Introduction:

Welcome to the world of Fintech credit cards! In today’s digital age, the finance industry has been revolutionized by the emergence of modern technologies. One such innovation is the advent of Fintech credit cards, which combine the convenience of traditional credit cards with cutting-edge financial technology.

Fintech credit cards are a new breed of credit cards that leverage technology to provide users with a seamless and user-friendly experience. These cards are issued by financial technology companies, known as Fintech companies, and offer a range of benefits and features that set them apart from traditional credit cards.

With Fintech credit cards, users can enjoy a host of advantages, such as easy application processes, enhanced security features, tailored rewards programs, and more. Additionally, these cards often come with innovative tools and online platforms that provide users with greater control over their finances, helping them manage their spending and track their transactions with ease.

Moreover, Fintech credit cards cater to the changing needs and preferences of users. They provide flexible payment options, real-time notifications, personalized spending insights, and simplified expense categorization. These features empower users to make more informed financial decisions and stay on top of their spending habits.

However, it’s important to note that Fintech credit cards may also have some potential drawbacks, such as limited acceptance at certain establishments or higher interest rates. Therefore, it’s crucial for individuals to assess their financial goals and needs before choosing a Fintech credit card.

In this article, we’ll delve deeper into the world of Fintech credit cards, exploring the definition, functionality, advantages, and disadvantages of these cutting-edge financial instruments. We’ll also highlight some of the popular Fintech credit card providers and provide tips on how to choose the right card for your specific needs. So, let’s embark on this journey into the fascinating realm of Fintech credit cards and discover how they can revolutionize your financial experience.

Definition of Fintech Credit Card:

A Fintech credit card is a financial product that merges the convenience and flexibility of traditional credit cards with the advancements in financial technology. It is issued by Fintech companies, which are technology-driven financial service providers aiming to enhance the customer experience and streamline financial transactions.

Unlike traditional credit cards that are typically issued by banks, Fintech credit cards are offered by companies that specialize in leveraging technology to improve financial services. These companies utilize innovative algorithms, mobile apps, and online platforms to provide users with a seamless and efficient credit card experience.

One key aspect of Fintech credit cards is the digitization of the application process. Instead of paper-based forms and lengthy approval procedures, individuals can apply for a Fintech credit card online or through a mobile app. The application process is often streamlined, providing quick decisions and instant access to virtual credit cards, while physical cards are mailed to the user’s address.

Fintech credit cards also come with advanced security features to protect users’ sensitive financial information. These may include real-time fraud detection, two-factor authentication, biometric authentication, and virtual card numbers that can be used for online purchases to safeguard against unauthorized transactions.

Furthermore, Fintech credit cards often offer personalized rewards programs tailored to users’ spending habits and preferences. By leveraging data analytics, Fintech companies can provide customers with targeted offers and incentives that align with their interests. This can range from cashback rewards on specific categories of spending, such as dining or travel, to loyalty points that can be redeemed for various benefits.

Another distinguishing feature of Fintech credit cards is the user-friendly interfaces and online platforms that accompany them. These tools allow users to manage their credit card accounts digitally, offering features such as balance monitoring, transaction categorization, spending insights, and the ability to set budget limits and receive real-time notifications.

In summary, Fintech credit cards combine the convenience of traditional credit cards with the innovative power of financial technology. They offer a user-friendly experience through digitized application processes, advanced security measures, personalized rewards programs, and intuitive online platforms. With Fintech credit cards, individuals can enjoy enhanced control over their finances and a tailored credit card experience that aligns with their needs and preferences.

How Fintech Credit Cards Work:

Fintech credit cards operate on a similar principle to traditional credit cards, allowing users to make purchases on credit and repay the borrowed amount over time. However, they incorporate digital technology to streamline the process and offer additional features that enhance the user experience.

When a user applies for a Fintech credit card, they typically follow an online or mobile application process. The applicant will need to provide personal information, such as their name, address, and income details, as well as consent to a credit check. Fintech companies leverage technology and algorithms to assess the applicant’s creditworthiness and determine their credit limit.

Once approved, the user will receive a physical credit card in the mail, along with instructions on activating it. Additionally, many Fintech credit card providers also offer virtual credit cards, which can be accessed and used immediately after the approval process. These virtual cards allow users to make online purchases before they receive the physical card.

When using a Fintech credit card for an in-person or online purchase, the transaction is processed in a similar way as with traditional credit cards. The user presents the physical card or enters the card details online, and the necessary information is transmitted securely to the payment processor for verification.

One of the advantages of Fintech credit cards is the use of advanced security features to protect against fraud. Many Fintech companies employ real-time fraud detection systems that monitor transactions for any suspicious activity. In addition, some Fintech credit cards utilize biometric authentication, such as fingerprint or facial recognition, for added security during online or mobile app transactions.

After making a purchase using a Fintech credit card, the user will receive a statement, either by email or through the online platform or mobile app. This statement outlines the transactions made during the billing period, the minimum amount due, and the due date for payment. Users can make payments towards their credit card balance either manually or set up autopay to ensure timely repayments.

Furthermore, Fintech credit cards often come with intuitive online platforms or mobile apps that allow users to manage their accounts and track their spending. These platforms provide features such as transaction categorization, spending insights, and budgeting tools, helping users gain a better understanding of their financial habits and make informed decisions.

Overall, Fintech credit cards simplify the credit card process by leveraging technology, offering features like instant virtual cards, advanced security measures, and user-friendly online platforms. By combining digital innovation with traditional credit card functionality, Fintech credit cards aim to provide a seamless and efficient credit card experience for users.

Advantages of Fintech Credit Cards:

Fintech credit cards offer several advantages over traditional credit cards, making them an attractive option for individuals seeking a more streamlined and personalized credit card experience. Here are some of the key advantages of Fintech credit cards:

1. Easy and Convenient Application Process: Fintech credit cards typically have a digital application process, allowing users to apply online or through a mobile app. This eliminates the need for extensive paperwork and lengthy approval processes, providing quick decisions and instant access to virtual credit cards. The physical card is then mailed to the user’s address.

2. Enhanced Security Measures: Fintech credit cards prioritize security by offering advanced features to protect users from fraudulent activities. These measures include real-time fraud detection systems, two-factor authentication, biometric authentication, and virtual card numbers for secure online transactions.

3. Personalized Rewards Programs: Fintech credit cards often provide tailored rewards programs based on users’ spending habits and preferences. By leveraging data analytics, these cards offer cashback rewards, loyalty points, or discounts on specific categories like dining, travel, or shopping. This allows users to maximize their rewards based on their individual preferences.

4. User-Friendly Online Platforms: Fintech credit cards come with intuitive online platforms or mobile apps that offer a range of features to assist users in managing their credit card accounts. These features may include transaction categorization, spending insights, budgeting tools, and real-time notifications. Users can easily track their spending, set budget limits, and receive alerts for any unusual activity.

5. Flexibility and Control: Fintech credit cards provide users with greater control over their finances. They offer flexible payment options, allowing users to choose between full payments, minimum payments, or custom payment amounts. Additionally, Fintech credit cards often come with tools that analyze spending patterns and provide personalized recommendations for financial management.

6. Quick and Efficient Customer Service: Fintech credit card providers typically excel in customer service, offering prompt and efficient support through online chat, email, or phone. Users can easily resolve any issues, report lost or stolen cards, or inquire about their account status, benefiting from the responsive and convenient customer service provided by Fintech companies.

7. Integration with Financial Management Tools: Many Fintech credit cards integrate with popular budgeting and financial management apps, allowing users to sync their transactions and analyze their spending alongside other accounts. This integration provides a comprehensive overview of their financial health and assists in strategic financial planning.

Overall, Fintech credit cards offer numerous advantages, including a streamlined application process, enhanced security features, personalized rewards programs, user-friendly online platforms, flexibility in payments, efficient customer service, and integration with financial management tools. These advantages cater to the needs and preferences of modern consumers, providing a seamless, convenient, and tailored credit card experience.

Potential Disadvantages of Fintech Credit Cards:

While Fintech credit cards offer numerous benefits, it’s important to consider the potential disadvantages associated with these innovative financial products. Here are some of the potential drawbacks to be aware of:

1. Limited Acceptance: Fintech credit cards may not be accepted at all establishments, as not every retailer or vendor may be equipped to process payments from these cards. This can be a limitation, particularly in certain regions or smaller businesses that have yet to adopt the necessary technology for accepting Fintech credit cards.

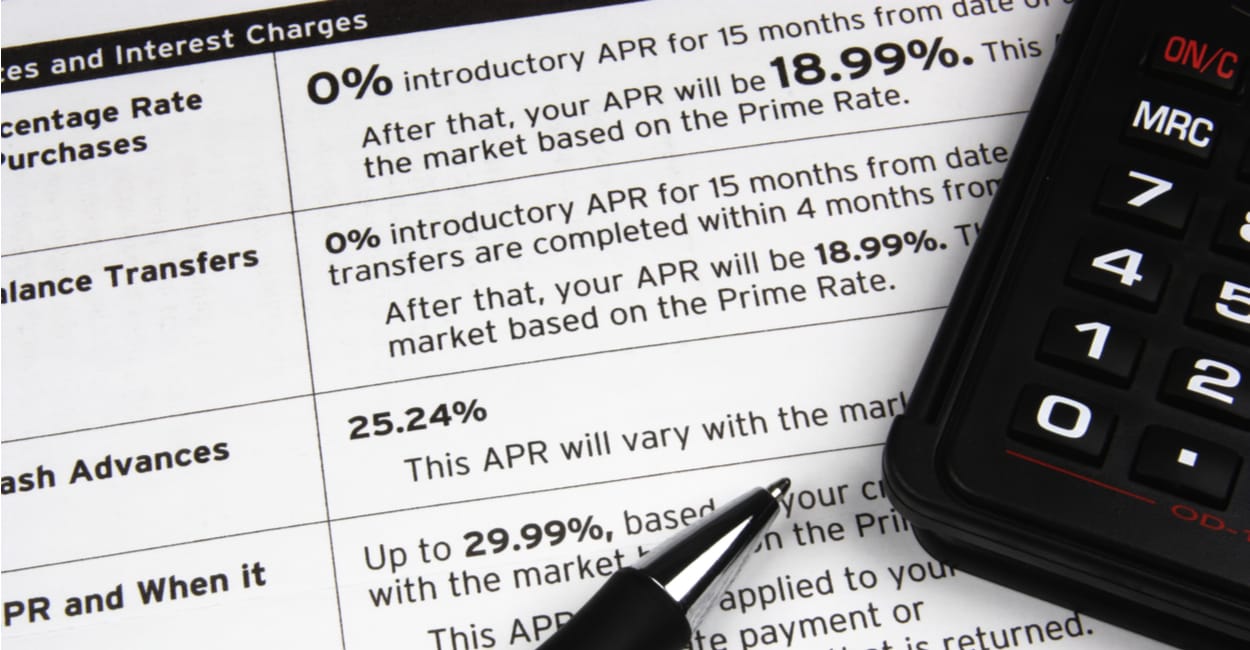

2. Higher Interest Rates: In some cases, Fintech credit cards may come with higher interest rates compared to traditional credit cards. This can be a disadvantage if users carry a balance from month to month, as the higher interest charges can accumulate and result in increased debt if not managed carefully. It’s important for individuals to review and compare the terms and interest rates of different Fintech credit cards before making a decision.

3. Potential for Technology Glitches: As Fintech credit cards heavily rely on technology, there is a possibility of encountering technical glitches or system failures. This could result in temporary disruption in accessing funds, making payments, or managing the credit card account. While such issues are typically resolved quickly, they can still cause inconvenience and disruption to users’ financial activities.

4. Potential Privacy Concerns: Fintech credit cards collect and process personal and financial data to provide personalized offers and services. Some individuals may have concerns about data privacy and the security of their information. It’s important to carefully review the privacy policies and security measures implemented by Fintech credit card providers and ensure that personal information is handled securely.

5. Limited Financial Services: Unlike traditional banks, Fintech companies may have a more limited range of financial services available. While Fintech credit cards offer convenient payment options, they may not provide other services such as loans, mortgages, or investment opportunities. This limitation may require individuals to seek additional financial services from traditional banks or other financial institutions.

6. Potential for Overspending: The ease and convenience offered by Fintech credit cards, along with personalized rewards programs, can potentially encourage overspending. Users may be tempted to make impulsive purchases or exceed their budget due to the lure of rewards. It’s crucial for individuals to maintain discipline and practice responsible financial habits to avoid accumulating debt and overspending.

7. Reliance on Technology: Fintech credit cards heavily rely on technology for various aspects, such as application processes, payment processing, and account management. This reliance on technology means that users may face challenges in situations where technology is unavailable, such as during system maintenance or network disruptions. Having a backup payment method like a traditional credit card or cash can help mitigate potential disruptions.

It’s important to note that the potential disadvantages of Fintech credit cards may vary depending on the specific provider and the individual’s financial needs and preferences. It’s advisable to thoroughly research and compare different Fintech credit card options to make an informed decision based on personal circumstances.

Popular Fintech Credit Card Providers:

The Fintech industry has witnessed the rise of several prominent companies that offer innovative and feature-rich Fintech credit cards. Here are some of the popular Fintech credit card providers:

1. Apple Card: The Apple Card, launched by Apple in partnership with Goldman Sachs, offers a seamless and integrated credit card experience for Apple device users. It provides cashback rewards, daily cash, and a user-friendly mobile app that allows users to manage their card, track spending, and receive detailed transaction insights.

2. Brex: Brex is a Fintech company that caters to startups and small businesses, offering a corporate credit card designed to meet their unique needs. With streamlined expense management, higher credit limits, and tailored rewards for business-related spending, Brex has become a popular choice among entrepreneurs for managing their finances.

3. Square’s Cash Card: Square, known for its payment processing solutions, offers the Cash Card, a Fintech credit card that links directly to the user’s Cash App account. It provides real-time rewards, enables peer-to-peer payments, and offers a boost feature, which provides discounts at select merchants.

4. SoFi Credit Card: SoFi, a leading Fintech company, offers a range of financial products, including Fintech credit cards. The SoFi Credit Card provides cashback rewards, no annual fees, and the option to redeem rewards towards paying down student loans or investing through SoFi’s platform. It also offers various member benefits and a user-friendly mobile app for easy management.

5. Chase Sapphire Reserve: Although not exclusively a Fintech company, Chase has ventured into the Fintech space with its Sapphire Reserve credit card. This premium travel credit card offers a range of travel benefits, including airport lounge access, travel credits, and lucrative rewards. The Chase Sapphire Reserve combines traditional banking services with modern Fintech features.

6. Capital One Venture: Capital One is known for its Fintech-driven approach to banking, and the Capital One Venture credit card reflects this mentality. It offers generous travel rewards, flexible redemption options, and a user-friendly mobile app that provides comprehensive account management features.

7. Revolut: With its digital banking services, Revolut has become a prominent player in the Fintech industry. Revolut’s credit card offers global acceptance, low foreign transaction fees, and rewards for spending. It also provides budgeting tools, spending analytics, and other Fintech features to help users manage their finances effectively.

These are just a few examples of popular Fintech credit card providers, but the Fintech landscape continues to evolve, with new players constantly entering the market. It’s important for individuals to research different providers, compare their offerings, and evaluate which Fintech credit card aligns best with their unique financial needs and preferences.

What Sets Fintech Credit Cards Apart from Traditional Credit Cards:

Fintech credit cards have gained significant popularity due to the unique features and advantages they offer to users compared to traditional credit cards. Here are some key factors that set Fintech credit cards apart:

1. Digital Integration: Fintech credit cards are designed to seamlessly integrate with digital platforms and technology. They often come with user-friendly mobile apps or online platforms that provide advanced account management features, real-time transaction notifications, and spending insights. This digital integration enhances the user experience and empowers individuals to have better control over their finances.

2. Streamlined Application Process: Fintech credit cards offer a digital and streamlined application process. Users can apply online or through a mobile app, eliminating the need for extensive paperwork and waiting times. Fintech companies utilize innovative algorithms and technology to assess creditworthiness quickly, providing users with instant access to virtual credit cards and speeding up the entire application and approval process.

3. Advanced Security Measures: Fintech credit cards prioritize security and employ advanced security measures beyond the industry standard. These measures may include real-time fraud detection systems, two-factor authentication, biometric authentication, and virtual card numbers that enhance security during online transactions. By leveraging technology, Fintech credit card providers strive to protect users against unauthorized transactions and ensure the security of their personal and financial information.

4. Tailored Rewards Programs: Fintech credit cards often offer personalized rewards programs based on users’ spending habits and preferences. Leveraging data analytics, these cards provide targeted offers, cashback rewards, loyalty points, or discounts on specific categories like dining, travel, or shopping. This customization allows individuals to earn rewards that align closely with their interests and maximize the value of their spending.

5. Enhanced Financial Management Tools: Fintech credit cards come with intuitive online platforms or mobile apps that offer comprehensive financial management tools. These tools include transaction categorization, spending analysis, and budgeting features that empower users to better understand their financial habits. They can set budget limits, receive real-time notifications, and gain insights into their spending patterns, promoting responsible financial management.

6. Flexibility and Innovation: Fintech credit cards are known for their flexibility and innovative features. They often offer flexible payment options, including the ability to customize payment amounts or choose from alternative payment plans. Fintech companies are constantly exploring new technologies and features to enhance the credit card experience, such as digital receipts, card-linked offers, or voice-activated commands.

7. Effortless Integration with Other Financial Services: Fintech credit cards seamlessly integrate with other financial services provided by the same Fintech companies. This allows individuals to access a range of services from a single platform, such as budgeting tools, savings accounts, investment options, or loans. The integration of various financial services simplifies financial management and provides users with a holistic approach to structuring their finances.

Overall, Fintech credit cards offer a range of features and advantages that distinguish them from traditional credit cards. With their digital integration, streamlined application processes, advanced security measures, tailored rewards programs, financial management tools, flexibility, and integration with other financial services, Fintech credit cards aim to provide users with a modern, convenient, and personalized credit card experience.

Tips for Choosing the Right Fintech Credit Card:

With the plethora of Fintech credit card options available, it’s important to consider several factors before choosing the one that best suits your financial needs and lifestyle. Here are some tips to help you make an informed decision:

1. Assess Your Spending Habits: Take a moment to evaluate your typical spending patterns and identify the categories where you spend the most. Look for Fintech credit cards that offer rewards or benefits tailored to your spending habits, such as cashback on groceries or travel rewards if you frequently fly.

2. Analyze Fees and Interest Rates: Carefully review the fees associated with Fintech credit cards, including annual fees, late payment fees, and foreign transaction fees. Additionally, compare the interest rates offered by different providers, especially if you anticipate carrying a balance on your credit card. Choose a card with reasonable fees and competitive interest rates.

3. Consider Security Features: Security is paramount when it comes to credit cards. Look for Fintech credit cards that offer advanced security measures, such as real-time fraud detection systems, two-factor authentication, and biometric authentication. Ensure the Fintech provider has a strong track record of data protection and follows industry-standard security protocols.

4. Evaluate Rewards and Benefits: Compare the rewards programs and benefits offered by different Fintech credit cards. Look for cards that align with your interests and provide the most value to you. Consider factors such as the value of the rewards, redemption options, expiration dates, and any restrictions or limitations on earning or redeeming rewards.

5. Review the Mobile App or Online Platform: Fintech credit cards typically come with a mobile app or online platform for account management. Evaluate the features and functionality of these platforms, such as transaction categorization, spending insights, and budgeting tools. Choose a Fintech credit card with an intuitive and user-friendly app or platform that provides the tools you need to manage your finances effectively.

6. Research Customer Reviews and Ratings: Read customer reviews and ratings of the Fintech credit cards you are considering. Look for feedback on customer service, ease of use, rewards programs, and any potential issues or limitations. This can give you insights into the experiences of other users and help you make an informed decision.

7. Consider Additional Financial Services: Some Fintech credit card providers offer a range of additional financial services, such as savings accounts, investments, or loans. If you are interested in integrating multiple financial services into one platform, consider Fintech companies that offer a comprehensive suite of services that align with your long-term financial goals.

8. Compare Providers: Take the time to compare different Fintech credit card providers and their offerings. Consider factors such as reputation, track record, customer support, and overall user experience. Look for providers that have a strong presence in the Fintech industry and are known for their innovative approach and customer-centric services.

By considering these tips, you can narrow down your options and choose the Fintech credit card that best meets your needs. Remember to prioritize factors such as rewards, security, fees, and functionality to find the ideal card that aligns with your financial goals and lifestyle.

Conclusion:

Fintech credit cards have revolutionized the way individuals manage their finances and make purchases. With their seamless integration of technology, advanced security features, personalized rewards programs, and user-friendly interfaces, Fintech credit cards offer a range of advantages over traditional credit cards.

These innovative financial products provide a convenient and efficient credit card experience by leveraging digital platforms, streamlining application processes, and offering enhanced security measures. Users can benefit from tailored rewards programs, access user-friendly online platforms, and receive real-time notifications, empowering them to make more informed financial decisions and take control of their spending.

However, it’s important to note some potential drawbacks, such as limited acceptance at certain retailers, higher interest rates, and potential privacy concerns. Individuals must carefully consider their spending habits, evaluate fees and interest rates, review security features, and compare different Fintech credit card providers before making a decision.

Popular Fintech credit card providers like Apple Card, Brex, Square’s Cash Card, SoFi Credit Card, Chase Sapphire Reserve, Capital One Venture, and Revolut offer a variety of unique features and benefits. It’s crucial to assess personal preferences and financial needs to choose the right Fintech credit card that aligns with one’s lifestyle.

By following some key tips, such as assessing spending habits, analyzing fees and interest rates, considering security features, evaluating rewards and benefits, reviewing mobile apps or online platforms, researching customer reviews, and comparing providers, individuals can make an informed decision and select the Fintech credit card that best suits their requirements.

Ultimately, Fintech credit cards have changed the landscape of the credit card industry, providing individuals with greater convenience, security, and personalization. As technology continues to evolve, Fintech credit cards are expected to become even more sophisticated and tailored to users’ needs, further enhancing the financial experience and empowering individuals to achieve their financial goals.