should also be cautious when making transactions in public settings to avoid potential eavesdropping or interference.

7. International Compatibility: NFC payment services may have limitations when used internationally. The availability and acceptance of NFC payment methods can vary from country to country, and currency conversion may also impact the overall usability.

It’s important to note that the limitations of NFC payment are continually evolving as technology and acceptance grow. As more merchants adopt NFC payment capabilities and as devices become more advanced, these limitations may be mitigated or overcome.

Users should consider their specific needs, preferences, and the prevalent NFC payment infrastructure in their area when deciding whether NFC payment is the right choice for them. NFC payment can provide a convenient and secure payment experience, but it is essential to be aware of its limitations to make informed decisions.

The Future of NFC Payment

The future of NFC payment is promising, with ongoing advancements in technology and increasing consumer adoption. Here are some key trends and developments that shape the future of NFC payment:

1. Expanding Merchant Acceptance: As NFC payment gains popularity, more merchants are likely to adopt NFC-enabled payment terminals. This increased acceptance will create a more seamless and consistent experience for consumers, encouraging broader adoption of NFC payment.

2. Integration with Wearable Devices: Wearable devices, such as smartwatches and fitness trackers, are becoming increasingly prevalent. NFC payment is expected to integrate further with these devices, allowing users to make payments directly from their wearables, enhancing convenience and accessibility.

3. IoT Integration: The Internet of Things (IoT) is connecting everyday objects to the internet, offering new opportunities for NFC payment. Smart home devices, connected cars, and other IoT-enabled devices could incorporate NFC technology, enabling seamless payment experiences across various touchpoints.

4. Biometric Advancements: Biometric authentication, such as fingerprint and facial recognition, is gaining popularity and enhancing security in various domains. NFC payment is likely to leverage advancements in biometric technology, providing more secure and frictionless authentication methods for users.

5. Enhanced Security: NFC payment will continue to focus on enhancing security features to protect user information and prevent unauthorized access. Advances in encryption techniques, tokenization, and multi-factor authentication will contribute to stronger security measures.

6. Seamless Integration with Loyalty Programs: NFC payment methods are expected to seamlessly integrate with loyalty programs, offering enhanced rewards and personalized offers to users. This integration will provide a unified experience, allowing users to earn and redeem loyalty points conveniently alongside their NFC transactions.

7. Global Expansion: NFC payment is expanding globally, with increased adoption in various regions. As these payment methods become more prevalent, cross-border compatibility and standardized protocols are expected, facilitating international NFC transactions.

8. Continued Innovation: The future will likely see ongoing innovation in NFC payment technologies. This includes advancements in communication speed, range, and compatibility, as well as the development of new use cases for NFC payment beyond traditional retail transactions.

Overall, the future of NFC payment looks bright, driven by technological advancements, consumer demand for contactless transactions, and the need for secure and convenient payment options. As NFC payment continues to evolve, it will play an increasingly significant role in the digital payment landscape, transforming the way we make transactions and shaping the future of commerce.