Technology has a way of making even smart people seem stupid. Often the names of advanced technologies appear to be in some foreign and unfathomable language. In reality, many of these technologies aren’t that complicated once someone explains to you what they are. A good example of this is a blockchain.

You may have heard the term “blockchain” banded with cryptocurrencies such as Bitcoin. Often, the word seems almost synonymous with digital currencies. Blockchains were created for cryptocurrencies. However, their applications go far beyond them. Even if you have no intention of buying or using cryptocurrencies, the multiple applications of blockchain technology may positively impact your life one day.

In this blockchain 101 primer, we will give you an introduction and guide to understanding “how blockchain works”. We will also describe how technology is affecting a myriad of important industries. At the same time, we will tell you how it may change your life for the better.

What Is Blockchain?

To truly understand what blockchain is, you must first understand why it was created.

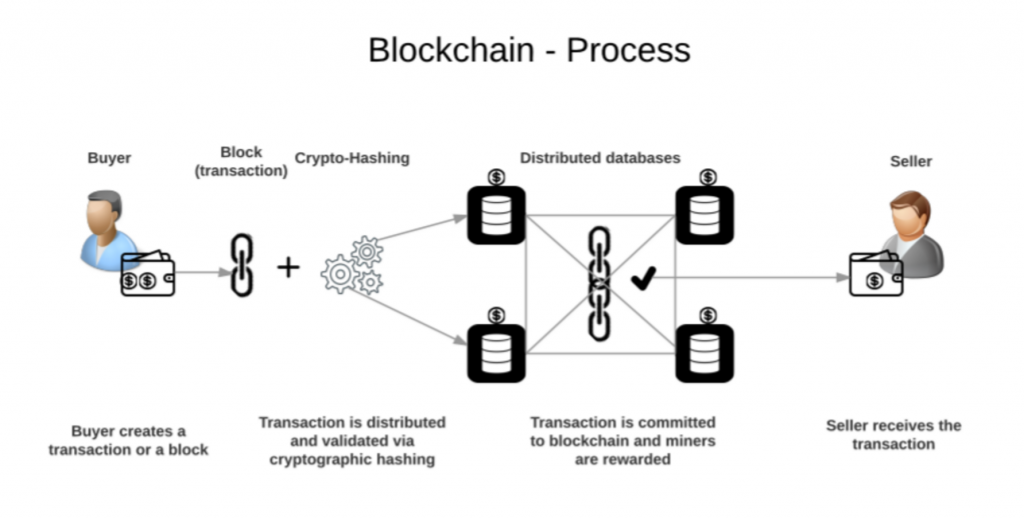

Bitcoin was the first cryptocurrency. By far, it is the most popular digital currency. However, it was not the first attempt to create a digital currency. What held others back from mainstream acceptance was a flaw called double-spending in which a digital token representing money could be spent more than once. The creator of Bitcoin developed blockchain. It was created specifically to solve double-spending. Moreover, it did so without the need of any central authority.

A blockchain gets its name from the fact that, in form, it is a chain of transaction blocks. This sounds complicated, but it is quite simple. You can look at a blockchain as being nothing more than a financial ledger. However, instead of keeping this ledger in a book, it is stored digitally and distributed over many independent computer servers that are also known as decentralized nodes. Each of these nodes keeps the same digital ledger. Moreover, each of these nodes confirms every single transaction made to the ledger. Additionally, these nodes prevent any changes to transactions that are already in the ledger. It also provides equal access to data stored in the ledger for all participants.

The distributed nature of blockchains makes it impossible for anyone, individual or entity, to control or manipulate ledger data. All other nodes will contradict and disavow any changes made to the ledger if a hacker had compromised a node or a node owner had malicious intent to it.

Blockchain: Powering The Future

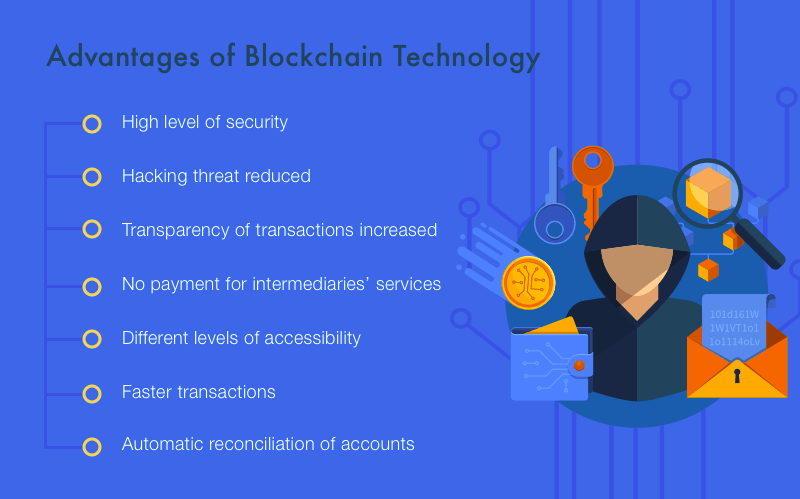

Everyone can trust the data kept within a blockchain. Moreover, they needn’t rely on any third party to provide this trust. This technology has helped cryptocurrencies to explode in popularity. Owners of these currencies know that no government, corporation, or individual has control over their money. This same technology has also led to an explosion of other authority-less applications.

Another key benefit of blockchain technology is transparency. Most blockchains, such as the one that underlies Bitcoin, uses a public blockchain. This means that anyone with access to the Internet can view every single transaction made to the ledger. In the case of Bitcoin, you can trace every Bitcoin from the time it was first created until the time it passed to its current owner. Even in a private blockchain, all participants have equal access to the ledger and can track all transactions made to it.

Why Non-Cryptocurrency Organizations Are Using Blockchain Technology?

Blockchain technology was designed specifically for cryptocurrencies such as Bitcoin. While these currencies rely on blockchains, organizations in both the private and public sectors quickly saw that they could apply the technology to solve a wide range of problems that had nothing to do with cryptocurrencies.

For many private-sector organizations, the decentralized nature of blockchains and its immutable and verifiable data means that they can use them to reduce the need for third parties to act as a counterparty to contractual obligations between two parties. Some organizations also see blockchains as a means to automate complex processes and reduce the need for creating and maintaining vast amounts of paperwork. Many large organizations are further using blockchains to track the distribution of goods and services, from the time of their creation until they reach their end-user.

For public-sector organizations, the prime benefit of blockchain technology is transparency. By placing important public information on a publicly accessible blockchain, all citizens can not only access this information but also trust it. A blockchain allows people to hold their government and the people who work for it more accountable.

The Applications Of Blockchain Technology

Blockchain technology is relatively new. Despite many organizations being naturally skeptical of new technologies, it has already been applied (or is in the process of being applied) in a wide variety of real-world applications outside of cryptocurrencies. These include the following:

Smart Contracts

Smart contracts are legal obligations between two entities. They are created and executed completely in computer code. Moreover, they allow these entities to track and enforce these obligations without the use of any third parties, including the judicial system. Many smart contracts also implement automated escrow payments in digital currency to complete the contract. This can dramatically reduce contract-related transaction costs. Moreover, it can increase the speed of contract execution.

Ethereum is currently the second-largest cryptocurrency by market capitalization. It was created specifically to facilitate these contracts. Many other cryptocurrencies, including Bitcoin, can support them as well.

Supply Chain Management

Major international corporations, such as Nestle and Walmart, have been developing applications that use blockchain technology for supply chain management. This allows them to track the entire chain of the products they sell. This starts from raw materials to work-in-progress inventory, all the way to their sale. Their systems do all this while providing data access to all interested parties, such as their business partners. Blockchains can also improve the auditing of these supply chains. This allows companies to find inefficiencies that they would have never found otherwise.

IBM has even developed various products to let companies quickly and easily build blockchain-based supply chain management systems. The Blockchain in Transport Alliance has been developing standards for these systems.

Financial Services

Blockchains are used to create and execute smart contracts. Moreover, in the development of systems that will settle stock trades, they also use Blockchain. A traditional settlement of trade can take many days. However, the use of a blockchain can reduce this wait to nothing. This is because the executing, clearing, and settling of trade takes place at the time of the trade. Additionally, it does all this without sacrificing any security. Blockchain-based settlement systems can also significantly reduce the cost of settling trades.

Settlement systems are being developed for the settlement of stock trades. Furthermore, it is also developed for the settlement of other types of securities, such as bonds.

Other forms of blockchain-based financial services systems include:

- Cross-Border Payment Systems

- Auditing Systems

- Regulatory Compliance Systems

Digital Voting

As stated previously, blockchains are not just for private companies or financial gain. Governments all around the world are using blockchain technology. They are using it to create applications that register various forms of public data. One of the most promising of these applications is digital voting.

In many parts of both the developed and the developing world, voter fraud is a major issue. However, many localities are building systems that use blockchain technology. These help them eliminate problems while providing the public with unprecedented transparency and trust.

How Will Blockchain Technology Benefit You

Not everyone gets rich from the Internet. However, technology is benefitting everyone. You can see this benefit every time you perform a search for information that would have been difficult (if not impossible) to collect. It also helps when you want to book rideshare or a bed & breakfast using your phone. Blockchain technology will benefit you in many ways even if you do not make millions from investing in it.

One of the biggest ways blockchain technology will benefit you is in the transaction fees you pay for bank accounts, money transfers, and escrow services. This is because the elimination of intermediary third parties will reduce the cost of these fees significantly. But this is just the beginning.

Joe Duran, the founder and CEO of United Capital, believes that in a decade from now, every transaction you make will involve a blockchain. This will make transactions cheaper, faster, and more secure than ever before. A recent survey by accounting and consulting powerhouse, PricewaterhouseCoopers, backs Duran’s assertion. It indicates that nearly 85% of companies are actively developing blockchain solutions. Furthermore, this will increase in the coming years.