Introduction

Welcome to the fascinating world of blockchain technology. Over the years, you may have heard the term “blockchain” thrown around in various contexts, but what exactly is it? In this article, we will provide a simple and straightforward explanation of blockchain to help you understand its significance and potential.

Blockchain is a revolutionary technology that has gained immense popularity and is transforming industries across the globe. It is the underlying technology behind cryptocurrencies like Bitcoin, but its applications extend far beyond digital currencies.

At its core, blockchain is a decentralized, distributed ledger that records transactions and ensures transparency and security. Unlike traditional centralized systems, where a single authority controls and validates transactions, blockchain operates on a peer-to-peer network.

Every transaction made on the blockchain is grouped together in a “block” and added to a chain of existing blocks. Each block contains a unique cryptographic hash, a digital fingerprint that verifies the integrity of the data it holds.

One of the defining characteristics of blockchain is its immutability. Once a block is added to the chain, it becomes nearly impossible to alter or tamper with the information it contains. This makes blockchain highly secure and resistant to fraud or unauthorized modifications.

The decentralized nature of blockchain also ensures that no single entity has control over the entire network. Instead, all participants in the network have a copy of the blockchain, ensuring transparency and preventing any single point of failure.

Blockchain technology has the potential to revolutionize various industries, including finance, supply chain management, healthcare, and more. Its ability to provide secure, transparent, and efficient transactions without the need for intermediaries has captured the attention of businesses and governments worldwide.

In the following sections, we will delve deeper into how blockchain works, its key features, the benefits it offers, and some of its real-world applications. So, fasten your seatbelts as we embark on a journey to unravel the mysteries of blockchain!

What is Blockchain?

Blockchain is a decentralized, distributed ledger technology that enables the secure recording, storing, and verification of transactions across multiple computers or nodes. It eliminates the need for intermediaries, such as banks or government institutions, by using cryptographic algorithms to validate and authenticate transactions. Blockchain is designed to deliver immutability, transparency, and security.

At its core, blockchain is a chain of blocks, where each block contains a list of transactions. These blocks are linked together using cryptographic hashes, creating an interconnected and tamper-proof chain. Each block contains a unique identifier called a cryptographic hash, which is generated based on the data within the block and the hash of the previous block.

When a new transaction occurs, it is added to a new block and broadcasted to all nodes on the network. The nodes in the network verify the transaction using complex algorithms and reach consensus on its validity. Once validated, the block is added to the existing blockchain, becoming a permanent part of the ledger.

One of the key features of blockchain is its decentralization. Unlike traditional systems that rely on a central authority, blockchain operates on a peer-to-peer network, where all participants have equal access and control over the blockchain. This decentralized structure ensures that no single entity has control over the entire network, making it resistant to censorship and attacks.

Another important characteristic of blockchain is its immutability. Once a block is added to the chain, it becomes nearly impossible to alter or delete the information it contains. This is achieved through cryptographic hashes and the distributed nature of the blockchain. Tampering with a block would require tremendous computational power, making it economically and technically infeasible.

Blockchain technology has evolved beyond its initial use in cryptocurrencies. It has found applications in various industries, including finance, supply chain management, healthcare, real estate, and more. By leveraging blockchain, businesses can streamline processes, enhance security, reduce costs, and increase transparency.

In the next section, we will explore how blockchain works in more detail, uncovering the mechanics behind its decentralized and secure nature.

How Does Blockchain Work?

Blockchain technology operates on a complex system of algorithms and protocols that enable its decentralized and secure nature. Understanding how blockchain works requires exploring its key components and processes:

1. Distributed Ledger: Blockchain utilizes a distributed ledger that is maintained across multiple nodes or computers. Each participant in the network has a copy of the entire blockchain, ensuring redundancy and transparency. This distribution of the ledger prevents a single point of failure and makes it difficult for hackers to manipulate the data.

2. Consensus Mechanisms: To validate and agree on the authenticity of transactions, blockchain employs consensus mechanisms. These mechanisms ensure that all nodes in the network reach agreement on the validity of a transaction before it is added to the blockchain. Popular consensus mechanisms include Proof of Work (PoW) and Proof of Stake (PoS).

3. Cryptographic Hashing: Blockchain uses cryptographic hashing algorithms to create unique identifiers for each block and secure the data within it. A hash is a fixed-length string of characters generated by applying the algorithm to the block’s data. Any modification to the data will result in a different hash, making it easily detectable.

4. Block Creation and Linking: Transactions are grouped together in blocks, which are added to the blockchain. Blocks are created through a process known as mining, where powerful computers solve complex mathematical puzzles. Once a block is mined, it is linked to the previous block using the hash value, creating an immutable and chronological chain of blocks.

5. Decentralization and Consensus: Blockchain’s decentralized nature ensures that no single entity has control over the network. All participants, or miners, in the network work together to validate transactions and reach consensus on their validity. This eliminates the need for a central authority and prevents manipulation or censorship of data.

6. Security and Immutability: Blockchain’s security is achieved through the combination of cryptographic hashing, consensus mechanisms, and distributed ledger. Once a transaction is added to the blockchain, it becomes nearly impossible to alter or delete. This immutability ensures data integrity and prevents fraudulent or unauthorized changes.

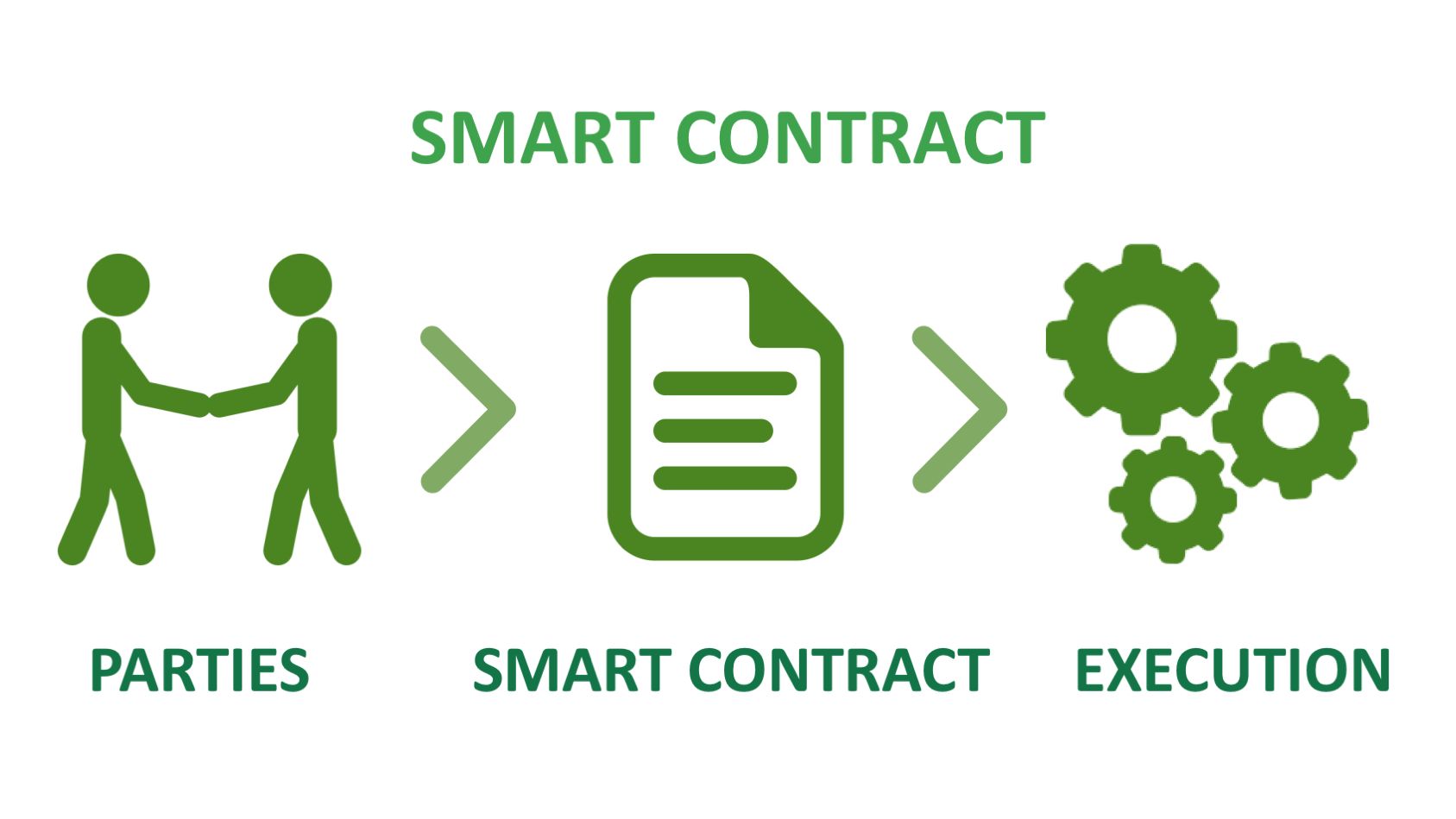

7. Smart Contracts: Smart contracts are self-executing contracts programmed onto the blockchain. They automatically execute predefined actions when specific conditions are met. Smart contracts enable the automation of complex processes and reduce the need for intermediaries, increasing efficiency and trust.

By leveraging these components and processes, blockchain provides a transparent, secure, and efficient platform for conducting transactions and storing data. In the next section, we will explore the key features of blockchain that make it a powerful tool for various industries.

Key Features of Blockchain

Blockchain technology offers several key features that make it a powerful tool for various industries. Let’s explore some of the fundamental characteristics of blockchain:

1. Decentralization: One of the most significant features of blockchain is its decentralized nature. Unlike traditional systems that rely on a central authority, blockchain operates on a peer-to-peer network where all participants have equal access and control over the blockchain. This decentralization ensures transparency, prevents a single point of failure, and reduces the risk of censorship or manipulation.

2. Transparency: Blockchain provides transparency by making the transaction history accessible to all participants in the network. Each transaction is recorded on the blockchain, creating an immutable and auditable ledger. This transparency not only enhances trust among participants but also enables real-time tracking and verification of transactions.

3. Security: Security is a crucial feature of blockchain technology. Blockchain utilizes advanced cryptographic algorithms to ensure the integrity and confidentiality of data. The immutability of the blockchain makes it highly resistant to tampering or unauthorized modifications. Additionally, the distributed nature of the blockchain makes it difficult for attackers to compromise the network.

4. Immutability: Once a transaction is added to the blockchain, it becomes nearly impossible to alter or delete. Each block contains a unique cryptographic hash, which is generated based on the data within the block and the hash of the previous block. Therefore, any tampering with a block would require altering the entire chain, which is computationally infeasible. This immutability ensures the integrity and reliability of the data stored on the blockchain.

5. Efficiency: Blockchain has the potential to significantly improve the efficiency of various processes. By eliminating intermediaries and automating trust through smart contracts, blockchain reduces the need for manual intervention, streamlines transactions, and eliminates redundant processes. This efficiency leads to cost savings, faster transaction processing, and improved overall productivity.

6. Trust and Accountability: Blockchain technology enables trust and accountability by providing a transparent and auditable record of transactions. The decentralized and consensus-driven nature of blockchain ensures that all participants reach agreement on the validity of transactions, reducing the need for trust in intermediaries. Additionally, smart contracts automatically enforce predefined rules and conditions, ensuring accountability and eliminating the risk of fraudulent activities.

These key features of blockchain make it an attractive solution for various industries, including finance, supply chain management, healthcare, and more. In the next section, we will explore the benefits that blockchain technology offers to businesses and organizations.

Benefits of Blockchain Technology

Blockchain technology offers a wide range of benefits that have the potential to transform industries and revolutionize business processes. Let’s take a closer look at some of the key advantages of adopting blockchain technology:

1. Enhanced Security: Blockchain provides a high level of security through its decentralized and immutable nature. The use of cryptographic algorithms ensures that data stored on the blockchain is protected from unauthorized access and tampering. This increased security reduces the risk of fraud, data breaches, and identity theft.

2. Increased Transparency: Blockchain brings transparency to transactions and operations by maintaining a shared and immutable ledger. All participants in the network have access to the same information, ensuring transparency and fostering trust among stakeholders. Real-time auditing and verification of transactions can be easily achieved, reducing the need for intermediaries.

3. Improved Efficiency and Cost Savings: Blockchain eliminates the need for intermediaries, streamlines processes, and automates trust through smart contracts. This results in faster transaction processing, reduced paperwork, and minimal manual intervention. By removing intermediaries, businesses can achieve cost savings and operational efficiency.

4. Enhanced Traceability and Accountability: Blockchain enables end-to-end traceability of transactions, products, and assets. Each transaction is recorded on the blockchain and is immutable, creating a transparent audit trail. This feature is especially beneficial in industries like supply chain management, where it is crucial to track and verify the origins and movement of goods.

5. Decentralization and Resilience: The decentralized nature of blockchain makes it resilient to failures and attacks. As the ledger is maintained across multiple nodes, there is no single point of failure. This ensures that the data and operations remain accessible even in the face of network disruptions or malicious attacks.

6. Improved Trust and Reduced Fraud: By eliminating the need for trust in intermediaries, blockchain technology enhances trust among participants. The transparent and tamper-proof nature of blockchain reduces the risk of fraud, as every transaction is recorded on the blockchain and can be verified by all participants. This benefit is particularly valuable in industries like finance and healthcare.

7. Potential for Innovation: Blockchain technology has opened up new possibilities for innovation and disruption across industries. With its decentralized, secure, and transparent framework, blockchain provides a fertile ground for developing novel applications and business models. Startups and established organizations alike can leverage blockchain to create innovative solutions and gain a competitive advantage.

As the potential of blockchain technology continues to be explored and harnessed, it is clear that its benefits extend far beyond traditional systems. The next section will delve into some real-world use cases of blockchain technology, demonstrating its applicability in various industries.

Use Cases of Blockchain

Blockchain technology has gained significant traction across various industries, presenting numerous real-world use cases. Let’s explore some of the industries and sectors where blockchain is being implemented:

1. Financial Services: Blockchain is revolutionizing the financial sector by enabling secure and efficient transactions. It facilitates faster cross-border payments, eliminates the need for intermediaries in remittances, and reduces fraud through transparent and auditable transaction records. Blockchain also holds the potential to simplify identity verification, streamline Know Your Customer (KYC) processes, and enable decentralized lending and peer-to-peer transactions.

2. Supply Chain Management: Blockchain enhances transparency and traceability in supply chains by providing an immutable and auditable record of every transaction and movement of goods. This increased visibility helps to prevent counterfeit products, ensure product authenticity, and improve inventory management. By tracking and verifying the origins of goods, blockchain can aid in ethical sourcing and fair trade practices.

3. Healthcare: Blockchain introduces a secure and interoperable platform for managing healthcare data. It enables patients to have control over their medical records, ensures privacy and security of sensitive health information, and facilitates better sharing of patient data among healthcare providers. Blockchain can also aid in the verification of the authenticity of drugs, enable clinical trials and research collaborations, and streamline insurance claim processing.

4. Real Estate: Blockchain has the potential to revolutionize the real estate industry by introducing transparency, efficiency, and improved security. It can facilitate the streamlined transfer of property ownership, reduce the need for intermediaries like lawyers and brokers, and eliminate fraudulent practices. Smart contracts on the blockchain can automate and enforce property agreements, ensuring transparency and reducing the risk of disputes.

5. Voting and Governance: Blockchain offers a secure and transparent platform for voting and governance systems. It can enhance the integrity of elections by ensuring that votes are accurately recorded and cannot be tampered with. Blockchain-based governance models enable decentralized decision-making and greater participation of stakeholders, reducing the risk of corruption and manipulation.

6. Intellectual Property: Blockchain can assist in the protection of intellectual property rights by recording and timestamping the creation and ownership of digital assets. This decentralized and tamper-proof ledger ensures the authenticity and provenance of creative works, thereby reducing infringement and providing a fair platform for artists and creators to monetize their creations.

These are just a few examples of the numerous industries and sectors where blockchain technology is making significant strides. As the technology continues to mature, more innovative and impactful use cases are being explored and implemented.

Conclusion

Blockchain technology is a game-changer that is transforming industries and revolutionizing the way we conduct transactions and store data. Its decentralized, transparent, and secure nature provides countless benefits across various sectors.

Blockchain offers enhanced security by utilizing cryptographic algorithms, ensuring the integrity of data, and preventing unauthorized access or tampering. The transparency of the technology fosters trust among participants, enabling real-time auditing and verification of transactions. Additionally, blockchain technology improves efficiency and reduces costs by eliminating intermediaries and streamlining processes.

The immutability of blockchain ensures that once a transaction is recorded, it cannot be altered or deleted. This feature has profound implications for industries such as supply chain management, where traceability and authenticity are of utmost importance.

Furthermore, blockchain technology empowers individuals by giving them control over their data and assets. It enables peer-to-peer transactions and eliminates the need for trust in intermediaries by utilizing smart contracts. This has implications for various sectors, including finance, where blockchain enables faster and more secure cross-border payments.

Real-world use cases of blockchain technology are already being implemented across industries such as finance, supply chain management, healthcare, and more. As the technology continues to evolve, the possibilities for innovative applications are endless.

However, it is important to recognize that blockchain technology is not a one-size-fits-all solution. It is crucial for businesses and organizations to carefully analyze their specific needs and assess whether blockchain aligns with their goals and requirements.

As we move forward, it will be fascinating to witness the continued advancement of blockchain technology and its widespread adoption. With its potential to enhance security, transparency, efficiency, and trust in various industries, the future of blockchain is undoubtedly promising.

So, brace yourself for a world where trust is decentralized, transactions are secure, and data is transparent – welcome to the era of blockchain!