Introduction

Welcome to the world of financial independence, where your investments work hard to provide you with a steady income. Living off investments is a dream for many people, offering the freedom to enjoy life on their own terms. Whether you’re nearing retirement or simply looking for ways to generate passive income, understanding how to make your investments work for you is crucial.

Investing involves putting your money into assets or ventures with the expectation of generating returns. The goal is to accumulate wealth and ultimately have those investments provide a sustainable income stream. However, living off investments requires careful planning, strategizing, and ongoing monitoring to ensure long-term financial stability.

In this article, we will discuss the different types of investments, how to set financial goals and determine your risk tolerance, build a diversified portfolio, manage and monitor your investments, create a passive income stream, and consider tax implications. We will also explore strategies for navigating market volatility and the importance of seeking professional advice. By the end, you should have a clear understanding of how to live off investments and make your money work for you.

Before we delve into the intricacies of living off investments, it’s important to emphasize the significance of proper financial planning. This involves taking stock of your current financial situation, analyzing your expenses and income, and setting realistic financial goals. Understanding your financial goals will help you determine the amount of income you need from your investments to sustain your desired lifestyle. It’s also essential to assess your risk tolerance, as this will influence the types of investments you choose.

Are you ready to embark on the journey of financial independence? Let’s dive in and explore the world of living off investments!

Understanding Different Types of Investments

When it comes to living off investments, it’s essential to have a clear understanding of the different types of investment options available. By diversifying your portfolio and exploring various investment avenues, you can maximize your potential for returns while mitigating risk. Here are some common types of investments to consider:

1. Stocks: Investing in stocks means buying shares of ownership in a company. Stock prices can fluctuate, but historically, they have provided higher returns compared to other types of investments over the long term. It’s important to research and analyze individual companies before investing in their stocks.

2. Bonds: Bonds are debt securities issued by governments, municipalities, or corporations. When you purchase a bond, you are essentially loaning money to the issuer in exchange for regular interest payments and the return of the principal amount at maturity. Bonds are generally considered less risky than stocks, making them a popular choice for income-focused investors.

3. Real Estate: Real estate investments can take various forms, such as rental properties, real estate investment trusts (REITs), or real estate crowdfunding platforms. Real estate has the potential for both income through rental payments and capital appreciation over time.

4. Mutual Funds: Mutual funds pool money from multiple investors to invest in a diversified portfolio of stocks, bonds, or other securities. This allows individual investors to access a broader range of investments without having to create and manage their own portfolios.

5. Exchange-Traded Funds (ETFs): ETFs are similar to mutual funds but trade on stock exchanges like individual stocks. They offer diversification and are often designed to track specific indexes, sectors, or asset classes.

6. Commodities: Commodities include physical substances like gold, silver, oil, or agricultural products. Investors can participate in commodities markets through various investment vehicles, such as futures contracts or commodity ETFs.

7. Cryptocurrencies: Cryptocurrencies like Bitcoin and Ethereum have gained significant popularity in recent years. These digital currencies operate on blockchain technology and offer a decentralized, secure, and potentially high-yield investment option. However, they also come with increased volatility and risks.

It’s important to note that each investment type carries its own level of risk and potential for returns. Diversifying your investment portfolio across different asset classes can help spread risk and achieve a balanced approach. Understanding the characteristics and dynamics of these investments will empower you to make informed decisions and tailor your portfolio to meet your specific financial goals and risk tolerance.

Setting Financial Goals and Risk Tolerance

Before diving into the world of investing, it’s crucial to set clear financial goals and determine your risk tolerance. Setting financial goals allows you to define what you want to achieve through your investments, while understanding your risk tolerance helps you make informed decisions about the level of risk you are comfortable with. Let’s explore these concepts further.

Financial Goals: Think about what you hope to achieve with your investments. Are you saving for retirement, a down payment on a house, or funding your children’s education? Knowing your financial goals will help you establish a roadmap for your investment strategy. It’s crucial to set specific, measurable, achievable, relevant, and time-bound (SMART) goals to stay focused and motivated.

Consider the time horizon for each goal. Short-term goals, such as saving for a vacation, may require investments with lower risk and quicker liquidity. On the other hand, long-term goals, such as retirement planning, offer more flexibility for higher-risk investments that have the potential for greater returns.

Risk Tolerance: Risk tolerance refers to your ability to endure fluctuations in investment value without compromising your financial well-being or emotional stability. Assessing your risk tolerance helps determine the optimal balance between risk and potential returns. Consider the following factors that can influence your risk tolerance:

Time Horizon: The longer your investment horizon, the more time you have to weather market volatility and potentially recover from any losses. This may allow you to have a higher risk tolerance and invest in more aggressive asset classes.

Financial Situation: Take into account your current financial situation, including your income, expenses, and overall net worth. A stable financial position with a surplus of income gives you more flexibility to take on higher-risk investments.

Comfort Level: Consider how comfortable you are with the ups and downs of the market. Some investors may be more risk-averse and prefer conservative investments, while others may be more comfortable with higher-risk investments that offer the potential for greater returns.

Knowledge and Experience: Evaluate your knowledge and experience in investing. If you are new to investing, it may be wise to start with lower-risk options until you gain a better understanding of the market.

It’s important to strike a balance between your financial goals and risk tolerance. If your goals require higher returns, you may need to accept a higher level of risk. Conversely, if preserving capital and minimizing risk is a priority, you may opt for more conservative investments.

Remember that financial goals and risk tolerance can evolve over time, so it’s essential to periodically reassess them and make adjustments to your investment strategy accordingly. Regularly reviewing your goals and risk tolerance will help ensure that your investment portfolio aligns with your changing circumstances and aspirations.

Building a Diversified Investment Portfolio

Building a diversified investment portfolio is a key strategy for managing risk and maximizing returns. Diversification involves spreading your investments across different asset classes, industries, and geographical regions. This approach helps protect your portfolio from the potential negative impact of a single investment and allows you to capture the opportunities presented by different sectors. Let’s explore the steps to building a diversified investment portfolio.

1. Asset Allocation: Determine the appropriate allocation of your investments across different asset classes, such as stocks, bonds, real estate, and commodities. The proportions will depend on your financial goals, time horizon, and risk tolerance. For example, a younger investor with a long-term horizon may have a higher allocation to stocks, while someone nearing retirement may have a higher allocation to bonds.

2. Invest in Different Industries: Within each asset class, consider investing in a variety of industries. This helps diversify your portfolio and reduces the impact of a downturn in any specific sector. Look for companies or sectors that you believe have growth potential and align with your investment goals and risk tolerance.

3. Geographic Diversification: Invest in companies or funds that operate in different geographical regions. This helps mitigate the risks associated with a downturn in one particular economy or region. Investing internationally exposes you to different market dynamics and opportunities for growth.

4. Consider Different Investment Vehicles: Explore different investment vehicles, such as mutual funds, ETFs, and individual stocks or bonds. Each vehicle offers its own advantages and disadvantages in terms of diversification, liquidity, and management fees. A mix of investment vehicles can enhance your portfolio’s diversification and flexibility.

5. Rebalance Regularly: Regularly review and rebalance your portfolio to maintain your desired asset allocation. Over time, certain investments may outperform others, leading to a shift in your original allocation. Rebalancing ensures that your portfolio remains aligned with your investment objectives and risk tolerance.

6. Seek Professional Advice: If you’re unsure about constructing and managing a diversified portfolio, consider seeking guidance from a financial advisor. They can provide personalized advice based on your unique circumstances and help you navigate the complexities of investment diversification.

Remember, diversification does not guarantee profits or protect against losses, but it is an essential risk management strategy. By building a diversified investment portfolio, you can potentially reduce the impact of market volatility and increase your chances of achieving consistent returns over the long term.

Managing and Monitoring Your Investments

Once you have built a diversified investment portfolio, the key to success lies in effectively managing and monitoring your investments. Proper management ensures that your investments align with your financial goals, risk tolerance, and market conditions. Let’s explore some essential practices for managing and monitoring your investments.

1. Keep Track of Your Portfolio: Regularly monitor the performance of your investments. Use tools, such as portfolio tracking software or online brokerage platforms, to stay updated on the value and growth of your portfolio. This allows you to make informed decisions and take timely action when necessary.

2. Review Investment Objectives and Risk Tolerance: Periodically reassess your investment objectives and risk tolerance. As your financial situation or goals change, you may need to adjust your investment strategy. Stay in touch with your long-term goals and ensure that your investments continue to align with them.

3. Evaluate Individual Investments: Regularly evaluate the performance of individual investments within your portfolio. Review their financial health, growth potential, and any news or events that may impact their value. Consider selling underperforming investments and reallocating funds to investments with better prospects.

4. Stay Informed: Keep yourself updated on market trends, economic indicators, and news that may impact your investments. Follow financial news, read industry reports, and stay connected with investment communities or advisors. Being well-informed empowers you to make educated decisions about your investments.

5. Rebalance Your Portfolio: Rebalancing ensures that your investments stay aligned with your desired asset allocation. Regularly review your portfolio and adjust the proportions of different asset classes if necessary. Rebalancing allows you to take profits from investments that have performed well and reinvest in other areas to maintain diversification.

6. Consider Tax Implications: Be aware of the tax implications of your investments. Understand how different investment income, such as dividends or capital gains, are taxed. Consider using tax-efficient investment strategies, such as investing in tax-advantaged accounts like Individual Retirement Accounts (IRAs) or 401(k)s, to minimize your tax liability and maximize your returns.

7. Monitor Fees and Expenses: Pay attention to the fees and expenses associated with your investments. High fees can erode your overall returns over time. Compare expense ratios and transaction costs between different investment options to minimize expenses and maximize your investment performance.

8. Review and Adjust as Necessary: Finally, regularly review your investment strategy and make adjustments as needed. Markets and economic conditions change, and your portfolio should adapt accordingly. Stay proactive in managing your investments to ensure they remain on track.

By effectively managing and monitoring your investments, you can optimize your portfolio’s performance, minimize risks, and stay on track towards achieving your financial goals.

Creating a Passive Income Stream

Creating a passive income stream is a goal for many investors, as it provides a steady stream of income without requiring active involvement or constant attention. Passive income can provide financial stability, flexibility, and the freedom to pursue other interests. Here are some strategies to consider when aiming to create a passive income stream through your investments.

1. Dividend-Paying Stocks: Investing in dividend-paying stocks is one way to generate passive income. Dividends are a portion of a company’s profits distributed to shareholders as cash or additional shares. Look for companies with a history of regular dividend payments and a strong track record. Dividends can provide a consistent income stream while allowing for potential capital appreciation.

2. Rental Properties: Real estate investments, particularly rental properties, can generate passive income through rental payments. Investing in residential or commercial properties can provide a reliable cash flow if managed effectively. Consider factors like location, property type, rental demand, and potential rental income when evaluating rental properties.

3. Real Estate Investment Trusts (REITs): REITs allow investors to pool their money to invest in a diverse portfolio of real estate properties. These properties can include apartments, office buildings, retail spaces, or even infrastructure. REITs offer a convenient way to invest in real estate without the need for direct ownership or property management responsibilities.

4. Peer-to-Peer Lending: Peer-to-peer lending platforms connect borrowers with lenders, cutting out traditional financial institutions. By participating as a lender, you can earn interest on the money you lend, providing a passive income stream. However, it’s important to assess the risks involved and diversify your loans across different borrowers to mitigate potential defaults.

5. Bond Investments: Investing in bonds can provide regular interest payments, generating passive income. Bonds can range from government bonds to corporate bonds, each with varying levels of risk and yield. Consider the creditworthiness of the issuer and the bond’s maturity period when selecting bonds to include in your portfolio.

6. Royalties and Intellectual Property: If you own copyrights, patents, or trademarks, you can earn passive income through licensing or royalty agreements. Intellectual property, such as books, music, or inventions, can generate income without requiring ongoing effort or active management.

7. Investment Funds and ETFs: Investing in income-focused mutual funds or exchange-traded funds (ETFs) can provide exposure to a diversified portfolio of income-generating assets. Such funds typically invest in dividend-paying stocks, bonds, or other income-producing securities. This allows you to benefit from the expertise of professional fund managers while enjoying regular passive income.

Remember that creating a passive income stream requires careful consideration, research, and ongoing monitoring. Assess the risks, evaluate the potential returns, and diversify your investments to minimize risk and maximize income generation. While passive income can offer financial independence, it’s important to allocate your investments wisely and regularly review your strategy to ensure optimal results.

Strategies for Living Off Investments

Living off investments requires careful planning and effective strategies to ensure a consistent and sustainable income stream. Here are some strategies to consider when relying on investments as a primary source of income.

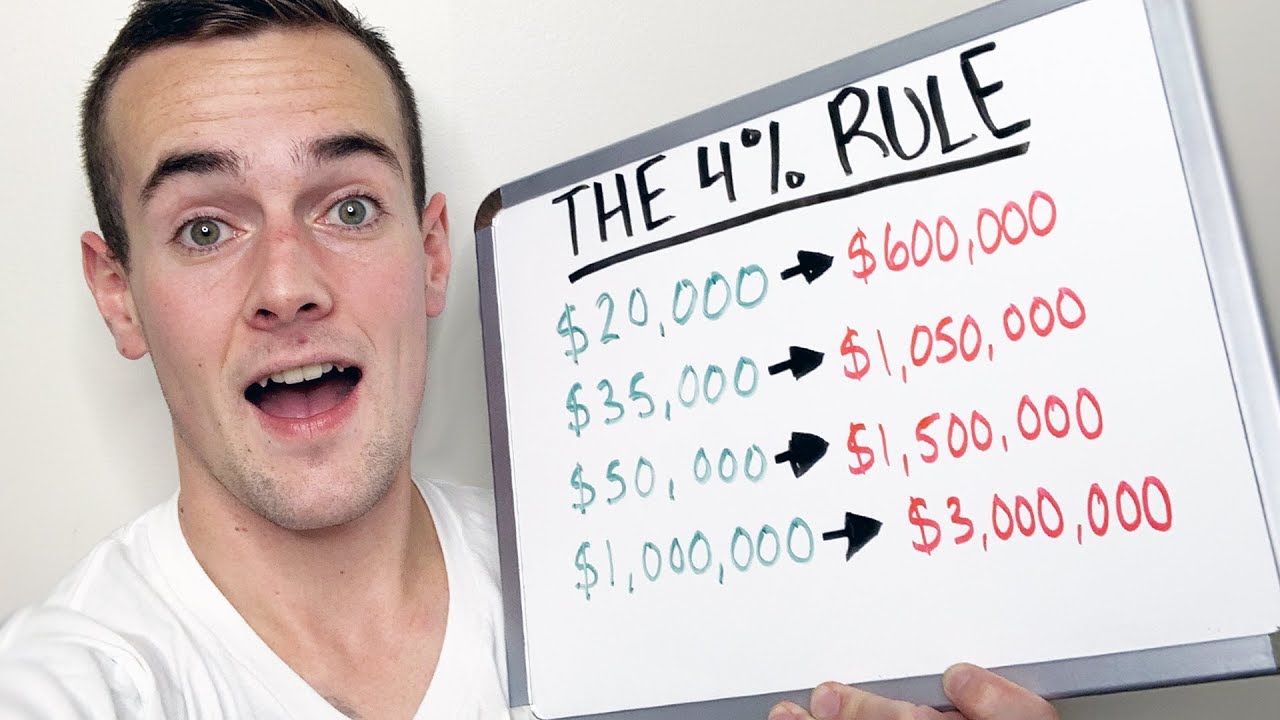

1. Determine Your Withdrawal Rate: Calculate a suitable withdrawal rate from your investment portfolio to cover your living expenses. The general rule of thumb is to withdraw no more than 4% of your portfolio’s value annually. Adjust this percentage as needed, considering factors such as inflation, market conditions, and your projected lifespan.

2. Set Up an Efficient Cash Flow System: Create a cash flow system that efficiently manages your income from investments. Establish a separate bank account for managing living expenses and set up automatic transfers to cover monthly bills. This system will ensure a smooth and organized financial process.

3. Prioritize Stability with Investments: Place a significant portion of your portfolio in stable, income-generating investments to ensure a reliable cash flow. Bonds, dividend-paying stocks, and real estate investments can provide steady income streams. Balance these income-focused assets with higher-risk investments that offer growth potential.

4. Diversify Income Streams: Relying on a single source of income, such as dividends or rental properties, can be risky. Diversify your income streams by investing in different assets and industries. This diversification can safeguard your income against potential downturns or fluctuations in specific sectors.

5. Budget and Prioritize Expenses: Create a comprehensive budget to plan and manage your expenses effectively. Prioritize essential expenses, such as housing, healthcare, and food, before allocating funds for discretionary items. Regularly review and adjust your budget to ensure it aligns with your investment income and financial goals.

6. Consider Supplemental Income: If your investment income is not sufficient to cover all your expenses, consider exploring part-time work or other supplemental income sources. This additional income can bridge any financial gaps while allowing your investment portfolio to grow.

7. Reinvest Dividends and Income: Reinvesting dividends and income generated by your investments can help grow your portfolio over time. By reinvesting, you can capitalize on compounding returns and potentially increase your future income.

8. Stay Mindful of Taxes: Stay informed about tax implications and strategies to optimize your investment income. Understand the tax rules related to capital gains, dividends, and interest income. Consider utilizing tax-advantaged accounts, such as IRAs or 401(k)s, to minimize your tax liability and preserve more of your investment income.

9. Regularly Review and Adjust: Continuously review and adjust your investment strategy based on changing market conditions, financial goals, and life circumstances. Regularly monitor your investments, stay informed about market trends, and consult with a financial advisor when needed.

Living off investments is a long-term endeavor that requires patience, discipline, and sound financial management. By implementing these strategies, you can enhance your financial stability and enjoy the freedom and flexibility that living off investments can provide.

Considering Tax Implications

When living off investments, it is crucial to consider the tax implications of your investment income. Understanding the tax rules and optimizing your tax strategy can significantly impact your after-tax income and overall financial success. Here are some important considerations for managing the tax implications of your investments.

1. Know the Different Types of Investment Income: Investment income can come in various forms, such as dividends, interest, capital gains, and rental income. Each type of income may be subject to different tax rates and rules. Familiarize yourself with the tax treatment of each type of investment income to ensure accurate reporting and effective tax planning.

2. Utilize Tax-Advantaged Accounts: Take advantage of tax-advantaged accounts, such as Individual Retirement Accounts (IRAs) and 401(k)s, to reduce your tax liability. Contributions to these accounts may be tax-deductible or made with pre-tax dollars, allowing your investment income to grow tax-free until withdrawal.

3. Consider Tax-Loss Harvesting: Tax-loss harvesting involves selling investments that have experienced a loss to offset gains and minimize your taxable income. By strategically selling securities, you can generate capital losses that can be used to offset capital gains or even reduce ordinary income up to a certain limit.

4. Understand Capital Gain Tax Rates: Capital gains tax rates vary based on the holding period of the investment. Short-term capital gains, from investments held for one year or less, are typically taxed at ordinary income tax rates. Long-term capital gains, from investments held for more than a year, may qualify for lower tax rates. Be aware of these rates to optimize the timing of your investment sales.

5. Be Mindful of Dividend Taxes: Dividend income is subject to different tax rates depending on whether they are classified as qualified or non-qualified dividends. Qualified dividends are generally taxed at lower capital gains tax rates, while non-qualified dividends are taxed at ordinary income tax rates. Understanding the distinction can help you plan your income and reduce your tax liability.

6. Plan for Required Minimum Distributions (RMDs): If you have tax-deferred retirement accounts like traditional IRAs or 401(k)s, be aware of the requirement to take minimum distributions starting at a certain age. Failing to comply with RMD rules can result in significant penalties. Consider the impact of RMDs on your tax liability and overall financial planning.

7. Consult with a Tax Professional: Tax rules can be complex and subject to change. Consider consulting with a tax professional who can provide personalized advice based on your specific financial situation and investment portfolio. They can help you optimize your tax strategy and ensure compliance with applicable tax laws.

8. Keep Records and Documentation: Maintain thorough records of all your investment-related transactions and expenses. Keep track of purchase and sale dates, cost basis, and any related expenses. These records will make it easier to accurately report your investment income and deductions when filing your tax returns.

By considering the tax implications of your investments and implementing effective tax planning strategies, you can minimize your tax liability and maximize your after-tax income. Taking the time to understand and manage the tax aspects of your investments is a crucial step in achieving long-term financial success.

Dealing with Market Volatility

Market volatility is an inevitable part of investing. Prices fluctuate, economic conditions change, and investor sentiment can sway the market. Dealing with market volatility is essential for managing your investments effectively and staying focused on your financial goals. Here are some strategies to consider when navigating through uncertain and volatile market conditions.

1. Maintain a Long-Term Perspective: Keep a long-term perspective when investing. While short-term market fluctuations can be unpredictable and unnerving, remember that investing is a journey that spans years or even decades. Historically, markets have recovered and delivered positive returns over the long term, even in the face of downturns and volatility.

2. Diversify Your Portfolio: Diversification is a fundamental strategy for reducing risk in your investment portfolio. By spreading your investments across different asset classes, industries, and geographical regions, you can potentially minimize the impact of a single investment or sector experiencing volatility. Diversifying your holdings helps provide stability and balance in uncertain market conditions.

3. Avoid Emotional Decision-Making: It’s easy to get caught up in the emotional roller coaster of market volatility. However, making investment decisions based on fear or panic can lead to poor choices. Instead, focus on your investment strategy and long-term goals. Avoid knee-jerk reactions and adhere to your planned investment strategy.

4. Review Your Portfolio Regularly: Regularly review your investment portfolio to ensure it aligns with your goals and risk tolerance. Market conditions may prompt the need for rebalancing your portfolio to maintain your desired asset allocation. Regular monitoring allows you to make informed decisions based on the current market environment.

5. Consider Dollar-Cost Averaging: Implementing a dollar-cost averaging strategy can help mitigate the impact of short-term market volatility. By consistently investing a fixed amount at regular intervals, you buy more shares when prices are low and fewer shares when prices are high. This method can help smooth out the effects of market fluctuations over time.

6. Keep Cash Reserves: Maintaining a cash reserve is wise, especially during periods of increased market volatility. Having readily available cash allows you to take advantage of potential investment opportunities that may arise during market downturns. It also provides peace of mind and helps cover unexpected expenses without having to liquidate investments at unfavorable times.

7. Stay Informed and Seek Professional Advice: Stay informed about market trends, economic indicators, and news that may impact your investments. Be aware of any changes in regulations or economic policies that may influence market behavior. Consider seeking professional advice from a trusted financial advisor who can provide guidance tailored to your investment objectives and risk tolerance.

8. Invest for the Long Term: Focus on strategies that align with long-term investing principles such as growth or value investing. These approaches prioritize the long-term potential of investments rather than short-term market fluctuations. Remember that investing should be viewed as a marathon, not a sprint.

Market volatility is an inherent feature of investing, and learning to navigate through it is critical for long-term investment success. By diversifying your portfolio, staying disciplined, maintaining a long-term perspective, and seeking professional advice when needed, you can effectively manage market volatility and stay on track towards your financial goals.

Seeking Professional Advice

When it comes to managing your investments and securing your financial future, seeking professional advice can greatly benefit you. Financial advisors have the knowledge, expertise, and experience to provide valuable guidance tailored to your unique circumstances and goals. Here are some reasons why seeking professional advice is essential in your investment journey.

1. Expertise and Knowledge: Financial advisors have in-depth knowledge of investment strategies, financial planning, and market dynamics. They stay up to date with the latest trends and regulatory changes. Their expertise allows them to assess your financial situation, identify potential risks, and recommend appropriate investment opportunities.

2. Personalized Financial Planning: A financial advisor can work closely with you to develop a personalized financial plan that aligns with your goals and risk tolerance. They will consider your current financial situation, income, expenses, retirement goals, and other factors to create a comprehensive plan that addresses your unique needs.

3. Portfolio Management and Diversification: Financial advisors can help you build and manage a diversified investment portfolio that aligns with your financial goals. They analyze your risk tolerance, time horizon, and income needs to develop an asset allocation strategy suited to your circumstances. By diversifying your investments, they aim to maximize returns and mitigate risk.

4. Behavioral Coaching: Emotions play a significant role in investment decisions. Fear, greed, and impulsive reactions can lead to poor choices. A financial advisor acts as a behavioral coach, helping you stay disciplined and avoid irrational investment decisions during turbulent market conditions. Their guidance can help you navigate through emotions and focus on long-term goals.

5. Tax Efficiency: Financial advisors understand the complexities of the tax system and can help you optimize your tax strategy. They suggest investment options that may result in lower tax liability, such as utilizing tax-advantaged accounts, capitalizing on tax-loss harvesting opportunities, and maximizing deductions. Their expertise can help increase your after-tax returns.

6. Retirement Planning: Planning for retirement involves careful consideration of factors such as income sources, lifestyle goals, healthcare expenses, and longevity. A financial advisor can help you develop a comprehensive retirement plan that incorporates investments, social security, and other income streams. They provide guidance on withdrawal strategies, tax-efficient retirement income, and adjusting your plan as circumstances change.

7. Regular Monitoring and Rebalancing: Financial advisors provide ongoing monitoring of your investments. They review market conditions, assess your portfolio’s performance, and make adjustments as needed. Regular monitoring allows them to take advantage of opportunities and make strategic changes to keep your portfolio on track.

8. Peace of Mind: Ultimately, seeking professional advice offers peace of mind. Knowing that a knowledgeable advisor is overseeing your investments and providing proactive guidance can alleviate stress and uncertainty. You can focus on other aspects of your life, knowing that your financial matters are in capable hands.

While seeking professional advice comes with a cost, the benefits of their expertise, personalized guidance, and peace of mind are invaluable. A financial advisor can be a trusted partner in helping you achieve your financial goals, navigate market complexities, and make sound investment decisions for a secure and prosperous future.

Conclusion

Living off investments is a goal that requires careful planning, strategic decision-making, and ongoing monitoring. By understanding different types of investments, setting financial goals, managing risk tolerance, and building a diversified portfolio, you can create a solid foundation for generating income from your investments.

Strategies such as creating a passive income stream, considering tax implications, dealing with market volatility, and seeking professional advice are essential components of a successful investment journey. Passive income sources like dividends, rental properties, and interest payments can provide a consistent stream of income, while understanding tax rules and optimizing your tax strategy can enhance your after-tax income.

Market volatility is an inevitable part of investing, but by staying focused, diversifying your portfolio, and seeking professional advice, you can navigate through uncertain times and avoid making emotional decisions. Regularly monitoring and adjusting your investments, budgeting effectively, and staying informed about market trends are all crucial components of managing your investments.

In conclusion, living off investments requires a well-thought-out strategy, discipline, and ongoing attention. By implementing these strategies and staying committed to your financial goals, you can increase your chances of achieving long-term financial independence and enjoying the freedom that comes with it.