Introduction

Smart contracts are poised to revolutionize the legal industry, potentially rendering traditional lawyers obsolete. With advancements in blockchain technology, smart contracts can automate and enforce the terms of an agreement without the need for intermediaries. This transformative technology has the potential to streamline business transactions, reduce legal costs, and increase efficiency.

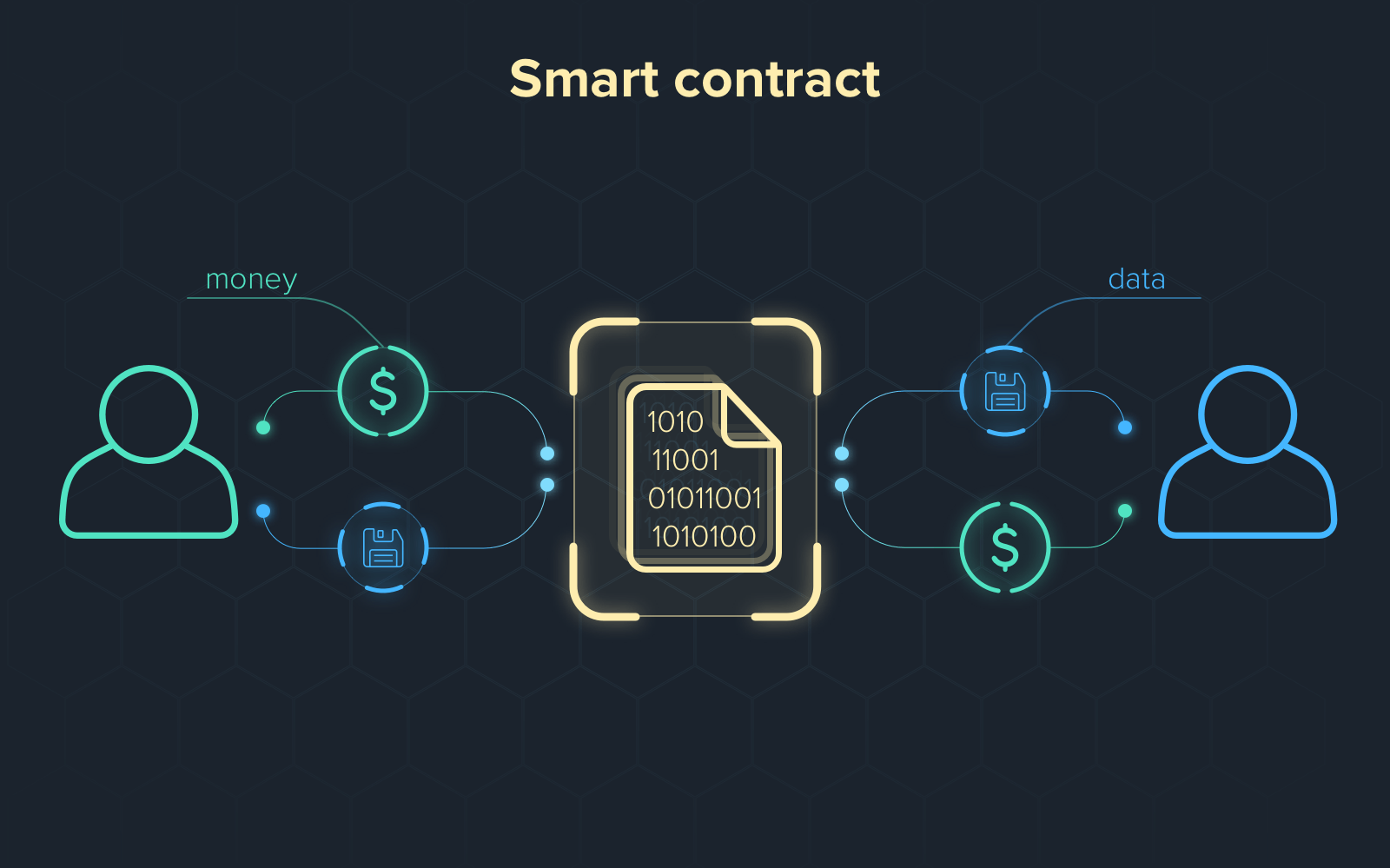

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They automatically execute the actions specified in the contract when the predetermined conditions are met. Developed on blockchain platforms like Ethereum, these contracts are distributed, transparent, and tamper-proof, ensuring trust and security.

Traditional contracts require lawyers to draft, review, and enforce agreements. However, smart contracts eliminate the need for intermediaries by automating these processes. By leveraging blockchain technology, smart contracts offer numerous benefits, including precision and accuracy, cost savings, speed, and increased transparency.

In the realm of business transactions, smart contracts can remove the reliance on lawyers for drafting and negotiating contracts. With pre-programmed conditions and clauses, smart contracts can save time and reduce errors. The automation and self-execution of smart contracts ensure that parties involved fulfill their contractual obligations, minimizing disputes and mitigating the risk of breaches.

Additionally, the use of smart contracts can significantly reduce costs. By eliminating the need for legal intermediaries, businesses can save on legal fees and expenses. With the automation of contract execution, companies can avoid costly delays, disputes, and litigation.

Speed is another advantage of smart contracts. Traditional contract processes often involve back-and-forth negotiations, revisions, and delays. In contrast, smart contracts can expedite the entire contract lifecycle, from drafting to execution. By removing the time-consuming manual processes, businesses can accelerate their operations and enhance productivity.

Furthermore, smart contracts offer increased transparency. The distributed nature of blockchain ensures that all parties have access to the same information, eliminating any doubts or discrepancies. This transparency strengthens trust and reduces the likelihood of fraud or manipulation.

While smart contracts have the potential to revolutionize the legal industry, they are not without challenges and limitations. The complexities of legal agreements and the need for human interpretation can pose challenges to fully automating certain contracts. Additionally, the reliance on blockchain technology presents scalability and regulatory concerns that need to be addressed.

Definition of Smart Contracts

Smart contracts refer to self-executing contracts with the terms of the agreement directly written into code. They are computer programs that automatically execute actions based on predefined conditions without the need for manual intervention. By leveraging blockchain technology, smart contracts ensure transparency, immutability, and security.

Unlike traditional contracts, which rely on legal intermediaries to enforce and interpret the terms, smart contracts execute themselves once the predetermined conditions are met. The agreement is encoded and stored on a blockchain, ensuring that it cannot be altered or tampered with. This decentralized nature eliminates the need for trust in a single party and establishes a trustless environment.

The code within smart contracts establishes rules and conditions that all participants in the contract must adhere to. The agreement is self-enforcing, as any actions triggered by the conditions are automatically executed. For instance, in a real estate smart contract, once the buyer transfers the required funds to the contract, ownership of the property is automatically transferred to them.

Smart contracts are typically developed on blockchain platforms, with Ethereum being a well-known example. Ethereum’s programming language, Solidity, enables developers to create complex and secure smart contracts. These contracts are then deployed on the Ethereum blockchain, making them publicly accessible and verifiable.

With smart contracts, the fulfillment of contractual obligations becomes automated, reducing the need for third-party intermediaries such as lawyers or escrow agents. The terms of the agreement exist within the code, making it transparent and ensuring that all parties have access to the same information.

Smart contracts provide several advantages over traditional contracts. Firstly, they eliminate the need for trust in a central authority, as the blockchain ensures transparency and consensus among participants. Additionally, smart contracts enhance efficiency by automating processes that previously required manual intervention.

It is important to note that smart contracts are not limited to financial agreements. They can be applied to various sectors, including supply chain management, healthcare, insurance, and intellectual property rights. With their ability to streamline processes, increase security, and reduce costs, smart contracts have the potential to transform multiple industries.

How Smart Contracts Work

Smart contracts operate on the principles of blockchain technology, utilizing decentralized networks to execute predefined actions when specific conditions are met. Understanding the underlying mechanics of how smart contracts work requires an exploration of their key components and the process of contract execution.

Smart contracts are written in programming languages specifically designed for the blockchain. One popular language is Solidity, used in Ethereum smart contracts. These contracts are stored on the blockchain, allowing for transparency and immutability.

The process typically begins with the creation of a smart contract. The parties involved define the terms and conditions of the agreement, which are then converted into code. This code includes the rules and actions that need to be executed automatically.

Once the smart contract is created, it is deployed onto the blockchain network. This process involves broadcasting the contract to the network’s nodes, which verify and validate the contract. The contract becomes part of a block and is added to the blockchain, making it publicly accessible.

Smart contracts are triggered by predefined conditions called “if-then” statements. These conditions may include factors such as a specific date, a certain value transfer, or the occurrence of a certain event. When the conditions are met, the agreed-upon actions are automatically executed, ensuring the fulfillment of the contract.

For example, consider a smart contract for an insurance policy. The contract may specify that if a certain predefined event, such as a natural disaster, occurs, then a predetermined payout will be automatically sent to the insured party. This process eliminates the need for manual claims processing and speeds up the insurance payout.

Smart contracts rely on the consensus mechanism of blockchain networks. Transactions within the smart contract are verified and validated by multiple nodes in the network. This decentralized verification ensures the integrity of the contract and prevents fraudulent activities.

One key feature of smart contracts is their immutability. Once deployed on the blockchain, the code and terms of the contract cannot be changed. This ensures that all parties involved have a transparent view of the agreement and that it cannot be tampered with.

However, it’s essential to have proper security measures in place, as vulnerabilities in the code can lead to exploits or hacks. Auditing the contract code and implementing best practices for smart contract development is crucial to mitigate these risks.

In summary, smart contracts operate by encoding the terms and conditions of an agreement into code, deploying the contract onto a blockchain network, and automatically executing actions when predefined conditions are met. Through the utilization of blockchain technology, smart contracts streamline processes, enhance transparency, and provide a secure and efficient way to execute agreements.

Benefits of Smart Contracts

Smart contracts offer numerous advantages over traditional contracts, revolutionizing the way agreements are created, executed, and enforced. These benefits include increased efficiency, cost savings, enhanced security, and improved transparency.

One of the key benefits of smart contracts is their ability to streamline processes and increase efficiency. By automating the execution of contract terms, smart contracts reduce the need for manual intervention and the associated administrative tasks. This saves time and ensures accurate and prompt execution of actions.

In addition to efficiency, smart contracts offer significant cost savings. Traditional contracts often incur expenses related to legal fees, intermediary services, and human resources. With smart contracts, these expenses can be greatly reduced or even eliminated altogether. The automation and elimination of middlemen lead to cost savings and increased value for all parties involved.

Security is another crucial advantage of smart contracts. The use of blockchain technology ensures that the terms of the contract are securely stored and cannot be tampered with. The decentralized nature of the blockchain and the immutability of smart contracts eliminate the risk of fraud, manipulation, or unauthorized changes to the agreement. This instills confidence and trust among the participating parties.

Moreover, smart contracts provide increased transparency. Traditional contracts often have information asymmetry, with one party having more knowledge or access to information than the other. Smart contracts, on the other hand, are stored on a distributed ledger, giving all parties equal access and visibility into the terms and actions of the contract. This transparency promotes trust and reduces the potential for disputes or misunderstandings.

Smart contracts also offer the potential for new business models and opportunities. Programmable contracts open up possibilities for innovative products and services. For example, decentralized finance (DeFi) platforms built on smart contracts enable peer-to-peer lending, decentralized exchanges, and other financial services that were previously restricted to traditional intermediaries. These new possibilities create a more inclusive and accessible financial ecosystem.

Furthermore, smart contracts can help streamline complex multi-party agreements. By automating the execution of conditions and actions, smart contracts can simplify and expedite the execution of complex agreements, such as supply chain contracts involving multiple stakeholders. This reduces the risk of errors, delays, and disputes, ultimately improving the efficiency and reliability of these collaborative processes.

In summary, the benefits of smart contracts include increased efficiency, cost savings, enhanced security, improved transparency, the potential for new business models, and streamlined execution of complex agreements. These advantages make smart contracts a promising technology that can revolutionize various industries and transform the way agreements are made and fulfilled.

Challenges and Limitations of Smart Contracts

While smart contracts offer numerous benefits, they also face several challenges and limitations that need to be considered. Understanding these limitations is crucial for the successful implementation and adoption of smart contract technology.

One of the main challenges is the complexity of legal agreements. Not all contracts can be easily encoded into code and automated. Many legal agreements require human interpretation, negotiation, and discretion. Complex legal contracts involving subjective terms, nuanced language, or unforeseen circumstances may be challenging to fully automate with smart contracts.

Another limitation of smart contracts is the reliance on blockchain technology. While blockchain provides security and transparency, it also presents scalability issues. As more contracts are added to the blockchain, the network’s performance may be affected, leading to slower transaction processing times and higher costs. Scalability solutions are constantly being developed, but it remains an ongoing challenge for smart contract adoption at a larger scale.

Furthermore, smart contracts may face regulatory challenges. The existing legal framework in many jurisdictions has not fully caught up with the technology. The legal enforceability of smart contracts and the rights and responsibilities of the parties involved may vary across different jurisdictions. Clear regulations and legal frameworks need to be established to ensure that smart contracts are recognized and enforceable in a consistent and reliable manner.

Smart contracts also face risks related to the quality and security of the code. While smart contract code is intended to be secure and tamper-proof, vulnerabilities and bugs can still exist. If exploited, these vulnerabilities can lead to financial losses or unforeseen consequences. It is crucial to conduct thorough code audits, implement best practices for smart contract development, and regularly update and maintain the contract code to mitigate potential risks.

An additional challenge is the lack of flexibility and adaptability. Once a smart contract is deployed on the blockchain, it becomes immutable and cannot be modified. This lack of flexibility may be problematic if changes or updates to the contract terms are required. Proposed solutions include the development of smart contract upgrade mechanisms or the integration of off-chain or hybrid solutions to allow for more flexibility while maintaining the benefits of blockchain technology.

Lastly, smart contracts may not completely eliminate the need for legal professionals. While they can automate certain aspects of contract management and execution, legal expertise may still be necessary for more complex agreements, dispute resolution, and ensuring compliance with legal and regulatory requirements. Lawyers will likely play a role in assisting with smart contract implementation, auditing, and navigating the legal challenges associated with the technology.

In summary, the challenges and limitations of smart contracts include the complexities of legal agreements, scalability issues with blockchain technology, regulatory challenges, code vulnerabilities, lack of flexibility, and the continued need for legal professionals in certain contexts. Addressing and mitigating these challenges are essential for the widespread adoption and successful implementation of smart contracts.

Impact of Smart Contracts on the Legal Industry

Smart contracts have the potential to significantly impact the legal industry, transforming the way legal agreements are created, executed, and enforced. This disruptive technology is poised to reshape various aspects of the legal profession.

One of the major impacts of smart contracts on the legal industry is the potential reduction in the need for intermediaries, such as lawyers and legal professionals. Smart contracts automate the execution of contractual obligations, eliminating the need for manual intervention and reducing administrative costs. This frees up legal professionals to focus on more complex legal matters and advisory roles, adding value in areas that require human expertise and judgment.

Smart contracts can also streamline the contract management process. With pre-programmed terms and conditions, smart contracts simplify and expedite the creation and negotiation of contracts. Additionally, these contracts provide transparency, ensuring that all parties have access to the same information and reducing the potential for disputes or misunderstandings.

Furthermore, smart contracts have the potential to reduce legal costs. Traditional legal processes often involve lengthy negotiations, revisions, and legal fees. By automating these processes, smart contracts can significantly reduce the time and resources required for contract management. This cost-saving potential can benefit both businesses and individuals, making legal services more accessible and affordable.

Smart contracts can also enhance legal compliance. By enforcing predefined rules and conditions, smart contracts ensure that all parties adhere to their obligations. This can help mitigate legal risks and increase trust between the parties involved. Furthermore, the transparency and immutability of smart contracts provide an auditable trail of actions, which can be useful in resolving disputes or legal challenges.

In addition to its impact on traditional legal processes, smart contract technology opens up new opportunities for the legal industry. The rise of decentralized applications, enabled by programmable smart contracts, has propelled the emergence of blockchain-based legal services. These services include decentralized dispute resolution, automated escrow services, and self-executing wills and trusts. Smart contracts enable the development of innovative legal solutions that were previously not feasible.

However, it is important to note that the impact of smart contracts on the legal industry is still evolving. Challenges related to legal interpretation, regulatory frameworks, code vulnerabilities, and the need for human expertise remain. Lawyers will continue to play a crucial role in providing legal advice, ensuring compliance, and navigating the legal implications of smart contracts.

In summary, smart contracts have the potential to revolutionize the legal industry by automating contract management, reducing costs, enhancing compliance, and enabling the development of innovative legal solutions. While challenges and limitations exist, the impact of smart contracts on the legal profession is likely to be transformative, with lawyers adapting and leveraging this technology to deliver more efficient and value-added legal services.

Roles of Lawyers in a Smart Contract-driven Future

While smart contracts have the potential to automate and streamline various aspects of the legal industry, they do not make lawyers obsolete. Instead, smart contract technology will reshape the roles and responsibilities of lawyers, emphasizing their expertise in complex legal matters and ensuring compliance in a smart contract-driven future.

One essential role that lawyers will play is in the initial setup and implementation of smart contracts. Lawyers can assist clients in understanding the legal implications of using smart contracts and guide them in choosing appropriate templates or frameworks. They can also review and audit smart contract code to ensure compliance with legal and regulatory requirements, mitigating potential risks and vulnerabilities.

Lawyers will also have a vital role in providing legal advice and assistance in negotiating the terms and conditions of smart contracts. While some contracts may be standardized and automated, many complex agreements may still require legal interpretation and negotiation. Lawyers will help clients navigate the intricacies of smart contracts, ensuring that their interests are protected and that the terms align with legal requirements and industry standards.

Furthermore, in dispute resolution, lawyers will continue to play a key role. While smart contracts aim to streamline the execution of contractual obligations, disputes may still arise in cases of non-performance, breaches, or conflicts in interpretation. Lawyers will be responsible for resolving these legal disputes, interpreting the terms of smart contracts and applying the relevant legal framework to reach fair and just resolutions.

Lawyers will also be instrumental in managing the legal implications of smart contracts within existing regulatory frameworks. As technology advances and legislation evolves, lawyers will provide guidance on compliance and regulatory issues related to smart contracts. They will help clients navigate the legal landscape, ensuring that smart contracts are enforceable and recognized within applicable laws and regulations.

Another crucial role for lawyers in a smart contract-driven future is assisting in managing the risks associated with smart contracts. While smart contracts are designed to be secure and tamper-proof, vulnerabilities in code can still exist, and unforeseen circumstances may arise. Lawyers will advise clients on risk management strategies, contractual safeguards, and insurance considerations to mitigate potential risks and liabilities.

Moreover, lawyers will continue to provide a human touch in the legal profession, offering personalized advice and guidance. Despite the automation and efficiency of smart contracts, clients may still require the reassurance and expertise of a lawyer when dealing with complex legal matters. Lawyers will provide strategic advice, creative solutions, and the ability to navigate nuanced legal issues that require human judgment and discretion.

In summary, the roles of lawyers in a smart contract-driven future will evolve to focus on areas that require legal expertise, negotiation skills, interpretation, compliance, risk management, and dispute resolution. While smart contract technology automates certain aspects of the legal process, lawyers will continue to play a crucial role in ensuring the legal validity, ethical application, and proper management of smart contracts in the ever-evolving legal landscape.

Conclusion

Smart contracts have the potential to revolutionize the legal industry, offering a more efficient, transparent, and automated approach to contract management and execution. These self-executing contracts, built on blockchain technology, have numerous advantages, including increased efficiency, cost savings, enhanced security, and improved transparency.

While smart contracts can streamline processes, reduce costs, and improve accuracy, they also present challenges and limitations. The complexities of legal agreements, scalability issues of blockchain technology, regulatory considerations, code vulnerabilities, lack of flexibility, and the need for human expertise in certain contexts all need careful consideration and mitigation.

In a smart contract-driven future, lawyers will play crucial roles in assisting clients with the implementation, negotiation, review, and compliance of smart contracts. They will provide valuable legal advice, mitigate risks, resolve disputes, navigate regulatory frameworks, and add a human touch to the legal profession.

Smart contracts have the potential to reshape the legal industry by transforming traditional contract processes, automating enforcement, and enabling the development of innovative legal solutions. Lawyers adapting to this technology will leverage its benefits while upholding their essential role in providing legal expertise, ensuring compliance, and safeguarding the interests of their clients.

As smart contracts continue to evolve and gain wider adoption, it is important for lawyers to embrace these technological advancements, stay informed about the latest developments, and adapt their skill sets accordingly. By doing so, lawyers will position themselves to thrive in a smart-contract-driven future, delivering more efficient and value-added legal services to clients.