Introduction

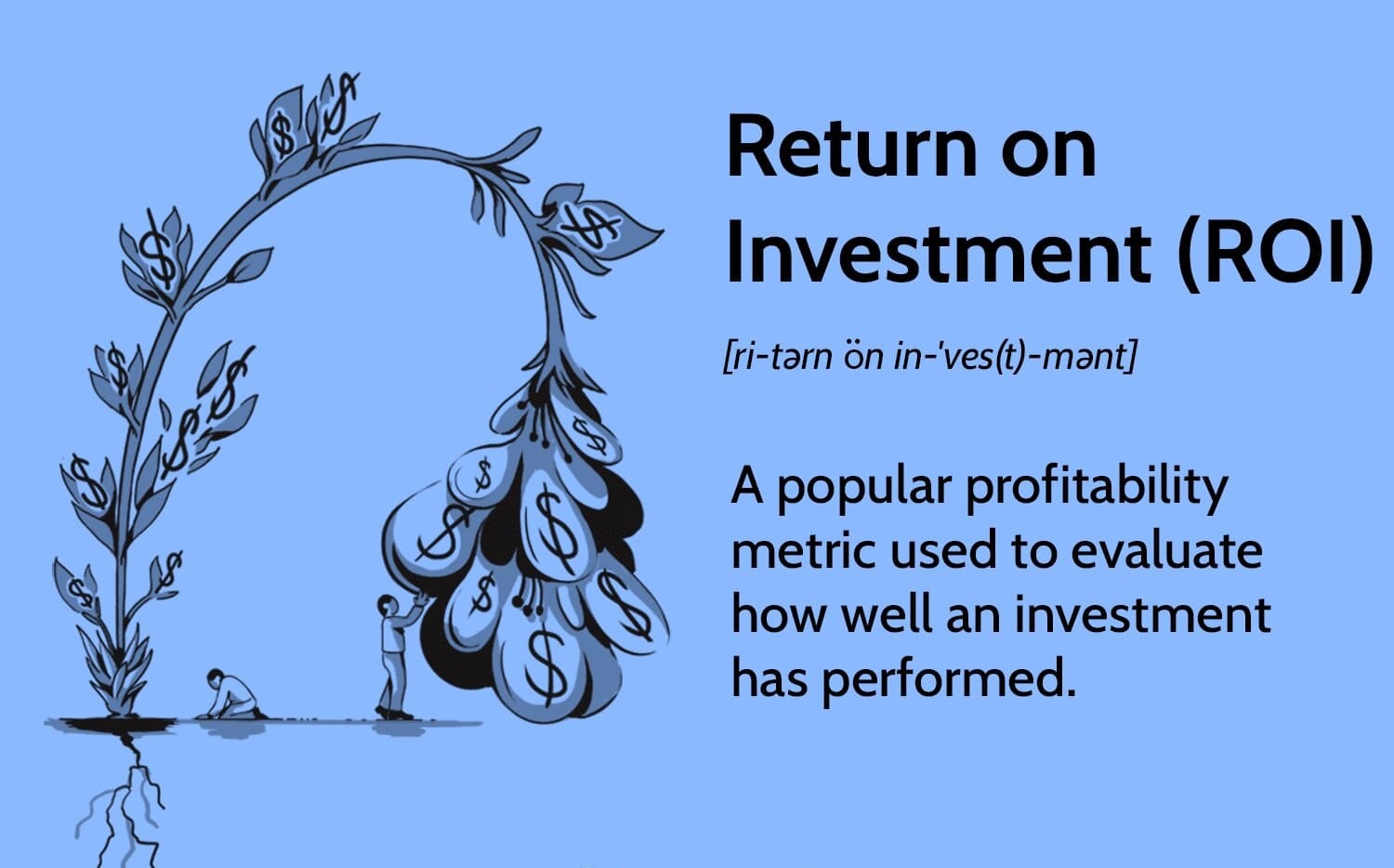

When it comes to investing, one of the key factors that investors strive for is a good rate of return. A rate of return refers to the gain or loss on an investment over a specific period of time, typically expressed as a percentage. It measures how well an investment has performed and is a crucial metric for assessing its profitability.

Investors are always on the lookout for investments that can generate a good rate of return. However, what constitutes a good rate of return can vary depending on various factors, including the investment strategy, risk tolerance, and market conditions. Furthermore, different types of investments have different average rates of return, making it important for investors to understand what to expect based on the asset class they are investing in.

In this article, we will explore the concept of rate of return, delve into the factors that can affect it, and discuss the historical average rates of return for different types of investments. We will also touch upon the relationship between risk and rate of return, as well as provide strategies that can help investors achieve a good rate of return.

It is important to note that while historical rates of return can provide guidance, past performance is not indicative of future results. Additionally, achieving a good rate of return requires careful analysis, research, and an understanding of your own investment goals and risk tolerance.

So, let’s dive in and explore the world of rate of return and what it takes to achieve a good return on your investments.

Understanding Rate of Return

Rate of return is a fundamental concept in investing that measures the profitability of an investment. It indicates the percentage increase or decrease in the investment’s value over a specific period of time. Understanding the rate of return is essential for investors to evaluate the performance of their investments and make informed decisions.

Rate of return can be calculated using the following formula:

(Ending Value – Beginning Value) / Beginning Value * 100

In simple terms, the formula takes into account the difference between the current value of the investment (ending value) and the initial investment value (beginning value), divided by the initial value and multiplied by 100 to express it as a percentage. This calculation shows how much the investment has grown or declined during the given time period.

It’s important to note that rate of return can be positive or negative. A positive rate of return indicates a profitable investment, where the investment has grown in value. On the other hand, a negative rate of return indicates a loss, meaning that the investment has declined in value.

Rate of return is often used as a benchmark for comparing the performance of different investments. Investors typically aim for a rate of return that exceeds the rate of inflation and provides a satisfactory return on investment. However, what constitutes a good rate of return can vary depending on various factors such as the investment strategy, risk tolerance, and market conditions.

Rate of return is influenced by various factors including market conditions, economic factors, management decisions, and investor sentiment. It can be affected by factors such as interest rates, inflation, company performance, industry trends, and geopolitical events. It’s important for investors to stay informed about these factors and their potential impact on the rate of return of their investments.

Now that we have a basic understanding of rate of return, let’s explore the factors that can affect it in the next section.

Factors Affecting Rate of Return

Several factors can influence the rate of return on investments. Understanding these factors is crucial for investors to make informed decisions and manage their investment portfolios effectively. Let’s take a closer look at some of the key factors that can impact the rate of return.

1. Economic Conditions: The overall economic conditions, such as GDP growth, inflation rates, and interest rates, can have a significant impact on the rate of return. During a period of economic expansion, investments generally perform well, leading to higher rates of return. Conversely, during economic downturns, investments may suffer and result in lower rates of return.

2. Market Risk: Investments are inherently exposed to market risk, which refers to the potential volatility and fluctuations in the financial markets. Factors such as market demand, supply, investor sentiment, and market volatility can significantly affect the rate of return. Investments in more volatile markets tend to have higher potential returns but also carry higher risk.

3. Investment Type: The type of investment chosen can greatly influence the rate of return. Different asset classes, such as stocks, bonds, real estate, and commodities, have varying historical rates of return. Stocks, for example, have historically offered higher returns but also come with higher volatility and risk compared to bonds or cash investments.

4. Time Horizon: The length of time an investment is held can impact the rate of return. Generally, longer time horizons provide more opportunity for compounding returns and potential growth. Conversely, short-term investments may have higher liquidity but may offer lower rates of return.

5. Investment Fees: The costs associated with investing, such as management fees, brokerage commissions, and transaction fees, can eat into the returns. It is crucial for investors to take into account these expenses when evaluating the overall rate of return potential of their investments.

6. Diversification: Diversifying an investment portfolio across different asset classes and geographic regions can help mitigate risk and potentially enhance overall returns. By spreading investments across different sectors and types of investments, investors can reduce the impact of a single investment’s performance on the overall portfolio return.

7. Investor Behavior: Investor behavior, including emotions, biases, and reactions to market movements, can impact the rate of return. Emotional decision-making, such as panic selling during market downturns or chasing trends during market rallies, can lead to suboptimal outcomes. Maintaining a disciplined and rational investment approach can help improve the chances of achieving a good rate of return.

By considering these factors and staying informed about market and economic conditions, investors can make more informed decisions and optimize their chances of achieving a desirable rate of return on their investments.

Historical Average Rates of Return

Understanding the historical average rates of return for different types of investments can provide valuable insights for investors. While past performance does not guarantee future results, knowing the historical averages can help set expectations and guide investment decisions. Let’s explore the historical average rates of return for some common investment types.

1. Stocks: Historically, stocks have provided the highest average rates of return among various asset classes. The average annual return for stocks, as measured by major stock market indices like the S&P 500, has been around 7-10% over the long term. However, it’s important to note that stock returns can be highly volatile, with significant fluctuations in shorter timeframes.

2. Bonds: Bonds have generally offered lower average rates of return compared to stocks. Government bonds and high-quality corporate bonds typically have average annual returns in the range of 2-5%. However, bonds offer more stability and income generation, making them a popular choice for risk-averse investors or those seeking regular fixed income.

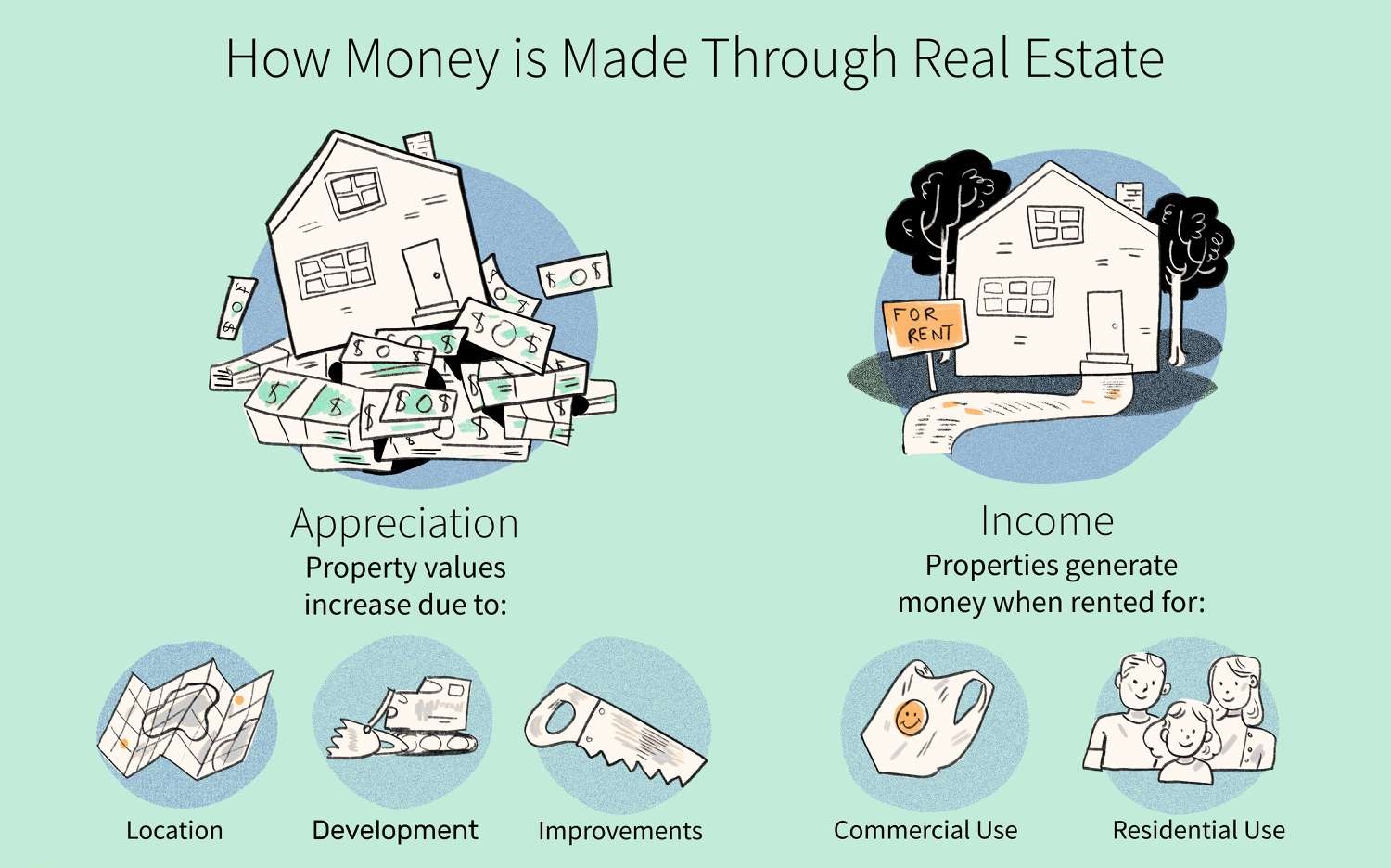

3. Real Estate: Investing in real estate, whether residential or commercial properties, has historically provided attractive average rates of return. Data from various sources suggest that real estate investments have delivered average annual returns of around 8-10% over the long term. Real estate returns can come from both rental income and property appreciation.

4. Commodities: Commodities such as gold, oil, and agricultural products can be a part of a well-diversified investment portfolio. Historically, commodity returns have varied significantly based on supply-demand dynamics and market conditions. While some commodities have experienced high average rates of return during certain periods, long-term average returns have been more modest, ranging from 2-5%.

It’s important to highlight that these average rates of return can vary significantly depending on the specific time period analyzed, the performance of the underlying securities, and other factors. Additionally, investment returns can be influenced by factors like inflation, taxes, and transaction costs.

Investors should also note that the pursuit of higher rates of return often involves assuming higher risks. Investments with potentially higher returns, such as stocks or real estate, may experience larger price fluctuations and increased volatility compared to lower-risk investments like bonds or cash.

When considering historical average returns, it’s crucial to align them with individual investment goals, risk tolerance, and time horizons. Diversification across different asset classes and periodic portfolio rebalancing can help investors navigate market uncertainties and optimize overall returns.

Now that we’ve explored historical average rates of return, let’s delve into the relationship between risk and rate of return in the next section.

Types of Investments and Their Average Rates of Return

There are various types of investments available to investors, each with its own characteristics and average rates of return. Understanding these different investment types can help investors make informed decisions and build a diversified portfolio. Let’s explore some common types of investments and their average rates of return.

1. Stocks: Stocks represent ownership in publicly traded companies. Historically, stocks have offered the highest average rates of return among different asset classes. The average annual return for stocks, as measured by stock market indices like the S&P 500, has been around 7-10% over the long term. However, it’s important to note that stock returns can be volatile, experiencing significant fluctuations in shorter timeframes.

2. Bonds: Bonds are debt securities issued by governments, municipalities, and corporations to raise capital. Bonds generally provide lower average rates of return compared to stocks but offer more stability and income generation. Government bonds and high-quality corporate bonds typically have average annual returns in the range of 2-5%. Bond returns are primarily driven by interest payments and changes in interest rates.

3. Real Estate: Real estate investments involve purchasing properties for income generation and potential appreciation. Real estate has historically provided attractive average rates of return. Data from various sources indicate that real estate investments have delivered average annual returns of around 8-10% over the long term. These returns come from a combination of rental income and property value appreciation.

4. Mutual Funds: Mutual funds pool money from multiple investors to invest in a diversified portfolio of assets. The average rates of return for mutual funds can vary widely depending on the fund’s investment objectives and underlying holdings. Equity-focused mutual funds have historically offered average returns in line with the stock market, while bond funds have delivered returns closer to those of bonds.

5. Exchange-Traded Funds (ETFs): ETFs are similar to mutual funds but trade on an exchange like a stock. Like mutual funds, ETF returns can vary depending on the investment strategy and underlying assets. ETFs that track broad-based indices, such as the S&P 500, tend to deliver returns in line with the performance of the index they are tracking.

6. Commodities: Commodities include resources such as gold, oil, natural gas, and agricultural products. Investments in commodities can be made through futures contracts or commodity-specific funds. Average rates of return for commodities can vary significantly based on supply-demand dynamics and market conditions. Long-term average returns for commodities have been more modest, ranging from 2-5%.

It’s important to note that these average rates of return can change over time and are subject to market fluctuations and economic conditions. Individual investment choices, as well as market timing and management fees, can also impact the overall returns achieved.

When constructing an investment portfolio, diversification across different asset classes can help spread risks and potentially improve overall returns. It’s advisable for investors to consult with a financial advisor and consider their investment goals, risk tolerance, and time horizon before making investment decisions.

Now that we’ve explored different investment types and their average rates of return, let’s discuss the relationship between risk and rate of return.

Risk and Rate of Return

When it comes to investing, risk and rate of return go hand in hand. These two concepts are interconnected, and understanding their relationship is crucial for investors. In general, the potential for higher returns usually comes with a higher level of risk. Let’s delve into how risk and rate of return are related.

1. Risk: Risk refers to the uncertainty and potential for loss in an investment. Different investments carry different levels of risk. Generally, investments with higher potential returns tend to have higher risk. For example, stocks are known for their volatility and can experience significant price fluctuations. On the other hand, bonds are considered lower-risk investments but offer more modest returns.

2. Rate of Return: Rate of return measures the gain or loss on an investment relative to its initial cost. It reflects the overall profitability of the investment over a specific period. The rate of return is influenced by various factors such as market conditions, economic factors, and investment performance.

3. Risk-Return Tradeoff: The relationship between risk and rate of return can be summed up by the risk-return tradeoff. This concept suggests that higher potential returns are usually associated with higher levels of risk. Investors who are willing to take on more risk have the potential to earn higher returns, but they also face a greater chance of losing money. Conversely, for investors seeking lower-risk investments, the potential rate of return may be more modest.

4. Risk Assessment: It’s important for investors to assess their risk tolerance and consider their investment goals before making investment decisions. Some investors may have a higher tolerance for risk and are comfortable with potentially larger fluctuations in the value of their investments. Others may have a lower risk tolerance and prioritize capital preservation over high returns.

5. Diversification: Diversification is a risk management strategy that involves spreading investments across different asset classes, sectors, or geographic regions. By diversifying, investors can reduce their exposure to the risks associated with a single investment. A well-diversified portfolio can potentially lower risk while still aiming for a reasonable rate of return.

It’s important to note that there is no one-size-fits-all approach to balancing risk and rate of return. Each investor’s risk appetite and financial goals will vary, and decisions should be made based on individual circumstances. Some investors may seek higher returns and are willing to tolerate greater risk, while others prioritize capital protection and prefer more conservative investments.

By understanding the risk-return tradeoff and their own risk tolerance, investors can make informed decisions to construct a portfolio that aligns with their financial goals and comfort level. Regular monitoring and review of investments are also vital to ensure that the risk-return balance remains appropriate over time.

Now that we’ve explored the relationship between risk and rate of return, let’s move on to discussing strategies for achieving a good rate of return.

Strategies for Achieving a Good Rate of Return

Achieving a good rate of return on investments requires careful planning, analysis, and implementation of effective strategies. While there is no guaranteed way to achieve success, there are several strategies that can potentially improve your chances of earning a good rate of return. Let’s explore some of these strategies.

1. Asset Allocation: Asset allocation involves diversifying your investments across different asset classes, such as stocks, bonds, real estate, and commodities. This diversification helps spread risk and can potentially improve overall returns. The optimal asset allocation will depend on your risk tolerance, time horizon, and investment goals.

2. Research and Analysis: Conduct thorough research and analysis before making investment decisions. This includes researching companies, industries, and macroeconomic trends that can impact the performance of your investments. Stay informed about market news, earnings reports, and other relevant information to make well-informed decisions.

3. Dollar-Cost Averaging: Dollar-cost averaging involves regularly investing a fixed amount of money into an investment regardless of market conditions. This strategy helps mitigate the impact of market volatility by purchasing more shares when prices are low and fewer shares when prices are high. Over time, this approach can potentially result in a better average purchase price and improve overall returns.

4. Long-Term Investing: Investing with a long-term perspective can help smooth out short-term market fluctuations and increase the likelihood of achieving favorable returns. By staying invested for a longer period, you can potentially benefit from compound growth and the power of compounding returns.

5. Rebalancing: Regularly review and rebalance your investment portfolio to maintain your desired asset allocation. Rebalancing involves adjusting the allocation of your investments to bring them back in line with your target percentages. This strategy ensures that your portfolio doesn’t become too heavily weighted in one asset class, reducing potential risks.

6. Identify Opportunities: Stay proactive in identifying investment opportunities, such as undervalued stocks, emerging industries, or promising sectors. Conduct thorough due diligence and analysis to assess the potential for growth and profitability. Timing can be crucial, so be patient and wait for the right opportunities to capitalize on.

7. Seek Professional Advice: Consider seeking the guidance of a financial advisor who can provide personalized advice based on your financial goals, risk tolerance, and market conditions. An experienced advisor can help develop a comprehensive investment strategy tailored to your needs and guide you through the ups and downs of the market.

It’s essential to note that investing involves risk, and no strategy can guarantee success. Market conditions, economic factors, and unforeseen events can impact the performance of investments. It’s crucial to stay informed, regularly review your investments, and adjust your strategies as needed.

By implementing these strategies and maintaining a disciplined approach to investing, you can increase your chances of achieving a good rate of return on your investments.

Now that we’ve explored strategies for achieving a good rate of return, let’s move on to evaluating your personal rate of return.

Evaluating Your Personal Rate of Return

Assessing your personal rate of return is an important step in evaluating the performance of your investments and making informed decisions. While it’s crucial to consider overall market conditions and industry benchmarks, evaluating your personal rate of return provides a more accurate reflection of your investment performance. Let’s explore how you can evaluate your personal rate of return.

1. Gather Investment Information: Begin by gathering information about your investments, including the initial investment amounts, subsequent contributions, withdrawals, and any changes in asset allocation over time. This information will allow you to calculate and evaluate your personal rate of return.

2. Calculate Returns: There are various methods to calculate personal rate of return, including the time-weighted method and the money-weighted method. The time-weighted method removes the impact of timing and focuses on the average performance of your investments. The money-weighted method considers the impact of your contributions and withdrawals over time. Use a reliable investment tracking tool or consult a financial professional to calculate your returns accurately.

3. Consider Time Horizons: Evaluate your personal rate of return over different time horizons to gain a comprehensive understanding of the performance of your investments. Analyze your returns annually, quarterly, or over a multi-year period to identify trends and assess consistency in performance.

4. Compare to Benchmarks: Compare your personal rate of return to relevant benchmarks, such as market indices or industry-specific performance indicators. Benchmarks provide a benchmark for comparison and help you assess the relative success of your investments. However, keep in mind that benchmarks might not match your specific asset allocation or investment strategy, so use them as reference points rather than definitive measures.

5. Adjust for Inflation and Expenses: Consider the impact of inflation and investment expenses on your personal rate of return. Inflation erodes the purchasing power of your investments over time, so it’s essential to evaluate your returns in real terms by subtracting the inflation rate. Additionally, account for any investment-related expenses, such as management fees or transaction costs, which can affect your overall returns.

6. Review and Reflect: Regularly review and reflect on your personal rate of return to identify areas for improvement or adjustments in your investment strategy. Analyze the performance of individual investments or asset classes within your portfolio to determine if any modifications are necessary. Use your evaluation to make informed decisions about rebalancing or reallocating your investments based on your financial goals and risk tolerance.

Remember, evaluation of your personal rate of return is a tool to assess performance and guide future investment decisions. It’s important to establish realistic expectations, considering that investment returns can fluctuate and are influenced by unpredictable market conditions. If you are uncertain about evaluating your personal rate of return, seek guidance from a financial advisor who can provide expert advice tailored to your specific circumstances.

Now that we’ve discussed evaluating your personal rate of return, let’s conclude our discussion.

Conclusion

Understanding and striving for a good rate of return is a key objective for investors. It involves evaluating investment performance, managing risk, and making informed decisions to optimize returns. Throughout this article, we have explored various aspects related to rate of return, including its definition, factors affecting it, historical averages, types of investments, risk-return tradeoffs, strategies for achieving a good rate of return, and evaluating personal performance.

It’s important to note that investing is not a one-size-fits-all approach, and what constitutes a good rate of return may vary based on individual circumstances and goals. Investors should consider their risk tolerance, time horizon, and financial objectives when developing an investment strategy. Diversification, research, and staying informed about market conditions are essential elements for successful investing.

While historical averages can provide valuable insights, they should not be relied upon solely when making investment decisions. Past performance does not guarantee future results. It’s crucial to remember that investment returns are influenced by market conditions, economic factors, and other variables that can change over time.

Evaluating personal rates of return allows investors to gauge the performance of their investments accurately. By calculating returns, considering time horizons, comparing to benchmarks, and adjusting for inflation and expenses, investors can gain a better understanding of their investment performance and make necessary adjustments to their portfolios.

In conclusion, achieving a good rate of return requires a thoughtful and disciplined approach to investing. Combine thorough research with an understanding of risk-return tradeoffs, and consider seeking guidance from a financial advisor when needed. By implementing effective strategies, monitoring performance, and maintaining a long-term perspective, investors can increase their chances of achieving their desired rate of return and reaching their financial goals.