Introduction

When it comes to the lending process, one crucial factor that lenders consider is the borrower’s creditworthiness. The creditworthiness of an individual is typically assessed using a credit scoring system. Among the various credit scoring models available, the FICO Score has gained significant prominence and recognition.

The FICO Score is a widely used credit scoring system that determines an individual’s creditworthiness based on their credit history. It provides lenders with a standardized evaluation of a borrower’s credit risk, helping them make informed decisions when extending credit.

Understanding the role of the FICO Score in the lending process is vital, as it can significantly impact one’s ability to secure loans, mortgages, and other forms of credit. It is essential to have a clear understanding of how lenders utilize this credit scoring model, the percentage of lenders that use it, and any potential alternatives that exist.

This article will delve into the significance of credit scores in the lending process, how lenders utilize credit scores, factors considered by lenders apart from the FICO Score, the percentage of lenders using the FICO Score, as well as the benefits and criticisms associated with its use. Additionally, alternative credit scoring models will be explored to provide a comprehensive view of the current landscape.

What is the FICO Score?

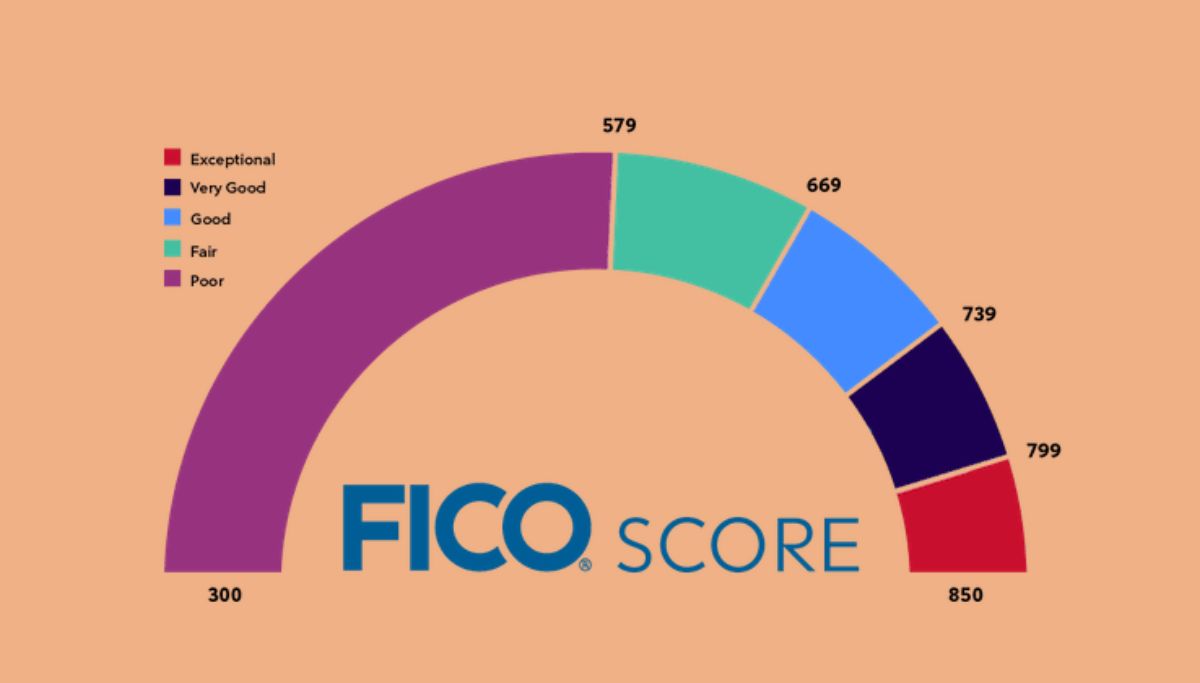

The FICO Score is a credit scoring model that is widely used by lenders to assess the creditworthiness of individuals. It was introduced by the Fair Isaac Corporation (FICO), a data analytics company, in the 1980s. The FICO Score ranges from 300 to 850 and is calculated based on various factors in a person’s credit history.

The FICO Score takes into account factors such as payment history, credit utilization, length of credit history, types of credit used, and the presence of any derogatory marks. Each factor carries a different weightage, and the final score is a reflection of an individual’s credit risk.

Lenders evaluate FICO Scores to determine the likelihood of a borrower repaying their debts responsibly. A higher FICO Score indicates a lower credit risk, making it more likely for individuals to be approved for credit and obtain favorable terms, such as lower interest rates.

It is important to note that there are multiple versions of the FICO Score, with the most widely used being FICO Score 8. However, newer versions, such as FICO Score 9 and FICO Score 10, have been introduced to provide a more accurate assessment of creditworthiness.

The FICO Score has become an industry standard and is used by a wide range of lenders, including banks, credit unions, mortgage companies, and credit card issuers. It serves as a benchmark for evaluating the creditworthiness of borrowers and plays a crucial role in the lending decision-making process.

Overall, the FICO Score is a well-established credit scoring model that provides lenders with a standardized way to assess an individual’s creditworthiness. Understanding how the FICO Score is calculated and utilized by lenders is essential for borrowers who aim to improve their creditworthiness and secure favorable credit terms.

The Importance of Credit Scores in the Lending Process

In the lending process, credit scores play a crucial role in determining whether individuals are eligible for credit and what terms they will be offered. Lenders heavily rely on credit scores to assess an individual’s creditworthiness and decide whether to approve a loan application.

Credit scores provide lenders with a quick and standardized way to evaluate the credit risk associated with a borrower. It allows them to gauge an individual’s likelihood of repaying their debts based on their past credit behavior.

One of the key benefits of credit scores is that they help lenders make informed decisions efficiently. Instead of manually reviewing each applicant’s credit history, credit scores simplify the evaluation process by providing a numerical representation of creditworthiness.

Furthermore, credit scores allow lenders to set appropriate terms and conditions for credit products. Individuals with higher credit scores are generally offered lower interest rates and favorable loan terms, while those with lower credit scores may face higher interest rates or even be denied credit altogether.

Credit scores also promote fairness in the lending process. By using objective criteria to assess creditworthiness, credit scores ensure that lending decisions are based on the individual’s credit history rather than subjective factors.

Another important aspect is that credit scores provide borrowers with a benchmark to understand their creditworthiness. By knowing their credit score, individuals can assess their chances of obtaining credit and take steps to improve their credit standing if needed.

In summary, credit scores are of paramount importance in the lending process. They provide lenders with a standardized way to evaluate credit risk, enable efficient decision-making, ensure fair treatment of borrowers, and offer borrowers valuable insights into their creditworthiness. Understanding the significance of credit scores can help individuals navigate the lending process more effectively and take measures to improve their credit standing.

How Lenders Use Credit Scores

Lenders use credit scores as a key tool in the lending process to assess the creditworthiness of borrowers. They play a pivotal role in determining whether a borrower will be approved for credit and what terms and interest rates will be offered. Here’s a breakdown of how lenders utilize credit scores:

- Initial screening: Lenders often use credit scores to conduct an initial evaluation of loan applications. They set a minimum credit score requirement, and applicants below that threshold may be automatically disqualified.

- Risk assessment: Credit scores help lenders assess the risk associated with lending money to a particular individual. A higher credit score suggests a lower credit risk, indicating that the borrower is more likely to repay their debts on time.

- Loan approval: Lenders use credit scores to determine whether to approve or decline a loan application. A higher credit score increases the chances of loan approval, while a lower credit score may result in rejection or require additional documentation and scrutiny.

- Interest rates: Credit scores influence the interest rates offered to borrowers. Individuals with higher credit scores are generally offered lower interest rates, reflecting their lower credit risk. On the other hand, borrowers with lower credit scores may face higher interest rates to compensate for the perceived higher risk.

- Loan terms: The terms of the loan, such as the loan amount, repayment period, and associated fees, may also be influenced by credit scores. Lenders may offer more favorable terms to borrowers with higher credit scores, while those with lower scores may face stricter terms or limitations.

- Limit decisions: Credit scores may impact the credit limits granted to individuals, especially for credit cards and lines of credit. A higher credit score may result in a higher credit limit, providing borrowers with more financial flexibility, while lower scores may lead to lower limits.

- Account approvals: In addition to loans, credit scores are considered when approving applications for credit cards, mortgages, auto loans, and other credit products. Lenders rely on credit scores to assess the risk associated with these accounts and to determine whether to approve or deny applications.

Overall, credit scores serve as a vital tool for lenders in evaluating creditworthiness and making informed lending decisions. By considering credit scores, lenders can mitigate risks, offer appropriate terms and interest rates, and ensure responsible lending practices.

Factors Considered by Lenders Apart from the FICO Score

While the FICO Score is a significant factor in the lending process, lenders also consider additional factors to assess an individual’s creditworthiness. These factors provide lenders with a more comprehensive view of the borrower’s financial profile and help them make informed lending decisions. Here are some of the key factors considered by lenders aside from the FICO Score:

- Income and employment history: Lenders evaluate the borrower’s income level and stability of employment to assess their ability to repay the loan. A steady income source and a reliable employment history indicate financial stability and increase the likelihood of loan approval.

- Debt-to-Income ratio (DTI): The DTI ratio measures the borrower’s monthly debt payments against their gross monthly income. Lenders consider this ratio to assess the borrower’s ability to handle additional debt responsibly. A lower DTI ratio indicates a healthier financial position.

- Payment history: Lenders review the borrower’s payment history, looking for past delinquencies, late payments, or instances of default. Consistent, on-time payments demonstrate responsible financial behavior and increase the borrower’s creditworthiness.

- Credit utilization: Lenders analyze the borrower’s credit utilization ratio, which measures the amount of available credit being utilized. A lower credit utilization ratio indicates responsible credit management and improves the borrower’s creditworthiness.

- Credit history length: The length of the borrower’s credit history is also considered by lenders. A longer credit history provides more data points for evaluation, giving lenders a clearer picture of the borrower’s credit behavior and ability to handle debt.

- Recent credit inquiries: Lenders examine the borrower’s recent credit inquiries to assess their recent credit-seeking activities. Multiple recent credit inquiries may raise concerns about the borrower’s financial stability or potential overextension of credit.

- Public records: Lenders consider public records such as bankruptcies, tax liens, and civil judgments when evaluating creditworthiness. Negative public records can significantly impact a borrower’s creditworthiness.

By considering these additional factors alongside the FICO Score, lenders can obtain a more comprehensive understanding of the borrower’s financial situation and credit behavior. This holistic assessment helps lenders make more informed lending decisions and ensures responsible lending practices.

The Percentage of Lenders Using FICO Score

The FICO Score is widely recognized and used by lenders across various industries. It has become the industry standard for evaluating creditworthiness and aiding lending decisions. While the exact percentage of lenders using the FICO Score may vary, it is estimated that a significant majority of lenders rely on this credit scoring model.

According to a report by the Consumer Financial Protection Bureau (CFPB), around 90% of top lenders in the United States use the FICO Score to assess consumer creditworthiness. This includes mortgage lenders, credit card issuers, auto loan providers, and other major financial institutions.

The dominance of the FICO Score can be attributed to several factors, including its longevity, widespread use, and the FICO brand’s credibility. The consistent methodology and proven track record of the FICO Score provide lenders with a reliable and trusted tool to evaluate credit risk.

Furthermore, the FICO Score is often favored by lenders due to its simplicity and easy integration into their existing systems. The familiarity and widespread adoption of the FICO Score make it more efficient for lenders to evaluate credit applications and make consistent lending decisions.

However, it is important to note that while the FICO Score is prevalent, there are also lenders who utilize alternative credit scoring models or develop their own proprietary scoring systems. This allows them to consider additional factors or customize the scoring model to align with their specific lending criteria.

Additionally, the use of alternative credit scoring models has gained traction in recent years, aiming to provide a more inclusive evaluation of creditworthiness by considering factors beyond traditional credit history. These models may incorporate data such as rental payments, utility bill payments, or banking transaction history to assess creditworthiness for individuals with limited credit history.

Despite the presence of alternative credit scoring models, the FICO Score remains the leading credit scoring model used by the majority of lenders. Its widespread adoption and established reputation make it a crucial factor in the loan approval process for many borrowers.

Overall, while the specific percentage of lenders using the FICO Score may vary, it is safe to say that a substantial number of lenders rely on this credit scoring model to assess creditworthiness and make lending decisions.

Benefits and Criticisms of Using FICO Score in the Lending Process

The use of the FICO Score in the lending process has both advantages and disadvantages. Let’s examine some of the benefits and criticisms associated with using the FICO Score:

Benefits:

- Standardization: The FICO Score provides a standardized measure of creditworthiness, allowing lenders to make consistent and reliable lending decisions. It offers a uniform evaluation system that is easily understood by both lenders and borrowers.

- Efficiency: The FICO Score streamlines the loan application process by providing a quick and automated assessment of credit risk. This efficiency enables lenders to make prompt decisions and borrowers to receive timely approvals or rejections.

- Predictive Power: Over the years, the FICO Score has demonstrated its predictive power in assessing credit risk. Lenders trust its accuracy in evaluating the likelihood of borrowers repaying their debts, which helps in reducing default rates and managing overall lending risk.

- Proven Validity: The FICO Score has been widely tested and validated over time, making it a reliable and trusted credit scoring model. Its long-standing reputation provides lenders and borrowers with confidence in its ability to assess creditworthiness accurately.

- Standardization: The FICO Score provides a standardized measure of creditworthiness, allowing lenders to make consistent and reliable lending decisions. It offers a uniform evaluation system that is easily understood by both lenders and borrowers.

Criticisms:

- Lack of Comprehensive Assessment: The FICO Score primarily focuses on credit history and does not consider other factors that may influence a borrower’s creditworthiness, such as income, employment stability, or personal circumstances. Critics argue that a more holistic assessment may provide a more accurate representation of a borrower’s ability to repay debts.

- Potential for Bias: Some critics argue that the FICO Score may be biased and may perpetuate systemic inequalities. Factors such as past delinquencies or collections may disproportionately impact individuals from marginalized communities, leading to unfair credit evaluations.

- Limited Adaptability: The FICO Score has undergone updates over the years, but it may not always reflect evolving consumer behaviors or financial practices accurately. Critics suggest that there is a need for more agile credit scoring models that can adapt to changing financial landscapes and consider alternative data sources.

- Focus on Historical Data: The FICO Score primarily relies on past credit behavior, which may not fully capture an individual’s current financial situation or ability to repay debts. Critics argue that a more forward-looking assessment that factors in real-time financial data could provide a more accurate evaluation.

- Exclusion of Thin-File and Credit Invisible Consumers: The FICO Score heavily depends on credit history, making it challenging for individuals with limited credit history, such as young adults or recent immigrants, to establish creditworthiness. This can result in them being excluded from credit opportunities or facing higher interest rates.

While the FICO Score offers a standardized and widely recognized evaluation of creditworthiness, it is crucial to acknowledge the criticisms surrounding its limitations. The ongoing discussion about alternative credit scoring models aims to address some of these concerns and provide more inclusive and comprehensive assessments of borrowers’ creditworthiness.

Alternative Credit Scoring Models

While the FICO Score remains dominant in the lending industry, alternative credit scoring models have emerged in recent years. These models aim to provide a more inclusive and nuanced evaluation of creditworthiness by considering additional factors beyond traditional credit history. Here are a few notable alternative credit scoring models:

VantageScore:

VantageScore is a credit scoring model introduced by the three major credit bureaus – Equifax, Experian, and TransUnion. It utilizes similar factors to the FICO Score but may weigh them differently. VantageScore models, such as VantageScore 3.0 and VantageScore 4.0, provide lenders with an alternative perspective on creditworthiness.

Experian Boost:

Experian Boost is a program introduced by Experian, one of the major credit reporting agencies. It allows individuals to add non-traditional payment data, such as utility bill payments and cellphone payments, to their credit reports. This additional information can positively impact credit scores, especially for individuals with limited credit history.

UltraFICO Score:

The UltraFICO Score, developed by FICO in collaboration with Experian and Finicity, considers banking transaction history in addition to traditional credit data. It allows individuals to voluntarily authorize access to their banking information to demonstrate responsible financial behavior and potentially improve their credit scores.

Alternative Data Models:

Various companies are implementing alternative data models that incorporate non-traditional data sources to assess creditworthiness. These sources may include rental payment history, education records, employment history, and public records. By considering a broader range of data, these models aim to provide credit access to consumers with limited credit histories or who have been underserved by traditional credit scoring models.

Machine Learning and Artificial Intelligence Models:

Advancements in machine learning and artificial intelligence have led to the development of credit scoring models that utilize complex algorithms to analyze vast amounts of data. These models can identify patterns and correlations to assess creditworthiness in a more dynamic and adaptive manner. Machine learning models can incorporate alternative data sources and quickly adapt to changes in consumer behavior and financial trends.

While these alternative credit scoring models have gained attention and recognition, they are not yet as widely adopted as the FICO Score. However, their emergence highlights the growing efforts to create more inclusive, diverse, and accurate methods for evaluating creditworthiness. The ongoing development and adoption of alternative credit scoring models contribute to a more comprehensive assessment of borrowers’ credit profiles and financial capabilities.

Conclusion

The FICO Score has established itself as the leading credit scoring model used by a majority of lenders in the lending process. It provides lenders with a standardized and efficient way to assess an individual’s creditworthiness, enabling them to make informed lending decisions and set appropriate terms and interest rates. However, there are both benefits and criticisms associated with the use of the FICO Score.

On one hand, the FICO Score offers standardization, efficiency, and proven validity. It simplifies the loan application process, provides a reliable assessment of credit risk, and allows for consistent lending decisions. Lenders rely on the FICO Score to predict the likelihood of borrowers repaying their debts and mitigate lending risks.

On the other hand, criticisms of the FICO Score include its limited scope, potential biases, and reliance on historical data. Critics argue that a more comprehensive assessment, considering factors beyond credit history, could provide a more accurate evaluation of creditworthiness. There is also a call for alternative credit scoring models that adapt to changing financial landscapes, consider alternative data sources, and address the needs of thin-file and credit invisible consumers.

Alternative credit scoring models, such as VantageScore, Experian Boost, and UltraFICO Score, have emerged to provide alternative perspectives on creditworthiness. These models incorporate additional factors, such as non-traditional payment data and banking transaction history, to offer a more inclusive and nuanced evaluation of credit risk. Additionally, machine learning and artificial intelligence models contribute to the development of adaptive and dynamic credit scoring approaches.

In conclusion, while the FICO Score remains widely used in the lending process, the emergence of alternative credit scoring models reflects ongoing efforts to improve and diversify credit evaluations. The future of credit scoring may involve a combination of traditional credit data, alternative data sources, and advanced analytics to provide lenders with a comprehensive understanding of borrowers’ creditworthiness and support fair and responsible lending practices.