Introduction

Welcome to our comprehensive guide on direct deposit and the banking information required to set it up. In today’s digital age, direct deposit has become the preferred method of receiving payments, whether it’s your paycheck, tax refunds, or government benefits. This hassle-free and secure method provides individuals with the convenience of having their funds directly deposited into their bank account, without the need for paper checks or manual depositing.

In this article, we will delve into the world of direct deposit and discuss the necessary banking information required to set it up. From personal details to bank account information and employer details, we will guide you through the process of providing the necessary data to ensure a seamless and smooth direct deposit experience.

Whether you are starting a new job, transitioning to a new payment method, or simply exploring the benefits of direct deposit, understanding the information required will empower you to make informed decisions and take advantage of this convenient payment method. So, let’s explore the world of direct deposit and uncover the banking information you need to provide to enjoy its benefits.

What is Direct Deposit?

Direct deposit is a financial service that allows individuals to receive payments electronically, directly into their bank account. It eliminates the need for physical checks and offers a secure, convenient, and efficient way to receive funds. Whether it’s your salary, government benefits, tax refunds, or any other form of payment, direct deposit ensures that your money is quickly and safely deposited into your account.

With direct deposit, your funds are deposited directly into your bank account on a predetermined schedule, such as weekly, bi-weekly, or monthly, depending on the payment source. This means you no longer need to manually deposit checks or wait in line at the bank to access your funds. Instead, your money is automatically credited to your account, enabling you to have immediate access to it.

Direct deposit offers numerous advantages over traditional payment methods. Firstly, it saves you time and effort by eliminating the need to visit a bank or cash a physical check. You no longer have to worry about lost or stolen checks, as your money is securely transferred electronically. It also ensures that your funds are available on time, even if you’re unable to physically go to the bank.

Another benefit of direct deposit is that it allows you to gain access to your funds faster. While traditionally, it may take several days for a check to clear and for funds to become available, direct deposit provides instant access to your money.

Direct deposit is widely utilized by employers to pay their employees’ salaries. It not only simplifies the payment process but also reduces administrative costs associated with printing and distributing paper checks. Additionally, direct deposit provides employees with a more reliable and predictable form of payment.

In addition to payroll, direct deposit is also used for various other types of payments, such as government benefits, retirement funds, tax refunds, and reimbursements from insurance companies. This method ensures that these payments are seamlessly deposited into the recipient’s bank account, providing convenience and security.

Now that we have a clear understanding of what direct deposit is and its advantages, let’s explore the specific requirements for setting up direct deposit and the information you need to provide.

Benefits of Direct Deposit

Direct deposit offers a range of benefits that make it a preferred payment method for individuals and organizations alike. Let’s explore some of the key advantages of using direct deposit:

- Convenience: Direct deposit eliminates the need for physical checks, reducing your trips to the bank. You don’t have to worry about lost or stolen checks, and you can access your funds immediately without waiting for clearance.

- Time Savings: With direct deposit, you save valuable time that would have been spent depositing checks manually. There’s no need to stand in line at the bank, as your funds are automatically deposited into your account.

- Security: Direct deposit provides enhanced security compared to physical checks. Your funds are electronically transferred, reducing the risk of theft or loss. You also have the option to receive email or text notifications whenever a deposit is made to your account, giving you peace of mind and better control over your finances.

- Reliability: Direct deposit ensures that your funds are available on time, even if you’re unable to visit the bank in person. It eliminates the risk of delayed or lost payments, providing you with a more reliable and predictable payment method.

- Faster Access to Funds: With direct deposit, your funds are available to you immediately after they are deposited. This is especially beneficial for individuals who rely on timely access to their funds to cover expenses or make investments.

- Streamlined Payments: Direct deposit simplifies the payment process for employers and organizations. It eliminates the need to print and distribute physical checks, reducing administrative costs and ensuring timely and accurate payments to employees or beneficiaries.

- Environmentally Friendly: By choosing direct deposit, you contribute to reducing paper waste. With no physical checks involved, direct deposit is an environmentally friendly alternative to traditional payment methods.

These are just a few of the many advantages offered by direct deposit. Whether it’s the convenience, time savings, enhanced security, or reliability, direct deposit has become the go-to method for receiving payments in today’s digital age.

Now that we’ve explored the benefits of direct deposit, let’s dive into how it works and the requirements for setting it up.

How Does Direct Deposit Work?

Direct deposit operates through the Automated Clearing House (ACH) network, which is a secure electronic payment system used by financial institutions to transfer funds electronically. Here’s a step-by-step breakdown of how direct deposit works:

- Employer initiates Direct Deposit: If you’re receiving your paycheck through direct deposit, your employer will initiate the process by obtaining your bank account details and the authorization to deposit your wages electronically.

- Bank Account Verification: Once your employer has the necessary information, they will verify your bank account details, such as your account number and routing number, with your financial institution. This verification helps ensure that the funds are being deposited into the correct account.

- Funds are Transferred: On the designated payday, your employer will electronically transfer the funds from their bank account to your bank account. This transfer occurs through the ACH network, which securely and efficiently processes the transaction.

- Funds are Deposited: Upon receiving the funds, your bank credits your account with the deposit amount. This process typically occurs overnight, and your funds will be available for use the next business day.

- Accessing the Funds: Once the funds have been deposited into your account, you can access them through various methods, such as ATM withdrawals, online banking, or using your debit card for purchases.

It’s important to note that the timing of the deposit may vary depending on your bank and your employer’s payroll practices. Some banks may credit the funds to your account earlier than the expected deposit date, while others may take longer.

Direct deposit is not limited to just employers’ payroll. It is also used for other types of payments, such as government benefits, tax refunds, pensions, and other recurring payments. The process is similar, where the respective organization electronically transfers the funds to your bank account through the ACH network.

One of the key advantages of direct deposit is the convenience and reliability it offers. You no longer have to worry about physically depositing checks or holding onto paper payments. The electronic transfer of funds ensures that your money is securely and efficiently deposited into your account, ready for your use.

Now that we understand how direct deposit works, let’s move on to explore the requirements and information needed to set up direct deposit.

The Requirements for Direct Deposit

In order to set up direct deposit, there are certain requirements and information that you need to provide. These requirements may vary depending on your specific situation, but generally, the following information is needed:

- Personal Information: You’ll need to provide personal information such as your full name, address, phone number, and email address. This information is used to identify and communicate with you regarding your direct deposit setup.

- Bank Account Information: You’ll need to provide your bank account details, including the bank’s name, your account number, and the routing number. This information is crucial as it ensures that your funds are deposited into the correct account.

- Social Security Number and Tax ID: Depending on the type of direct deposit, you may be required to provide your Social Security number or Tax ID number. This is typically necessary for payroll-related direct deposits or government benefit payments.

- Employer Information: If you’re setting up direct deposit for your salary or wages, you’ll need to provide your employer’s information, such as their name, address, and contact details. Your employer will use this information to process and transfer your payments electronically.

- Authorization: In many cases, you’ll need to sign an authorization form or provide consent for direct deposit to be set up. This authorization confirms that you agree to have your payments deposited electronically into your designated bank account.

These are the general requirements for setting up direct deposit, but keep in mind that specific organizations or financial institutions may have additional or slightly different requirements. It’s best to check with your employer or the organization responsible for the direct deposit to ensure you have all the necessary information and documentation.

By providing the required information and meeting the necessary requirements, you can take advantage of the numerous benefits that direct deposit offers. Not only does it simplify the payment process, but it also ensures that your funds are available on time, providing you with a convenient and reliable method of receiving payments.

Now that we understand the requirements for direct deposit, let’s delve into the specific personal and bank account information needed for setting it up.

Personal Information Needed for Direct Deposit

When setting up direct deposit, you will be required to provide certain personal information to ensure the smooth and secure transfer of funds. The following are the key pieces of personal information needed for direct deposit:

- Full Name: You will need to provide your full legal name as it appears on official documents such as your ID or Social Security card. This ensures that the funds are deposited into the correct account and that your identity is verified.

- Address: Your current residential address is required for accurate account identification and record-keeping purposes. Make sure to provide the most up-to-date address to avoid any potential issues with your direct deposit setup.

- Phone Number: Your contact number enables the organization initiating the direct deposit to get in touch with you if there are any questions or issues regarding your account or payment.

- Email Address: Providing an email address allows for electronic communication regarding your direct deposit. This may include notifications of deposit confirmations, updates, or any other relevant information related to your payments.

- Social Security Number (SSN) or Tax ID: Depending on the type of payment, you may be required to provide your Social Security Number (SSN) or Tax Identification Number (TIN). This information is used for identification purposes and to comply with tax regulations.

It is important to ensure that the personal information provided is accurate and up-to-date. Any discrepancies or errors could cause delays or issues with the direct deposit process. Ensure that you double-check the information before submitting it to avoid any potential complications.

Keep in mind that the specific personal information required may vary depending on the organization or entity initiating the direct deposit. Some may require additional information or documentation to verify your identity or eligibility for certain payments.

By providing the necessary personal information, you are ensuring a secure and efficient transfer of funds into your designated bank account. It also serves as a way for the organization responsible for the direct deposit to keep accurate records and communicate with you regarding your payments.

Now that we have covered the personal information required for direct deposit, let’s move on to the bank account information you need to provide.

Bank Account Information Required for Direct Deposit

When setting up direct deposit, it is essential to provide accurate and complete bank account information to ensure that funds are deposited into the correct account. The following are the key pieces of bank account information required for direct deposit:

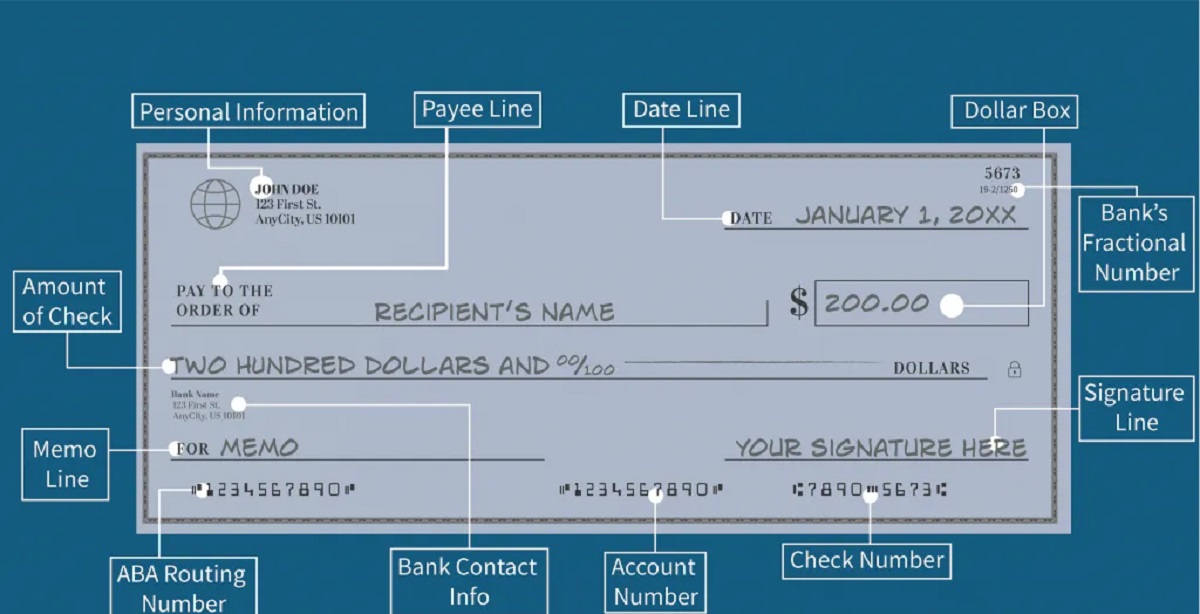

- Bank Name: You will need to provide the name of the bank where you have an active checking or savings account. This information ensures that the funds are deposited into the correct financial institution.

- Account Type: Specify whether your bank account is a checking or savings account. This information helps direct the funds to the appropriate account type.

- Account Number: You must provide your bank account number, which is a unique identifier for your account. This number allows the organization initiating the direct deposit to accurately deposit funds into your specific account.

- Routing Number: Also known as the ABA routing number, this nine-digit number identifies the bank and branch where your account is held. It ensures that the funds are routed to the correct financial institution and account.

It’s important to note that the location of the bank may impact the routing number. For example, banks in different states or regions may have different routing numbers. Make sure to provide the correct routing number associated with your specific bank branch.

To ensure the accuracy of your bank account information, consider reviewing a checkbook or contacting your bank directly. The checkbook typically includes the account number and routing number, making it easier to provide the correct details for direct deposit.

Remember, the bank account information provided is confidential and should be kept secure. Double-check the information to avoid any errors or complications with the direct deposit setup.

By providing accurate and complete bank account information, you enable the organization initiating the direct deposit to transfer funds seamlessly and securely into your designated account. This information is crucial for a successful direct deposit process.

Now that we understand the bank account information required for direct deposit, let’s explore the additional information needed, such as your Social Security number and employer details.

Social Security Number and Tax ID for Direct Deposit

For certain types of direct deposits, such as payroll or government benefits, you may be required to provide your Social Security number (SSN) or Tax Identification Number (TIN). Here’s why this information is needed:

- Social Security Number (SSN): Your SSN is a unique nine-digit number issued by the Social Security Administration. It serves as both an identification number and a way to track your earnings for Social Security benefits and taxation purposes. When setting up direct deposit for payroll or government benefits, your SSN helps verify your eligibility and ensure accurate allocation of funds to your account.

- Tax Identification Number (TIN): If you don’t have an SSN, you may be required to provide a Tax Identification Number (TIN) instead. A TIN is issued to individuals and businesses by the Internal Revenue Service (IRS) for tax reporting purposes. It serves a similar purpose to an SSN and is required for tax-related direct deposits, such as tax refunds.

Both the SSN and TIN are used for identification and verification purposes, ensuring that the funds are deposited into the correct account and complying with tax regulations. It’s important to provide the correct and up-to-date SSN or TIN to avoid any delays or issues with your direct deposit setup.

When providing your SSN or TIN, it’s crucial to exercise caution and protect your personal information. Only provide this information to trusted and reputable entities. Be cautious of phishing attempts or fraudulent requests for sensitive information.

By providing your SSN or TIN for direct deposit, you enable the organization initiating the deposit to properly identify and allocate funds to your account, ensuring a smooth and secure transfer of funds.

Now that we understand why the SSN or TIN is required for certain types of direct deposits, let’s move on to discussing the employer information needed for payroll direct deposits.

Employer Information for Direct Deposit

When setting up direct deposit for payroll, you will need to provide specific information about your employer. This information helps facilitate the direct deposit process and ensures that your wages are accurately and securely deposited into your bank account. The following are the key pieces of employer information required for direct deposit:

- Employer Name: You will need to provide the name of your employer, including the official company name. This information helps identify your employer and confirm the legitimacy of the direct deposit setup.

- Employer Address: It is important to provide the correct mailing address of your employer. This includes the street address, city, state, and zip code. It allows for accurate communication and ensures that payments are processed correctly.

- Employer Contact Information: Providing the contact information of your employer, such as their phone number or email address, allows for effective communication and may be necessary for verification or resolving any direct deposit-related inquiries.

- Employee ID or Payroll Number: Some employers require the inclusion of an employee ID or payroll number. This unique identifier helps distinguish between employees and ensures that payments are allocated correctly to individual accounts.

It’s important to provide accurate and up-to-date employer information to avoid any delays or complications with your direct deposit setup. Double-check with your employer or HR department to ensure that you have the correct details.

Keep in mind that the specific employer information required may vary depending on the organization or payroll provider. If you are unsure of any required details, reach out to your employer’s human resources department for guidance.

By providing your employer information, you enable the organization responsible for direct deposit to verify your employment and process your payroll payments accurately and efficiently. This ensures that your wages are seamlessly deposited into your designated bank account.

Now that we understand the employer information required for direct deposit, let’s move on to the steps involved in setting up direct deposit.

How to Set Up Direct Deposit

Setting up direct deposit is a straightforward process that can be completed easily by following these simple steps:

- Gather Required Information: Collect all the necessary information needed for direct deposit, including your personal information, bank account details, Social Security number or Tax ID, and employer information. Ensure that you have accurate and up-to-date information at hand.

- Complete Direct Deposit Authorization Form: Many employers or organizations have a direct deposit authorization form that you need to fill out. This form typically asks for your personal information, bank account details, and employer information. Fill out the form accurately and make sure to sign it if required.

- Submit the Form: Once you’ve completed the direct deposit authorization form, submit it to your employer or the organization responsible for handling direct deposits. You may need to submit the form electronically or hand it in physically, depending on the submission process adopted by your employer.

- Verification Process: The organization initiating the direct deposit, such as your employer or benefits provider, will validate the information provided on the form. This verification process ensures the accuracy and security of the direct deposit setup.

- Confirm Deposit: After the information has been verified, you will typically receive a confirmation of your direct deposit setup. This may be a written confirmation, an email notification, or a deposit notification from your bank indicating that the funds have been deposited successfully.

It’s important to note that the processing time for direct deposit setup may vary depending on the organization, payroll cycles, and verification procedures. It’s always a good idea to double-check with your employer to confirm when you can expect direct deposit to take effect.

Remember to keep your bank account information and personal details secure. Only provide them to trusted and reputable organizations. Be cautious of any suspicious requests for sensitive information or phishing attempts.

By following these simple steps, you can easily set up direct deposit and start enjoying the convenience and benefits it offers. No more waiting for checks or making trips to the bank – direct deposit ensures that your funds are reliably and efficiently deposited into your bank account.

Now that we’ve covered the process of setting up direct deposit, let’s address some common questions related to direct deposit.

Frequently Asked Questions about Direct Deposit

Here are some frequently asked questions about direct deposit:

- Is direct deposit safe? Yes, direct deposit is a safe and secure method of receiving payments. It eliminates the risks associated with physical checks, such as loss or theft. Direct deposit utilizes encryption and secure networks to transfer funds electronically, ensuring the confidentiality and integrity of your financial information.

- How long does it take for direct deposit to take effect? The time it takes for direct deposit to take effect can vary. Some employers and financial institutions process direct deposits quickly, making funds available within one to two business days. However, in some cases, it may take longer, especially when setting up direct deposit for the first time or during holidays or weekends.

- Can I split my direct deposit between multiple accounts? In many cases, yes. Some employers or financial institutions offer the option to split your direct deposit between multiple accounts. This allows you to allocate a portion of your funds to a checking account for everyday expenses and another portion to a savings account or investment account.

- What happens if my bank account information changes? If your bank account information changes, you will need to update it with your employer or the organization responsible for direct deposit. This typically involves submitting a new direct deposit authorization form with the updated bank account details.

- Can I cancel or stop direct deposit? Yes, you can cancel or stop direct deposit at any time. Simply notify your employer or the organization initiating the direct deposit and provide any necessary information or documentation to discontinue the service.

- What if I have issues with my direct deposit? If you encounter any issues with your direct deposit, such as missing or incorrect deposits, it’s important to reach out to your employer or the organization responsible for the direct deposit. They are best equipped to address and resolve any problems you may encounter.

Remember, specific policies and procedures related to direct deposit may vary depending on your employer, financial institution, or payment source. It’s always a good idea to consult with the appropriate parties for accurate and up-to-date information specific to your situation.

Now that we’ve addressed some common questions about direct deposit, let’s conclude with a summary of the key points covered in this guide.

Conclusion

Direct deposit offers a convenient, secure, and efficient way to receive payments directly into your bank account. By understanding the requirements and providing the necessary information, you can enjoy the benefits of direct deposit, such as time savings, improved security, faster access to funds, and streamlined payments.

In this guide, we covered the basics of direct deposit, including what it is and how it works. We discussed the personal information and bank account details needed to set up direct deposit and explored the importance of providing accurate employer information. We also answered common questions related to direct deposit, addressing concerns about safety, processing times, account changes, and more.

If you’re considering direct deposit for your payroll, government benefits, or other recurring payments, be sure to gather the required information and follow the necessary steps outlined in this guide. Remember to keep your personal and bank account information secure, only provide it to trusted sources, and be cautious of any suspicious requests for sensitive details.

Direct deposit continues to gain popularity due to its convenience, reliability, and benefits. By embracing this digital payment method, you can simplify your financial transactions, save time, and have greater control over your funds. Take advantage of the ease and efficiency of direct deposit to enhance your financial well-being.

We hope this guide has provided you with valuable insights and information about direct deposit. If you have any further questions or need assistance with setting up direct deposit, reach out to your employer or financial institution for guidance and support.