Introduction

With the rise in popularity of mobile payment apps, Venmo has become a household name for convenient money transfers. However, it’s important to examine the potential drawbacks and consider the reasons why you shouldn’t use Venmo as your primary payment method. While Venmo offers ease of use and seamless transactions, there are several factors that might make you think twice about relying on this platform.

In this article, we will explore some of the main concerns surrounding Venmo, including the lack of buyer/seller protection, privacy issues, security vulnerabilities, hidden fees, inconvenient transfer limits, and difficulties with customer support. By uncovering these drawbacks, we aim to provide you with a holistic view of the platform and suggest alternative options that might better suit your needs.

While it’s true that Venmo has its advantages, it’s crucial to be informed about its limitations and potential risks. Let’s delve into each of these concerns and evaluate whether Venmo is the right choice for you.

Lack of Buyer/Seller Protection

One of the main reasons why you should think twice before using Venmo is its lack of buyer/seller protection. Unlike other payment platforms, such as PayPal, Venmo does not offer the same level of security when it comes to disputes and fraudulent transactions.

When you make a payment through Venmo, the funds are instantly transferred from your bank account or linked credit/debit card. However, once the transfer is completed, there is little recourse if the transaction goes wrong. If you encounter an issue with a seller, such as receiving a damaged item or not receiving the item at all, Venmo does not offer a formal dispute resolution process to help you recover your money.

Additionally, if you are a seller, you are also at risk of fraudulent buyers who may claim that they never received the item even though they did. Without proper buyer/seller protection, you may be left without any means to resolve the dispute and recover your funds.

It’s important to note that Venmo’s terms of service clearly state that the platform should not be used for commercial transactions. While many users still engage in buying and selling activities, it’s essential to understand that Venmo is primarily designed for peer-to-peer payments between friends and family. As a result, Venmo offers limited protection for commercial transactions, leaving users vulnerable to potential scams or disputes.

Therefore, if you frequently engage in online purchases or sales, it’s advisable to consider alternative payment platforms that provide stronger buyer/seller protection and dispute resolution mechanisms.

Privacy Concerns

Another significant issue with using Venmo is the potential privacy concerns surrounding the platform. Venmo operates as a social payment app, allowing users to see and interact with each other’s payment activity through a social feed.

While the social aspect of Venmo can be fun and engaging for some, it also means that your financial transactions are visible to others by default. This level of transparency may make some users uncomfortable, especially when it comes to sensitive or personal transactions.

Although Venmo offers privacy settings that allow users to limit the visibility of their transactions to varying degrees, the default setting is set to public, meaning that anyone on the platform can see your payment history unless adjusted. This lack of privacy control can be a cause for concern, particularly if you prefer to keep your financial transactions private.

Furthermore, Venmo collects and analyzes user data to personalize the user experience and offer targeted advertisements. While this is a common practice among many online platforms, it raises questions about the security and privacy of your personal information.

It’s important to weigh the convenience of using Venmo against your privacy concerns. If you prioritize keeping your financial transactions private, you may want to explore alternative payment methods that offer more robust privacy features.

Security Vulnerabilities

When it comes to financial transactions, security should always be a top priority. Unfortunately, Venmo has faced several security vulnerabilities in the past, raising concerns about the safety of user data and funds.

One of the most notable concerns is the potential for unauthorized access to your Venmo account. If your Venmo account is compromised, unauthorized individuals may be able to access your linked bank account or credit/debit card information, putting your finances at risk.

In addition, there have been instances of fraudulent transactions and scams targeting Venmo users. These scams often involve phishing attempts or fraudulent sellers who exploit the lack of buyer/seller protection on the platform. If you fall victim to a scam, you may find it challenging to recover your funds.

Venmo has taken steps to improve security measures, such as offering two-factor authentication and encouraging users to enable PIN or fingerprint authentication. However, it’s important to be aware of the potential risks and take necessary precautions to protect your account.

It’s recommended to regularly monitor your Venmo account for any unauthorized activity, use strong and unique passwords, and avoid clicking on suspicious links or sharing sensitive information. Additionally, consider using additional security measures, such as a virtual private network (VPN), when accessing Venmo from public Wi-Fi networks.

If security is a top concern for you, it might be worth exploring alternative payment methods that have a stronger reputation for robust security measures and a proven track record of protecting user data.

Hidden Fees

While Venmo is celebrated for its simplicity and ease of use, it’s important to be aware of the potential hidden fees associated with using the platform. While Venmo itself does not charge any fees for standard transactions, there are certain scenarios where you may encounter unexpected charges.

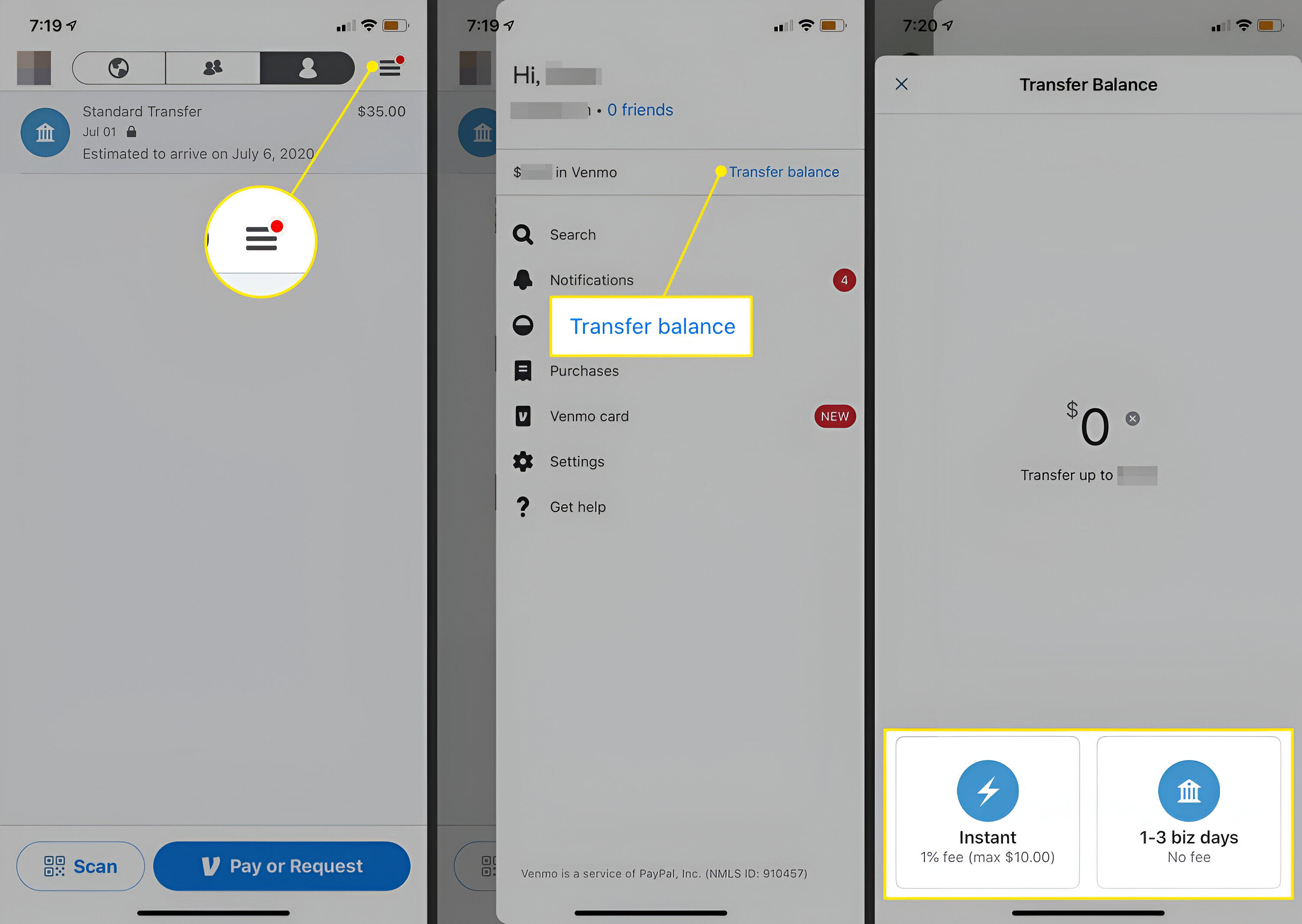

One of the primary sources of hidden fees on Venmo is the use of credit cards for transactions. When you use a credit card to send or receive money, Venmo imposes a 3% fee on the total transaction amount. This fee can quickly add up, especially for larger transactions.

Additionally, if you choose to transfer your Venmo balance to your bank account instantly, rather than waiting for the standard transfer timeframe, Venmo charges a 1% fee with a minimum fee of $0.25 and a maximum fee of $10 per transaction.

These hidden fees can come as an unwelcome surprise and significantly impact your overall transaction costs. It’s crucial to fully understand the fee structure of Venmo and carefully consider the costs associated with using certain payment methods or opting for expedited transfers.

If you’re concerned about hidden fees and wish to avoid additional charges, it may be worthwhile to explore other payment platforms that offer more transparent and competitive fee structures.

Inconvenient Transfer Limits

Another factor to consider when using Venmo is the inconvenience of transfer limits imposed by the platform. While Venmo allows you to send and receive money with ease, there are certain limits on how much you can transfer within a given time period.

Initially, Venmo sets a weekly rolling limit on the amount of money you can send and receive. This limit may vary depending on various factors, including your account verification status and transaction history. These limits are in place to mitigate the potential for fraudulent activity and maintain the security of the platform.

For most users, the initial weekly limit is set at $299.99. However, this limit can be increased up to $4,999.99 by verifying your identity and confirming additional financial information.

While these limits may suffice for everyday transactions or payments among friends, they can be quite restrictive for larger transactions, such as paying rent or making significant purchases. If you find yourself frequently exceeding the transfer limits, you may be inconvenienced by having to split payments or seek alternative payment methods.

Furthermore, even with the increased transfer limit, there is still a cap on the maximum single transaction amount. Venmo imposes a maximum transaction limit of $4,999.99, which may not be sufficient for certain high-value transactions.

If you anticipate needing to make larger transactions on a regular basis, it’s worth considering alternative payment platforms that offer higher transfer limits or have more flexible options to accommodate your financial needs.

Difficulties with Customer Support

One common complaint among Venmo users is the difficulties they encounter when trying to reach customer support. While Venmo offers a customer support team to address user inquiries and issues, getting timely and satisfactory assistance can be a challenge.

The primary method of contacting Venmo’s customer support is through an email support system. Users can submit their questions or concerns via email and are typically provided with a response within a few business days. However, the lack of immediate assistance can be frustrating, especially when users are facing urgent issues or require immediate resolution.

Additionally, Venmo does not offer a direct customer support phone line, which can further compound the frustration for users seeking real-time assistance. This lack of accessible customer support channels can leave users feeling ignored or left without a clear avenue for resolution.

Furthermore, there have been reports of users experiencing difficulties in resolving disputes or issues with transactions. The limited buyer/seller protection, combined with the challenges of reaching customer support, can make it especially frustrating for users who encounter problems with their payments.

If having prompt and efficient customer support is important to you, it may be worth considering alternative payment platforms that offer more accessible and responsive customer service channels.

Alternatives to Venmo

If the concerns surrounding Venmo have made you reconsider using the platform, there are several alternative payment options available that offer different features and may better suit your needs. Here are a few popular alternatives to consider:

PayPal: PayPal is one of the most well-known and widely used payment platforms. It offers strong buyer/seller protection, robust security measures, and a user-friendly interface. PayPal allows you to send and receive money, make online purchases, and even transfer funds internationally.

Zelle: Zelle is a popular peer-to-peer payment service that allows users to send and receive money directly from their bank accounts. It offers fast and secure transactions and is widely supported by many major banks in the United States.

Google Pay: Google Pay is a mobile payment and digital wallet platform that allows you to make payments online, in-app, and in-person. It offers simplicity, security, and seamless integration with other Google services.

Apple Pay: If you’re an Apple user, Apple Pay is a convenient option that allows you to make secure payments using your iPhone, iPad, or Apple Watch. It offers strong security features and is compatible with a wide range of retailers and services.

Cash App: Cash App, also known as Square Cash, is a popular mobile payment app that allows you to send and receive money, make purchases, and even invest in stocks and Bitcoin. It offers a user-friendly interface, quick transfers, and includes a Visa debit card for easy spending.

These are just a few examples of alternative payment platforms available in the market. Each platform has its own unique features, strengths, and weaknesses. It’s important to evaluate your specific needs, such as security, buyer/seller protection, and convenience, and choose the platform that best aligns with your requirements.

Conclusion

While Venmo offers a convenient and user-friendly platform for transferring money between friends and family, there are several significant factors to consider before relying on it as your primary payment method. The lack of buyer/seller protection, privacy concerns, security vulnerabilities, hidden fees, inconvenient transfer limits, and difficulties with customer support can all be important considerations when evaluating Venmo’s suitability for your financial needs.

If you frequently engage in commercial transactions, require stronger buyer/seller protection, or value enhanced privacy, it may be wise to explore alternative payment platforms such as PayPal, Zelle, Google Pay, Apple Pay, or Cash App. These platforms often provide additional security measures, robust customer support, and greater flexibility to accommodate your specific requirements.

Ultimately, the decision of whether or not to use Venmo depends on your individual preferences and priorities. It is crucial to weigh the benefits and drawbacks of the platform and consider alternative options that better align with your financial goals and preferences.

By making an informed decision and choosing the payment method that best suits your needs, you can ensure a secure and seamless financial experience while minimizing potential risks and inconveniences.